jetcityimage

Dear readers/followers,

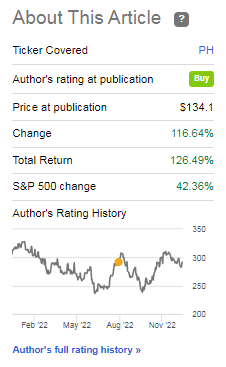

I write about Parker-Hannifin (NYSE:PH) about on a half-year basis, updating you on where this very solid company goes. Ups and downs aren’t rare here, with about double-digit movements in either away on a 3-6 month basis. Since my last article, we’ve been seen a drop back down – and a rise back up again.

There are ways to work this investment for a solid upside – and after the decline and updated numbers, let me show you what we have here.

Parker-Hannifin’s update after 3Q22

My first article on PH was during the coronavirus pandemic. Would you like to see how my return for my investment has been looking since that initial investment all that time ago back in 2020?

Seeking Alpha Article PH (Seeking Alpha)

This is how I invest, and how I believe most people should be investing. Buying quality at a cheap price, holding onto quality, and then trimming slowly as we reach overvaluation. I’ve done some trimming on PH as well, and I don’t regret that trimming.

My very early stance was to Buy and hold forever.

My updated stance is now actually that every investment has a “BUY”, a “HOLD” and a “TRIM” or “SELL”. I’m now very comfortable selling even quality if I believe the price is right, and I may reinvest at a better upside.

PH has been that, but I never trim everything – so I still have a position in this company.

This is a solid business. It was originally called the Parker Appliance Company, which is a business specializing in motion and control technologies. With a 103-year history, the company is old and has been publicly traded since the ’60s. Without exaggerating, Parker-Hannifin is one of the largest companies in the world specializing in these areas.

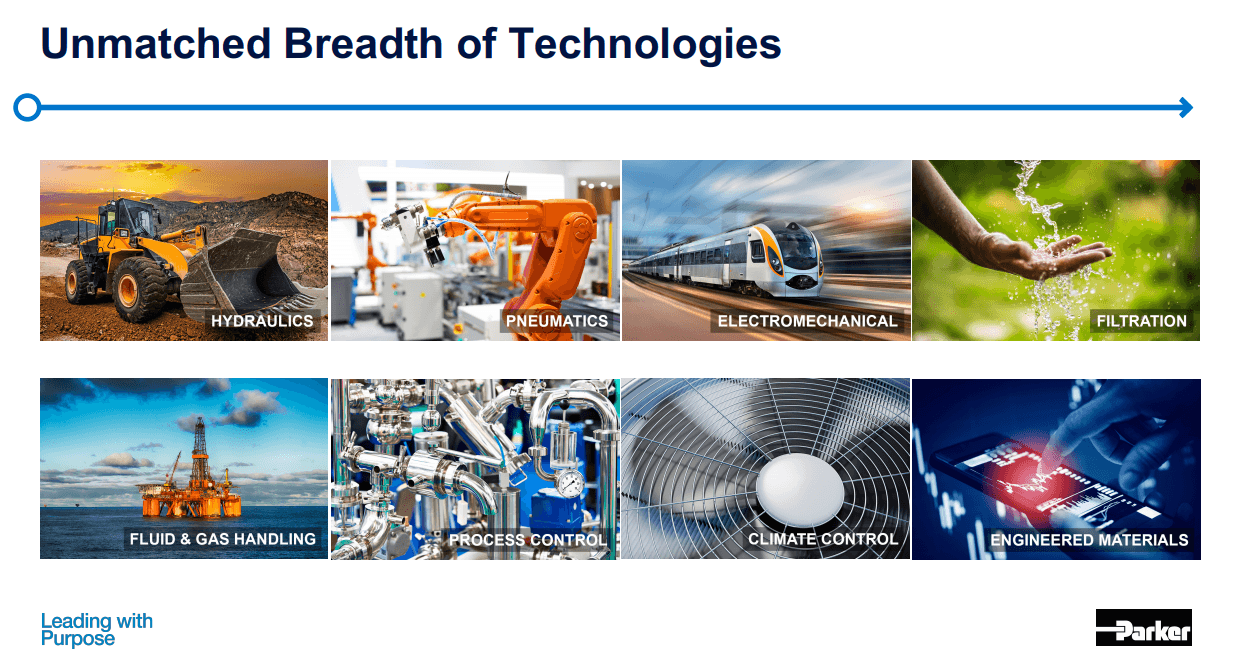

Motion & Control is a $140B global markets, and Parker is #1 in terms of overall market share in this market. The company has a breadth of technologies, capacities, and end markets that are staggering.

PH IR (PH IR)

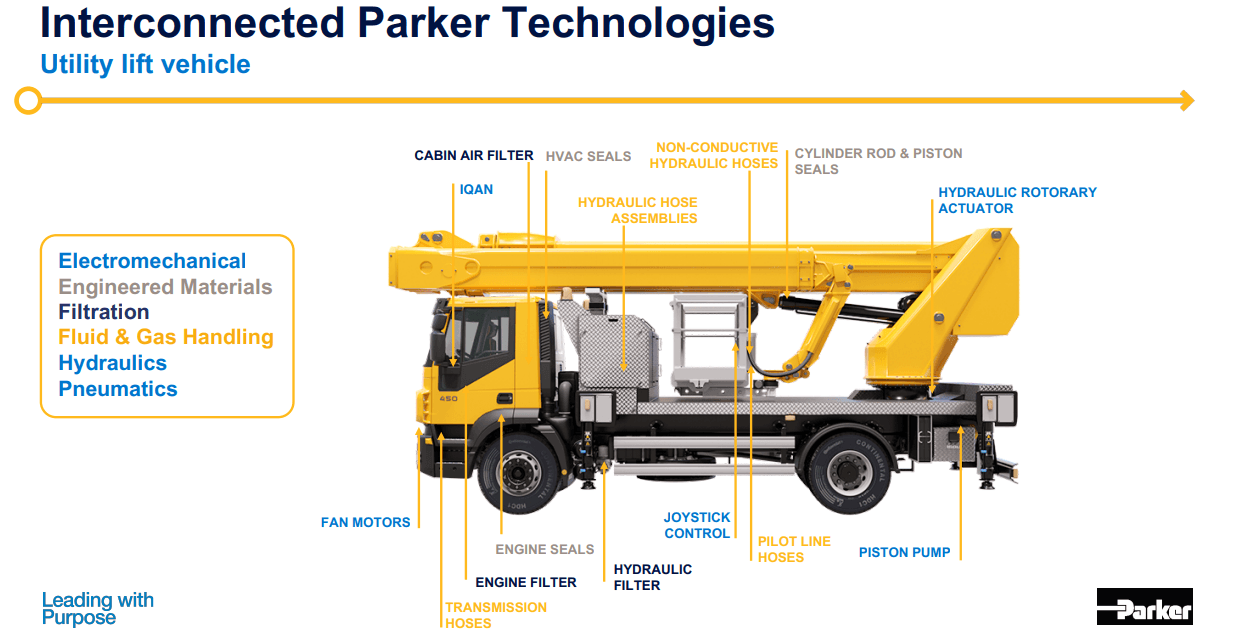

The company’s operations are split into a number of appealing segments, focusing on the technologies and expertise that Parker offers geographically, as well as the aerospace systems segment, which offers both commercial and military customers, with products such as control actuation systems, engine systems, fuel insertion systems, hydraulics, lubrication components, pneumatics, power conditioning, thermal management, brakes, wheels and metering products. Just in Aerospace, the company has end customers such as Airbus (OTCPK:EADSF), Rolls-Royce (OTCPK:RYCEF) and COMAC across the world.

The company’s actual products and end market can be better exemplified by looking at the company’s presentations.

Parker Hannifin IR (Parker Hannifin IR)

Now add to that every other segment the company works in, and you’re starting to get a picture of what the company does. While it may be exaggerated to say the world would stop without Parker, the company is certainly involved in some very crucial operations – not just new products, but developing better replacement parts and improvements overall as well.

In its operations, the company employs nearly 60,000 people all over the world and is headquartered in Ohio.

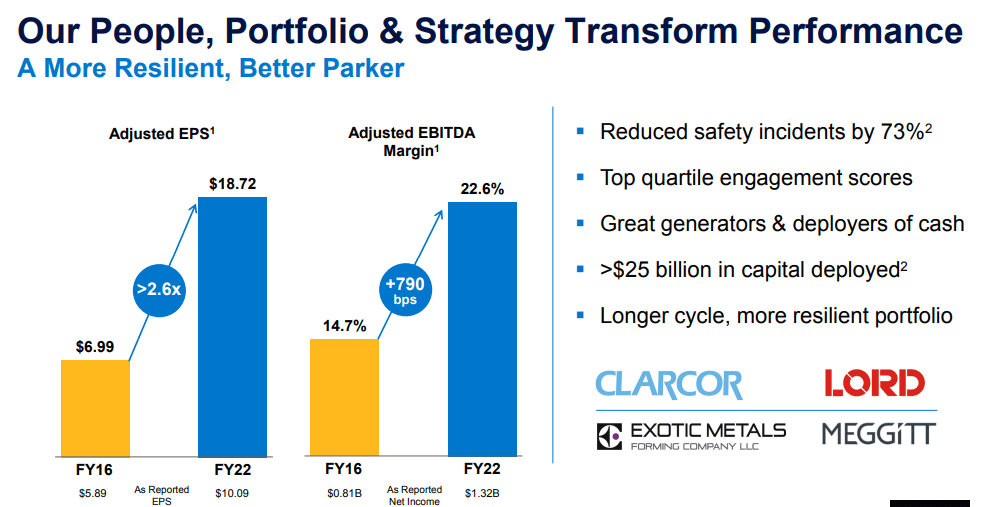

The results for the latest few years are superb, illustrating the reason behind the growth that the company’s share price has been seeing.

PH IR (PH IR)

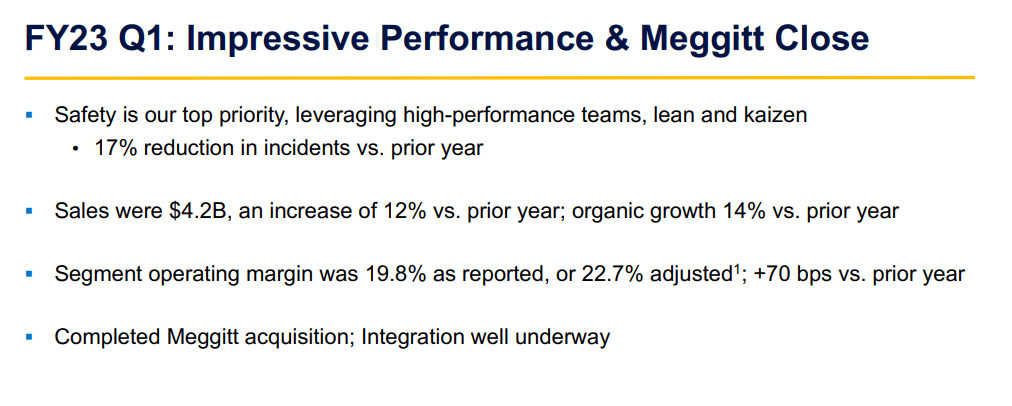

The company has been focusing on its fundamentals turning operations even more efficient. PH expects to deliver record-annual results for this fiscal. The last results we have are the 1Q23, and the company is continuing its acceleration.

The company has a confident set of targets for the fiscal of 2027E, and it’s currently very confident in reaching those targets for the next 4 fiscals.

So, a quick recap – market leader in the Motion & Control markets, and one that goes back over 100 years. The company works with a decentralized operating structure, with 88 divisions reporting to PH with P&L ownership.

The company has 17,000 global independent distribution outlets that generate 50% of the company’s annual industrial revenues. The company is already very much prepared for the move into clean energy and the like, because 66% and above is already enabling clean technologies.

PH’s goal is reaching a global market share of 20%. The company’s current market share is 13%, which is already impressive – but is expected to grow more.

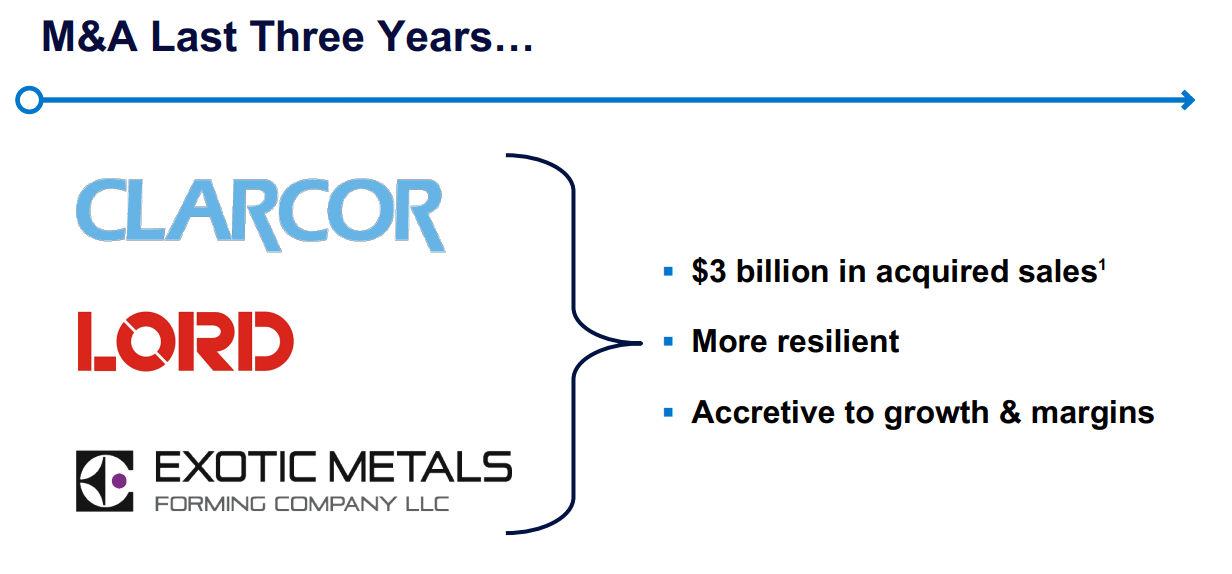

The company has already grown more efficient. Over the past few years, Parker has transformed – going from 126 divisions in 2014 to 88 divisions today in 2022 – and that includes multiple significant M&As. Aside from Meggit, here are a few more that the company has executed on.

PH IR (PH IR)

While not having worked personally with the company’s products in any direct way, I know of people even in Sweden who work with Parker, and their anecdotal evidence/opinion on the company is that the company’s thinking works – and results in higher sales and customer preference. Parker’s goal is to make “must-have” products of high value while at the same time improving margins and customer experience. This can only be done if the customer accepts the higher price point for Parker products – and so far, judging by results, customers do this.

When I first wrote about PH, the company was A-rated. Today, it’s down to BBB+, which is still great, but fundamentals are down somewhat. Furthermore, and as you can see from my articles, there’s a decent amount of stock price instability and volatility in this company. Less than a year ago it was at $334, now it’s at $290 – and has been below $250/share. There’s a decent amount of up and down here.

Sales and other numbers for 1Q23 were solid.

PH IR (PH IR)

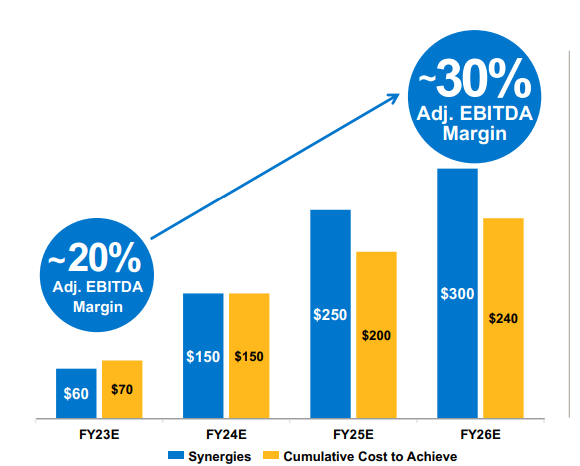

The company is in the rare position to have been able to expand EBITDA margins during a cost-increase cycle – and not by small amounts either, with an expectation of being able to repeat that performance in the next few years.

PH IR (PH IR)

The driver of these things, aside from what we see above, are things like a focus on a far longer product cycle. FY15, the company’s business had less than 25% Longer-cycle components. In 2027, that number is expected to be over 50%, which is expected to be one of the primary enablers of these trends.

The company’s EPS growth has gone up by 2.7x since 2016, and the EBITDA has increased by nearly 8% in terms of margins, more than doubling in straight EBITDA to $1.32B for the FY22 period.

Downsides and what is impacting the company’s bottom line and EPS are things like the company’s debt, which has been ratcheted up due to M&A’s, and where interest expenses are currently eating up much of the efficiencies the company is managing. It doesn’t take away from what I consider to be an absolutely killer quarter and future – and the reason for my shifting to “BUY” on PH here soon, but the downsides to the company are the debt and the very low dividend yield.

At current times, it’s no more than 1.83%, and any sub-2% dividend really needs to be justified and focused on prior to investing, as I see it.

Let’s look at the valuation for Parker Hannifin.

Parker-Hannifin Valuation

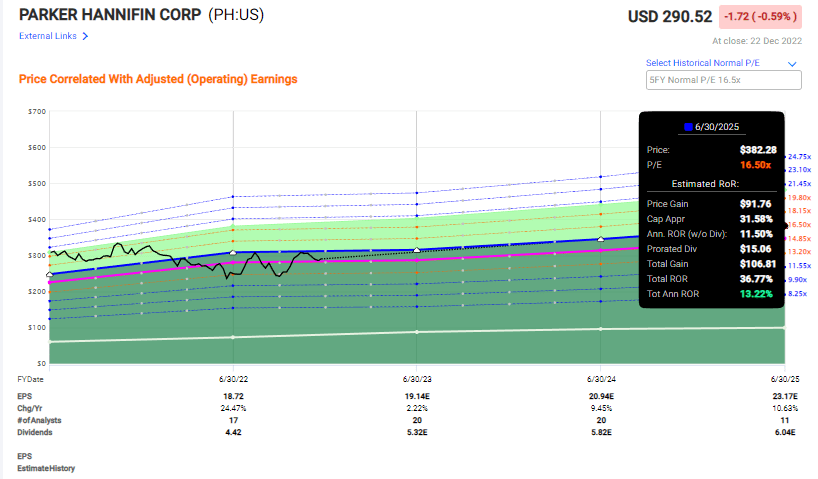

As mentioned, Parker-Hannifin typically trades at quite a bit of a premium between 15-20x P/E. During the crisis, as high as 22-23x, and lower/bottoming at times. During recent months, we’ve seen the company drop as low as 12.8x, which is where my interest has come into play.

Obviously, we have no plans to invest even into such a great company at massive multiples. The yield and the return potential are too low to interest us here – but that’s not where we are.

The average premium on a 5-year basis as things are currently seen is around 16.5x P/E, but today we’re at 15.3x P/E which is a discount to at least the premium for the company. Here is what you can expect out of Parker-Hannifin if you invest today, and the premium holds for the next 3 years – which, by the way, I believe it will.

PH Upside (F.A.S.T graphs)

So, that’s not a bad way to potentially spend your capital, with a double-digit potential for growth. But is it the best in this market, or even for this company? That’s a different question.

Because as unstable as things are right now, there are plenty of opportunities in the market. What I’m going to do in this specific case is highlight one play that I would consider as an alternative.

But first – analyst targets. S&P Global considers Parker-Hannifin to have an average target of $342, which is an upside based on $290 of 17.8%. That’s 18 analyst with a low of $260 and a high of $484 – a massive range. I would say $342 is far too high for this company and where I have been trimming my position.

In the last article, I gave PH a $270/share PT. That is no longer fair given the current macro and the company’s performance. The company has underperformed relative to my price target, but despite this, I’m raising it here.

I’m also considering the company a “BUY”.

Thesis for Parker-Hannifin’s Common shares

My thesis for Parker-Hannifin is as follows:

- Parker-Hannifin is a market leader in certain technologies, and a company that over the years has proven its ability to generate excellent earnings, as well as deliver on superb mergers and acquisitions. Its market sectors are through-cyclical, and secular growth trends should deliver continued upside here.

- However, the valuation at current times remains prohibitive for a market-beating upside. Only by assuming premiums of 16-18x do we see alpha, and this is not something I would want to invest in.

- Because of this, I remain at a “BUY” here for the time being, and my PT for the company is $300.

Remember, I’m all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company isn’t technically cheap, but it’s a “BUY” here.

The Options Play for Parker-Hannifin

As I said, I will also take a look at a different way to approach the company here. You could, if you have the capital, write a cash-secured put that grants a good upside for the company, even if there is a tricky bit with the company due to the sheer share price.

Here is a play I’m looking at.

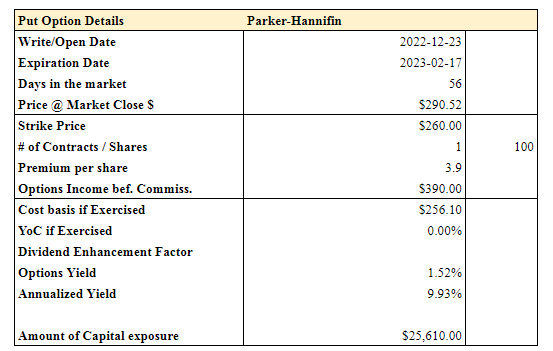

PH Options (Author’s Data)

So, a few problems with this one. First, the capital exposure is very high for 56 days, even at just one contract – depending on your net worth. Secondly, there’s a decent chance for assignment as I see it. Also, note that the options chain data is from yesterday – so I wouldn’t go into this one unless you can get a 10% annualized RoR in a 30-60 day period with a 10% or above movement from the stock price.

And then you still need the capital.

But if you can do this, then I would go for the options play. I’m considering it here, I’m not going to pull the trigger straight away. I’m keeping my common shares, and I’m keeping my eyes open.

Questions? Let me know!

Be the first to comment