ChristianChan

One of the most significant trends in 2022 was the sharp rise in mortgage rates. Last year, the average 30-year mortgage rate rose from near-record all-time lows of ~2.75% to nearly 7.5% over just a few months. However, they have declined since mortgage rates remain the highest in over a decade at just over 6%. Mortgage rates have never risen as quickly as last year, so the total result of the shock will likely become more apparent through 2023.

Mortgage companies, such as mortgage REITs in the ETF (REM), took the most significant immediate hit as the sharp decline in mortgage asset values caused their book values to compress. REM fell by just over 40% peak-to-trough, but under-hedged and agency-centric “mREITs” like AGNC (AGNC) lost over 60% of their value. Those with more robust hedge portfolios (usually through Mortgage Serving Rights or “MSRs”), such as Rithm Capital (NYSE:RITM), saw lower losses at only ~30%. That said, all mortgage REITs began 2023 with stellar performance, with most rising 10-20% during the year’s first month.

Although mREIT valuations are not as low as two months ago, the sector still boasts the highest yields. For example, RITM boasts a forward yield of ~10.6%, with the ETF REM’s yield at ~9.4%. If it is true that the mortgage, and broader property market, are stabilizing this year, then great value-for-risk may be found in the mortgage REIT sector.

In my view, Rithm is a particularly interesting example because it has a more diversified portfolio than most, with exposure to agency and non-agency mortgages, MSRs, commercial loans, origination, and even single-family residential rental properties. This strategy makes Rithm less exposed to specific risks like a rise or fall in interest rates but does give the company greater exposure to broader risks in the property market. RITM has a very high yield today, so many income investors consider the company a value investment. While RITM offers a high yield, the firm carries specific risk factors that investors should consider in 2023.

Low Valuation, Strong Diversification

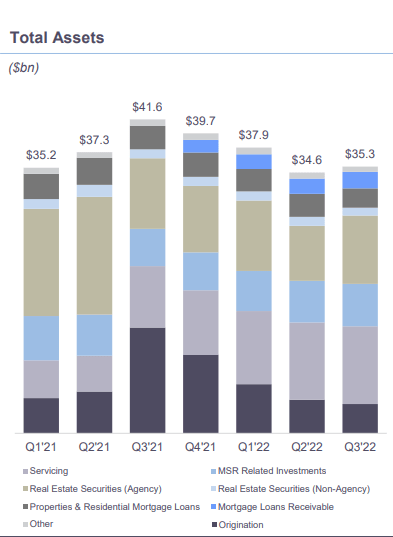

Rithm Capital is fundamentally different than most of its peers due to its diversified focus across the mortgage industry. Many mortgage REITs focus entirely on leveraged agency mortgage-backed securities, which carry lower credit risk and higher interest rate risk. There are mortgage REITs that focus primarily on higher credit-risk commercial loans. Others invest mainly in origination and mortgage servicing, which have closer ties to property sales volumes and credit risks. Typically, originations decline when mortgage rates rise, but the values of MSRs increase due to a decline in refinancing risk. Unlike its peers, Rithm is focused on all of these segments. See its asset exposure below:

Rithm Capital Assets 2021-2022 (Rithm Capital Investor Presentation Q3 2022)

Rithm’s strategy changed significantly after its massive 70%+ drawdown in 2020. That year, the company took a brutal hit due to the sharp rise in mortgages in forbearance forced the company to cover significant losses and dramatically increased servicing costs. Since then, the company has deleveraged and refocused its portfolio on superior assets. The company recently ditched its external manager and rebranded from “New Residential” to “Rithm.” The move costs the company $400M but will save it $60-$65M annually. More importantly, the company’s internalization makes it a more attractive investment due to the agency risks associated with external REIT management. While this change caused Rithm to lose some liquidity capacity at an inopportune time, I believe it benefits the company in the long term.

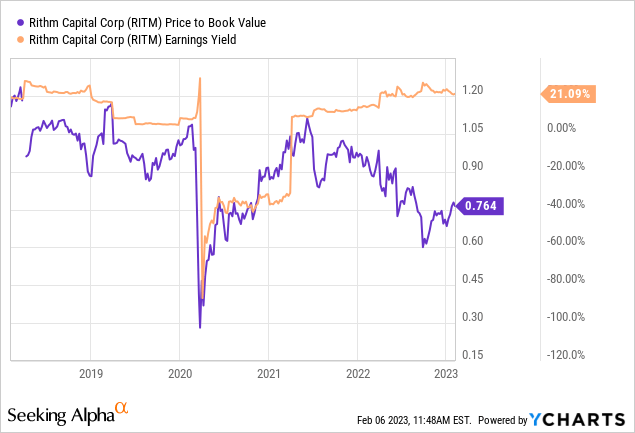

Indeed, investors appear scared to return to the stock after its significant losses in 2020. The company’s price-to-book and price-to-earnings (inverse of earnings yield) are very low, while its dividend is double-digit. See below:

RITM is cheaper than many of its peers and is trading far below its book value despite stronger resilience last year. Compared to most peers, RITM has far less direct exposure to higher interest rates, explaining its more robust performance in 2022. However, the firm likely has significant exposure to credit risks in the mortgage market, particularly a sizeable national rise in delinquencies or defaults not met with stimulus from the Federal government. Thus, if you firmly believe the mortgage market will remain stable despite the fall in affordability, RITM could be a substantial value investment.

RITM Carries Greater Risks in 2023

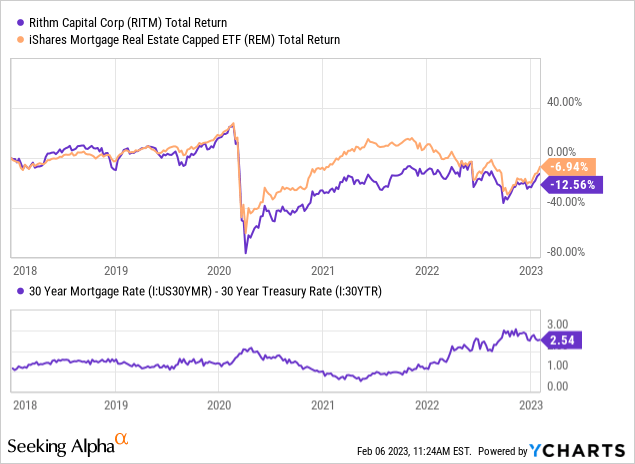

In 2020, the sharp decline in interest rates temporarily boosted the value of some of Rithm’s assets and increased refinancing demands, offsetting some of the benefits. Last year, the more significant rise in interest rates dramatically increased the value of its MSRs but lowered the originations and the importance of its portfolio assets. Overall, it has much less direct interest rate exposure than most since it owns assets that hedge each other given mortgage rate shocks. In 2020, RITM (New Residential) underperformed significantly as credit risks grew; however, it outperformed last year when mortgage spreads rose dramatically due to its massive MSR portfolio. See below:

Mortgage spreads have stabilized at high long-term levels. Since mortgage rates rose much faster than Treasury rates last year (which also rose quickly), it is apparent that investors are concerned regarding the safety of mortgages. Most residential mortgages are secured by the agency’s Fannie Mae (OTCQB:FNMA) and Freddie (OTCQB:FMCC) and hypothetically carry low default risk. However, the equity value of those two companies has crumbled to extreme lows, losing over 75% of their value since 2021. In all likelihood, with 50X+ leverage levels and crumbling equity value, neither company can fulfill obligations if there is a widespread increase in mortgage defaults (without another massive government bailout).

Seemingly, mortgage spreads are elevated due to the risk of the agencies failing or struggling to meet obligations in a slowing property market. With troubles in the property market growing, I believe Fannie and Freddie’s potential strains are an existential threat to Rithm. For one, investor concern regarding the agency MBS market’s stability could cause mortgage spreads to rise further. That is good news for MSRs unless defaults and delinquencies rise – which is very likely. Today, Rithm’s MSR book is in a “goldilocks” environment of high spreads and low defaults, but I do not expect that to continue with mortgage rates and home affordability as they are today.

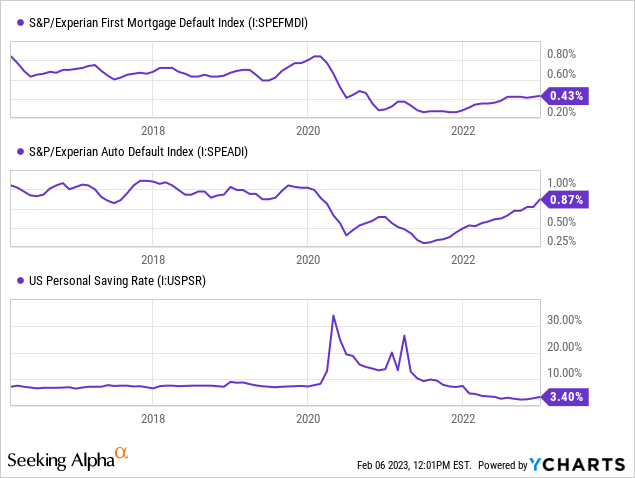

On the surface, mortgage default levels are low today, but they are rising. Auto loan defaults are a potential predictive signal for mortgages since people will likely avoid auto loan payments before their mortgage. This trend is backed by a sharp decline in savings levels. See below:

First mortgage defaults are still technically below pre-COVID levels. However, this is partly because many defaulted mortgages became “forbearance” mortgages in 2020. Since then, forbearance levels have declined dramatically but did rise slightly in recent months with the increase in “normal” defaults. Default levels declined in 2020 due to the sharp surge in savings levels (associated with massive COVID unemployment benefits); however, the rise in living costs since has caused savings levels to fall well-below pre-pandemic normal levels. In my view, these data indicate potential weakness for services in 2023 as defaults appear likely to rise as savings run dry amid higher living costs. A possible recessionary rise in unemployment would undoubtedly accelerate this trend, but employment levels remain strong today.

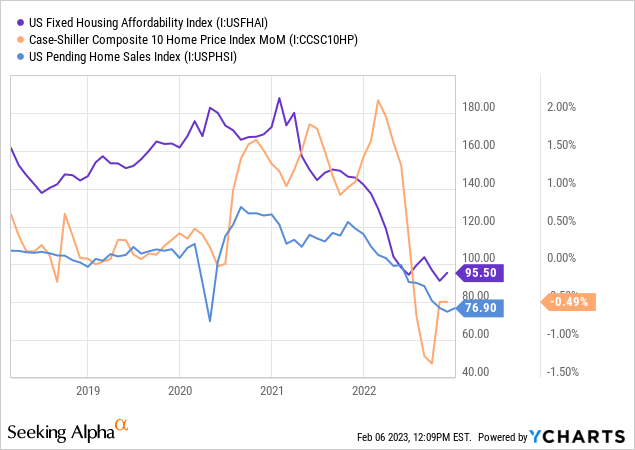

Unsurprisingly, the sharp increase in home prices in 2020, followed by the even more considerable rise in mortgage rates, has led to extreme housing unaffordability. More recently, this trend has resulted in a sharp decline in existing home sales and a slight fall in urban home prices. See below:

Unless mortgage rates fall (which is not necessarily suitable for Rithm), the property market will slow faster in 2023. At this point, it does not appear too likely that home prices will fall significantly nationally (due to inventory levels). Still, they could undoubtedly decline in geographical regions with more significant risks. Areas like California, with higher home valuations, declining populations, and greater exposure to technology layoffs, appear to be at the most significant threat. Still, the “goldilocks” environment for residential real estate is undoubtedly over, as affordability and recessionary factors seem likely to hamper originations and increase defaults.

The Bottom Line

Overall, I am not bullish on RITM due to the high immediate risk exposures to the mortgage market. In my opinion, based on the evidence, the company will take a significant hit this year due to a potential rise in mortgage defaults as many households struggle to make ends meet amid higher living costs, potential employment strain, and low home affordability. If these risk factors grow large enough that Fannie Mae and Freddie Mac face liquidity issues, then Rithm’s counterparty exposure could jeopardize the firm; however, this risk could be mitigated by government stimulus or a return to QE.

While I would not invest in RITM, I am also not particularly bearish due to the firm’s low valuation. It trades well below its book value and at a very high yield and earnings level. Since RITM trades at a considerable discount to offset its economic risk exposure, it is understandable that many investors are interested in the company. If mortgage defaults do not rise in 2023, as I suspect, then RITM likely has a tremendous upside as its rises toward (or above) its book value while paying a substantial dividend. Still, bullish investors in RITM may not want to invest money they cannot afford to lose since RITM could rapidly lose all or most of its value if the mortgage market continues to sour.

Be the first to comment