Maksym Isachenko/iStock via Getty Images

Article Thesis

The last two years were strong for the mining industry, but recession worries made Rio Tinto Group (NYSE:RIO) and its peers drop during the second half of 2022. More recently, however, economic reopening in China has been a boon for commodities, as iron ore and copper demand have increased while prices have soared. Rio Tinto should have a strong 2023 and the longer-term outlook is good as well, but RIO isn’t the bargain it was last fall.

China Reopening Is Good For Business

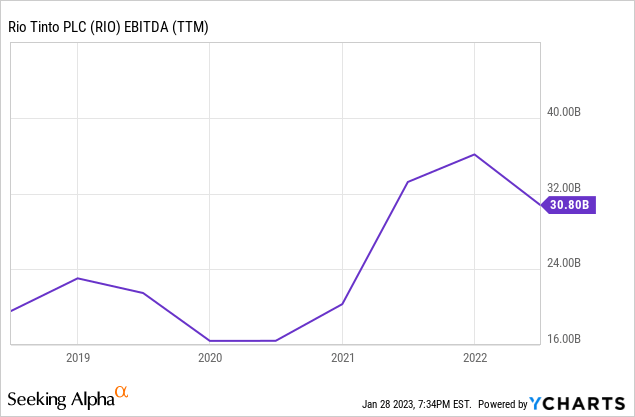

The assets of major mining companies such as Rio Tinto Group do not change much over a couple of years, as major mines have very long reserve lives. But the profits and cash flows these mines generate can vary a lot from one year to another, as commodity prices naturally play a big role in the revenues RIO and its peers generate. Since costs are fixed to a large degree, revenue swings result in big earnings and cash flow swings.

These ups and downs are clearly visible in Rio Tinto’s past results:

Especially the first half of 2020 was rather weak, as commodity prices were weak due to a global economic shutdown. But during the second half of 2020, and especially in 2021 and early 2022, commodity prices soared. This included base metals such as copper and iron ore to which Rio Tinto is highly exposed.

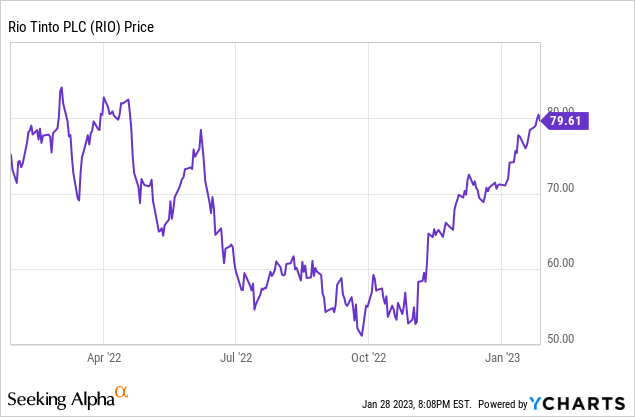

Rio Tinto’s shares unsurprisingly went up significantly during the time when markets were euphoric about strong commodity pricing, but shares came crashing down in the second half of 2022. High inflation forced central banks to hike interest rates, which led to worries about a potential recession. At the same time, China was locked down due to COVID, thus commodity sales to that country were at a below-average level.

From highs in the mid-$80s in spring 2022, RIO fell all the way to $50 — at that point, shares were pretty cheap, considering the fact that the long-term profit outlook doesn’t change too much even if there is a recession, which was and still is not guaranteed anyway. But towards the end of 2022, and in early 2023, RIO started to perform very well again. This was primarily the result of China’s changing COVID policy — instead of going for a Zero COVID approach with massive lockdowns, China is now opening up its economy again.

That, in turn, has led to increasing demand for all kinds of industrial goods and commodities, including basic ones such as iron ore or copper, as showcased by the following charts:

Iron Ore (Seeking Alpha)

Copper (Seeking Alpha)

Both charts, for iron ore and copper, show that prices are down slightly over the last year. They are, however, up massively from the levels seen last summer and fall. I do believe that there is a good chance that commodity prices, including iron ore and copper, will remain high, on average, over the coming years, due to several reasons:

First, getting new projects up and running has become rather complicated. Lengthy and costly approval processes in many countries are a burden for companies that want to grow their output, and some activist investors also are against new projects due to their environmental impact. This will be a hindrance to new supply over the coming years.

Second, demand will grow based on a range of macro trends, including China’s reopening, massive required infrastructure spending in the US, Europe, etc. in order to keep aging infrastructure intact, additional demand from emerging and developing markets where a growing middle-class results in growing investment and consumer spending. Last but not least, building out the green economy and related infrastructure around the world will require massive resources. Electric grids will need to be upgraded, which will require copper and steel (and thus iron ore), wind mills require huge amounts of steel, and so on.

All in all, there is thus a good likelihood that growing demand will go hand in hand with subdued supply growth in the foreseeable future, I believe. That should keep commodity prices high and may cause them to rise to even higher levels compared to where they are today. That, in turn, makes for a positive environment for Rio Tinto and other mining companies, as their profits should be compelling if iron ore, copper, etc. prices are high.

The company announced its most recent results last July, as RIO reports half-year and full-year results only. In the first half of 2022, Rio Tinto generated $15.5 billion of EBITDA, or $31 billion annualized. H2 of 2022 was most likely worse, as commodity prices had pulled back, but since they have now risen back up, 2023 could see an EBITDA result in the $30+ billion range, at least as long as commodity prices remain elevated.

The company also managed to generate $10.5 billion of operating cash flow, or $21 billion annualized. After subtracting Rio Tinto’s capital expenditures, the company generated an annualized free cash flow of a little north of $14 billion during the first half of 2022. I believe that free cash generation in 2023 could be at a similar level — since RIO is currently valued at around $130 billion, that would imply a free cash flow yield in the 10%-11% range, which would be quite attractive.

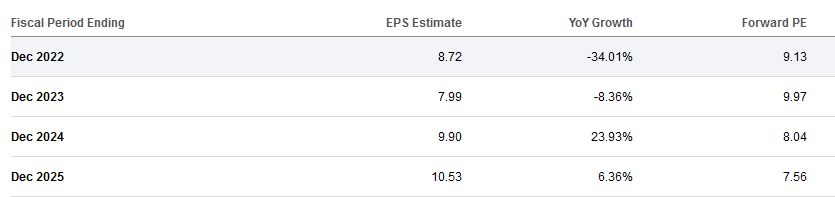

Looking into the future, we see the following profit estimates for RIO:

Seeking Alpha

Profits see a profit decline in 2023, relative to 2022. I believe that this might get revised over the coming weeks, as iron ore and copper have risen substantially in the very recent past — maybe not all Wall Street analysts have factored that into their models yet. But even if EPS indeed does come in at $8, down slightly versus 2022, that would still be far from a disaster. After all, that would equate to an earnings multiple of just 10, as RIO trades for exactly $80 right now. In other words, even with a potential earnings pullback in 2023 accounted for, RIO offers an earnings yield of 10% at current prices, which seems pretty attractive.

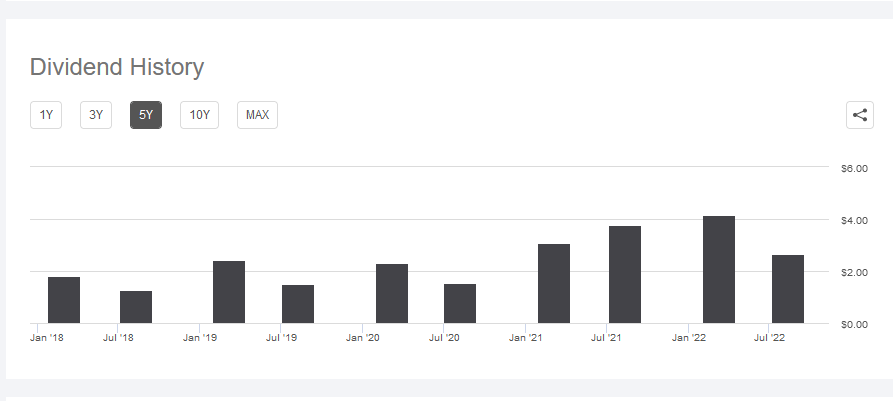

Rio Tinto has a policy of returning a large portion of its free cash flow to investors via dividends. The company isn’t doing buybacks at a high pace, and since RIO already has a strong balance sheet, further balance sheet strengthening isn’t really needed. Since RIO is generating uneven profits, its dividend payout is uneven as well:

Seeking Alpha

There are ups and downs, with 2022 being a year of particularly strong dividends. The company paid out $6.84 in 2022, which translates into a trailing dividend yield of 8.6% at current prices. There is no guarantee that the payout in 2023 will be comparable, but based on the recent recovery in commodity prices that makes me believe that 2023 will be a successful year for the company, 2023 could be a year with another hefty payout.

Summing Things Up

Commodity prices, including those that are relevant for mining giant Rio Tinto, have risen substantially in recent weeks, as China’s new COVID policy (economic reopening) is improving the demand outlook. The longer-term outlook for iron ore demand, and especially copper demand, is healthy as well, which is why I believe that RIO and its peers could generate healthy profits in the coming years.

On the other hand, RIO has rallied close to 60% from the lows seen last fall, thus from a timing perspective buying today isn’t the most optimal choice. Last August, I wrote a bullish article on Rio Tinto — since then, it has delivered a total return of 37%, versus a 5% decline for the broad market. Following this hefty outperformance of more than 40%, I am somewhat less bullish on RIO — the stock should still do well in the long run and the valuation is far from high, but it’s not a super bargain anymore, either. The volatility of the stock could result in better buying opportunities down the road, I believe.

Be the first to comment