chonticha wat/iStock via Getty Images

iShares MSCI Global Gold Miners ETF (NASDAQ:RING) is an exchange-traded fund with exposure to companies that derive the majority of their revenues from gold mining. Gold mining companies are often viewed by gold enthusiasts as an alternative to investing in gold and/or to achieve some kind of perceived “beta” (relative volatility) to the spot price of gold. However, it is important to remember that gold mining companies are technically ‘short gold’, since they are literally in the business of digging up gold and selling.

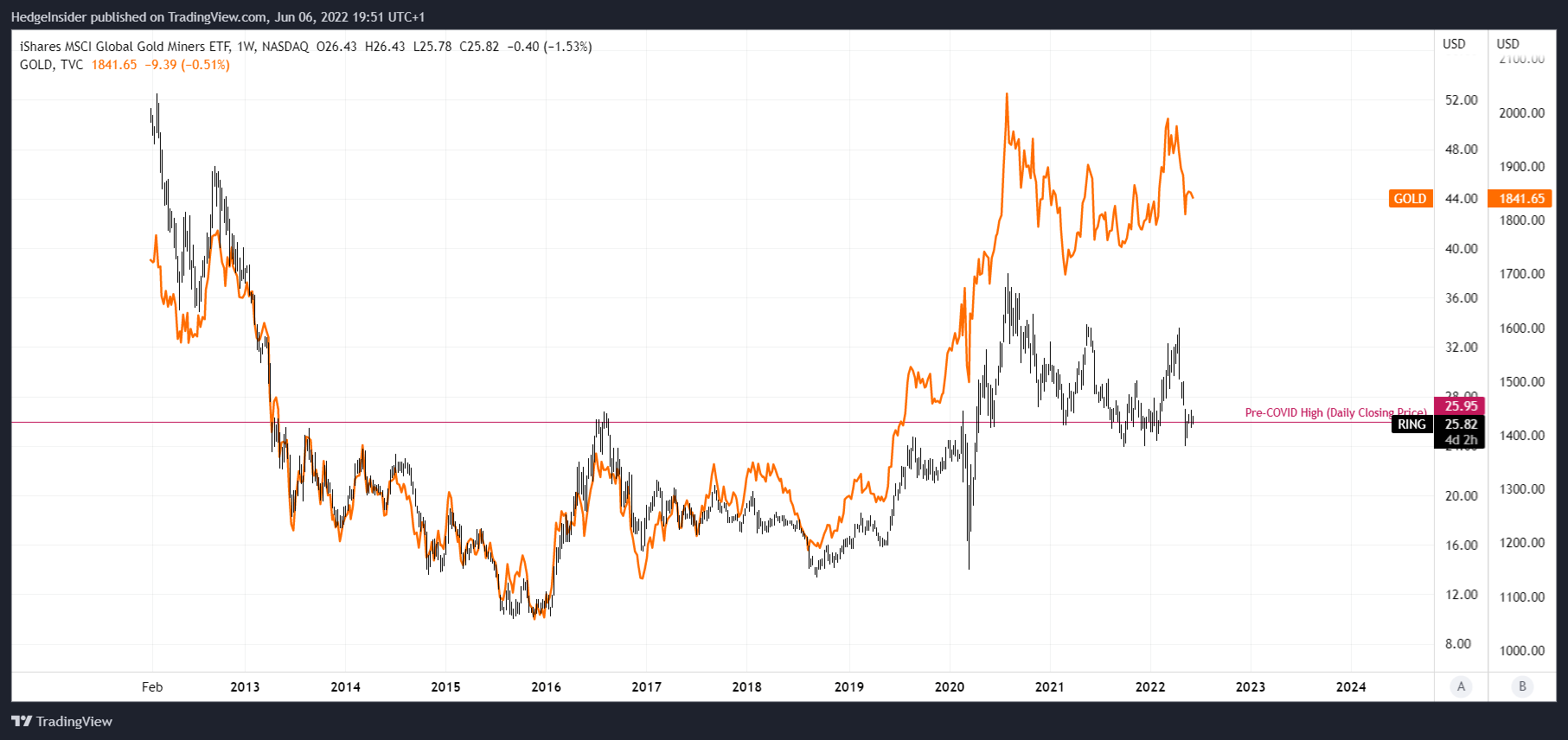

Gold miners do tend to do well when the gold price is rising, but they can under-perform too. For example, as illustrated below, RING’s share price (excluding any dividends and buybacks) is about where it was relative to pre-Covid-19 prices in early 2020 (and indeed well below the inception price of the fund). Meanwhile, the spot price of gold is at least higher than it was when the RING ETF was launched, and considerably higher than prices seen immediately before the emergence of COVID-19.

TradingView.com

There are different ways to value gold, but ultimately it is down to the market; as we generally all know, the utility value of gold is only a fraction of the market price. If I have understood, the price of gold is largely driven by changes in risk-on/risk-off sentiment, rather than due to demand from industrial users of gold. The relationship between gold and risk sentiment itself is subject to change though, and gold can often rally during anticipated change and then sell off after realized change (for example, gold rallied into the escalation of Russo-Ukrainian war during 2022, but has since sold off).

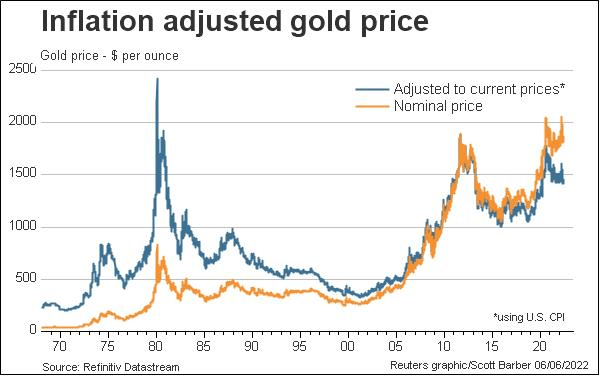

Nevertheless, in the long run, one would assume (or at least hope, for the sake of gold investors) that the ‘precious metal’ will hold its own against inflation. Gold has a patchy record as an inflation hedge though. The chart below is a logarithmic chart for the price of gold since the early 1970s. Evidently the price of gold has indeed risen over time, supported by monetary devaluation (via inflation).

TradingView.com

However, as shown below, the inflation-adjusted price over the long run is a bit patchier.

thomsonreuters.com

I think the important point is that while gold mining companies will probably always be OK in terms of there being an underlying demand for gold in volume, there is only so much gold out there to mine, and marginal improvements in mining productivity are going to become thinner and thinner over time, and in inflation-adjusted terms, there is possibly a minor headwind to gold miner margins.

RING seeks to replicate the performance of its benchmark, the MSCI ACWI Select Gold Miners Investable Market Index. There were 36 constituents in the most recent factsheet for the index, although iShares currently report a prevailing 40 holdings under the RING portfolio. In any case, the fund is concentrated, with the top 10 holdings representing 70.62% of the portfolio as of June 3, 2022.

Data from iShares.com

The benchmark index, as of May 31, 2022, reported trailing and forward price/earnings ratios of 19.47x and 14.55x, respectively, with a price/book ratio of 1.56x, and a dividend yield of 2.35%. The implied forward return on equity was therefore about 10%, which is not high. With gold prices currently elevated (and indeed, the forward price/earnings ratio of RING’s benchmark index implying a forward one-year earnings growth rate of over a third), a forward ROE of about 10% is not impressive. The implied dividend distribution rate is about 45%, which we could assume will be fairly constant.

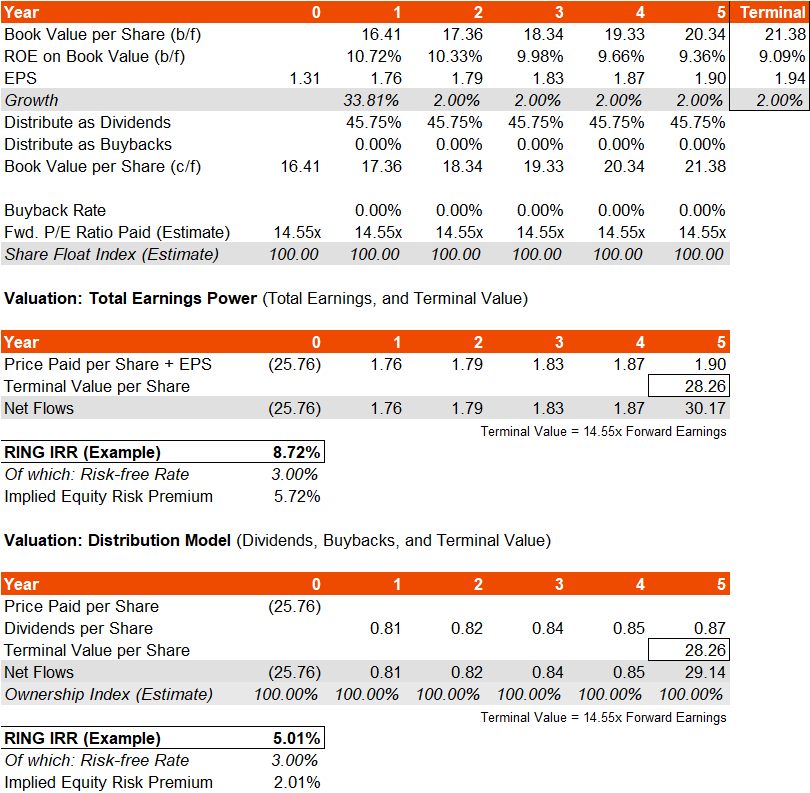

Some gold companies do buy back shares (e.g., Newmont (NEM) has in the recent past) however other gold miners have been issuing shares, while various of these buyback programs can reverse during negative cyclical changes in the gold mining industry. I will therefore just assume a 0% net buyback rate overall for now. Also, RING is mostly exposed to U.S. and Canada equity listings, so I will assume a risk-free rate in my calculations of 3% (about what the current U.S. and Canadian 10-year bonds are yielding). The above data and assumptions generate the following IRR gauge, assuming a drop-off in the return on equity but keeping earnings growth at a floor of 2%.

Author’s Calculations

The floor of 2% might be giving the industry some credit. In any case, my three-year and five-year average earnings growth rates come to 11.66% and 7.69%, respectively. This compares to Morningstar‘s current consensus estimate for the three- to five-year average earnings growth rate of 13.29% on a forward basis. So, I am possibly being conservative (I am basically just giving MSCI credit for its forward one-year earnings forecast, but otherwise assuming a stable 2% growth rate).

On the above assumptions, while the “distribution model” (of valuing RING on its dividends and indicative terminal value) renders a low IRR of 5.01%, the more holistic “total earnings power” model (of valuing prospective total portfolio earnings and the terminal value) gives us an indicative IRR of 8.72%.

With a risk-free rate of 3%, that means the underlying equity risk premium is about 5.72%. RING does not carry excess beta on average, but being exposed to commodities you can anticipate the potential for strong under-performance given an adverse cyclical shift in the gold price and/or mining industry. “Down beta” can be expected to be elevated, even during broad risk-off moves in equity markets. For example, RING fell -47.8% peak-to-trough during the February-March 2020 COVID-19 scare. The S&P 500 fell a lesser -35.4%. In general, I would be comfortable assuming an elevated equity risk premium for RING, and so while an ERP of over 5% might be considered elevated for the broader and more diversified equity market indices, it is probably fair for RING.

Therefore, in my base case, I would say RING is fairly valued. I did however not consider a change in the terminal value by way of adjusting the forward price/earnings multiple from the current 14.55x. If we do assume a 2% terminal growth rate, a forward earnings yield of 6.87% (the inverse of a forward P/E of 14.55x) with an assumed risk-free rate of 3% implies an ERP of about 5.87%. Again, I consider this quite reasonable given the risks associated with commodity markets. I don’t think a change to the multiple is necessary.

In summary, while RING is likely to continue to tick along and generate a moderate return on equity at the portfolio level, I don’t think the current IRR implied by the present share price implies awfully good value. I am neutral on RING.

Be the first to comment