AntonMatveev

RBC Bearings (NYSE:RBC) manufactures precision bearings internationally. RBC recently posted its Q2 FY24 results with a decent growth in sales. I believe it has good growth potential once the softness in the industrial market passes, which might take some time. However, for now, I have a hold rating on RBC, considering the valuation and the technical chart.

Financial Analysis

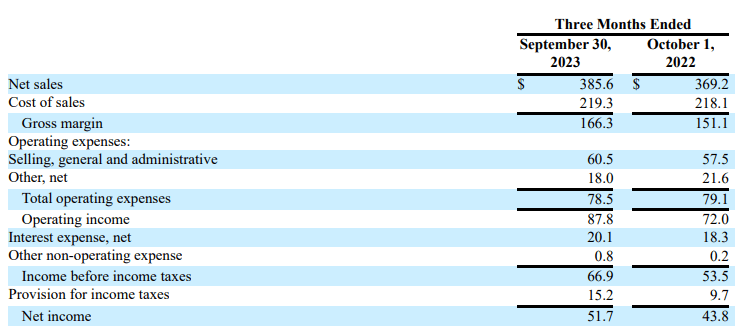

RBC recently announced its Q2 FY24 results. The net sales for Q2 FY24 were $385.6 million, a rise of 4.4% compared to Q2 FY23. Its aerospace and defense segment saw significant growth, which led to an increase in sales. The net sales from the aerospace segment grew by 22.9% in Q2 FY24 compared to Q2 FY23. The major reason for the growth was improving supply chain and strong OEM demand. The gross margin for Q2 FY24 was 43.1%, which was 40.9% in Q2 FY23. The solid improvement in gross margins was mainly due to better synergy from its Dodge acquisition and better absorption rates.

Seeking Alpha

The net income for Q2 FY24 was $51.7 million, an increase of 18% compared to Q2 FY23. The overall sales growth was positive, but sales in its industrial business, which accounts for 67% of its sales, declined by 2.8%. There are some headwinds in this segment, like the slowdown in the construction and semiconductor market, which is hampering its growth, and no one knows when the slowdown will end. Some experts are predicting the slowdown to last till the end of 2024. So these can hamper its growth in the coming quarters. But other than that, the increased aerospace activity is proving beneficial for them. Its sales growth in the past two years has been impressive, and the management is expecting its FY24 sales to be around $1.6 billion, which is 7.5% higher than FY23. Once the headwinds in the industrial segment perish, then we can see solid sales growth in the future.

Technical Analysis

Trading View

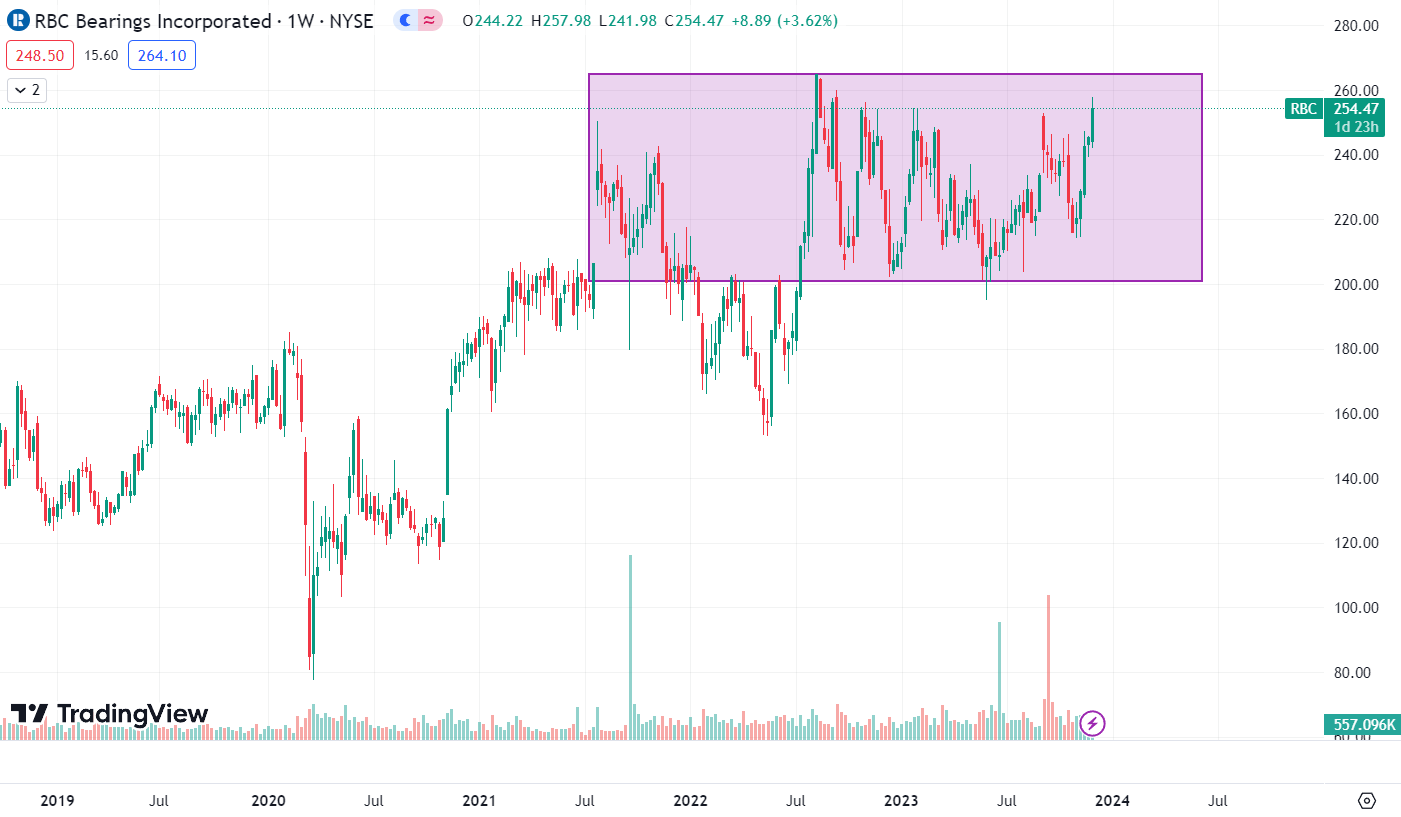

RBC is trading at $254.4. The stock has been consolidating for about two years now in a range of $200-$265. There can be two scenarios where one can buy it. One, if the stock breaks the $265 level, then we can expect fresh buying momentum in the stock, and $265 is also its all-time high, so if the breakout happens, then there will be no resistance level for the stock. So, the stock might give a huge upward target. The second buying opportunity will arise if the stock price reaches the $200 level. The reason I think it might be a good buy at $200 is because the stock has strong support there, and buying it at $200 will be a better idea than buying it at the current level. The reason I am saying this is because no one knows how long the consolidation will last. It can go on for another two years. So, investing at the current price can get investors’ money stuck for a long time without any returns. So unless one of the two scenarios that I mentioned happens, I think one should avoid investing in it.

Should One Invest In RBC?

First, if we look at RBC’s valuation, RBC has a P/E [FWD] ratio of 27.96x compared to the sector median of 17.36x. It is trading at a higher multiple than the sector, and I think it can trade at an even higher multiple in the future than it is now once its industrial segment comes back on track. Once it happens, the growth it might experience can be solid, and, in my opinion, high-growth companies trade at a higher valuation than other companies. But for now, I think there is no buying opportunity in RBC, considering its current valuation and stock price. I am assuming high growth once the headwinds in the industrial segment pass, which can take time, and its stock price is at that level where it provides no opportunity. So, for now, I am assigning a hold rating on RBC.

Risk

In fiscal 2023, 2022, and 2021, the top 10 customers constituted around 41%, 36%, and 36% of their net sales, respectively. As a result, a significant decline in their sales, cash flows, and profitability may arise from the loss of one or more of those clients or from a marked drop in their purchases. One of their main clients could stop making purchases from them if there was a negative shift in their business.

The combined efforts and merger of manufacturers may result in the loss of clients and/or exert downward pricing pressure on component part sales. For instance, the number of defense contractors overall has decreased as a result of the recent consolidation in the defense business. Furthermore, in the event that one of their clients is bought out or combined with another company, the newly created company might stop doing business with them as a supplier due to an existing business arrangement between one of their rivals and the acquiring company or because it might be more cost-effective to combine some of their suppliers into the newly created company. It’s hard to say how big of an impact these consolidations might have on their business.

Bottom Line

RBC posted decent results despite softness in the industrial market. I think once the headwinds pass, the growth might accelerate, but it might take time. In addition, the stock price is at that level where investing might get your money stuck for a long time. So, for now, I have a hold rating on RBC.

Be the first to comment