designer491/iStock via Getty Images

Summary

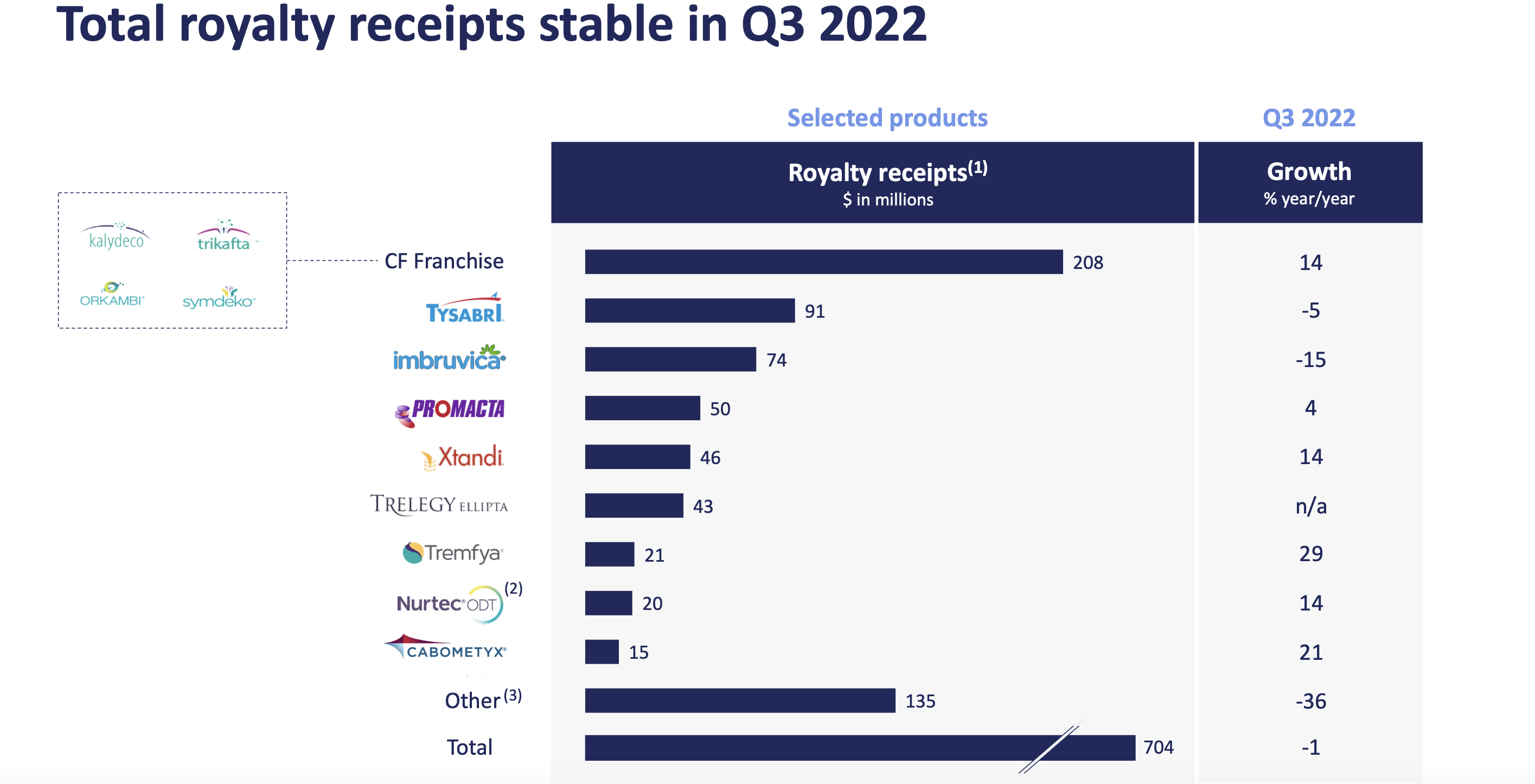

Royalty Pharma (NASDAQ:RPRX) is a profitable, dividend paying company with a business model which involves buying royalty streams. It has provided funding for unprofitable biotech companies, funded R&D projects for large pharma companies and purchased royalties from commercial products such as Humira and Lyrica. The company has a sustainable business model and a solid track record for investing in quality assets. The CF franchise showed significant growth (14% year/year) in addition to accounting for a significant portion of Royalty Pharma’s current revenue ($208 million of $704 million in Q3). The focus of this article is on the development of new CF medicines and how this may impact royalty revenue in the future.

Royalty Pharma owns CF royalties

The CF Foundation provided funding to Vertex to develop medicines for CF patients and subsequently sold these royalties to Royalty Pharma. Royalty Pharma purchased the CF Foundation’s royalties for Kalydeco, Orkambi, Symbeko and Vertex’s best seller, Trikafta for $3.3 Bn in 2014. It was the largest pharmaceutical royalty deal ever completed. Royalty Pharma recently invested an additional $575 million for additional royalties which an analyst at Evercore ISI valued at $1.2-1.3 Bn. The analyst was perplexed that they were sold for half of that amount.

Vertex (NASDAQ:VRTX) is currently developing a new triple combination of vanzacaftor/tezacaftor/deutivacaftor and will be determining if it is superior to Trikafta (elexacaftor/tezacaftor/ivacaftor). Deutivacaftor, a component of the new triple, is a deuterated version of ivacaftor. For those who do not fondly recall high school chemistry, isotopes are atoms which are the same element but have varying numbers of neutrons. Deuterated medicines are small molecules where a normal hydrogen is replaced by a heavier isotope of hydrogen called deuterium. This small change of replacing 9 hydrogen atoms is done to improve half-life and potentially improve side effects. A better side effect profile is possible because the therapeutic dose required may be lower than in an “un-deuterated” molecule.

This also potentially creates a new patentable molecule and companies such as Concert Pharma (CNCE) are Vertex are pursuing deuterated versions of molecules betting that they have cleverly developed a unique pharmaceutical which can be protected by an independent composition of matter patent. If Vertex successfully develops the new triple combination, they can also potentially reduce the royalty burden payable to Royalty Pharma.

The CF franchise from Vertex accounted for $208 million of Royalty Pharma’s $704 million in Q3 sales, making it a very significant revenue source. It also represented a growth driver as CF royalties were up 14% year over year and CF sales are expected to continue to increase in 2023.

Royalty Pharma Q3

Key questions which impact Royalty Pharma include will Vertex be successful in developing the new triple therapy and will this new deuterated molecule enable Vertex to reduce the royalty burden paid to Royalty Pharma. In an optimal situation for Vertex, they would only owe royalties on only one of the 3 components of the new triple combination.

Terrance Coyne of Royalty Pharma commented on the new triple therapy:

“…obviously, CF is a very important franchise for us, and we looked at a range of scenarios for CF. I think at a high level, though, we’re just sort of taking a step back, we continue to believe that Trikafta sets a really high bar. It’s been transformational for that disease. We haven’t seen anything so far based on the Phase 2 data. We haven’t seen detailed data, but based on the sort of press release that everyone else has seen, we haven’t seen anything that suggests that the new triple combination is any better at this point. So I think we feel really good about the long-term potential of Trikafta.”

Perhaps the best indication of whether Vertex has a superior triple combination can be gleaned by reflecting on its leadership position scientifically in CF. Vertex is the only company who markets correctors and potentiators and has a de facto monopoly. These drugs were developed in house by Vertex after the acquisition of Aurora Biosciences. One of the key scientific breakthroughs that was pivotal in the process was the development of a pre-clinical model which allowed Vertex to screen large numbers of potential molecules and assess efficacy accurately.

Vertex developed a HBE (human bronchial epithelial) assay cell line which was derived from donor lung tissue from a relatively healthy CF patient. Vertex perfected the process of growing HBE cells which then provided a model which proved to be highly predictive of clinical efficacy. In fact, the model has been shown to be quantitatively predictive of how efficacious drugs are in humans with CF. When Vertex developed Trikafta, they actually put multiple combinations into human clinical trials which allowed them to assess the predictive accuracy of the assay. In fact, results in humans were highly correlated to the assay—leaving them with options as to which medicine to bring forward.

This model allows Vertex to test the new triple combination therapy and assess whether it is likely to be superior. While Royalty Pharma has publicly stated that, “we haven’t seen anything that suggests that the new triple combination is any better at this point,” it is likely that Vertex has data that provides accurate insights into the efficacy profile.

Vertex’s Stuart Arbuckle stated at the recent Jefferies conference:

“We have great preclinical assays, which have proven to be both qualitatively and quantitatively predictive of what is going to happen in people with CF. Our HBE assays, which we developed in our labs in San Diego, have been incredibly predictive of how things will actually work in people with cystic fibrosis. So when we look at the new triple combination in those same assays, it delivers higher levels of chloride transport, which is the marker of CFTR function in the lab. So that’s incredibly encouraging, higher levels than we’ve seen with TRIKAFTA ever before. In addition to that, we’ve done a Phase 2 study with this same combination. And again, we saw higher levels of both FEV1 and also lower levels of sweat chloride. Sweat chloride is the pharmacodynamic marker in patients with CF of CFTR function. And we saw greater reductions in sweat chloride with this new combination than we saw with TRIKAFTA. So both of those give us reasons to believe that this combination could be even better than TRIKAFTA.”

Given the current trials in CF conducted by Vertex are virtually identical in design, cross trial comparisons are particularly meaningful. He also added that the primary endpoint for phase 3 is non-inferiority to Trikafta, but statistical analysis will be conducted for superiority. Thus, even if efficacy is similar, the new triple could be approvable by FDA if shown to be non-inferior. Patients can benefit from once daily dosing and a potentially better side effect profile.

Investors have good reason to believe Vertex has enough scientific expertise in CF to confidently make comparisons which inform their development decisions. The enormous investment to bring this new triple combination therapy from pre-clinical to phase 3 suggests Vertex is confident that the clinical trials will show excellent results.

Royalties

The current royalty rate for Trikafta is in the low double-digits (up to 12% per WSJ). The royalty rate for the new triple would be in the low single-digits and it may be close to 4%. Given this, if Vertex successfully brings the new triple combination to market, Royalty Pharma may receive dramatically less revenue from Vertex.

At a recent investor conference, Evercore’s analyst addressed the CF franchise issue when she stated,” It’s your opinion that you expect CF to be very durable for multiple reasons, not just based on what the incremental offering is from Vertex, but also because you believe you have legal grounds to assume that you do have royalties on even a next gen molecule as well.” Terrance Coyne of Royalty Pharma responded, “obviously, CF is a very important franchise for us, and we looked at a range of scenarios for CF…But we also, obviously, we understood that investors wanted to understand what the risk was under downside scenarios. And what we said is that we sort of see it as sort of a couple of hundred million dollar headwind to our business towards the back half of this decade.”

Royalty Pharma’s position is that deuterated versions of molecules still require royalty payments. Mr. Coyne stated at a recent conference, “Yes, we believe deuterated Kalydeco is simply Kalydeco and it should have the same royalty rate as Kalydeco.” The CEO added, “When we made the investment, we were extremely careful on our legal diligence and IP diligence…. We added a residual $600 million investment in this franchise where we bought out some residual interest that the cystic fibrosis foundation had. And again, we updated our diligence, very really careful IP diligence on all of this. And we got very comfortable and that’s why we ended up deploying another $600 million. So we’ll see. I mean we feel highly, highly confident on our legal position here.”

Vertex has taken a starkly different position. Vertex’s Stu Arbuckle stated, “Yes. I mean, from our perspective, it’s not really a matter of opinion. It’s a matter of contractual facts. So we feel pretty confident in our assessment of the contract and our view that the royalty rate is going to be…low single-digits… So we don’t think it’s a matter of opinion. We think it’s a matter of fact.” If the new triple combination shows strong efficacy, Vertex would be wise to encourage switching from older medicines and could even have the flexibility to offer it at a lower cost to encourage payers to cover it.

Given the entrenched positions of both companies, costly legal actions may be required to resolve this issue. Vertex may simply pay the low single digit royalty they believe is due and it will be Royalty Pharma’s burden to take legal action. This is likely to be a costly and prolonged legal process which may become an overhang on the stock.

Risks

Royalty Pharma has a sustainable business but the model involves similar risks to a large pharma company including negative clinical trial readouts from development-stage assets and competition in the commercial setting resulting in disappointing royalty payments. Gantenerumab, a medicine for which Royalty Pharma hoped to earn royalties recently failed in the clinic. This resulted in a non-cash impairment charge of $273.6 m which illustrates that the company faces risks which are similar to large cap pharma companies which are diversified but do experience setbacks in their pipelines. An unfavorable resolution to a legal dispute which may ensue with Vertex is an additional risk.

Conclusions

Given the difficulties unprofitable biotech companies currently face raising cash, Royalty Pharma is well positioned to negotiate favorable terms. Another positive factor is that the company has a high quality portfolio of medicines from which they earn royalties which speaks to the quality of their due diligence process. Royalty Pharma trades at a modest P/E of 10 and pays a dividend of 2%. In our view, investors might also consider a diversified large pharma company such as BMY which has a slightly lower P/E and over a 3% dividend rather than Royalty Pharma if they wish to have exposure to the pharmaceutical business.

The CF franchise accounted for approximately 30% of the last quarter’s revenue and upside in recent quarters has been at least partially driven by the strong performance from the CF franchise. Given Vertex’s new triple therapy could reach the market in 2024, rather than a growing CF royalty stream, a decrease in CF revenue is possible. Moreover, Royalty Pharma may need to defend their legal position which will undoubtedly be a prolonged and expensive process. While other investments in their portfolio may be successful, CF is a significant part of their revenue and an unfavorable resolution to this issue could impact Royalty Pharma’s earnings.

Be the first to comment