Introduction

There is no certainty in life. However, sometimes the odds are stacked in your favour. We see the possibility of purchasing Rolls Royce (OTCPK:RYCEF) shares currently at 6.17 GBP as one such situation, Below, we explain why we believe this.

Share prices don’t go down without a reason. Unfortunately, opportunities don’t come without risk. The buyer must judge whether the risk is justifiable by appreciating the possibility of a loss relative to a gain, and the potential size of that loss relative to the potential gain. This is the sole job of an investor. Simple, but not easy.

In the physical world the currency of life is energy. In the financial world the currency of life is cash. Rolls Royce is likely to produce considerably more cash during the next 10 to 12 years than its total current market cap of approx. 12 billion GBP. Considering the long contractual nature of its business, this provides quite a unique opportunity. We believe this opportunity arises from a number of negative circumstances that have occurred in short order, creating the perception the business is of lower quality than it is likely to demonstrate in the future via its capability of generating cash, and its return on tangible assets. Such issues include:

- Engineering costs to resolve issues with the Trent 1000 engine

- Fears that issues with the Trent 1000 may reveal issues with other RR engines

- Cash flow relatively muted as the old engine product cycle ends, and the business migrates into its new engine cycle. Selling engines is a poor business – maintaining them is a great business. With time the latter will dominate the former

- Rolls Royce is currently out of the narrow body market – and orders for large body planes have been tepid, especially relative to narrow body orders

- Complicated accounting, increasing debt, increasing negative news flow, a perception of a strong brand losing its way evident from its absence in the narrow body market

Ultimately, we view Rolls Royce as a “long cycle business”, at the inflection point of that cycle, which usually does not sit well with a more “short-term orientated” stock market investors.

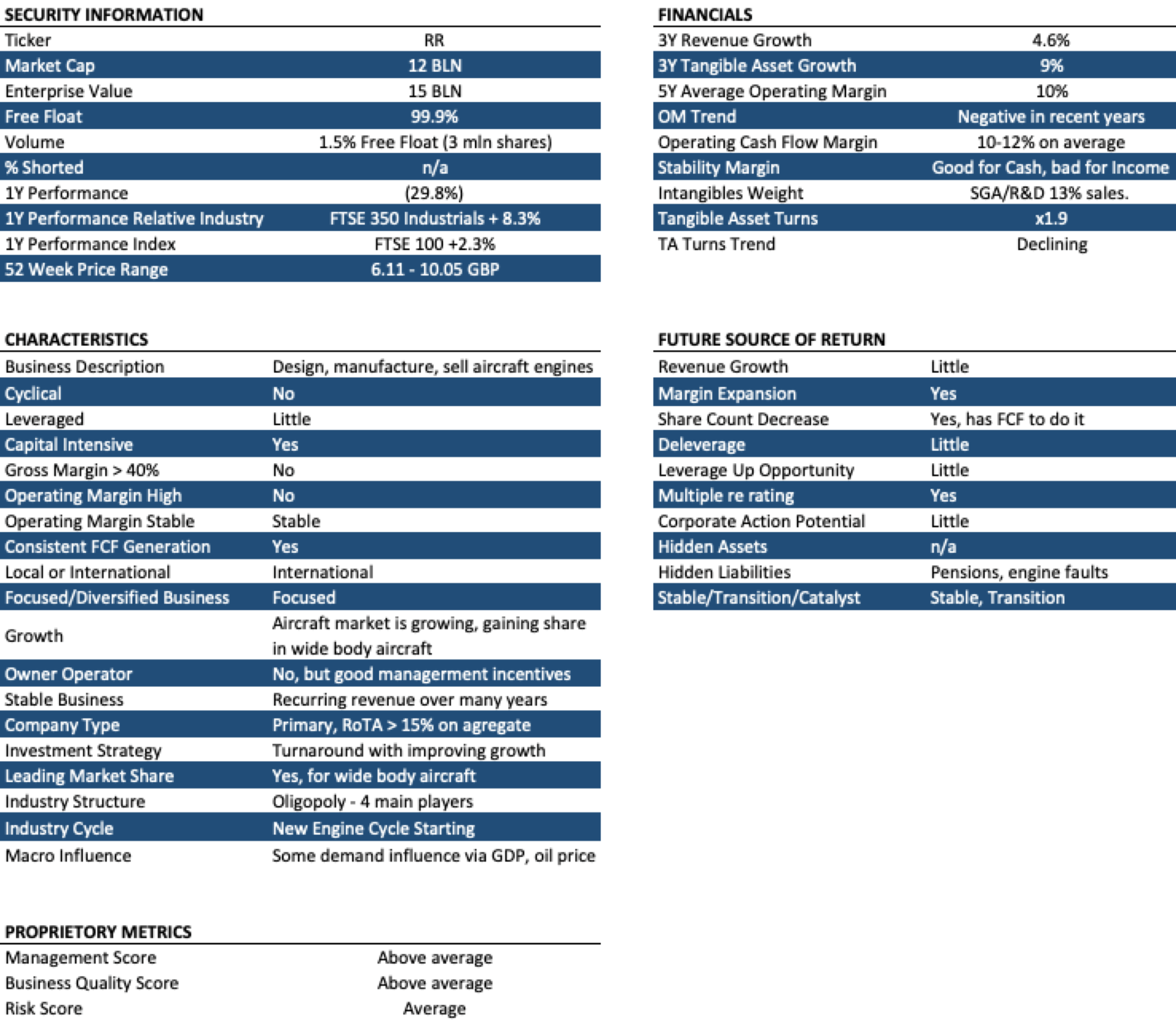

Below find a tear sheet I use to summarise the investment idea:

{kind=link}

Source: Author based on company fillings and market data from Yahoo finance.

Industry Structure and Dynamics

The Aircraft Engine industry is a natural oligopoly due to the large costs of developing new engine technology at the outset. There are similar market structures in adjacent fields, such as the aircraft manufacturers (Boeing (BA)/Airbus (OTCPK:EADSF), as well as other aerospace equipment suppliers. The intense competition in the engine market results in manufacturers willing to sell their products without profit, but capture significant value from the MRO (maintenance, repair and overhaul) business – the so called razor/blade business model.

In commercial aviation the major players in the manufacturing of turbofan engines are Pratt & Whitney (UTX), General Electric (GE), Rolls-Royce, and CFM International (a joint venture of Safran Aircraft Engines (OTCPK:SAFRF) and General Electric). The turbofan is a type of air breathing jet engine. A jet engine discharges a fast-moving jet that generates thrust by jet propulsion.

Rolls-Royce is the current market leader in the wide-body aircraft segment (aircrafts having a fuselage wide enough to accommodate two passenger aisles). In the narrow body market CFM is the leader. CFM has an exclusive contract for its LEAP engines to power Boeing’s 737 MAX family jets. That exclusivity offers a big share of the narrow-body jet engine market. The LEAP-1A engine is also an option for Airbus’s popular A320neo family of jets, which is competing with a geared turbofan (GTF) offering from United Technologies subsidiary Pratt & Whitney.

While Pratt & Whitney’s engine is slightly more fuel-efficient than the LEAP-1A, CFM has still managed to win a majority of the Airbus business. The GTF engine has suffered a string of reliability issues. Indeed, a number of airlines are switching from the GTF engine to the LEAP-1A as a result. IndiGo is an important customer for Pratt & Whitney’s GTF engines for Airbus 320neos, yet recently the Indian budget carrier placed a $20 billion order (at list prices) for CFM International Leap-1A engines to power 280 Airbus A320neos and A321neos.

GE is also a strong competitor in the wide-body jet engine space with its GEnx offering. In this case it faces competition for powering Boeing 787 Dreamliners, from Rolls-Royce. However, the Rolls-Royce Trent 1000 engines have also suffered reliability problems, allowing GE to gain market share in this space. GE has also had engine issues with the GE9X used to power the Boeing 777X, alongside the problems forced upon it by the grounding of the Boeing 737 MAX.

Much noise has been made by the large number of new engine issues in recent years by all the major manufacturers. This is likely driven by Airbus SE and Boeing Co. having brought several new passenger jets to market in quick succession, and their powerplant suppliers having had to ramp up production rapidly. Furthermore, a lot of new demand is from emerging markets where dusty or polluted air can put additional strain on engines, which in the past have not been tested in that environment.

Yet the problems haven’t affected all new technologies. Rolls-Royce’s XWB powerplant for the Airbus A350 has proven reliable so far. Also the core gearing innovation underpinning Pratt’s GTF also appears to work as planned; a relief because it cost around $10 billion to develop.

Demand for air travel continues to increase, an important metric that provides a tailwind for the engine manufacturers. Growth in revenue passenger kilometers (RPK) will regularly exceed the annual expansion of gross domestic product in most economies—particularly in high-growth areas like China and India, which continue to have an expanding middle class. Even amid global trade tensions, the projections for commercial air travel remain optimistic across all regions of the world. The active global commercial fleet stood at 26,307 aircraft in 2018; during the next 10 years it is estimated to see a 3.7% annual growth, increasing the fleet to 37,978.

The industry is also seeing increasing pressure regarding environmental concerns, hence airlines demand more fuel-efficient aircraft engines. As with the automotive industry, the aerospace sector is gearing up for an epochal effort to curb carbon emissions. Aviation accounts for 2%-3% of greenhouse gas emissions, but the sheer volume of plane deliveries in coming years will counteract engine efficiency gains. Aviation’s share could rise to between 10% and 25% by 2050, a recent Roland Berger study found.

However, unlike carmakers, the airlines lack viable technological alternatives. Biofuels have potential, but today’s battery limitations mean the disruption seen in the automotive industry has not yet made a similar impact in the aviation industry. Yet electrification over time is expected to have as dramatic an impact on aviation as the replacement of piston engines by gas turbines.

In this evolution to the third era of aviation our interest was piqued by Rolls-Royce’s agreement in 2019 to acquire the electric and hybrid-electric aerospace propulsion activities of Siemens (OTCPK:SIEGY) (the eAircraft business). The eAircraft business has been developing a range of all-electric and hybrid electric propulsion solutions for the aerospace industry. The eAircraft team were already known to Rolls-Royce as they worked together on the E-Fan X demonstrator project which, when flying, will demonstrate hybrid electric propulsion at the scale required to power regional aircraft.

Engine manufacturers are already working on next generation engines, likely the last before electrification plays a larger role. Rolls-Royce claims its Ultrafan technology will deliver a 25% improvement in fuel burn compared to the first generation of Trents, and suitable for new single- or twin-aisle aircraft entering service from the mid-2020s. GE’s GE9X should increase fuel efficiency by 10% over the GE90, and currently is the sole-sourced engine for the Boeing 777X family. Pratt and Whitney will continue its roll out of its GTF engine, with its geared fan technology. The GTF engine powers five aircraft platforms, with the Airbus A220, the Airbus A320neo family and Embraer E190-E2 already in commercial service. The GTF-powered A320neo has achieved a 16% reduction in fuel consumption, a 75% reduction in noise footprint and a 50% reduction in nitrogen oxide emissions.

Whilst much has been discussed about the engines themselves, it should be re iterated that the bulk of the value in this business is generated through MRO contracts. The European Commission has in the past inquired about the maintenance market of global aerospace suppliers. A clear sign that it is a lucrative business. Manufacturers and suppliers like the double digit margins available in such business, and we note that third party service providers seem to be less dominant as the technology from manufacturers are becoming more advanced – for example due to emerging new technologies like predictive maintenance – hence allowing more value to be accrued to the original developer. The EC inquiry was based on whether equipment suppliers were withholding crucial information on products — such as manuals and technical drawings — to ensure that only they or their partners can provide spare parts or carry out high-quality maintenance. Add to this that there are fewer independent MRO providers because of consolidation, and it’s not a surprise that aircraft maintenance is becoming more expensive. Indeed, the industry is becoming so lucrative that even the two biggest aircraft manufacturers, Airbus and Boeing, indicated they expect to exponentially increase their MRO business over the next several years. However, they do not have the expertise to enter the engine market.

One cannot end this section without mentioning the grounding of the Boeing 737 Max. Apart from the obvious consequences to Boeing/Airbus dynamics, it also affects the suppliers of the different planes that will be affected, and therefore change how the profit pool is distributed in the aircraft engine industry. It should also not be lost to the reader that in 2015 Boeing proposed launching a new mid-sized jetliner to fill a gap between the narrow and wide-body aircraft (NMA), with airline operations beginning in 2025. Boeing put back a decision to select an engine for the NMA even before the fatal crash of the Ethiopian Airways Max on March 10, 2019. The subsequent worldwide grounding of the 737 may force the company to suspend work on the new plane to focus its full attention to getting the narrow-body workhorse flying again. This could be an important change for Rolls Royce, who dropped out of the race to power Boeing’s planned mid-market aircraft in early 2019, saying it did not want to risk more disruption for its airline customers by rushing out a product without extensive testing – this being driven by the desire to avoid a repeat of the problem suffered with its Trent 1000 engine that powers Boeing’s Dreamliner 787. Rolls had initially regarded the NMA as a potential launch platform for its new Ultrafan engine. Whatever the decision on the NMA, Rolls intends to bid to power the next generation of single-aisle planes expected to succeed both the Max and Airbus SE’s A320neo jets from 2030. That would represent a milestone for the company after it quit the narrow-body market in 2011 to focus solely on bigger planes, which has left the sector to General Electric Co. and Pratt & Whitney. A delay in the NMA plane increases the chance Rolls can bid for this contract with its new Ultrafan technology.

A Brief History of Rolls Royce

Rolls-Royce Holdings plc is a British multinational engineering company that designs, manufactures and distributes power systems for aviation and other industries. Rolls-Royce is the world’s second-largest maker of aircraft engines (after General Electric), dominates the wide body aircraft engine market, and is listed on the London Stock Exchange, where it is a constituent of the FTSE 100 Index, it has the ticker RR.

The company has a rich history of innovation, including in the late 1950s producing the world’s first turbofan engine that entered service, and today producing some of the world’s most energy efficient aircraft engines, as well as developing some very promising next generation products such as the Ultrafan engine, electric powered aircraft, and advanced digital services to help maintain engines. The company’s history has also tasted troubled times. In 1971 Rolls-Royce Limited declared bankruptcy. The company blamed its collapse on the huge losses incurred in developing the engine for the Lockheed Aircraft Corporation’s Tristar airbus. Rolls said it could not proceed with the engine under the fixed price contract it had (such a contract provides a fixed payment to the supplier, hence cost overruns are a liability for the supplier, not the customer). In bankruptcy its business and assets were bought by the British government. Rolls-Royce motors was separated out in 1973. Rolls-Royce plc returned to the stock market in 1987 under the government of Margaret Thatcher.

Whilst today Rolls has an enviable position in the wide body market, it’s position is not so positive in the narrow body market. Historically it gained this exposure with a joint venture (International Aero Engines, IAE) with Pratt & Whitney. This joint venture has been successful on the A320 family, splitting the market with CFM-56 from the GE/Snecma joint venture. Whilst IAE has no presence on the Boeing 737, it still has about 25% of the narrow body market

The new A320 Neo will utilise the PW1000G (from Pratt & Whitney) and LEAP X from CFM International (GE/Safran JV) as its engine choices, with IAE out of the picture. Pratt & Whitney offered GTF technology to the IAE JV, but Rolls Royce preferred its own three spool RB285 design. This offering has not been viewed favourably by the industry, and no manufacturer has selected the Rolls offering.

In 2015 Mr. Warren East replaced the then CEO, Mr. John Rishton. Mr. East came from the British Chipmaker, ARM, where he developed an excellent record over many years. However, many queried the relevance of that experience considering the large difference between the two industries.

Not long after coming on board, in 2017, Rolls-Royce posted its largest ever pre-tax loss of £4.6 billion. This included a £4.4 billion write down on financial hedges that the company used to protect itself against currency fluctuations, and a £671 million penalty to settle bribery and corruption charges with the Serious Fraud Office (SFO), the US Department of Justice, and Brazilian authorities. The stock price declined significantly. Since them it has also taken a charge of £2.4 billion to cover faults with some Trent 1000 engines on Boeing’s 787 Dreamliner. Rather than going thousands of hours between inspections, the faults with turbine blades means the engines currently require inspection far more regularly.

However, we believe Mr. East is helping build up strong positive momentum within Rolls Royce. He has shown himself to be prudent, able to make tough decisions, focused on the long term benefits of the business, and responsible to all stakeholders of the company. We find a good deal to like from his actions, including:

- He has not pushed to gain access to the narrow body market via a rash acquisition, or pushing forward an aggressive R&D agenda.

- Instead focused the business by divesting the commercial marine business, and the civil nuclear services businesses in the U.S., Canada, Mondragon France, and Gateshead UK.

- Indeed, Rolls Royce dropped out of the race to power Boeing’s planned mid-market aircraft saying it did not want to risk more disruption for its airline customers by rushing out a product without extensive testing.

- June 2018 the company announced a restructuring to create three simpler decentralised units (civil aerospace, defence and power systems). Decentralisation is often a positive step to incentivise more free thinking and innovation through less stifling group wide bureaucracy, and helps develop a deeper sense of accountability and responsibility within local management.

- Rationalise back office functions and to remove middle management functions (Rolls Royce is notoriously bureaucratic – and the executive team has faced this issue head on).

- The cost savings should amount to £400 million per year by 2020, with an up-front restructuring cost of £500 million.

- Continuous investment in next generation technology such as the Ultrafan engine.

Whilst Rolls has rightfully received negative press on the Trent 1000 engine issues, we should note other engine makers have not been free of trouble, as mentioned in the previous section.

The Product Line

The Trent family of seven different engines has now accumulated more than 140 million flying hours since the first Trent (Trent 700) entered service in 1995. We highlight some below:

Source: Author based on company fillings, Wikipedia

- The Trent XWB is the world’s most efficient large aero engine flying today, and the world’s fastest-selling wide body engine with more than 1,800 in service or on order. As it recently approached five years in service, it has achieved more than five million flying hours, and demonstrated an excellent dispatch reliability of 99.9 per cent

- The Trent 1000 has made headlines for all the wrong reasons in recent years, due to corrosion related fatigue cracking of turbine blades that were discovered in early 2016, grounding up to 44 aircraft. Rolls claims it has helped reduce the GEnx dominance of the Boeing 787 engine market. However, in early 2018, of 1277 orders, 681 selected GE (53.3%), 420 Rolls-Royce (32.9%) and 176 were undecided (13.8%). Rolls has lost considerable market share due to issues with the engine, initially receiving over 40% of new orders for the Boeing 787, and declining as the engine problems have dragged on. There are currently over 800 Trent 1000 engines in service

- The Trent 7000 is based on the Trent 1000, hence some fear it could share its durability problems and that it could deter buyers. Rolls-Royce’s CEO Warren East said the 7000 was not affected by the Trent 1000 issues. As of January 31st 2020, 45 A330 Neo’s have been built. Between January 2014 and November 2019, the A330/A330neo had 477 net orders (net of cancellations) compared to a total of 407 for all three variants of the 787. The A330neo program was the best-selling Airbus widebody over the same period. Hence there is a potential for a wide runway for growth on this product line.

- The NMA aside, the first available application for the Ultrafan could be a re-engined version of the Airbus A350 that the European company is studying for introduction toward the end of the 2020s.

- It is clear from the data above that Airbus continues to be Rolls closest industrial partner. With the issue Boeing is suffering with the grounded 737 MAX, this is a blessing for Rolls (for the moment).

Valuation

We see over the next few years Rolls revenue increases from 16 billion to closer to 20 billion. At the current price one need not assume greater revenue increases to have the potential for a 70 – 100% return from the current price to fair value based on a 17x to 20x multiple on free cash flow (“FCF”). During this period we expect margins on operating cash flow to settle around the 13% level (currently 14%), with capex averaging around 7% sales (currently at 10%). This should generate free cash flow of around 1.2 billion per annum (a 10% FCF yield on the current market cap). With a tangible asset base of around 9 billion, this generates a return on tangible assets (RoTA) of around 13%. More than your average commodity business, but not a suitable qualification to be a Primary business. We suspect the concentration of the Boeing/Airbus duopoly ensures value is better extracted by the aircraft manufacturers, who generate considerably higher returns on tangible assets (hence why Rolls gross margin is only 20%). However, the level of the RoTA today is compensated by its duration and stability as the MRO contracts are of a very high quality. This is ultimately why we view Rolls Royce as a primary business.

We believe the primary source of value add for Rolls comes from its asset turnover (revenue/tangible assets) rather than its margin. As indicated above, price is heavily negotiated by the Airbus/Boeing duopoly, keeping the margin in check. Hence, the asset turnover metric must be closely watched. With turns on tangible assets at 1.8x at the moment – as more of the new engines go into service, and since maintaining the MRO contract is less capex intensive than developing and building new engines, we should see this metric improve considerably. Indeed, if we review Rolls result before the notable increase in capex from 2013, we can see a regular turn on tangible assets around 2.5x. This would improve today’s RoTA considerably, and make Rolls a clear Primary business. The average tangible asset turnover over the last decade is 2.3x. Hence, the business is clearly under earning at the moment.

There is also potential for some margin increase as the MRO revenue mix increases, and as such business generates a higher operating margin closer to 20%. However, with continuous capex needs to develop new engines, and one hopes a continuous sale of new engines, we assume aggregate FCF margins will not increase much over 7%.

Conclusion

- Rolls Royce is entering an inflection point in its aggregate engine cycle, where important models will become more cash-generative moving forward. The current stock price does not consider this to be realistic, indeed, the market expects future earning power to decline, extrapolating recent issues and large expenses to continue indefinitely

- The Trent 1000 is a risk that has damaged cash flow in the last 2 years, and can continue to damage cash flow in a smaller way in the future. We think the decline in the stock price compensates the investor for this scenario at today’s price.

- Respectable and capable management in a profitable and growing industry whilst holding a strong balance sheet offer a strong lines of defence to minimise fears of a dilutive rights offering or bankruptcy.

- The stability of the business from recurring revenue through long term MRO contracts will come to the fore when temporary, large expenses in developing new programs and resolving engine issues are reduced. When it does it will likely lead to a strong multiple re rating. This business does not deserve a 10x multiple on FCF, but between 17x- 20x. We do not expect the latter costs to ever disappear, but we do believe that due to where we are in the business’s engine cycle, they are larger than their average contribution over the company’s entire engine cycle

- Rolls is likely to continue taking market share in the wide body market, particularly with the Trent XWB and Trent 7000 engines. This will allow the business to grow

- The biggest risk we foresee is that other engines in their product line suffer a fate similar to the Trent 1000. As time passes and these engines enjoy more service time, this risk reduces.

Disclosure: I am/we are long RYCEF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment