felixmizioznikov

RH (NYSE:RH), together with its subsidiaries, operates as a retailer in the home furnishings. It offers products in various categories, including furniture, lighting, textiles, bathware, décor, outdoor and garden, and child and teen furnishings.

In May, 2022 we have published an article about RH on Seeking Alpha, titled: “RH: Pros And Cons Of Starting A Position Right Now“. Back then, we have rated the company’s stock as hold. Our primary arguments for the neutral rating have been:

- In the last five years, RH has been able to consistently expand its margins and improve its return on assets.

- Both the revenue growth and the margins of the company compare favourably to the respective sector median.

- Macroeconomic headwinds, including elevated inflation and poor consumer sentiment, create uncertainty in the near term.

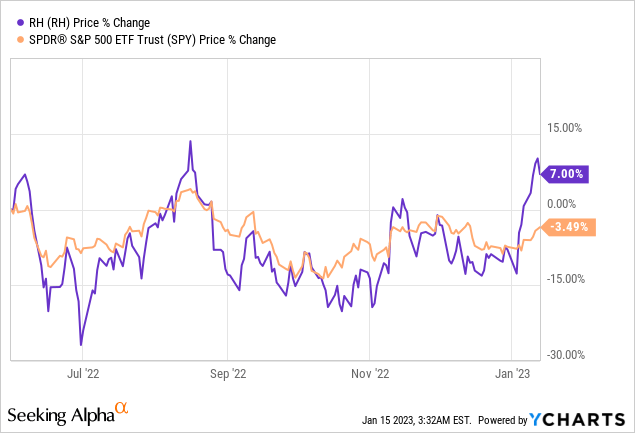

Since our writing, RH’s stock price has increased by 7%, largely driven by the recent jump in the stock price. Generally, in the period, RH’s stock price has been quite volatile. In the same time frame, the broader market has declined by about 3%.

In today’s article, we are revisiting our previous thesis to see, whether it is still intact. We will start our discussion by looking at a set of economic indicators, which could gauge the strength of the consumer and the health of the housing market. Then, we are going to analyse some of the management’s commentary with regards to the firm’s near- and long-term strategy, released in December together with the Q3 quarterly filings.

Economic indicators

Consumer confidence

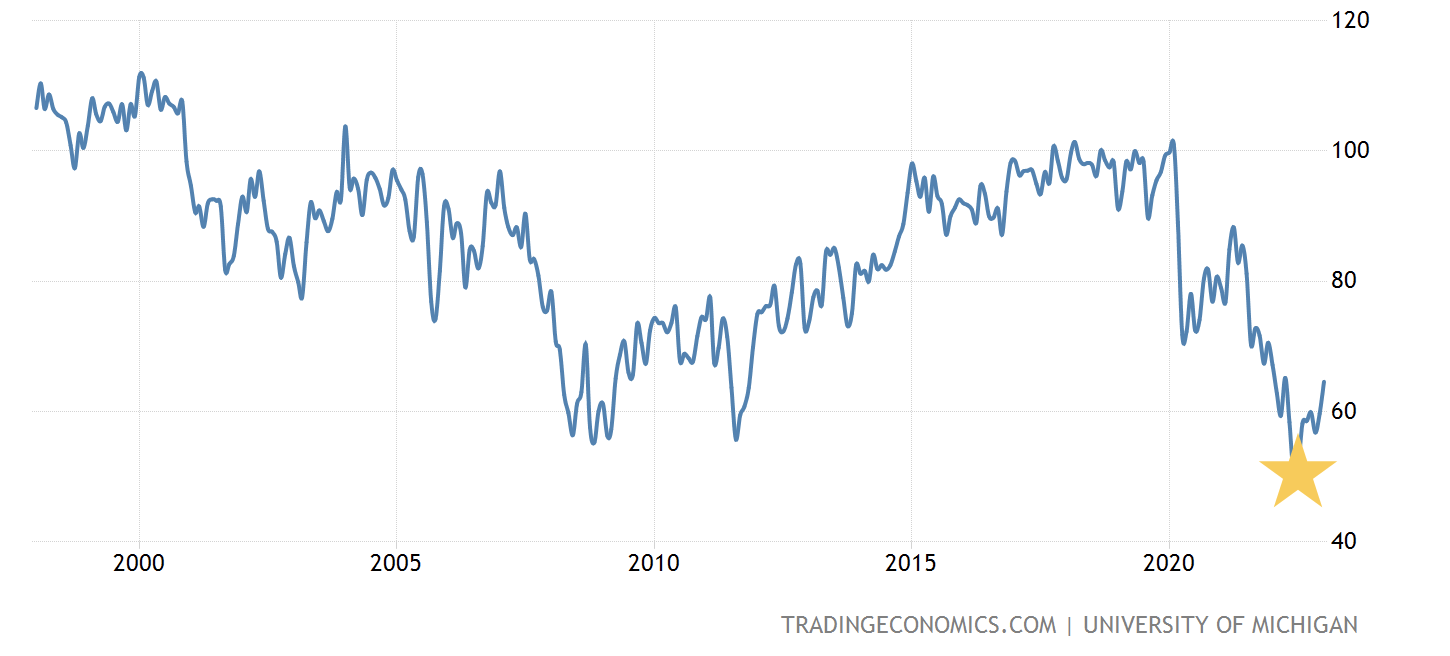

Since our last writing in May 2022, consumer confidence has somewhat improved, but continues to remain at historically low levels.

U.S. Consumer confidence (Tradingeconomics.com)

The continuing poor sentiment is likely to keep negatively impacting the spending behaviour of the consumer, likely resulting in weak demand for durable and non-essential products. In 2022 this phenomena has already been observed as RH’s Q3 revenues have declined to $869 million versus $1.006 billion a year ago. As long as inflation is elevated and recession fears exist, we believe it is not likely to see a dramatic improvement in demand.

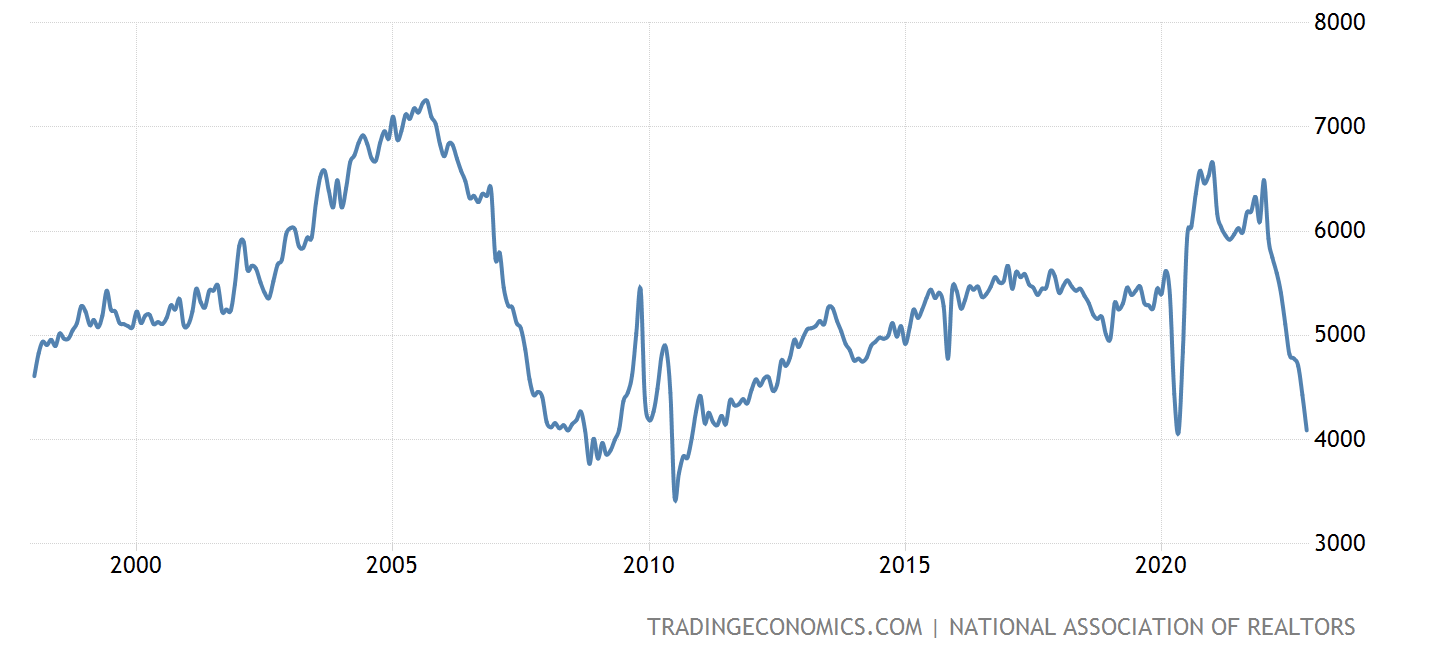

Housing

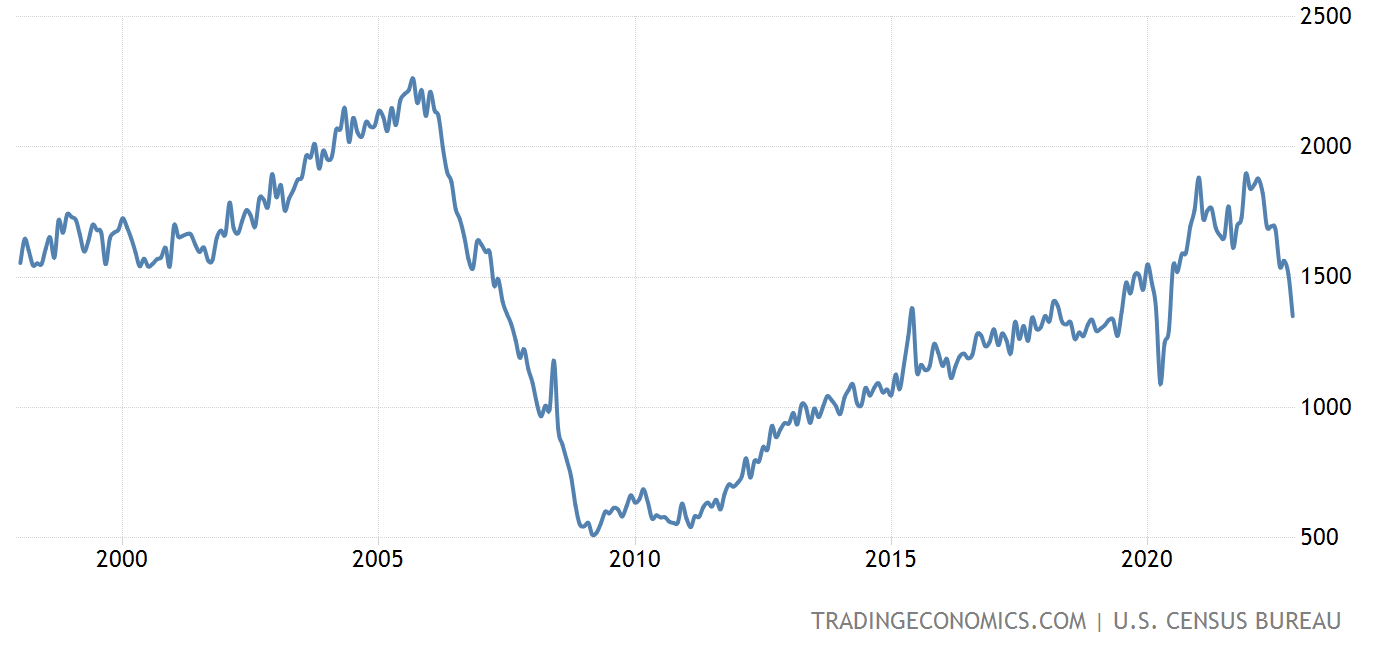

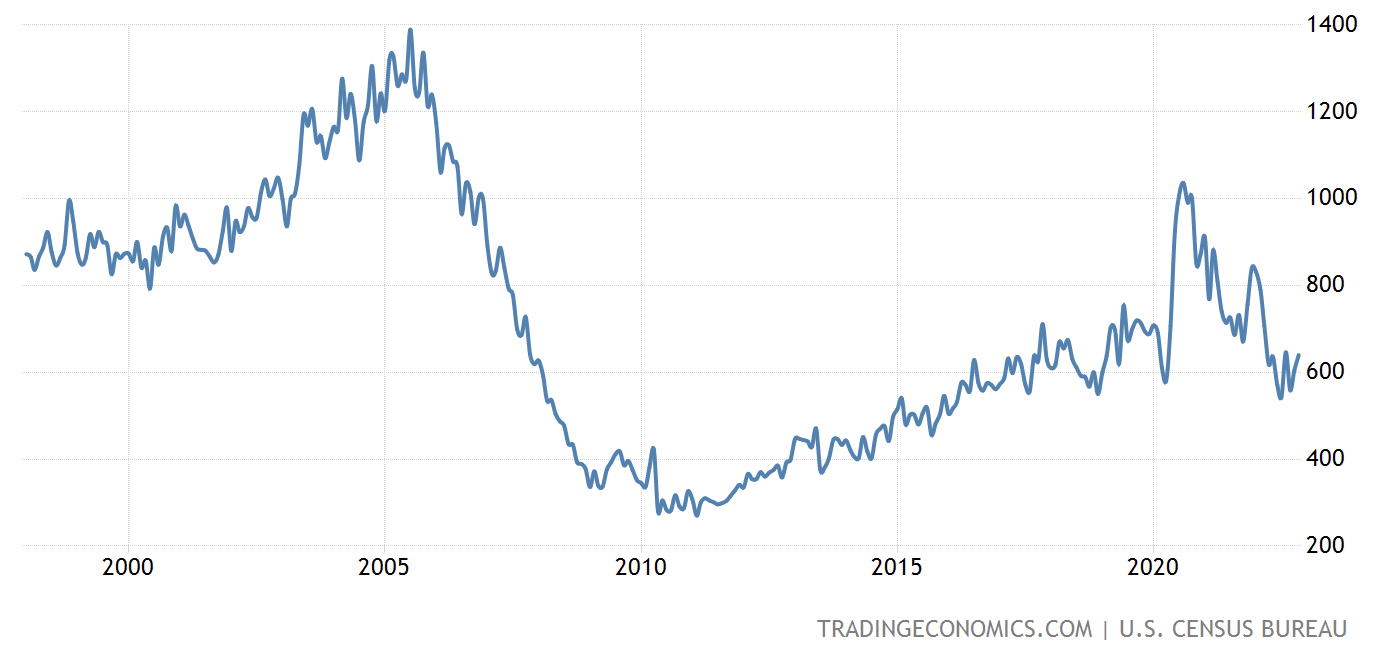

The housing market also appears to have been slowing rapidly in the previous quarters. Both the number of building permits in the United States and the new/existing home sales figures have been declining sharply.

U.S. Building permits (Tradingeconomics.com) New home sale (Tradingeconomics.com) Existing home sales (Tradingeconomics.com)

As long as the interest rates are elevated and uncertainty about the terminal rate exists, the demand and size of mortgages for homes are likely to remain suppressed. The slowing housing market may also negatively impact RH’s financial performance. Management has also acknowledged the negative impacts:

As noted in our previous shareholder letter, we expect our business trends will continue to deteriorate as a result of accelerating weakness in the housing market over the next several quarters and possibly longer due to the Federal Reserve’s anticipated monetary policy and the cycling of record COVID-driven sales and backlog reductions.

RH’s Q3 results and comments

As already mentioned, RH’s Q3 revenues have fallen to $869 million versus $1.006 billion a year ago, while the gross margin has contracted 50 basis points, primarily driven by fixed occupancy deleverage, partially offset by an increase in product margins. On the other hand, the company has delivered a 20.8% adjusted operating margin in Q3, exceeding their own outlook.

The declining sales together with the relatively stable margins are a reflection of the firm’s long term strategy. Management has made the following comment in their letter to shareholders:

As previously mentioned, widespread discounting continues across our industry, and while it’s been almost two years since we’ve deployed a promotional email, we’ve been receiving two sale emails per day from many home furnishings retailers. Although the stark contrast in strategy may lead to a short-term risk of market share loss, we believe there is certain long-term risk of brand erosion and model destruction for those who choose the promotional path. […] It’s that discipline and long-term thinking that has enabled us to set new standards for financial performance in the home furnishings industry and our results now reflect those of luxury brands as we delivered a 20.8% adjusted operating margin in the third quarter, […]

One of the advantages that we have highlighted in our previous writing about RH was their solid margin performance. From this perspective, we are pleased to see that they keep their focus on the margins. For this reason, we do not expect a significant contraction. On the other hand, investors need to be aware that market share loss now might be costly in the longer term. Expenses may increase as the firm tries to regain their past customers.

As a result, revenues are expected to have fallen by 3.5% to 4.5% in fiscal 2022.

RH has been recently downgraded at Goldman Sachs on margin concerns. We partially agree with this downgrade as demand is indeed likely to weaken, but management has clearly stated that they are focusing on keeping their margins stable. Therefore, the margin concerns at Goldman may be too pessimistic. The pull-forward of demand may also be taking place, as along with RH’s net revenue decline, accounts receivable have slightly increased. It may be an indication that RH is offering more favourable credit terms in order to maintain its sales.

We are downgrading RH to Sell from Neutral on our view that sales will likely remain pressured, given purchases are discretionary and larger ticket, the likely pull-forward of demand and highly promotional environment,[…]

Goldman has also assigned a price target of $215 per share, representing a 30% downside from the current price levels.

We also have to mention that in the long term, the recent acquisitions of RH may be able to fuel revenue- and profit growth.

Conclusion

While margins have remained relatively stable due to the firm’s reluctance to offer promotions and discounts, sales have significantly fallen. At the same time accounts receivables have slightly increased year-over-year.

The macroeconomic environment remains challenging as consumer sentiment continues to be poor and the housing market appears to be rapidly deteriorating as well.

Goldman has downgraded the stock on sales and margin concerns.

We are also downgrading the stock to “sell”. We would like to see the macroeconomic environment improving, before we would again consider owning the stock.

Be the first to comment