Spencer Platt

Thesis

Market excesses seen in 2021 are coming back to haunt the speculative investor. Arguably few companies incorporate the COVID-bubble as well as Robinhood (NASDAQ:HOOD), the brokerage firm on a mission to democratize finance.

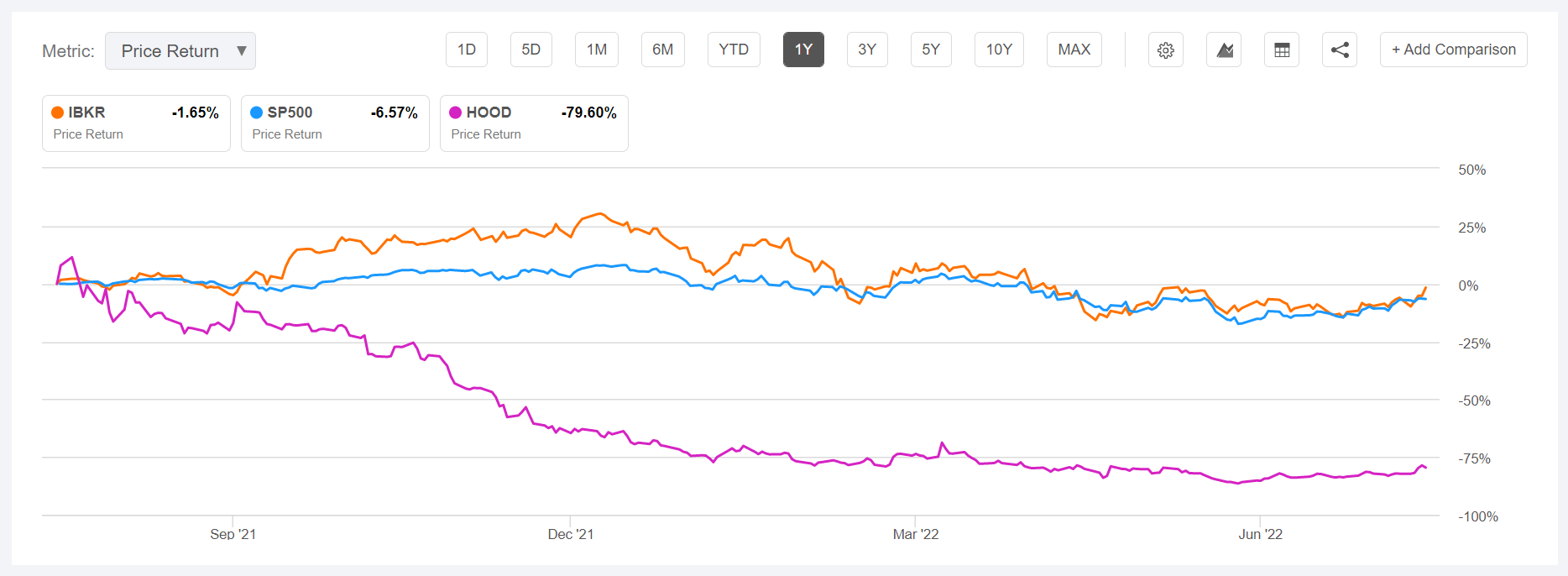

Robinhood is down more than 80% for the trailing twelve months. But don’t let the drawdown fool you: Robinhood stock is still trading expensive at about x5 Price-to-Sales. And as the company’s Q2 results have shown, this stock will likely go even lower.

Seeking Alpha

Looking at Robinhood’s financials, it is hard not to be bearish on the company’s stock. Assuming that a stock brokerage firm is fairly valued at about x1 Price-to-Book, I see 30% more downside. Moreover, I argue that the conservative investor should be looking to buy Robinhood, if a purchase is reasonable at all, at a 30% discount to the fair sector multiple.

The Hangover After The Boom

Robinhood has been enormously successful in 2020 and 2021, as the COVID-induced stay-at-home trend paired with government stimulus checks and paired with a booming stock market has induced many retail investors to become stock market investors and traders. The boom was fueled by the Reddit meme-stock mania that saw companies such as GameStop (GME), AMC (AMC) and Bed Bath & Beyond (BBBY) surge by multiple thousand percentage points. Given a no-commission trading promise and a gamified mobile-firs platform, many new investors joined Robinhood.

But since then, the stock market has tanked, the crypto boom has arguably ended, and investor sentiment has soured, with a vengeance that rivals the intensity of the initial boom. CEO Vlad Tenev commented:

We have seen additional deterioration of the macro environment, with inflation at 40-year highs accompanied by a broad crypto market crash.

Moreover, Robinhood has experienced regulatory and government scrutiny: Only recently, the company has been fined with a $30 million liability

for significant failures in the areas of bank secrecy act/anti-money laundering obligations and cybersecurity.

At the same time, the SEC is reflecting on a proposal that could significantly pressure Robinhood’s business model ‘payment for order-flow’, which is a monetization strategy where brokerage firms like Robinhood are paid fees from market makers such as Citadel Securities to allow them to execute the transaction.

Disastrous Q2 Results

Robinhood reported Q2 2022 results on August 2nd after market and the company strongly disappointed. During the period from April to end of June, Robinhood reported total revenues of $318 million, which represents a decrease of about 44% as compared to the same period one year prior. Topline is also below analyst consensus, which had expected $321 million of revenues.

The brokerage firm’s asset under custody plunged 31% to $64.2 billion (QoQ). Robinhood’s payment for order flow exposure is still significant, with $202 million accounting for almost two thirds of the company’s total revenue.

Although the company has narrowed net loss, investors should note that Robinhood is still not profitable. For the period, Adjusted EBITDA (non-GAAP) was negative $80 million. Robinhood’s net loss for the quarter attributable to shareholders was $295 million, improved from a loss of $502 in Q2 2021. The net loss per share was $0.34.

Given that the challenging macro-environment is likely to persist, guidance is not rosy either:

GAAP total operating expenses for full-year 2022 to be in the range of $2.46 billion to $2.60 billion, representing a decrease of approximately 25% to 29% from the prior year;

total operating expenses, excluding share-based compensation, for full-year 2022 to be in the range of $1.70 billion to $1.76 billion, representing a decrease of approximately 7% to 10% from the prior year. (These amounts include severance and other restructuring charges of $17 million in connection with the April 2022 Restructuring and an estimated $45 million to $60 million in connection with the August 2022 Restructuring); and

share-based compensation for full-year 2022 to be in the range of $760 million to $840 million, representing a decrease of approximately 47% to 52% percent from the prior year. (These amounts include the benefit of share-based compensation reversal of $24 million in connection with the April 2022 Restructuring and an estimated share-based compensation reversal of $40 million to $50 million in connection with the August 2022 Restructuring.)

Investors should note that share-based compensation in 2022 represents a shareholder equity dilution of almost 10% of the company’s market capitalization.

Still Overvalued

Despite the negative sentiment surrounding Robinhood stock, and despite the 80% sell-off YTD, I argue that HOOD is still trading very expensive. For reference, the company is valued at a one year forward P/S of x6.7, which is more than 100% premium to the sector. One year forward P/B is x1.3, a 10% premium respectively.

Given the company’s non-existent profitability (1), legal challenges (2) and exposure to the low net-worth retail investor (3), how could an investor possible justify a premium for HOOD? In my opinion, the company should trade at (at least) at a 30% sector discount in order to provide a balanced risk/reward. And I see the fair sector multiple at x1 P/B.

Thus, according to my estimation, I see about 50% downside for HOOD (30% to get to x1 P/B, multiplied by a 30% discount — 0.7*0.7 mathematically)

Accordingly, my target price for the stock is about $5.1/share.

Risks To My Thesis

The major risk to my thesis is, in my opinion, that somehow the market rediscovers his risk-seeking attitude, and hence speculative stock trading becomes fashionable again. If this were to be the case, Robinhood’s trading business would likely be a key beneficiary. Personally, however, I see a continuation of the bull-market as unlikely. Or at least, I do not expect that this scenario will be a major risk within the next 6-12 months.

Conclusion and Recommendation

In my opinion, Robinhood is a clear sell. Not only is the company trading expensive, but also the perceived justification for a premium (retail trading boom) has faded. Moreover, Robinhood is not profitable and regulatory scrutiny will likely pressure the company’s business model going forward.

To compensate for the risk, I argue that Robinhood should trade at a 30% discount to the fair industry P/B ratio, which I estimate at x1. Accordingly, my target valuation for the company is x0.7 P/B, which translates into $5.1/share.

Be the first to comment