Editor’s note: Seeking Alpha is proud to welcome Seal Bay Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

piranka

Rimini Street, Inc. (NASDAQ:RMNI) has been overly punished by the market and is fundamentally undervalued, trading at less than 1x sales with a 63% gross margin. We believe RMNI has an excellent risk/reward profile and offers significant upside. RMNI provides an excellent value proposition to customers and has the ability to reaccelerate growth as the leader in the emerging third-party support market for enterprise software.

Background

RMNI is a global provider of enterprise software support products and services. CEO Seth Ravin founded RMNI in 2005 with the goal to disrupt and improve the enterprise software support industry – providing better support at a lower price. In doing so, he has pioneered the third-party support industry for enterprise software. RMNI now serves 3,010 active clients and has served 180 Fortune 500 and Global 100 companies since its inception. RMNI’s revenue is split evenly between U.S. and international clients.

RMNI has operated as vendor replacement support, primarily for Oracle (ORCL) and SAP (SAP) products. While that is still RMNI’s main focus, it has recently expanded its offerings and has plans to continue doing so. RMNI recently expanded into application management services (AMS), a significant opportunity that we’ll discuss below.

Value Proposition

From an investment perspective, RMNI’s most appealing trait is its overwhelming value proposition to clients and high customer satisfaction ratings. Ravin likes to describe the value proposition in terms of optimizing the IT budget. Every IT department has a limited budget, no matter how large or successful the company. The IT budget is a constrained resource. There will always be more asked of the IT department than what they can provide. IT will always be making allocation decisions, and RMNI can help them optimize their budget with its lower cost support solutions.

As investors, we avoid companies that compete primarily on price. While price is part of RMNI’s value proposition, RMNI embodies the moniker of “cheaper, better, faster.” RMNI assigns senior engineers with an average of 15 years of experience to each client. RMNI guarantees a 10-minute response time for critical issues, with the average case response time from engineer to client of less than five minutes. RMNI also has a company bonus program that is based on client satisfaction and client retention, further aligning the interests of the engineer and the client. RMNI enjoys an impressive 4.9 out of 5.0 average client satisfaction rating.

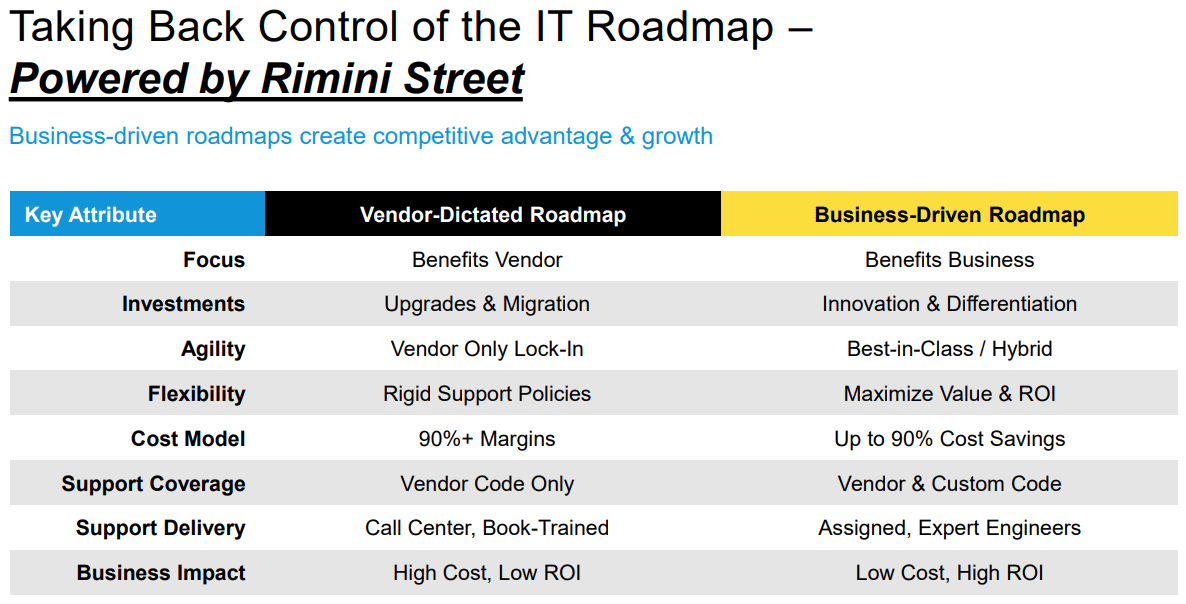

RMNI offers clients what it calls a “business-driven roadmap” as opposed to a “vendor-dictated roadmap.” Benefits include avoiding costly forced upgrades and migration, as well as a more flexible support model that aims to maximize value and ROI for the client.

Company Presentation

RMNI provides software support at a fraction of the cost of what the vendor would customarily charge. RMNI asserts that clients realize a total cost savings of anywhere from 50% to 90% by switching from vendor support to RMNI. This frees up a huge chunk of the IT budget that can then be allocated to business transformation. At the core of RMNI’s value proposition is reducing the portion of the budget that gets consumed by ongoing operations and enhancements so that more of the budget can go to business transformation, a crucial factor in remaining competitive.

The cost savings aspect of RMNI is also appealing from an investment perspective. RMNI theoretically becomes more attractive during a recessionary period because it can provide clients with significant cost savings that they can begin realizing in a relatively short amount of time.

AMS Opportunity

From a high-level overview, there are five tiers of IT support ranging from Level 0 to Level 4. RMNI has historically operated at Level 4, which is software support from the software vendor (or vendor replacement). RMNI expanded its offerings to include Level 3 and Level 2 support, advanced technical support known as AMS. RMNI does not offer Level 1 (help desk support for end-user inquiries) or Level 0 (self-help).

RMNI began providing AMS in response to requests from existing clients for whom they were already providing Level 4 support. AMS gives RMNI an excellent opportunity to cross-sell additional services to existing clients. Cross-selling has been a point of emphasis that management has highlighted on recent earnings calls. RMNI’s excellent customer satisfaction should help with selling additional services to existing clients.

RMNI launched AMS in late 2019. RMNI offers an “industry-unique service bundle” with both application management services and application support services offered, covering Levels 2/3/4 in support. AMS significantly increases RMNI’s total addressable market (TAM), which we address further in the next section. According to The Business Research Company, the AMS market is expected to grow from $23.4B in 2021 to $59.7B in 2026, a CAGR of 20.5%.

Total Addressable Market

RMNI estimates the TAM of their current offerings at $29.2B. This is comprised of $8.3B for Oracle Support, $7.4B AMS for SAP, $6.2B for SAP Support, $3.8B AMS for Oracle, and $3.5B AMS for Salesforce (CRM). The global TAM for IT Levels 2/3/4 support is estimated at $170B based on data from Forrester Research and RMNI’s own calculations. With full-year 2022 revenue likely to be in the $405M range, RMNI is not constrained by TAM. The market opportunity is significant; the question is how much RMNI can capture.

Competition

RMNI asserts that it is the only third-party support provider at global scale. According to Gartner metrics, RMNI holds an 86% market share of the third-party support industry for enterprise software. Given the lack of at-scale competition in third-party support, RMNI primarily competes against the vendors whose products they support. This includes Oracle, SAP, Microsoft (MSFT), and IBM (IBM).

Although they are competing against established players, RMNI wins many of these deals for reasons discussed above. RMNI offers excellent customer service with senior engineers assigned to each client and fast response times. As displayed in the “IT Roadmap” graphic, RMNI offers tailored support to provide more flexibility to the client and ultimately a higher ROI of their software support. Lastly, RMNI offers a compelling 50% to 90% total cost savings to clients.

AMS has an entirely different set of competitors. These include Tata, Infosys (INFY), Capgemini (OTCPK:CGEMY), Accenture (ACN), and Cognizant (CTSH). The AMS market is fragmented with a long list of players that extends far beyond the ones highlighted here.

Although RMNI is newer in the AMS space, it is able to offer the same core component of its vendor replacement value proposition – superior customer satisfaction. A differentiator for RMNI in AMS is that RMNI also provides Level 4 support. Some clients prefer the continuity of having one company provide all the support for Levels 2-4. This also reduces ambiguity regarding cases that could fall in the domain of either Level 3 or Level 4 support.

Financial Overview

RMNI has a market cap of $378M and an EV of $338M. Revenue for the first three quarters of 2022 was $301M, with management guiding for 2022 full-year revenue to be $404M to $406M once Q4 is reported. Taking the midpoint of $405M, revenue would come in at an 8.2% increase over 2021 revenue. This is a deceleration of growth from 2021 (+14.7% YOY growth) and 2020 (+16.3% YOY growth). While the slower growth in 2022 is a cause for concern, we remain positive on the long-term prospects for RMNI.

Q3 2022 revenue was $101.9M, an increase of 6.6% over Q3 2021. RMNI has a near even split of U.S. and international revenue, with Q3 2022 revenue comprised of 52% U.S. clients and 48% international clients. Management noted that Q3 2022 international revenues on a U.S. dollar denominated basis were negatively affected by conversion to a strong dollar.

Annualized recurring revenue was $399.8M for Q3 2022, a 6.2% increase YoY. The revenue retention rate for service subscriptions was 94% for Q3 2022. Greater than 80% of the subscription revenue is locked in for at least 12 months (non-cancellable). The revenue retention rate for service subscriptions was 94% or 95% for each of the first three quarters of 2022. RMNI’s recurring revenue model and high retention rates give the stock a solid floor moving forward.

While gross margin of 60%+ is already strong, we project that operating margin will expand to double digits. Gross margins have been consistent in the 61% to 64% range over the past three years. Management is guiding for full-year 2022 gross margins to come in at 62.5% to 63.5%. Operating income was $13.7M for the first three quarters of 2022 for an operating margin of 4.5%. Operating expenses as a percentage of revenue through the first three quarters of 2022 totaled 57.7% of revenue, broken down as follows: 34.4% sales and marketing, 19.0% G&A, and 4.1% net litigation costs. We project significant improvement in operating margin over the next few years by reducing operating expenses as a percentage of revenue, particularly G&A and litigation expenses.

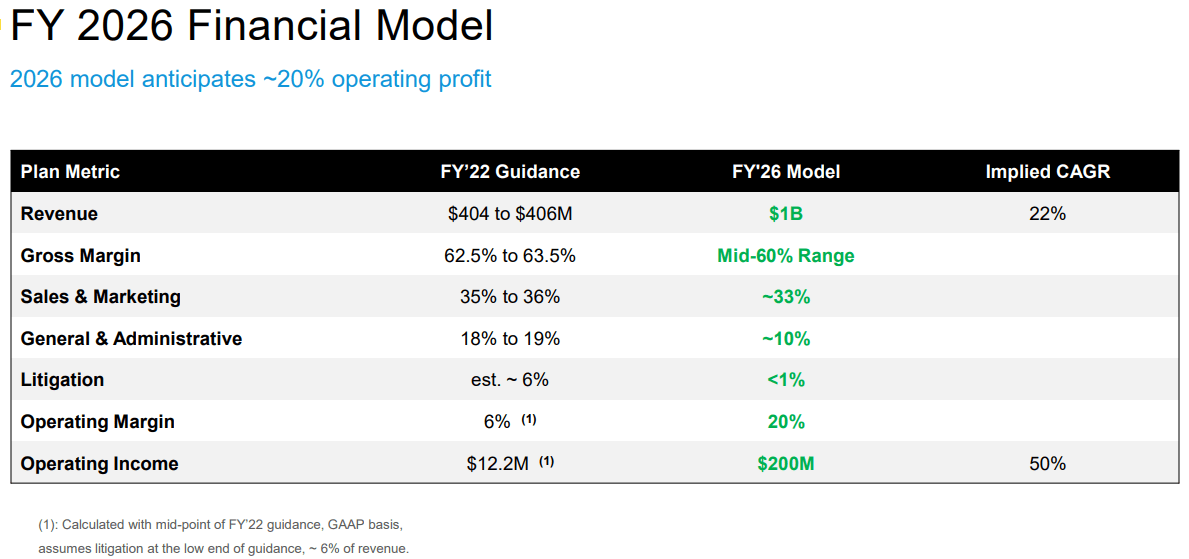

Management’s FY 2026 Financial Model

In 2021, RMNI announced a strategic growth plan to achieve $1B in annual revenue by 2026. Despite the slowing growth in 2022, RMNI has maintained the $1B target. Management has reiterated the $1B number on every earnings call and included it as recently as Jan. 12, 2023, in their presentation at the 25th Annual Needham Growth Conference. It’s safe to say that the market is not buying this number, as RMNI’s stock price would be much higher if the market were anticipating this growth. Although we acknowledge that $1B by 2026 is overly optimistic, RMNI can fall well short of this lofty goal and still provide outsized returns.

Nonetheless, with the recent financials in mind, we will provide management’s FY 2026 Financial Model for reference.

Company Presentation

Based on our calculations, the implied CAGR for revenue is roughly 25% now (not 22% as referenced in the slide above). A focal point for RMNI has been reengineering the business to accommodate a $1B revenue scale operation. As per Ravin during the Q2 2022 earnings call:

We were previously a 30%-type growth company traditionally. I think the opportunity and the demand is there for us to have that kind of business even on a much bigger number. And I decided I was going to step back in and take it personally to get us where I believe we need to be and complete the transition to $1 billion revenue scale by the end of this year. I think it’s no secret that it’s taken us a little bit too long to get through this transition. We should have had it done in a year. It’s been 18 months. And I’m determined to complete the transition by the end of 2022 and leave us in a very strong position out of the starting gate for 2023.

Balance Sheet and Share Repurchases

RMNI has a solid balance sheet, with $118.6M cash and cash equivalents vs. $71.4M of long-term debt. RMNI made a significant move in July 2021 to improve its financing position. RMNI entered into a $90M, five-year senior secured credit facility. The interest terms are LIBOR plus a margin of 1.75% to 2.50%. RMNI used $88M of the credit facility to redeem its remaining Series A Preferred stock. This greatly reduced RMNI’s annual financing costs. RMNI paid roughly $27M in financing costs in 2020, with $15.8M of dividends paid on Series A preferred stock. RMNI’s interest expense totaled $3.0M through the first three quarters of 2022, with no more Series A preferred stock remaining.

Dilution was previously an issue, with share count increasing by 29% from 2019 to 2021. Share count leveled off in 2022, only increasing by 1%. In June 2022, RMNI announced an increase in its share repurchase plan. The plan originally authorized repurchases of up to $15M over two years and was increased to authorize up to $50M in repurchases over the next four years ($50M is equivalent to 13.2% of the current market cap). RMNI’s shift from share dilution to share repurchases speaks to the company’s improved financing position, another factor that should raise the floor of the stock relative to previous years.

Ownership and Capital Structure

RMNI’s largest shareholder is Adams Street Partners and its affiliates, owning 26.7% of RMNI’s Common Stock. Adams Street Partners originally made an equity investment in RMNI in 2009, eight years before RMNI went public. Although our preference is that companies do not have a single shareholder with such a large portion of the shares, we do not view this as a major risk for RMNI.

Ravin owns 12.9% of RMNI’s outstanding shares of common stock. Ravin’s interests should be well aligned with shareholders given his significant stake in the company.

RMNI has warrants outstanding for 3.4M shares of common stock exercisable at $5.64 per share. These warrants expire in June 2026. These warrants are currently out-of-the-money. The stock price would need to increase by more than 20% to exceed the exercise price, so the warrants are not a concern for current purchasers of the stock (the warrants are accounted for below).

Risks

RMNI has significant risks that should be carefully considered. We will address three main risks in the following sections. Ultimately, our investment decisions are based on an evaluation of risk vs. reward. We believe that despite RMNI’s risks, it has a favorable risk/reward profile.

Litigation with Oracle

RMNI has been engaged in a legal battle with Oracle since 2010 when Oracle originally sued RMNI and RMNI then countersued. There is a lot to digest from the 13 years of litigation, so we will just offer a few highlights and our outlook as opposed to a full history. Most importantly, RMNI’s business model of providing third-party support was ruled to be legal. Therefore, we do not view the litigation as an existential threat to RMNI. The court did find RMNI guilty of copyright infringement and originally ordered RMNI to pay $124M in damages to Oracle, although that number was later reduced.

Management has acknowledged that the litigation with Oracle will continue, and we do not see a clear end in sight. From Oracle’s perspective, it makes sense to keep the legal battle going until the courts order a stop. Oracle wants to protect its high-margin maintenance revenue that RMNI is trying to capture. Unfortunately for RMNI, the legal fees are more damaging to them than they are to Oracle given the drastic discrepancy in the size of the two companies. The main outcome we see from the litigation is continued drag on operating margins as litigation expenses eat a portion of potential income each year.

One note of caution when researching the litigation – the press releases from both RMNI and Oracle tend to be biased, with each side declaring victory on the same case in at least once instance. The court rulings or summaries from unbiased sources are more reliable.

Sales Challenges

As we discussed earlier, RMNI had a disappointing 2022 (and late 2021) in terms of slowing sales growth. This was largely attributed to challenges with the sales team and execution. RMNI added significant headcount to the sales team over the past two years in an effort to scale growth. However, given RMNI’s somewhat complex sales cycle, new sales hires can take about 12-18 months to get up to full speed (although management has mentioned trying to get that number below a year). Coupled with hiring challenges and employee turnover, common issues faced by many organizations over the past two years, sales performance underwhelmed.

During the Q3 2021 earnings call this was a main focus, with Ravin referencing lack of sales execution and “rookie mistakes.” Throughout 2022 this remained a theme, although slightly less dire than at the end of 2021. On the Q2 2022 earnings call Ravin announced, “I am now dedicating a majority of my time to maturing our service offerings, delivering innovative new marketing and improving global sales execution.” Ravin reiterated this on the Q3 2022 earnings call as well, saying:

As I detailed in our last quarterly call, I’m now dedicating a majority of my time to improving global sales execution, maturing our service offerings, and delivering innovative new marketing campaigns to build deeper pipelines of new client and cross sell opportunities globally.

We will continue to keep a close eye on sales execution in 2023.

Lack of a Catalyst

In his book Margin of Safety, Seth Klarman writes that value investors should always be on the lookout for catalysts. Catalysts reduce risk because if events are likely to close the gap between price and underlying value quickly, the probability of underlying value eroding in the meantime is reduced. Unfortunately, we do not see a clear upcoming catalyst for RMNI. However, for the patient long-term investor who can tolerate volatility, we feel that RMNI is significantly undervalued.

Over the past two years, RMNI’s stock price has fluctuated from $3.30 up to $11 and back to $4. Some of this drop was precipitated by slowing growth from RMNI, while some can be attributed to the market-wide sell-off – particularly in small caps. While the stock price is back where it was two years ago, the company has made significant progress in the meantime.

Valuation

For the purposes of this article, we will present four valuations: our downside case, base case, upside case, and a valuation based on management’s FY 2026 financial model. We use 2026 for each of the cases for consistency. All cases assume fully diluted shares with the $5.64 warrants being exercised for 3.4M common shares. For the purposes of this article, we developed a simple valuation based on three variables: CAGR of revenue, operating margin, and an EV multiple of operating income.

Please note that only revenue, operating margin, and operating income are directly stated in management’s FY 2026 financial model – the remaining figures are calculated by us based on our corresponding assumptions.

Seal Bay Capital

We assigned a lower multiple of 10x to the two lower growth rate scenarios and a higher multiple of 15x to the two higher growth rate scenarios. Of the four scenarios presented, the base case scenario is our most likely projected outcome. The base case would net a 24% annualized return over the next four years. The market is currently pricing RMNI closest to the downside case scenario. This is a key reason why we like the stock – we feel that it is being priced pessimistically, meaning that any positive surprises could generate excellent returns. Our upside case would generate an annualized return of 49% over the next four years (roughly 5x).

Conclusion

For risk-tolerant investors, RMNI offers an attractive risk/reward profile. RMNI is a volatile stock with small company risk. However, it has key positive attributes, including an overwhelming value proposition for customers and a leading position in a growing market. Given that we feel the market is pricing RMNI pessimistically, it is a high conviction holding with significant upside. We believe that anything under $6 is a good entry price with three to five years as a realistic investment horizon.

Be the first to comment