Detry26/iStock via Getty Images

Recommendation

My recommended rating for Reynolds Consumer Products (NASDAQ:REYN) is neutral. I believe the macro outlook and management’s constant change in guidance are not doing any good to the stock. While the business has structural competitive advantage that I like, I believe the stock’s near-term performance will revolve a lot around guidance and when the world is going to recover from this recessionary period. As such, my verdict is to put off any thoughts of purchasing the stock until valuation is much cheaper.

Business

REYN is a producer and vendor of household packaging materials. Aluminum foil, plastic wrap, oven bags, and slow cooker liners are just some of the products the company sells to aid in meal prepping, cooking, cleaning, and storing.

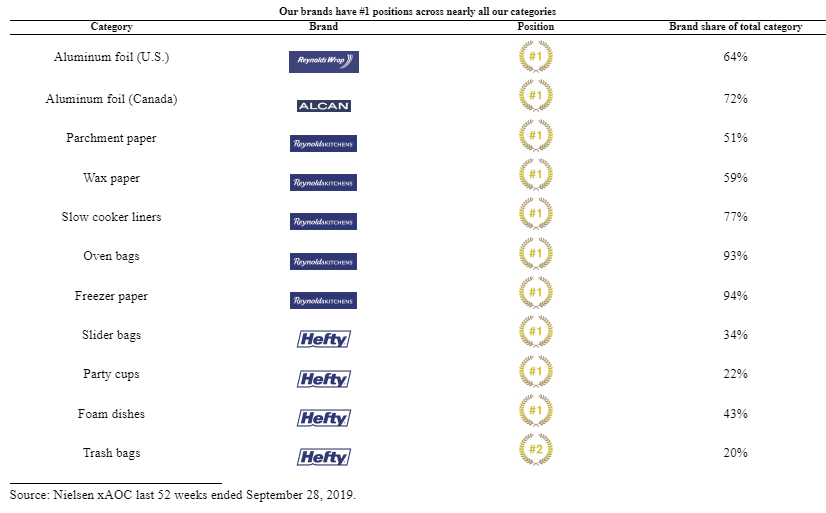

Leading market position

There is a REYN product in the vast majority of homes across the United States, making it the market leader in its field. It markets its wares under well-known labels like Reynolds and Hefty. Products in which REYN has the largest share of the U.S. market are the primary driver of revenue for the company, both for its branded and store-brand offerings. Moreover, REYN is in the top two in terms of market share based on revenue in almost all of its major product categories. This chart from a while back shows how popular REYN products are even though the information is a little stale now.

S-1

Strategic relationship with customers

REYN has built a solid reputation over the years, and the company has also forged important partnerships with industry heavyweights. Throughout their many end points, REYN’s customer relationships are founded on a solid foundation of trust. REYN has been in business for over seven decades, and they continue to work with many of its original customers. An experienced sales force, with an average tenure of over 10 years, is another key factor in REYN’s ability to maintain its high standard of service and delight its clientele.

Not only that, but the most of products are manufactured in the U.S. Additionally, RENY’s nationally dispersed manufacturing footprint offers logistical benefits and supply-reliability assurance to retail partners thanks to its carefully chosen locations. I think REYN’s major customers greatly appreciate the shorter supply chain it provides in contrast to rivals and the vendor-managed stock control it provides to prevent product shortages.

Manufacturing footprint is a competitive advantage

For a manufacturer, REYN has a sizable footprint, with over 5,000 workers spread across more than ten factories. REYN is able to maximize distribution efficiency, lessen the length of delivery times, and cut down on transportation expenses thanks to these inexpensive and effective production facilities. I think this large production base, established over many years, gives REYN an advantage over rivals. Management has determined that it would cost more than $2.5 billion to recreate REYN’s manufacturing assets.

This is not only an economically daunting task, but it would also be extremely challenging to duplicate REYN’s in-house manufacturing expertise and technology that allow their machines and equipment to operate faster, consistently rolling out lean manufacturing projects at each location, with the goals of decreasing waste, increasing uptime, and maximizing output. There is a lot of automation at all of REYN’s facilities, and I think that the company’s proprietary manufacturing technologies and automation processes make it hard for rivals to catch up.

Moreover, REYN’s large size and depth of vertical integration give it a significant advantage in the market. REYN’s extensive vertical integration grants reduces its dependence on suppliers and enables it to better manage costs. Further, it helps cushion the blow of import price swings.

Innovation capability is also an edge

While it may be a cliche, being creative and innovative is a significant benefit. Most notably when trying to appeal to customers whose tastes are constantly shifting. REYN has a history of success in the realm of innovation, with the company’s efforts having been directed toward the incorporation of novel features into its already established product lines and the creation of brand new lines to meet the needs of consumers.

At the heart of REYN’s innovative capacity is the company’s prodigious knowledge of consumer preferences and behavior. Remember what I said up top about REYN’s long operating history and long-standing relationships with customers? They help with REYN gathering such insights. Based on these observations, REYN is able to design products that offer the qualities and performance levels sought after by customers.

3Q22 earnings

Ecommerce channel has room for growth

Due to the ease of online ordering and delivery, I expect REYN to have increase its penetration into e-commerce channels, particularly for categories of products that can be shipped cheaply and quickly. In my opinion, REYN is in a good position to compete profitably and increase its share of the rapidly expanding online retail market because of its strong relationships with online retailers. More importantly, I think it’s important for REYN to offer both name-brand and private-label options through their online store to appeal to the widest possible audience of online shoppers. Furthermore, most REYN products are suitable for the e-commerce channel as they have a long shelf life and require little to no extra packaging.

Levered balance sheet not an issue

The high leverage ratio of REYN compared to other Staples companies is a potential cause for concern among investors. REYN’s net debt to EBITDA as of 3Q22 is around 4.1x. Getting debt down to 2x or 2.5x EBITDA seems to be a top priority for REYN’s management, so I expect the company has already begun taking steps in that direction. If REYN spends half of its free cash flow (generated between now and FY24) on debt repayment, it should have no issues reaching this target, according to consensus estimates.

Continuous revision of guidance is an issue

REYN’s 3rd negative guidance revision for 2022 in 3Q22 is definitely not a good sign. In 3Q22 earnings, management revised its commentary about FY23 preliminary guidance it shared in the 2Q22 quarter. The company, in my opinion, exaggerated the staying power of the volume spike caused by Covid and played down the price elasticity headwinds that would come from private labels. In addition, they don’t give themselves a big enough buffer in their projections to account for unforeseen difficulties, like the ones it encountered with its plant’s machinery. I believe these are all temporary problems that can be easily addressed, but in my opinion management must abandon its practice of lowering expectations in order to regain trust.

Valuation & model

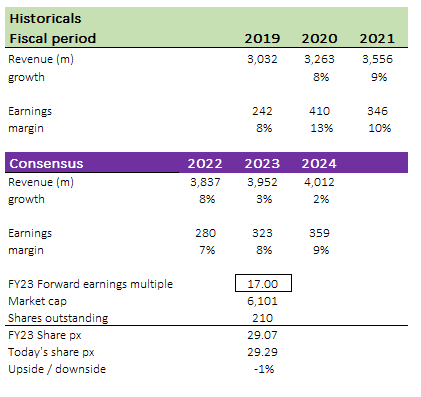

Using consensus estimates, I believe REYN is worth $29.07 in FY23, making the stock reasonably priced. The issue I have with REYN is a lack of visibility and trust in management’s outlook. As a result, the model incorporates a significant amount of conservatism (which I believe is the same case for consensus as well). When compared to the average and the expected growth slowdown in FY23/24, the valuation multiple today suggests a forward earnings multiple of nearly 19x. I believe valuation should drift downwards back to its long-term average of 17x.

If we consider all of these factors, as I have, I believe that now is not the time to invest in REYN.

Author’s own calculations

Risk

Green movement to non-plastic products

Environmental concerns have increased the pressure on businesses to reduce plastic production over the past few years. Since a considerable amount of REYN’s business stems from customers’ penchant for plastics, any new legislation passed by the US government requiring people to reduce their plastic-ware consumption could put a damper on REYN’s financial performance.

Summary

In my opinion, the stock is not being helped by the fact that management is constantly shifting its outlook and forecasts. Despite my optimism about the company’s long-term prospects thanks to its advantageous industry structure, I anticipate that the stock’s near-term performance will be driven more by forward guidance and expectations for an economic recovery. Therefore, until the stock’s valuation drops significantly, I wouldn’t recommend buying it.

Be the first to comment