User10095428_393

About four months ago, I wrote that RLJ Lodging Trust (NYSE:RLJ) would be a great stock to buy if the risk of an upcoming recession increased due to the crisis in Ukraine. Since my article, the risk of a recession has increased and RLJ has plunged 17%. The stock needs to decline another 10% to reach the strong technical support of $10. In this article, I will analyze why RLJ will be a great bargain at a stock price around $10 for the investors who can maintain a long-term perspective.

Why the stock has plunged

The shareholders of RLJ have suffered over the last five years. To be sure, the stock has dramatically underperformed the broad market over this period, as it has shed 42% whereas the S&P 500 has rallied 60%.

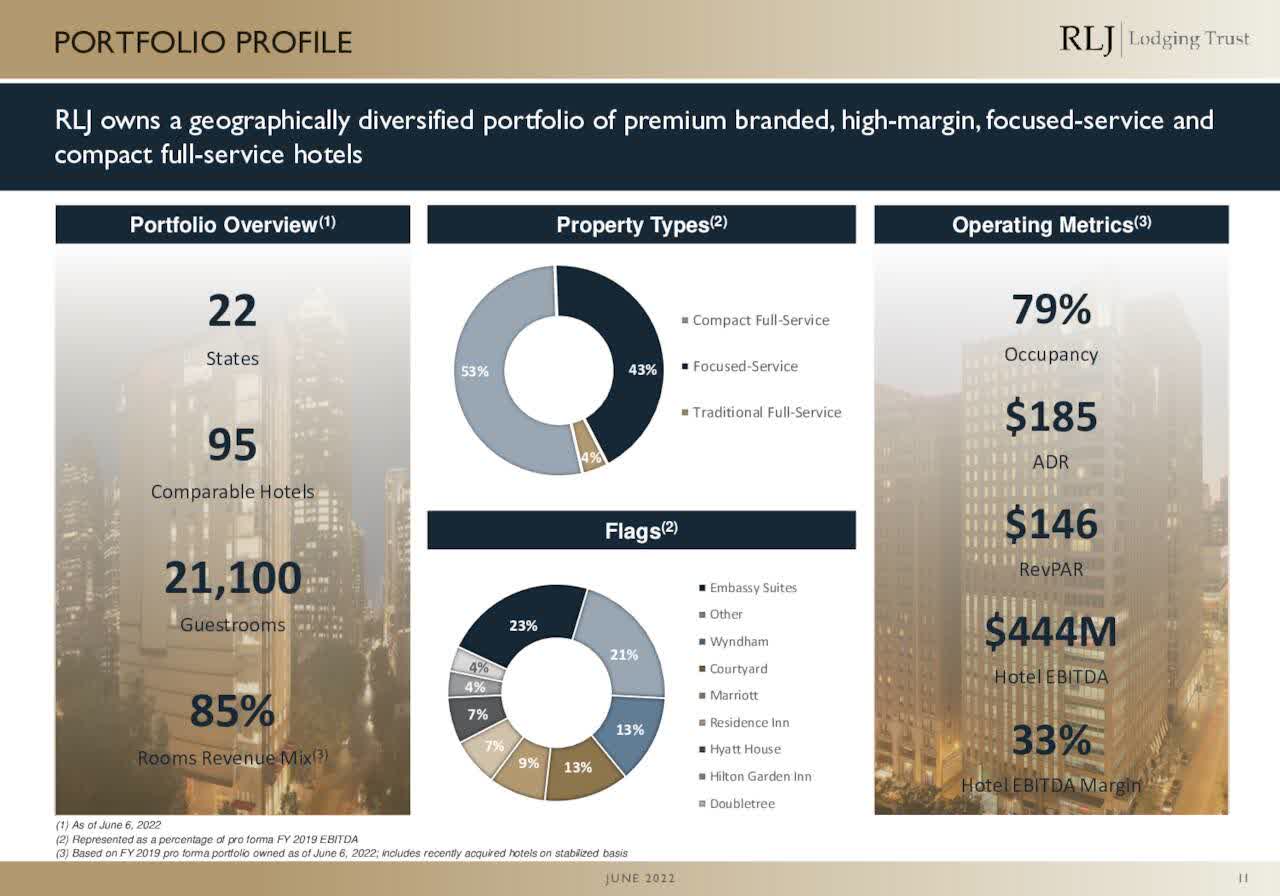

The first reason behind the vast underperformance is the coronavirus crisis. RLJ is a REIT that owns premium-branded, high-margin hotels. It currently owns 95 hotels, with 21,100 rooms in 22 states.

RLJ Lodging Trust Overview (Investor Presentation)

The trust generates 46% of its EBITDA in Sunbelt markets, which are characterized by higher economic growth than the rest of the country, and earns more than half of its earnings from luxury hotels, such as Hilton, Marriot and Wyndham.

The impact of the coronavirus crisis on luxury hotels was severe in 2020 and 2021. Both leisure and business travel collapsed and thus the demand for luxury hotels plunged. The impact of the pandemic was clearly reflected in the business performance of RLJ, which incurred its first loss in more than a decade in 2020. In addition, management cut the dividend by 97% in 2020 and the stock slumped 75% in the first quarter of that year.

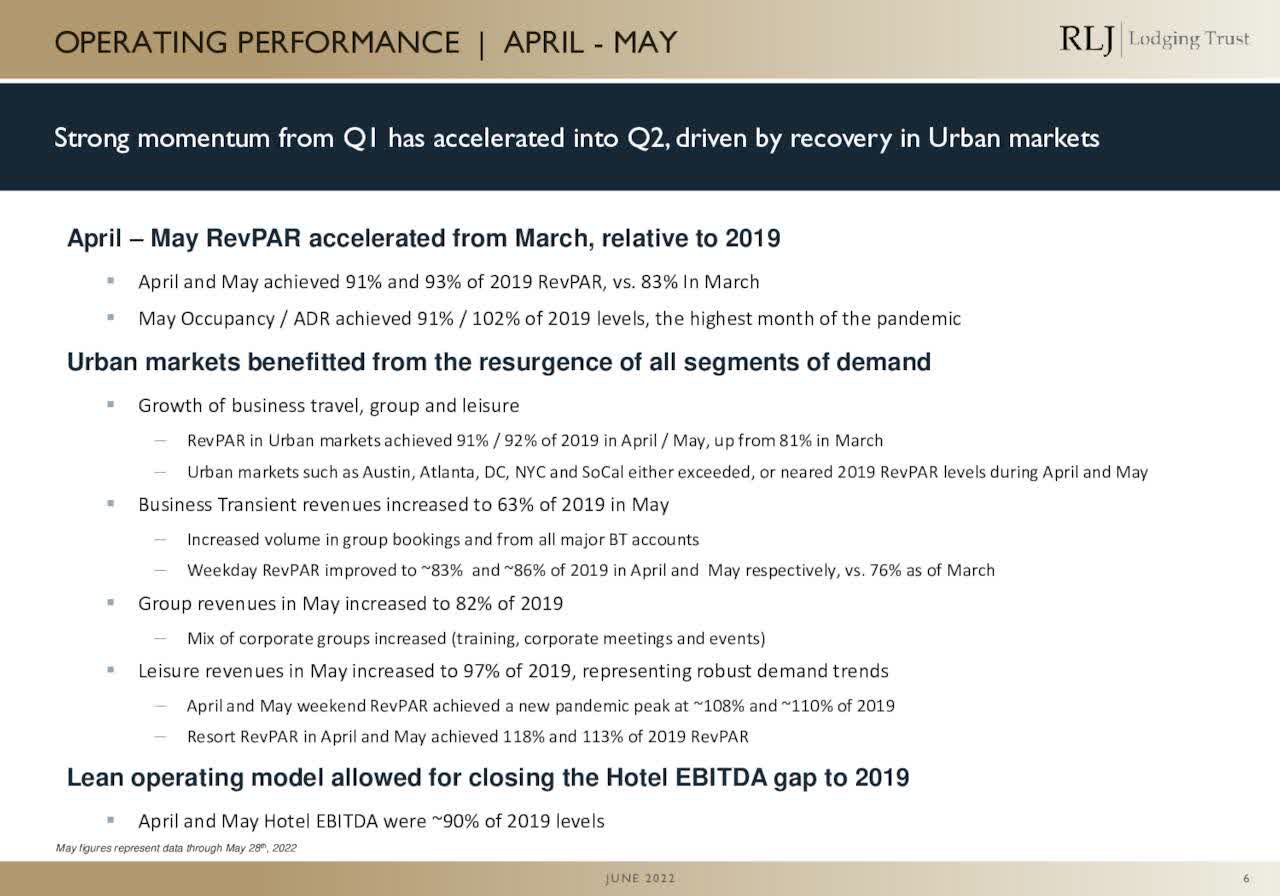

Fortunately, RLJ has begun to recover strongly from the pandemic thanks to the massive distribution of vaccines worldwide and the resultant recovery of leisure and business travel. In April and May, RLJ achieved revenue per available room (RevPAR) that was 91% and 93%, respectively, of the figure reported three years ago, before the pandemic. These two months mark a strong recovery from March, whose RevPAR was only 83% of the level reported in 2019.

RLJ Lodging Trust Recovery (Investor Presentation)

The only factor that still exerts a drag on the performance of RLJ is business travel, which remains significantly lower than it was before the pandemic. Business transient revenues are still 37% lower than they were in 2019. However, the trend is positive, as employees are in the process of claiming back their normal lifestyle.

Analysts seem to agree on this, as they expect RLJ to grow its funds from operations [FFO] per unit from $0.19 in 2021 to $1.39 this year and $1.89 in 2023. If analysts prove correct, then the FFO per unit in 2023 will be just 7% lower than the pre-pandemic level of $2.03.

While the business of RLJ is recovering from the pandemic, the stock has been in a strong downtrend this year due to fears that the aggressive interest rate hikes of the Fed in response to high inflation may cause a recession. Indeed, if a recession shows up, RLJ will be vulnerable due to the luxurious nature of its hotels.

However, even in the adverse scenario, a recession will not last for years. If a recession shows up, the Fed will reduce interest rates and thus it will help the economy return to its long-term growth trajectory. RLJ will endure the downturn and will recover strongly whenever the economy recovers.

Strong balance sheet

RLJ can easily endure a potential recession because it has one of the strongest balance sheets in the REIT sector. Its net debt (as per Buffett, net debt = total liabilities – cash – receivables) currently stands at $2.0 billion, which is approximately equal to the market capitalization of the stock and about six times the annual FFO in 2019. As a result, it is manageable, especially given the absence of meaningful debt maturities until 2024. It is also important to note that 100% of debt is fixed or hedged, and hence the REIT is well protected from the environment of rising interest rates. To cut a long story short, RLJ should be able to endure a recession and emerge stronger whenever the economy recovers.

Valuation

Based on the aforementioned expected FFO per unit of $1.39 this year, RLJ is trading at a forward price-to-AFFO ratio of 8.1. In addition, the stock is trading at only 5.9 times its expected FFO per unit of $1.89 in 2023. This is an exceptionally cheap valuation level, especially for a REIT with a healthy balance sheet.

The cheap valuation of RLJ has resulted primarily from fears of an upcoming recession, but the REIT should be able to endure a recession thanks to its solid balance sheet. Whenever the economy recovers from such a recession, the market will probably reward the stock with a much higher price-to-FFO ratio. To provide a perspective, the stock has traded at an average price-to-FFO ratio of 10.0 over the last decade. Therefore, the stock is exceptionally attractive from a long-term perspective right now.

Risk

Due to the sensitivity of its luxurious hotels to economic downturns, RLJ will be vulnerable in the unlikely event of a prolonged recession. In such an adverse scenario, the REIT is likely to perform poorly for an extended period, and the aforementioned investment thesis will take longer to play out. Therefore, only the investors who can endure stock price pressure for a long period and remain focused on the long-term prospects of RLJ should consider purchasing the stock.

Final thoughts

Bear markets are ideal for providing opportunities to purchase solid stocks at depressed valuation levels. RLJ certainly fits this description, as it is a high-beta stock due to the luxurious nature of its hotels, which are sensitive to the underlying economic conditions. If the stock approaches the technical support of $10, it will become a great bargain. Long-term investors can then wait patiently for the stock to recover towards the pre-pandemic level of $17, which will correspond to a reasonable price-to-FFO ratio of 9.0 based on the expected FFO in 2023.

Be the first to comment