Editor’s note: Seeking Alpha is proud to welcome Andre Geraldes as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Jarretera/iStock Editorial via Getty Images

Rubis (OTCPK:RBSFY)(OTCPK:RUBSF) appears to be, even using conservative estimations, a great stock to have in a diversified portfolio. My assessment of fair value is in the high 30s €. I believe the COVID-19 issues, together with management’s decision to enter the renewables area (creating a possible dividend cut fear), drove prices to a level where there’s a possibility of interesting returns and a large margin of safety.

The business currently ticks most of Bill Ackman’s investment checklist: Rubis is predictable, in a strong position, has proven management with equity, has limited risk exposure, and is cash flow generative while trading at an attractive valuation. I view the recent focus on some long-term trends, like hydrogen and solar energy, as a positive sign. Their presence in niche markets, spread between developing and developed markets where larger players look away, proved interesting and continues to provide opportunities to grow and expand into other adjacent areas. If maintained, the eye-catching dividend should be beneficial in anchoring the stock price during a recession, and providing some dividend returns while the share price lags the true perceived value.

While the case is mostly positive, Rubis’ core business is focused on distributing oil and gas products that provide low returns on equity and invested capital, even though their exposure to price fluctuations of the input commodities is low. The low double-digit ROE added to a 2/3 payout ratio damages growth opportunities. That, together with potential profitability impacts from the new renewables department, present my main concerns for the future. The possibility of a dividend cut must also be considered, as this might translate into another sellout, since they might need additional capital to expand the capital-intensive renewable business. It’s worth mentioning that management canceled the possibility of having the dividend in newly issued shares because of depressed stock prices, and even did their first buyback, preventing current shareholders from further dilution.

Analyzing the business through the categories of legendary former Magellan Fund manager Peter Lynch, I believe Rubis narrowly fits into the “Stalwart” category, with some risk of falling into the disliked “Slow Growth” category.

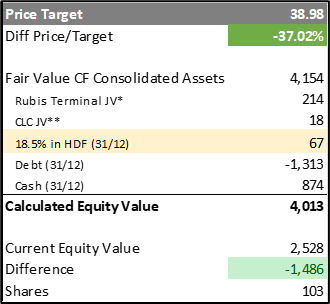

Rubis DCF approach (Rubis Annual Report)

Business

Rubis’ activity is currently focused on distributing and trading oil and gas products in the form of LPG cylinders, vehicle fuels through service stations, aviation fuels, bitumen, and others. These activities are divided between the areas that provide the retail and marketing and the areas that provide support to the mentioned operations – like shipping, refining, and logistics. As per the company’s latest annual report, both areas were the sole providers of consolidated earnings with a 70% and 30% EBIT split, respectively.

After the acquisition of the majority position in Photosol, a new division of renewables was created to include the photovoltaic business and HDF Energy’s position. This division is expected to have minimal EBITDA impact in 2022, but it is intended to increase significantly to 25% in the medium term. Plans to leverage Rubis’ international footprint are already in motion, with one example being the new Caribbean green hydrogen project that combines SARA refinery (core business), HDF (hydrogen), and solar (Photosol). Additional synergies can be expected.

The fourth and last division includes the joint venture named Rubis Terminal, which separated from the core areas after the sale of a 45% stake to Squared Capital Fund to bolster financial flexibility and future growth. The JV stores and handles liquid products that range from agricultural and oil products to chemical and petrochemical derivatives in France, Spain, Netherlands, and Belgium. Rubis consolidates Rubis Terminal through the equity method, thus the investment is accounted for in the balance sheet and the profit separately in the P&L. That also means that the significant debt is off-balance sheet (5x net debt/EBITDA).

Rubis’ strategy is focused on delivering and fulfilling the energy needs of individuals and professionals alike in the markets where they are present.

Competitors, competitive advantages, and barriers to entry

Competition in these sectors is vast and diverse since the final product is similar or even equal among competitors in the industry. As such, the focus must be on the distribution network and providing it in the cheapest way possible. In my opinion, the competitive advantages of Rubis lay in the efficient scale present in their “small” markets together with their refineries, services stations, agents, and resellers. When combined with heavy regulation, that provides some “moat.” The fact that most of the geographies have a small potential market benefits them in discouraging large investments from new competitors, creating the so-called oligopolies.

Most of the markets where Rubis is present are mature; price wars or major competition are unlikely. The non-spectacular returns on capital also keep new competitors from trying to enter the fray and the regulation, while lowering returns, works to protect their position. In some situations they have even a monopoly, like the SARA refinery in Martinique.

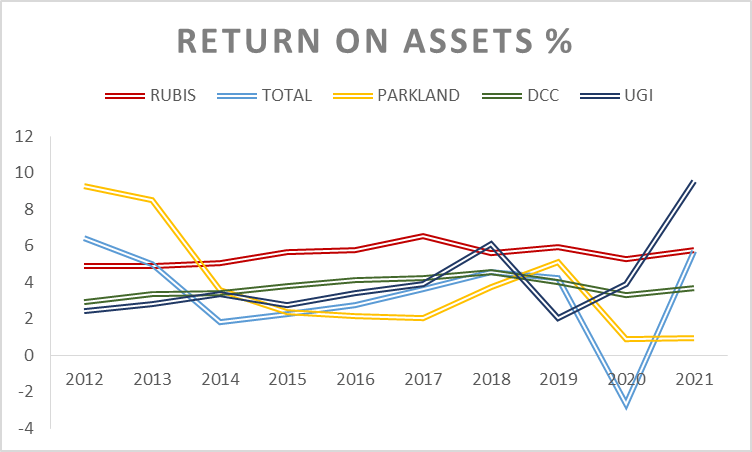

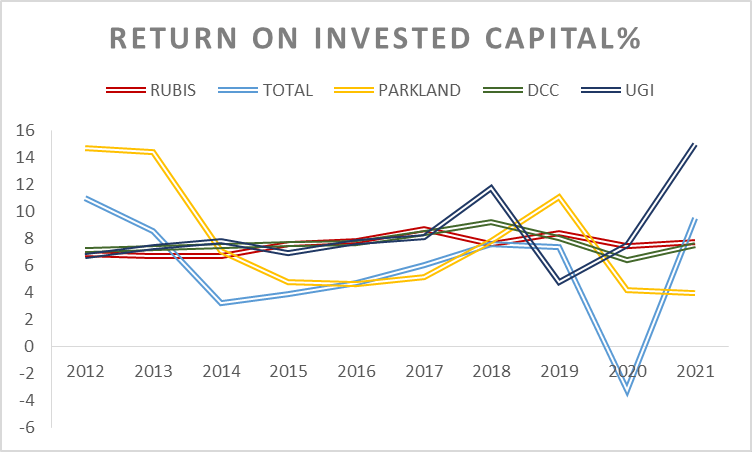

It’s difficult to select competitors for Rubis because each market might present different players. But, for the sake of comparison, I’ve used large worldwide distributors: TotalEnergies (TTE), Parkland (PKI:CA), DCC (OTCPK:DCCPF), and UGI (UGI). Here’s an overview of how they stack up:

- Parkland and DCC have significantly lower historical returns and margins in comparison.

- TotalEnergies is a larger company that also includes additional parts of the value chain with the upstream. Despite appearing relatively cheap and focusing on renewables, TotalEnergies is significantly exposed to oil prices and lacks the predictability of the “cost-plus” model.

- UGI has the most interesting margins and returns of the five, but also appears abnormally high with the rise of energy prices after the COVID-19 period. The company is somewhat closer to a utility provider, with part of the revenues coming from B2C electricity resale. It’s worth mentioning that net debt/EBITDA is more than 6x, a value higher than I would prefer even for a stable business – a low-interest coverage ratio.

I believe Rubis to be superior to these competitors because of responsible financial leverage, better-than-average returns/margins, cash flow convertibility, and, last but not least, their low volatile returns.

ROA for Rubis and its competitors (Morningstar.com)

ROIC for Rubis and its competitors (Morningstar.com)

Financials

Looking at the yearly values as of Dec. 31, 2021, the balance sheet appears to be solid; shareholder equity is higher (2.7B€) compared to the liabilities side (2.5B€), and net debt is relatively low (439M€) – less than 1x EBITDA – not yet including the Photosol acquisition. Since their strategy has been based on growth from acquisitions, they have a fairly large amount accounted for in goodwill (1.2B€), which might raise some doubts even with the standard impairment tests done each year. Working capital increased significantly from 2020 to 2021 (335M€ to 558M€) and I assume to be a correction derived from the pandemic and higher oil prices, although this should be verified in the next report.

For the P&L, things appear to be improving from COVID-19 lows with volumes picking up (5,049,000 m3 to 5,401,000 m3) and EBIT also increasing similarly (366M€ to 391M€). 2022 numbers might reflect difficult times because of high oil and natural gas prices. Rubis might struggle to pitch natural gas as a substitute for coal and wood in developing countries if prices are high. As stated by Jacques Riou (the co-founder and managing director) in an interview, volumes are more important than revenues because higher prices mean higher revenues, but not necessarily higher profits.

Lastly, the cash flow statement shows a similar picture. Operating income roughly compares to the cash flow from operations minus working capital changes (303M€ vs. 391M€), which reinforces the quality of the results. It should be taken into consideration that the cash flow from the joint venture is coming from the dividend received and not from the operation side. For the valuation exercise, I considered a rough 300M€ of free cash flow assuming growth and maintenance capex and a flat working capital accrual.

Management

The company is still managed by the co-founders – Gilles Gobin and Jacques Riou – who, through secondary owned organizations, complete the experienced management board. It’s worth highlighting that Gobin still guarantees Rubis’ debts with his assets, giving extra motivation for a long-term approach.

The management compensation policy is comprised of a fixed and variable part. Variable compensation has a quantitative and qualitative criterion that corresponds to the performance of multiple factors, including share price, EBITDA, earnings vs. estimations, and more. The fixed part is equal to last year’s compensation plus hourly rate change for the industry workers. It’s positive to see that the general partners also own shares of the company; although small in percentage, the position is close to 2.5%.

Overall, Rubis has an experienced management team with a proven track record of growing the company and incentives to maintain it.

SWOT analysis

|

Strengths |

Weaknesses |

Opportunities |

Threats |

|

Strong position in niche markets where it operates |

ESG score |

Pivoting the business toward renewables |

“Dividend aristocrat” status and the obligation of maintaining the status quo, or the possibility of cutting it |

|

Established distribution network and some regulated businesses, providing barriers to entry |

Sector disliked by investors – the high cost of capital |

HDF stake and strategic partnerships |

Operational accidents that might increase regulatory and environmental risk |

|

Low exposure to oil and gas prices |

Dependent on some high-risk markets |

Synergies from Photosol, HDF, and current core business |

Integration and execution of the renewable sector accordingly with the price paid |

|

Generates predictable and solid cash flows |

Asset-heavy business |

||

|

Exposed to high-growth markets, which should maintain fossil fuels for the coming years |

CO2 pollutant |

||

|

Experienced management team comprised of founding members with ownership of Rubis |

Might struggle to sell if commodities are expensive |

||

|

Low cyclicality of products |

|||

|

LPG considered a “bridging fuel,” especially in developing countries |

|||

|

Simple, predictable, boring, and mature core business – unlikely to see major competition between existing players |

Future outlook and risks

The importance of the terminal value and long-term future is high and should always be a concern for long-term investors. I believe natural gas usage, especially in Africa and the Caribbean, will be present for many years by way of a less harmful alternative to other fossil fuels like coal and oil. The current energy crisis, exacerbated by the war in Ukraine, forced the European Union to determine natural gas to be green and sustainable because of its role in allowing the transition to greener energy sources. McKinsey’s study has peak liquified natural gas demand happening in 2046, which will probably be much later for developed countries.

Thinking about the company’s other main cash provider – service stations – I have confidence that it will be transformed to include alternative energy sources like electricity or hydrogen or any other that might appear. And their inclusion of Photosol and HDF might help with the transformation. Having said that, it’s my opinion that this is the riskier part of the business, since “refueling” with electricity is different and it’s currently possible to build almost anywhere that is connected to the power grid. Their storage division will probably follow the same transformation, with some storage already being occupied by agricultural and chemical products.

GDP growth is a good indicator of possible volume growth for the business. The Caribbean and African regions are expected to expand more than the developed regions; for example, IMF reports real GDP growth for 2023 above 5% for Kenya, Rwanda, and Uganda. There is also the possibility that current macro environment challenges weigh negatively on, at least, next year’s results despite low cyclicality.

Valuation

Since future predictions are rarely fulfilled in these scenarios, I’ve decided to opt for a simpler approach and will look at the outcome by employing a price target range. To get the best results possible, I’ve combined three methods of valuation: the dividend model, free cash flow to the firm, and a multiples approach.

Using the dividend model with next year’s presumed dividend of 1.94€ (12% ROE with 65% payout ratio) and perpetual growth of 4.20% (lower than historical numbers), I get an intrinsic value of 21.75€. This is slightly lower than the current price for a great 13.11% expected return.

When using the full free cash flow to firm model, I’ve decided to create three scenarios with the same starting 300M€, but changing the growth rate from 0% to 6% and perpetual growth from 1% to 3%. After weighing these scenarios and adding joint ventures, cash, and the HDF position, while subtracting debt to the enterprise value, I get to an intrinsic value of roughly 39€ – substantially higher than the current price.

Lastly, for the multiples relative valuation, I’ve compared industry averages for U.S. distribution companies, competitive current and five-year averages, and Rubis’ own five-year averages. Assuming a 13 EV/EBIT and a 9 EV/EBITDA conservative scenario, the share price could be worth in the area of 44€.

Applying the three approaches and weighing 25% for the dividend and multiple model and 50% for the FCFF, I come up to a mid-30s€ price range – already including a good margin of safety.

Conclusion

In my opinion, the recent share price offers an asymmetrical risk/reward proposition because of COVID-19 issues, uncertainty for the new renewables divisions, and dividend investors dumping the stock because of a possible dividend cut to support growth. I see the downside risk as limited. Rubis is a growing, diversified, well-managed, low-volatility company trading at an 8% sustainable dividend yield. And I assume the Photosol acquisition will neither add nor destroy value to Rubis.

Be the first to comment