draganab

For those not familiar with it from an economic perspective, the space economy may not seem all that appealing. This is opposite of outer space itself, which most children seem to dream of visiting as astronauts when they grow up. But the fact of the matter is that this has now become a rather sizable and continuously growing part of the global economy. Both governments and commercial entities are investing heavily in this market for a variety of reasons, including telecommunications, foreign state monitoring, and more. In fact, in 2021 alone, the industry grew by roughly 9%, hitting $469 billion in all. One of the companies in this space that should at least be on the radar of investors is Rocket Lab USA (NASDAQ:RKLB). With a market capitalization of $2.35 billion, this particular enterprise is fairly small in the grand scheme of things. In addition to that, it is suffering from a profitability and cash flow perspective. But with revenue growing nicely and backlog standing at all-time highs, there might be some potential for investors who don’t mind an elevated amount of risk.

Way out there

The management team at Rocket Lab USA describes the company as an end-to-end space business that focuses on delivering reliable launch services, spacecraft design services, spacecraft components, spacecraft manufacturing, and on-orbit management solutions for its customers. The company does seem to have a rather large pool of activities that it engages in relative to its size. For instance, it does provide customers with a new generation of small spacecraft called Electron. This is a fully carbon-composite launch vehicle that, amongst other things, utilizes the company’s own electric turbopump 3D printed engines. From its launch in 2017 through the end of 2021, the company delivered well over 100 spacecraft to space across 33 successful orbital missions for both commercial and government customers alike. On top of this, the company has its own private launch complex in New Zealand that has two different launch pads, with the second one alone capable of supporting up to 120 missions every year.

The most recent news that sent shares of the company up just the other day was that the company had successfully launched its first Electron mission from US soil, marking the 33rd Electron mission overall. This particular mission included not one but three satellites that were taken to a 550-kilometer orbit for a customer called HawkEye 360 that plans to utilize it in its radiofrequency geospatial analytics offerings. This brings the total number of satellites launched by the company to orbit to 155 and marks the success of the third launchpad it now has in operation.

It’s incredibly important to note that this is an enterprise dedicated to continued innovation. For instance, the firm has been developing its own new launch vehicle called Neutron, which will be in advance and reusable 8-ton payload class launch vehicle specifically designed for large constellation deployments, interplanetary missions, and human spaceflight. This is not just a simple launch vehicle though. In fact, the company is constructing its own production complex where the vehicle will be produced. That complex is 250,000 square feet of space set on a 28-acre site in Virginia. The company is also working on a new engine, currently referred to as Archimedes. This year, the company will run its first tests on the 3D-printed engine components that it’s producing for that device. This is just a taste of the activities that the company engages in. It also has other operations, such as a reaction wheel prototype that it’s making for a major constellation customer, with the company’s own production line capable of delivering up to 2,000 units per year.

Author – SEC EDGAR Data

Between 2019 and 2021, the company experienced some growth. But it’s not growth that I would be particularly head over heels for here. After seeing revenue drop from $48.4 million in 2019 to $35.2 million in 2020, it did pop higher to $62.2 million in 2021. On the bottom line, the picture for the company has only gotten worse. Net income, for instance, went from a loss of $30.4 million in 2019 to a loss of $117.3 million in 2021. Operating cash flow turned from negative $21.6 million to negative $71.8 million, while the adjusted figure for this went from negative $21 million to negative $63.8 million. And finally, EBITDA for the business went from negative $28 million to negative $90.7 million over the same three-year window.

Author – SEC EDGAR Data

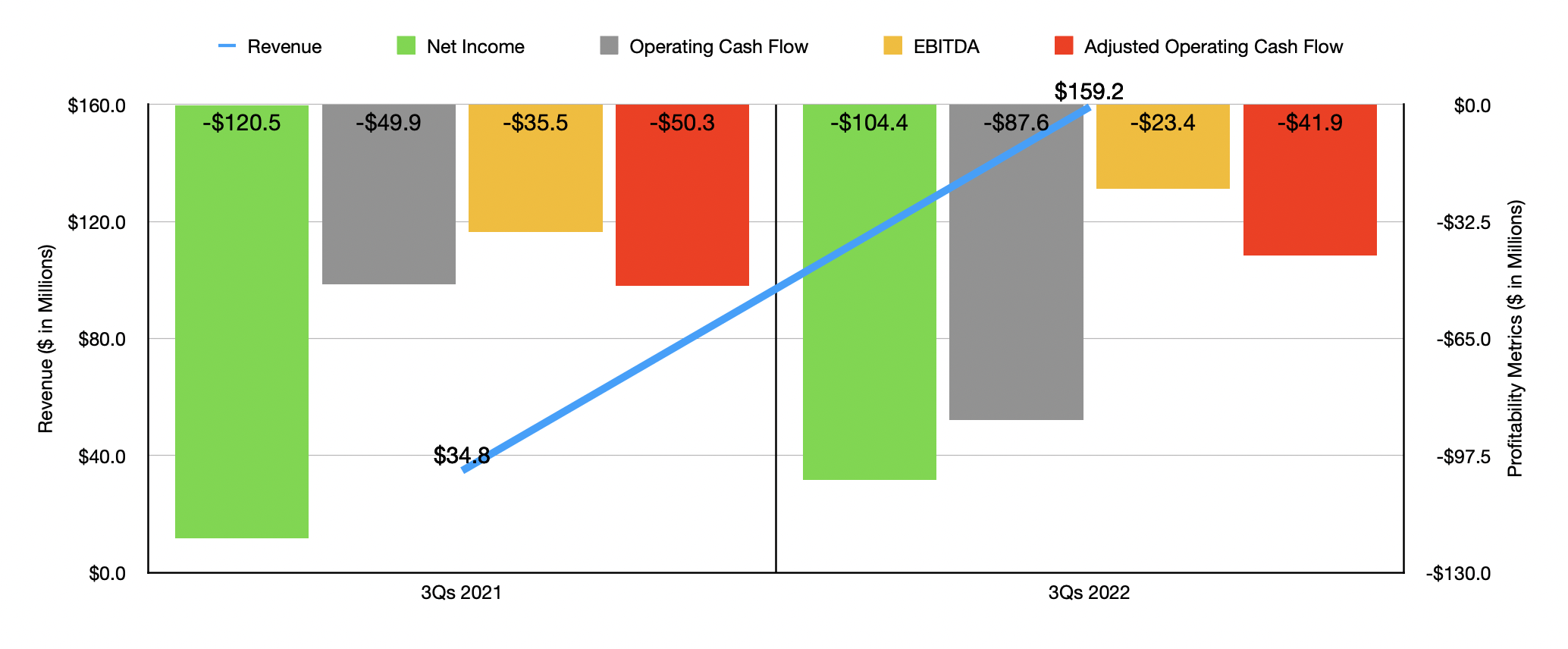

Based on this data alone, I would normally stay far away from the company. While it can be okay to invest in a company that’s generating large and growing losses and cash outflows, you need to see rapid growth in order for that to be justified. But the picture has now changed when we start looking at data for 2022. For the first nine months of the year, sales came in at $159.2 million. That’s significantly higher than the $34.8 million reported the same time one year earlier. This increase, management said, was largely because of $85.9 million coming from acquisitions that closed in the final quarter of 2021 and in the first quarter of 2022. Higher launch cadence delivered growth of $23.5 million, while organic growth for the company’s space system products and services pushed sales up by $15.1 million. To bolster this growth further, consider that, by the end of the third quarter, backlog for the company came in at $520.6 million. Of this, $122.4 million is associated with launch activities while $398.2 million is associated with the company’s space systems. By comparison, backlog at the end of the third quarter of 2021 came in at only $183.1 million.

This is the kind of growth that could create some great upside for the company. But we also need to pay attention to bottom line results. And even on that, we are seeing some improvement. The net loss for the company in the first nine months of 2022, for instance, came in at $104.4 million. That’s an improvement over the $120.5 million loss experienced one year earlier. It is true that operating cash flow worsened, turning from negative $49.9 million to negative $87.6 million. But if we adjust for changes in working capital, it would have actually improved from negative $50.3 million to negative $41.9 million. Meanwhile, EBITDA for the company went from negative $35.5 million to negative $23.4 million. For those worried about the company running out of cash, consider that cash in excess of debt right now stands at $384.8 million. This does give the company a good deal of runway while it grows its revenue and focuses on bottom line improvements.

Author – SEC EDGAR Data

Unfortunately, you can’t really value a company like this. But what you can do is ask what kind of cash flow the company might need to achieve in order to be at least fairly valued. As part of this analysis, I looked at three different scenarios for both operating cash flow and EBITDA, with the former being compared to the company’s market capitalization and the latter being compared to its enterprise value. The first scenario looks at what kind of cash flow or EBITDA would be needed for the company to trade at either a price-to-operating cash flow multiple or an EV-to-EBITDA multiple of 10. The more lenient scenario looks for a multiple of 20, while the most lenient scenario looks for one of 30. As you can see, these are still rather high hurdles to climb, given the amount of revenue the company generates. Likely, it would have to grow meaningfully and/or cut down on costs, if it wishes to become a truly viable enterprise for the long haul.

Takeaway

From a balance sheet perspective, a backlog perspective, and a growth perspective, Rocket Lab USA is a really interesting and attractive opportunity. It’s also helpful that bottom line results for the firm showed improvement throughout much of 2022. Unfortunately, the significant net losses and cash outflows still weigh on the firm and will likely continue to do so until management can prove that they can at least move toward cash flow neutrality. Having said that, the company’s long runway, combined with the size and growth of the industry in which it operates, leads me to be a bit more neutral on the firm. Because I do recognize that risks exist, I cannot bring myself to rate it a ‘buy’. But I do think it makes for a decent ‘hold’ if we assume financial results will continue to improve and that backlog will remain robust for the company.

Be the first to comment