24K-Production

Robinhood (NASDAQ:HOOD) has since its July 2021 IPO gone full circle as far as investor sentiment is concerned. It was hyped during the IPO as the next big darling of Wall Street but its stock has in the quarters that followed steadily lost value due to growing concerns over its weakening fundamentals and gloomy outlook.

At least this is how I view the overall HOOD investment case given my disposition as a long-term oriented investor looking for qualities such as growth, improving margins, a moat and strong business case, capital returns to shareholders, healthy cash flows, and a strong balance sheet, among other important fundamental qualities.

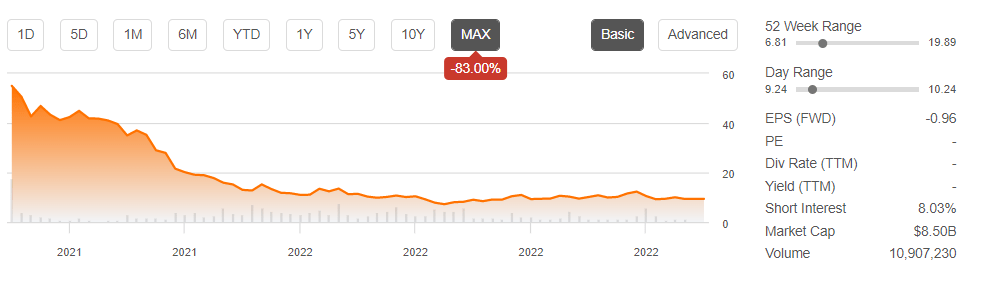

HOOD has enjoyed favorable publicity and admiration (mixed with some criticism) for its role in making financial markets more accessible to armies of newbie retail investors. It has sadly not drawn the same enthusiastic response from investors who, voting with their money, have sold off the stock and generally been ultra bearish, judging by the stock price performance. For all the hype it garnered during its debut as a publicly traded company, HOOD is one of the worst performing IPOs of the last 2 years, having lost more than 80% to date.

HOOD is one of the worst performing IPOs in the last 2 years (Seeking Alpha)

It’s ironic that the very markets that HOOD has diligently worked to make more accessible to retail investors have decidedly turned against it. HOOD went public at a valuation of $32 billion in mid-2021, rapidly shot to a market cap of around $60 billion in the initial few weeks following the hyped IPO, but then started declining persistently. As a sign of the sour investor sentiment surrounding the stock, HOOD lost all its IPO gains in less than two quarters of going public and has, since November 2021, been on a sustained freefall. It currently sports a market cap of around $8.50 billion, just 25% of what the market valued it when it went public.

Such a precipitous fall merits a closer look. There are two possibilities to consider when dealing with a stock that has fallen this much. The first one is the possibility of a market overreaction. Perhaps something about the business has been fundamentally misunderstood by investors and the stock is a great bargain. The opposing viewpoint is that perhaps there are underlying issues of a chronic and progressive nature that are adversely affecting the business and that the management cannot realistically address. Buying the stock in the latter case would be a great mistake as, regardless of how much it has fallen, it could still continue falling as it struggles to get new bulls.

It’s important to have your own methodology of arriving at conclusions about the fundamentals of a business like HOOD whose stock has been consistently underperforming. I personally use the following three questions as an initial framework to assess whether or not it’s worth investing in a beaten down stock.

-

What is the state of the industry and what are the company’s growth prospects?

-

Where is the cash to fund operations and meet obligations coming from?

-

Is the company facing external risks with outsized potential impacts?

In subsequent paragraphs I share a brief analysis of how, in my opinion, HOOD scores against these questions. In summary, it scores very poorly on all three. It’s important to state at this point that, going into 2023, the outlook looks worse for the company.

Current operational headwinds cause for concern

When it comes to the state of the industry and the company’s growth prospects, HOOD faces operational headwinds that dim its growth prospects. HOOD’s platform allows users to invest in stocks, exchange-traded funds (ETFs), options, gold, and cryptocurrencies. This is nothing new or revolutionary. Fidelity, Vanguard and a host of other players have been offering this service for decades to millions of retail investors in the US and internationally. HOOD’s only differentiator in this low margin, highly competitive business is its commission-fee model. It basically has no moat.

Moreover, the outlook for future growth isn’t encouraging at the moment. Retail investors, who are HOOD’s target market, are on the whole not as enthusiastic about the markets right now as they were during the speculative frenzy that gripped markets in 2020 and 2021, roping in millions of newbie investors hoping to strike it rich fast with meme stocks, crypto and other risky bets.

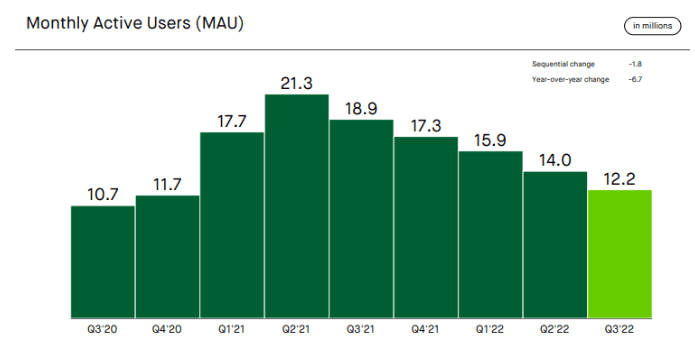

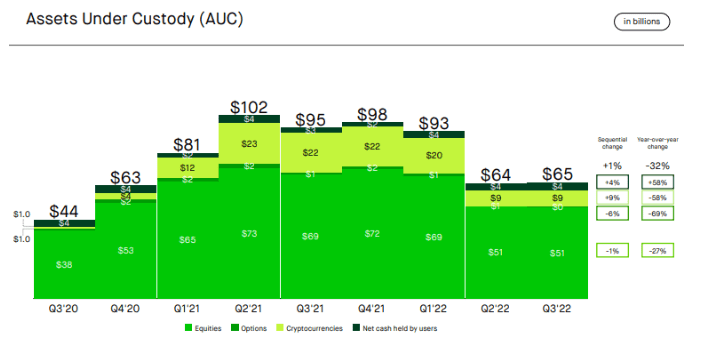

The decline in retail investor interest in 2022 is understandable in view of the inflationary environment, interest rate hikes and weak returns on equities witnessed through the year. In line with this trend, HOOD’s latest operational results paint a picture of a business in decline or struggling to reverse a decline (depending on where you sit on the glass half full/half empty debate). The charts below, drawn from its latest earnings presentation, illustrate this.

HOOD Q3 2022 Earnings Presentation HOOD Q3 2022 Earnings Presentation

HOOD is essentially losing monetizable customers (its revenue generation plans such as selling order flows depends on having an engaged user base). It is further selling a commoditized product in an industry experiencing a cyclical downturn for that target market. Stock market conditions are still not conducive for a roaring comeback of the retail investor, 15% of who got their start in 2020.

Reckless Stock Based Compensation policy

HOOD is a loss making entity so it funds its operations through its creditors and shareholders. Think about this: in 2021, HOOD tapped into its share registry and “withdrew” shares worth $1.57 billion. This is what is recorded as the share-based compensation expense for that year. This “withdrawal of shares” is the best way to frame the discussion on stock based compensation, a practice that can silently wipe off long term shareholders if done recklessly since it increases the share count and dilutes stockholders.

HOOD’s share-based compensation policy is one huge red flag. The company’s share-based compensation expenses for FY2021 of $1.57 billion represent an unbelievable 86% of the $1.82 billion in revenue it made at the time. Talk about a management team who are professional fundraisers. HOOD has sadly continued this destructive stock based compensation trend in 2022.

Crypto contagion

Because of crypto trading, HOOD is also exposed to external risks that could have a disproportionate impact on its performance as a business and a stock. Earlier in November it plunged along with crypto when the FTX saga broke out, losing some 20% in one session at the time.

Moreover, it is reported that embattled FTX CEO Sam Bankman-Fried took out a 7.6% stake in Robinhood worth $648 million in May, according to an SEC filing. His worsening woes could lead to this position being liquidated, further adding downside pressure. HOOD maintains that it has no exposure to FTX but fear is a powerful thing and the last thing any financial institution wants now is association with Sam. The generally bearish conditions in the crypto market also mean HOOD’s own crypto trading revenues will be depressed.

Possible risks to thesis

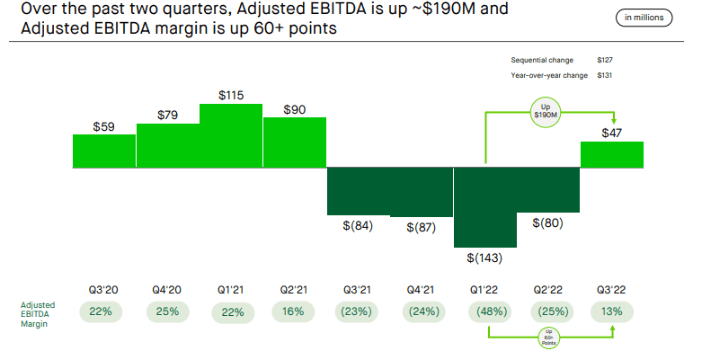

HOOD’s third quarter results show that it could be turning a corner from an operational standpoint as its reported adjusted EBITDA of $47 million, the first positive report in five consecutive quarters.

HOOD’s EBITDA improving (Q3 earnings presentation)

The other factor to consider is that HOOD has a strong balance sheet. It closed the third quarter with more than $6 billion in cash and no debt. Having sufficient capital and liquidity resources in a rising interest rate environment is great for a player like HOOD as net interest revenue earned from this cash can offset weakness in revenues from its trading platform. Tellingly, the company’s net interest revenue jumped to $128 million in Q3 from $74 million in Q2, with the bulk of this growth coming from interest on investments and corporate cash.

If investors bet that these factors are sufficient to turnaround the business, then the stock could reverse its downtrend in 2023. The fact that the Robinhood brand is also highly popular could make the company an acquisition target by a bigger player. This could create some upside potential.

These are some of the reasons why I could be wrong and the stock could actually go up in 2023. However, even though nothing is impossible, not everything is worth betting on. In my opinion, it’s better to keep off this stock for now as the risk outweighs the opportunity.

Be the first to comment