ricochet64/iStock Editorial via Getty Images

Introduction

Roche (OTCQX:RHHBY, OTCQX:RHHBF, OTCPK:RHHVF), the world-renowned pharmaceutical and diagnostics giant, released its annual results on Feb. 2, 2023. I’ve covered the company before, most recently in a comparative analysis with Johnson & Johnson (JNJ), where I highlighted why I think JNJ is the better dividend stock overall, but nonetheless consider Roche an impressive long-term investment.

In this update, I will provide my opinion on the annual results, but more importantly on the recent insider selling of 2.7 million voting securities (ISIN CH0012032113, OTC ticker OTCQX:RHHBF).

Brief Earnings Review

For 2022, Roche reported sales growth of 0.8% in CHF, which I personally consider quite positive in light of the fading pandemic-related restrictions and the associated decline in demand for SARS-CoV-2-related testing equipment. Of course, the strong Swiss franc – with its safe haven status still intact in times of heightened geopolitical uncertainty – also played a role, resulting in slightly higher sales growth at constant exchange rates (2%). However, as Roche is a globally diversified company, I see no reason to focus on theoretical currency-adjusted results. Therefore, all figures discussed in this article are reported figures and have not been adjusted for currency effects.

2022 free cash flow, adjusted for working capital effects and expenses for stock-based compensation and defined benefit pension plans (normalized free cash flow, nFCF) was below the previous year’s figure, but was still acceptably high at around CHF 13 billion, which corresponds to a free cash flow margin of 20% (Figure 1).

![Roche’s [RHHBY, RHHBF] free cash flow, after normalizing with respect to working capital and adjusting for stock-based compensation and defined benefit plan expenses; free cash flow margin in percent of sales](https://static.seekingalpha.com/uploads/2023/2/15/49694823-16764855653248434_origin.png)

Figure 1: Roche’s [RHHBY, RHHBF] free cash flow, after normalizing with respect to working capital and adjusting for stock-based compensation and defined benefit plan expenses; free cash flow margin in percent of sales (own work, based on the company’s 2017 to 2022 annual reports)

This puts Roche in a very comfortable position from a dividend perspective, as the company only paid out CHF 7.8 billion in 2022, a decrease of 3.7% year-over-year ((YoY)) or a payout ratio of 60% based on nFCF. The decline, of course, is not due to a dividend cut (Roche increased its 2022 dividend by 2.2% to CHF 9.3) but to the repurchase and cancellation of 55.3 million bearer shares from Novartis (NVS, OTCPK:NVSEF) in December 2021 (p. 9, 2022 annual report). For 2023, Roche’s Board of Directors proposed a 2.2% dividend increase to CHF 9.50 (the 36th consecutive increase), translating to a dividend yield of 3.42% (non-voting shares) and 3.13% (voting shares), as of Feb. 15, 2023.

So why are Roche ADRs (OTCQX:RHHBY) down 30% from their 52-week high? After all, the company reported sales growth despite the fading pandemic and announced another dividend increase. I see two main reasons:

At the start of the pandemic, Roche made headlines with its fully automated cobas high-throughput qualitative testing system (which also was recently approved for the detection of monkeypox virus), which is reported through Molecular Lab, a subdivision of the Diagnostics division. I have no doubt that many short-term investors bought Roche because of its COVID-19 franchise and are therefore increasingly pessimistic about the company due to declining demand for testing equipment and COVID-19 therapies.

Molecular Lab sales totaled CHF 3.5 billion in 2022, representing 19.5% of Diagnostics sales or 5.5% of total sales. It’s also worth noting that part of Roche’s SARS-CoV-2 diagnostics (rapid tests) is reported in the Point of Care division. Overall, SARS-CoV-2 diagnostics were responsible for sales of CHF 4.1 billion, down 13% YoY. Of course, such a decline is not insignificant, but it should be seen against the backdrop of growth in Roche’s base diagnostics business (+7% YoY). Sales in the Diagnostics segment as a whole were flat YoY, which I consider a very solid performance given the fading pandemic.

More importantly, Roche’s performance in its Pharmaceuticals segment (72% of total sales) was somewhat weak. Sales were up 1.1% YoY, or up 2.2% when excluding COVID-19 treatments Actemra (tocilizumab) and Ronapreve (casirivimab/imdevimab, originally developed by Regeneron (REGN)). Of course, such growth figures are minuscule in direct comparison to Merck (MRK), which reported strong growth (22% YoY) thanks to its blockbuster cancer treatment Keytruda (pembrolizumab). A fairer comparison would probably be Johnson & Johnson, which reported 1.3% year-over-year sales growth.

Roche’s somewhat weak performance was driven by sharp declines in Avastin (bevacizumab, -31% YoY, CHF 2.1 billion) and Herceptin (trastuzumab, -20% YoY, CHF 2.1 billion) due to strong competition from biosimilars. After all, the two cancer therapeutics already were approved in the U.S. in 2004 and 2008, respectively. However, Roche’s combination product of Herceptin and Perjeta (see below), approved in 2020 and marketed under the brand name Phesgo as a subcutaneously administered treatment for HER2-positive breast cancer, is ramping up very well (118% YoY, CHF 740 million).

Ocrevus (ocrelizumab, multiple sclerosis), Perjeta (pertuzumab, breast cancer), Hemlibra (emicizumab, hemophilia A), and Tecentriq (atezolizumab, cancer treatment) together accounted for 29% of Roche’s 2022 sales and grew 19%, 3%, 35%, and 15% YoY, respectively. Perjeta stands out negatively as the drug was already approved back in 2012 and due to internal competition from Herceptin, Phesgo, and Kadcyla (trastuzumab-emtansin). Hemlibra’s approval was recently expanded to include patients with only moderate hemophilia A. Regarding Tecentriq, Roche reported positive results from a phase III study evaluating the drug’s efficacy when administered subcutaneously.

I think it’s important to note that all of these products are biologics. Through Genentech, Roche has become a leader in antibody-based therapeutics. Of course, they all face loss of exclusivity (LOE) sooner or later or have already lost their main patent protection (see above). However, biologics are somewhat less vulnerable to post-LOE competition than small molecule drugs because the development and successful commercialization of biosimilars is generally quite complex. In addition, biologics will be treated more favorably than small molecule drugs under the Inflation Reduction Act (see, for example, this open-access review).

However, a closer look reveals that Roche is focused not only on biologics in general, but on cancer therapeutics in particular. It should be borne in mind that this is a very competitive area, and Roche also is plagued by setbacks, such as Tecentriq not meeting its co-primary endpoint of progression-free survival in a phase III study of PD-L1-high metastatic non-small cell lung cancer.

In 2022, Roche received the approval for Lunsumio (mosunetuzumab, relapsed or refractory follicular lymphoma), but also for a non-oncology biologic, namely Vabysmo (faricimab), which is used to treat wet macular degeneration and diabetic macular edema. The drug generated sales of CHF 591 million in 2022. Roche also reported positive phase III data for the biologic’s use in treating patients with retinal vein occlusion. Recent setbacks in the non-oncology area include Alzheimer’s treatment gantenerumab failing to meet the primary endpoint of slowing clinical decline in two trials (GRADUATE I and II), or news that crenezumab cannot prevent cognitive decline in people with a genetic mutation associated with the early onset of Alzheimer’s disease.

For 2023, Roche expects sales to decline in the low single digits at constant exchange rates (likely slightly higher on a reported basis), primarily due to declining demand for SARS-CoV-2 testing equipment and COVID-19 therapeutics. The company expects sales of its COVID-19 franchise to decline by CHF 5 billion, essentially a nearly 60% decline, compared to combined 2022 sales of Actemra (CHF 2.7 billion), Ronapreve (CHF 1.7 billion), and SARS-CoV-2 diagnostic devices and consumables (CHF 4.1 billion). As a result, I estimate that Roche’s base business (i.e., excluding the COVID-19 franchise) will grow in the mid- to high-single digits in terms of sales in 2023, already factoring in a projected CHF 1.6 billion decline in Avastin, Herceptin and Rituxan. This suggests that Roche’s underlying business is performing acceptably well, but it’s of course important to keep in mind the company’s focus on oncology biologics. Against the backdrop of solid growth in Roche’s underlying business, it’s hardly surprising that management has – once again – held out the prospect of a further dividend increase in 2024.

What To Make Of The Massive Insider Sale?

A week after 2022 results were published, on February 10, Roche issued a press release explaining that “a member of a shareholder group with pooled voting rights sold 2.7 million Roche bearer shares” via an accelerated bookbuilding process – de facto overnight. While the Roche Long Term Foundation acquired 20% of these shares, which are held as treasury stock and used for stock-based compensation purposes, it’s hardly surprising that the transaction had a material negative impact on the stock. While the non-voting equity securities (and thus RHHBY ADRs) fell only marginally, Roche bearer shares, which were trading at over CHF 330 the day before the transaction, opened around 7.5% lower the next day. Due to the ongoing selling pressure, which is probably attributable to investor uncertainty, the shares are currently trading at CHF 298 (Feb. 15, 2023).

Although the identity of the seller has not been disclosed, it’s speculated that it was Maja Hoffmann, who has a strong commitment to arts and culture and played a leading role in the development of Luma Arles, an arts campus in the southern French city of Arles. For example, she financed the construction of the city’s iconic metal tower designed by star architect Frank Gehry (seen in the main image of the article). From this point of view, and given her reputation as an art collector and philanthropist, the transaction, valued about CHF 830 million (CHF 307 per share, about $900 million), is not overly suspicious. Nevertheless, it should be remembered that the Hoffmann-Oeri clan was known for always acting together as a group of shareholders, and this transaction definitely represents a violation of that long-standing practice. It can be theorized that the clan is slowly but surely reducing its involvement – after all, the transaction represented 2.5% of the total number of voting securities currently outstanding (approximately 107 million).

However, while the size of the transaction is concerning in theory, I would counter that Roche bought back and cancelled over 55 million voting shares from Novartis not too long ago. Prior to the transaction, the Hoffmann-Oeri clan controlled a total of 45% of the voting shares (72 million out of a total of 160 million). Maja Oeri, a former member of the voting pool, owns a further 8.1 million shares, representing 5.1% of the voting rights. As a result of the buyback from Novartis and subsequent cancellation of the shares, the voting rights held by the Hoffmann-Oeri clan increased to 67.5% and those held by Maja Oeri to 7.6%. Therefore, even though the sale of 2.7 million shares was certainly a significant transaction, I would not over-interpret it, as Hoffmann-Oeri’s share of the voting rights has only declined to about 65%, which is still significantly higher than before the Novartis transaction. Personally, I have no doubt that the Hoffmann and Oeri families still have an interest in being majority shareholders, also in view of the appointment of Thomas Schinecker to succeed Severin Schwan as CEO of Roche.

Valuation Update And Conclusion

I don’t think Roche’s quality as a company can be questioned after another solid year. Granted, the company is currently a bit over-reliant on antibody-based cancer therapeutics, but this concentration risk is very visible at the moment and therefore likely reflected in the share price. Also, as mentioned earlier, I doubt that there are any deep-rooted uncertainties about the company’s ownership structure, and instead I think it’s only reasonable to view the significant insider transaction in light of the philanthropic involvement of Maja Hoffmann, who is known to be engaged in large projects – assuming, of course, that she was the one who sold the shares.

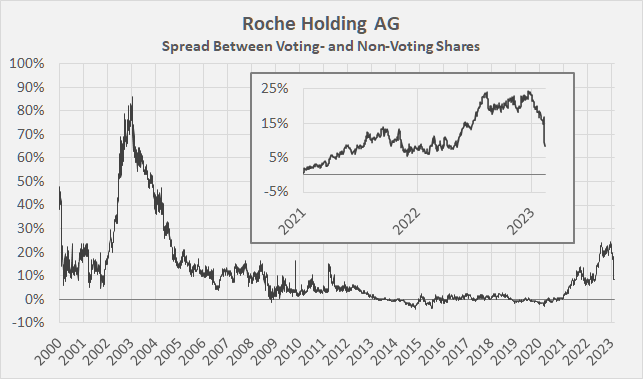

Therefore, I see the drop in the share price as an opportunity to re-evaluate the stock. Previously, I had concluded that Roche was a somewhat inferior stock compared to Johnson & Johnson from a dividend growth standpoint, but it’s still a well-managed company and the market leader in diagnostics and also in biotechnology (through Genentech). Given that the inexplicable spread between the non-voting and the voting securities has narrowed as a result of the significant insider transaction (currently a 9% premium, Figure 2), I think it’s now safe to also own Roche through the voting shares.

Figure 2: Historical spread between Roche’s voting and non-voting shares (own work, based on the daily closing share prices of RO and ROG on the SIX Swiss Exchange)

At a current price of CHF 280 for the non-voting equity securities or CHF 300 for the bearer shares, it’s hard for me to call the stock expensive, but I’m not as enthusiastic as Morningstar, which currently rates the ADR as a five-star opportunity with a fair value of $57 (with upside potential of more than 50%).

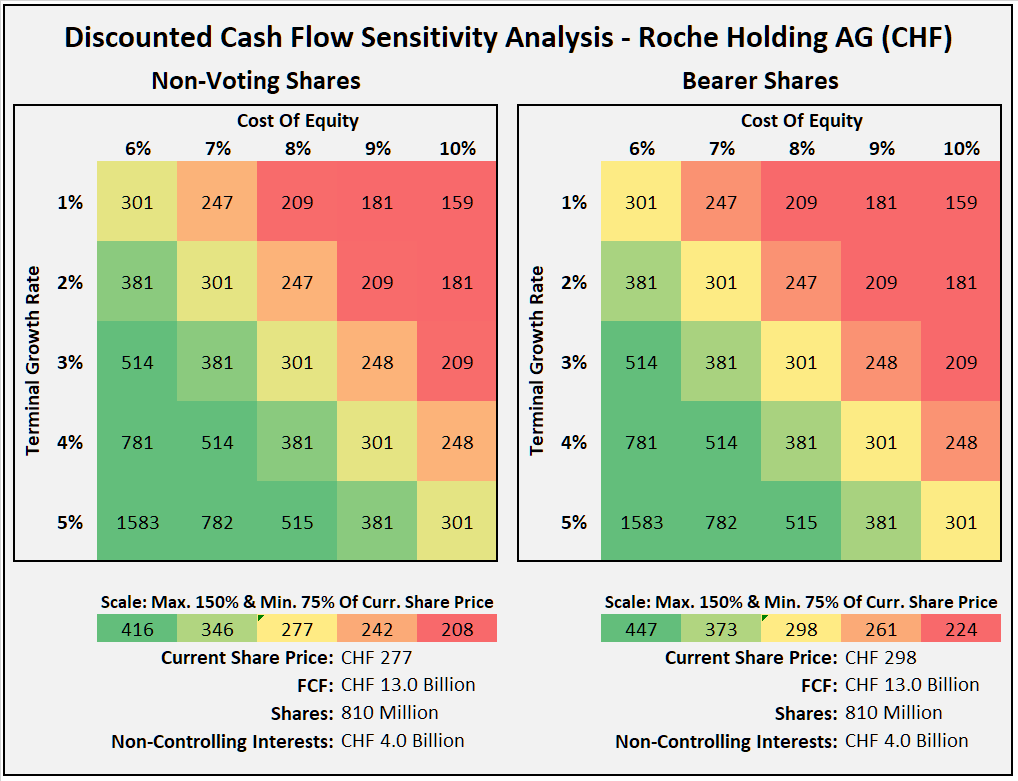

Given the high quality of Roche’s business and solid balance sheet (Aa2 long-term rating with stable outlook), a cost of equity of 8% seems reasonable, not forgetting rising interest rates (higher implied discount rate). Performing a discounted cash flow analysis based on Roche’s average nFCF for 2020-2022 and a 3% terminal growth rate, the stock would currently be fairly valued from the perspective of a potential owner of the voting shares (Figure 3). The non-voting shares currently trade at a discount of about 8% to the bearer shares. The ADRs, equivalent to 1/8 of a non-voting share, are currently trading at $37.5, and the same conclusion applies as for the non-voting shares – the stock is trading at a slight discount to fair value, assuming a cost of equity of 8% is considered reasonable and Roche can grow its nFCF by 3% per year in perpetuity. Of course, the Swiss franc is still quite expensive, so U.S. investors should consider the potential downside risk from a rising dollar. This also would have a negative impact on the investor’s dividend yield on cost, but at the same time Roche’s earnings (reported in CHF) would increase. For completeness, Figure 4 shows the FAST Graphs chart for Roche’s ADRs, which confirms that the stock is also slightly undervalued from an adjusted operating earnings perspective (blended price-to-earnings ratio of 14).

Overall, I still think there are better dividend growth stocks in the healthcare space, but only few with a similar “sleep well at night factor” – such as Johnson & Johnson. I’m very confident in Roche’s long-term prospects, its broadly diversified business (see my previous article), its conservative management, its rock-solid balance sheet, and finally, its strong and reliable free cash flow, so I consider the company to be a very solid long-term investment. Roche’s near-term challenges – overexposure to antibody-based cancer therapeutics and a somewhat weak pipeline – are broadly visible and reflected in the share price. Since I do not view the recent insider transaction as a negative and the spread between voting and non-voting shares is no longer significant, I have decided to start building a position in voting shares of Roche. I acknowledge that the spread may narrow further in the coming months, as there is no real justification for a premium due to concentrated ownership. Also, the Swiss franc may depreciate somewhat against the euro and the U.S. dollar. For these reasons, I’m building my position rather slowly, also keeping in mind that with the resurgence of speculation in ultra-high duration growth stocks, “safe haven” value stocks could come at least somewhat under pressure.

Figure 3: Discounted cash flow sensitivity analysis for Roche Holding AG from the perspective of the owner of voting and non-voting shares (own work, based on the 2022 annual report, the February 15 closing share prices of RO and ROG on the SIX Swiss Exchange, and own calculation of free cash flow)

![FAST Graphs chart for Roche’s ADRs [RHHBY]](https://static.seekingalpha.com/uploads/2023/2/15/49694823-1676491409118265_origin.png)

Figure 4: FAST Graphs chart for Roche’s ADRs [RHHBY] (obtained with permission from www.fastgraphs.com)

Thank you very much for taking the time to read my article. Do you agree or disagree with my conclusions? How did you like it, my style of presentation, the level of detail? Also, if there is anything you’d like me to improve or expand upon in future articles, do let me know in the comments section below.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment