MF3d

Investment Thesis

In this comprehensive analysis, I focus on the compelling investment case for Roche Holding AG (OTCQX:RHHBY, OTCQX:RHHBF, OTCPK:RHHVF), an underlying gem in the pharmaceutical and diagnostics industry. My thesis hinges on Roche’s strong position in the healthcare sector, underscored by its innovative solutions in critical areas like oncology and diagnostics. The company’s successful navigation through the COVID-19 pandemic, evidenced by its effective diagnostic tools and treatments, reinforces its adaptability and commitment to global health challenges.

Financially, Roche’s resilience is a key highlight. Despite the pandemic’s impact, the company has shown impressive growth, particularly in its pharmaceutical division, driven by new, market-leading medicines. This, coupled with the diagnostics division’s strategic focus and adaptability in a shifting market landscape, exemplifies Roche’s solid business foundation.

Roche’s strategic collaborations, such as with Nvidia, and key acquisitions, like Telavant Holdings, signal its forward-looking approach in the evolving field of healthcare, particularly in AI and new treatment avenues. While aware of potential risks like regulatory challenges and currency fluctuations, I maintain a bullish stance on Roche. Its robust financial performance, strategic initiatives, and innovation-driven growth trajectory make it an attractive investment opportunity.

Introduction

Roche Holdings is a global leader in the pharmaceutical and diagnostics industry, primarily focused on advancing science to improve people’s lives. The company’s core business involves researching, developing, and delivering a wide range of innovative healthcare solutions. Roche’s pharmaceutical division concentrates on therapeutic areas such as oncology, immunology, infectious diseases, ophthalmology, and neuroscience. Additionally, the company is a pioneer in in-vitro diagnostics and tissue-based cancer diagnostics, as well as a frontrunner in diabetes management. Roche is also deeply involved in the fight against COVID-19, offering both diagnostic tools and treatments. With a strong commitment to research and development, Roche strives to address unmet medical needs and contribute to the global healthcare system’s evolution. The company’s extensive portfolio, cutting-edge research, and significant contributions to medical science and healthcare underscore its prominent position in the industry.

Current Financials

In evaluating Roche’s current financial performance, the recent third quarter sales webinar for 2023 unveiled some encouraging figures that reinforce my positive outlook on the company. Let’s dive into the specifics that shape my buy thesis.

For starters, the group’s growth of 1% at constant exchange rates, despite the ongoing COVID-19 pandemic, signals a resilient and adaptable business model. It’s noteworthy that excluding COVID-19 related sales, the growth rate jumps to an impressive 9%. This growth is a testament to the company’s strong underlying performance, which outshines the temporary boost from pandemic-related sales.

A key highlight is the Pharma division, which grew 9% at constant exchange rates, with newer medicines as pivotal growth drivers. The success of VABYSMO and POLIVY particularly stands out. VABYSMO, expected to reach annual sales above Swiss Franc (CHF) 2 billion (1 CHF is 1.13 USD), and POLIVY’s rapid uptake in the U.S. following FDA approval, showcase Roche’s ability to innovate and capture significant market share swiftly.

The Diagnostics division also deserves praise, growing at 7% year-to-date in constant exchange rates, outperforming the market. The division’s agility in navigating the reduction in COVID-19 sales (anticipated to decline by CHF 4.5 billion) and AHR biosimilar erosion (about CHF 1.1 billion) is commendable. Their strategy to focus on core business growth amidst these headwinds aligns with a sustainable growth trajectory.

Roche’s achievements in the third quarter, like the approval of TECENTRIQ in subcutaneous formulation and EU approval for Evrysdi, further bolster my confidence. Also, ELEVIDYS, a first-of-its-kind gene therapy for Duchenne muscular dystrophy, has gained approvals in two global markets, with imminent Phase III EMBARK study results. These milestones demonstrate the company’s sustained innovation and ability to secure regulatory approvals, vital for long-term growth.

However, it’s essential to maintain a balanced view. The negative impact of COVID-19 sales tapering off and the ongoing currency headwinds, especially in Q3, are factors that require careful monitoring. These challenges, though significant, seem manageable given Roche’s robust base business performance.

In conclusion, Roche’s current financials paint a picture of a company adept at navigating market challenges, leveraging its innovative capabilities, and maintaining a steady growth trajectory. While being mindful of the evolving healthcare landscape and market risks, I support and reaffirm my buy rating for Roche, expecting the company to continue its strong performance.

Forward Guidance

The forward outlook for Roche appears exceptionally promising, particularly in light of recent developments. At the core is my belief that Roche’s strength lies in its robust growth in both pharmaceuticals and diagnostics, diversified portfolio, and a solid pipeline of potential blockbuster drugs. Notably, the company’s Q3 results demonstrated a remarkable 9% growth at constant exchange rates, excluding COVID-19 impacts, showcasing the inherent strength of its core business.

Of particular interest are the two drugs I previously mentioned, VABYSMO and POLIVY, which are key growth drivers in Roche’s portfolio. VABYSMO, expected to exceed CHF 2 billion in annual sales, and POLIVY, especially in its first-line diffuse large B-cell lymphoma application, have seen rapid uptake in the U.S. and other countries. This is a testament to Roche’s ability to innovate and capture significant market share in key therapeutic areas.

In terms of management’s perspective, CEO Thomas Schinecker’s comments are enlightening. He highlights the performance across different parts of the group, emphasizing the strong base business growth in diagnostics and the impressive performance of newer pharmaceutical products. This aligns with Roche’s strategy of focusing on innovative medicines and diagnostics, which is key in this industry, while also reassuring growth to investors.

The positive Phase II KARDIA-1 results for zilebesiran in hypertension, alongside other important drug readouts and diagnostics launches, further reinforce Roche’s potential for sustained growth. The company’s guidance, anticipating sales at the upper end due to strong base business growth, despite the headwinds, is another factor of an optimistic outlook. Management also noted that even dividends will increase in Swiss francs.

In conclusion, my investment thesis for Roche in 2023 is underpinned by its strong growth in core areas, successful navigation of market challenges, and a promising pipeline. The company’s strategic focus on innovative healthcare solutions, coupled with effective management and a diverse portfolio, positions it well for future success.

The Big News

As I reflect on the recent groundbreaking collaboration between Genentech, a biotechnology subsidiary of Roche, and Nvidia, it’s clear that this partnership marks a significant leap in the realm of drug discovery and development. I believe Roche Holdings will benefit greatly. This collaboration, underpinned by Nvidia’s AI supercomputing and Genentech’s proprietary machine learning algorithms, isn’t just a mere business transaction; it’s a fusion of technological prowess and biomedical ingenuity, poised to revolutionize how we approach healthcare challenges.

During a recent discussion with Kimberly Powell, Nvidia’s Vice President and General Manager of Healthcare, her insights illuminated the profound implications of this alliance. Powell’s journey, which traversed from electrical and computer engineering to healthcare technology, mirrors the interdisciplinary nature of this collaboration. Her experience reveals the transformative power of accelerated computing in healthcare, a domain traditionally constrained by the limits of conventional computing technologies.

Nvidia, initially renowned for its graphics processing capabilities, evolved into a leader in accelerated computing, a transformation pivotal for healthcare advancements. The company’s early forays into medical imaging, using accelerated computing for complex computations required by diagnostic imaging devices, laid the foundation for today’s advancements in AI-driven healthcare solutions. This journey from graphics to healthcare is emblematic of the innovative spirit driving Nvidia, a spirit now synergizing with Genentech’s cutting-edge biotechnological research.

The significance of Nvidia’s role in genomics, particularly in partnership with Oxford Nanopore, cannot be overstated. Their work in AI and deep learning has unlocked new possibilities in genomics, a field critical for understanding and treating myriad health conditions. Genomics, once bottlenecked by data-intensive and time-consuming processes, is now being propelled into a new era of efficiency and precision, thanks to Nvidia’s AI capabilities.

DeepMind’s AlphaFold represents another landmark in AI’s role in healthcare. By enabling rapid, accurate predictions of protein structures, AlphaFold has democratized access to information once deemed unattainable, fueling discoveries across the globe. This advancement is not just a technical triumph but a beacon of hope for accelerating drug discovery processes, which have traditionally been laborious and costly.

The collaboration between Genentech and Nvidia exemplifies a new paradigm in drug discovery, where AI and machine learning are not just tools but foundational elements driving innovation. This partnership is set to optimize Genentech’s “lab in a loop” system, integrating experimental data with computational models to uncover new patterns and predictions. Such integration is a testament to the potential of AI in transforming drug discovery from a hit-and-miss endeavor to a more precise, predictable, and efficient process.

Moreover, this collaboration isn’t just about enhancing existing processes; it’s about reimagining what’s possible in healthcare. By harnessing Nvidia’s AI supercomputing and Genentech’s machine learning algorithms, we’re not just looking at incremental improvements in drug development; we’re witnessing the dawn of a new era in healthcare, where the convergence of technology and biology could lead to personalized medicine and treatments unimaginable a few years ago.

The Genentech-Nvidia collaboration is more than just a strategic business move; it’s a confluence of vision, technology, and expertise that promises to redefine the boundaries of healthcare and drug discovery. I encourage those who want to be ahead of the future of healthcare to see this partnership as a signal of innovation. This is an investment opportunity to consider since this world is ever-evolving in the landscape of technology and healthcare, and in this case, to better human health.

Additionally, another media release that I wanted to mention is the acquisition of Telavant Holdings by Roche, valued at $7.1 billion, which represents a strategic and promising move for Roche. This acquisition grants access to RVT-3101, an innovative therapy for inflammatory bowel diseases, including ulcerative colitis and Crohn’s disease. What makes this deal particularly compelling is RVT-3101’s unique approach, targeting both inflammation and fibrosis, suggesting its potential application across a spectrum of diseases beyond just bowel disorders. Owning full development, manufacturing, and commercialization rights in key markets like the U.S. and Japan, Roche stands to significantly bolster its portfolio in the high-need area of inflammatory diseases. Additionally, the possibility of a global collaboration with Pfizer on a next-generation therapy underlines the forward-looking and growth-oriented strategy Roche is adopting. This deal not only enhances Roche’s competitive edge but also hints at long-term growth potential, reinforcing my ‘buy’ thesis for Roche’s stock.

Risks

The recent FDA warning letter addressed to a clinical investigator working on Roche’s Phase 3 study for XOFLUZA introduces some risks to the development and potential approval of this antiviral drug. The FDA’s concerns about the adherence to the investigational plan, particularly around subject eligibility testing, raise questions about the integrity and reliability of the study’s results. Moreover, the lack of sufficient oversight and detailed corrective actions by the investigator further complicates the situation, potentially leading to delays in the study’s progression or even jeopardizing its continuation. This issue not only poses a risk to Roche’s immediate project timelines but also reflects on their broader clinical research practices. I recommend watching how Roche addresses these compliance issues going forward, as their resolution or persistence will impact investor confidence and the company’s ability to bring new drugs to market efficiently.

Following, in my assessment, the currency headwinds Roche faces, as detailed in the Q3 report, present a tangible risk. The Swiss franc’s strength, particularly against the U.S. dollar and other major currencies, has unfavorably impacted sales figures, translating to a stark 7.3 percentage point discrepancy when comparing constant exchange rates to actual reported sales. This volatility can obscure the company’s true operational performance.

On the flip side, Roche’s CFO has addressed this issue, pointing to a robust natural hedge within the company’s financial structure. With substantial operations and costs also in these currencies, the impact is somewhat mitigated at the operational level, suggesting that while reported figures are affected, the underlying business health remains solid.

Valuation

In my considered view, the valuation metrics from Seeking Alpha offer a compelling case for a buy thesis on RHHBY. Starting with the forward Price to Earnings (P/E) ratio, which stands at a robust 15.39 against the sector median of 26.93, we’re looking at a stock that is undervalued relative to its peers – an A- grade from Seeking Alpha underscores this strength. This lower P/E ratio could indicate that the stock is currently priced at a discount to its intrinsic value, considering future earnings, which signals a strong buy opportunity for value investors.

Diving into the Price to Cash Flow (P/C) metric, the company is again below the sector average at 13.90, compared to 16.12, and a B grade here indicates a healthy cash flow situation relative to its price. This is significant because it suggests that the company is generating more cash flow relative to its stock price than other companies in the sector, potentially offering a more stable investment.

The Total Trailing Twelve Months (TTM) Dividend Yield presents an even more attractive aspect of the stock, standing at a solid 3.78%, vastly outperforming the sector median of 1.74%. An A grade for dividend yield reflects not just the stock’s current income-generating capability but also the potential for future dividend growth, a critical factor for income-focused investors.

Lastly, the forward Price to Sales (P/S) ratio of 3.25, with a B- grade, is slightly below the sector median of 3.64, hinting again at potential undervaluation. Sales are the lifeblood of any company, and a lower P/S ratio may suggest that the stock’s market price has not yet caught up to its sales potential.

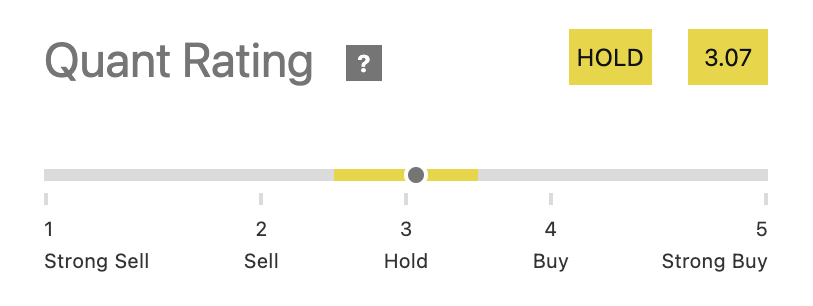

However, as depicted below, the Quant Rating describes a Hold with a score of 3.07. This is an alternative perspective to contrast how I have evaluated the company; I simply want to give you more light on the story for consideration.

Quant Score (Seeking Alpha)

Overall, in comparison to its sector, I believe the stock stands out across multiple financial health indicators, suggesting a more conservative and potentially undervalued pricing. These metrics paint a picture of a company that is not only fundamentally solid but also possibly overlooked by the market at present, especially with the Nvidia partnership potential. Such a discrepancy between the company’s strong fundamentals and its market valuation could provide a strategic entry point for investors. It’s these nuances in the valuation metrics that, in my opinion, make this stock an attractive buy.

Conclusion

I firmly believe that Roche Holdings stands as a formidable player in the pharmaceutical and diagnostics industry. The company’s innovation in key areas such as oncology and diagnostics, combined with its resilience during the COVID-19 pandemic, illustrates its strong position in the healthcare sector. Financially, the company has displayed impressive growth and adaptability, particularly in its pharmaceutical division, underpinned by groundbreaking medicines. Strategic collaborations with tech giants like Nvidia and significant acquisitions, including Telavant Holdings, further demonstrate Roche’s commitment to pioneering in healthcare and exploring new treatment avenues. While cognizant of the risks, such as regulatory challenges and currency fluctuations, I remain bullish on Roche. The company’s robust financial health, strategic foresight, continuous innovation, and a reliable partnership position it as an attractive investment opportunity with great upside. Roche’s journey reflects a blend of scientific excellence and visionary leadership, making it a compelling choice for investors looking toward the future of healthcare.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment