Piotrekswat

The market has been tough in the year 2022. There is 40-year high inflation that is not only causing a lot of uncertainty in the marketplace but also impacting the working folks in their daily lives. Interest rates are rising, and the market is giving warning signs of a looming recession. But in spite of all the negative headlines, there’s no reason that you should not think of planning a successful and rich retirement with stock investments. In fact, the opposite.

We want to show our readers, especially the new and relatively younger investors – what’s possible with starting and investing early for the future. The earlier you start, the easier the path will be. Even if you’re late to investing and saving for the future, there’s no reason to be disheartened. After all, it’s better late than never, and there are ways to make up for the lost time. If you’re already into your late 40s or even 50s, you can still achieve financial freedom – it will just require a little more sacrifice and determination. Always start with reasonable and achievable goals first, and once you have achieved the first set of goals, build on them by setting new and higher targets. In this article, we will provide a retirement planning roadmap for a couple who has just turned 45 and they wish to retire by the age of 62.

So, why do we often talk of a million dollars? We talk about a million dollars simply as a milestone. Sure, a million dollars is not the same as it used to be just two decades ago. Most financial planners would now advise shooting for $2 million to have a comfortable retirement. Due to inflation, since early 2000, the buying power of one dollar has reduced to less than 60 cents today, and that’s not counting the current bout of high inflation. So, even with that basis, now you would need over $1.6 million to maintain the same standard of living as you could afford with one million in the early 2000s. But it is important to remember that everyone’s needs are different. For some, a million dollars could be a very tall target, while for others, it may be an insufficient amount to retire. So, it all depends on your own individual perspective and your current way of life. But for most everyday working folks, the first time they hit a million-dollar mark in retirement savings, it’s an important achievement. At the same time, folks who have retirement 20 years away (or more) should definitely target $2.0 million to retire comfortably.

So, how much do you need to retire? This can vary greatly from person to person, depending upon current income, basic living expenses, health status, personal spending habits, hobbies, availability of other sources of fixed income like pension and social security, and most importantly, the place where you may decide to live in retirement.

To plan for retirement, always start with some basic questions:

- What would be your basic expenses in retirement?

- How much savings would be enough to retire?

- When and at what age should you retire?

The above questions are critical to the planning process. As such, these questions are interrelated and interdependent. As such, there are no pre-set or generic answers. But first things first; how much money would you need in retirement for your basic expenses on a monthly basis? It’s mostly determined by your personal situation. We will try to answer this and other questions on a methodical basis in the next section.

For the vast majority of people, Social Security and Medicare play an important financial role in their retirement planning. For Social Security purposes, the full retirement-benefits age is considered 66 years, which gradually rises to 67 years for folks born in 1955 or later. The early Social Security benefits become available at age 62, albeit at 25%-30% lower rates. Medicare plans become available starting at age 65, which is essential for many folks to be able to retire. So, because of medical insurance necessity and Medicare eligibility at 65, most working folks plan to retire at 65. That said, we think one also should have a contingency plan to be able to retire a few years early (say at age 62), just in case it’s forced upon by any circumstances.

Let’s say you and your spouse just turned 45 and have not given serious thought to retirement. Well then, it may be just the right time to get into the planning process. You are not late, but there’s not much more time left to wait. It’s probably high time that you make a plan and put it into practice. For the purpose of this article, we will consider a couple who have just turned 45 and want to be prepared for retirement in 17 years.

Note: This article is part of our Retirement Series, where we write periodically on retirement themes. Each time, our focus is on a specific set of circumstances and age groups. At times, you may notice some repetition of some core principles and strategies, but they are necessary for the benefit of new readers.

All of the tables and charts in this article have been prepared by the author unless explicitly specified otherwise.

Part I: Retirement Planning for our Hypothetical Couple – John and Lisa

As usual, to make it easy to understand the concept, we would use our hypothetical couple – John and Lisa – to demonstrate the planning process.

Let’s assume John and Lisa are 45 years of age and wish to retire in 17 years at 62. It’s possible that they would change their mind in the future and may decide to work longer, but the idea is to be prepared to retire by the age of 62 or even sooner if they want to or have to. We will assume that they both work full time, and their current household gross income is $130,000 a year, which falls solidly in the middle-class income group.

Their current retirement savings are at $150,000, not a meager amount but nowhere close to where it needs to be. They’re mostly invested in tax-deferred plans like 401K and/or IRAs. We also have to account for the fact that the market has done exceedingly well in the last decade, except in the last few months, but the next decade may not be as good as the last one.

In any case, they have done a good job of accumulating the current savings of $150,000, and they have been saving roughly 6% of their paycheck. However, they will have to ramp up their savings rate to reach their goal of a million dollars in today’s dollars. According to financial planners, their savings should be roughly 5-7 times their current gross income by the time they are 55 years of age. In other words, in just ten years, they should accumulate roughly $700,000. So, clearly, they will need to make some tough choices if they hope to have a comfortable retirement starting at 62. They would have to make some sacrifices now and cut down some of their discretionary spending in order to save and invest more.

While trying to plan for their retirement:

- The first question they need to answer is how much savings would be enough for them to retire. Retirees of today have to plan for 30-40 years of retirement because people are living much longer than just a few decades ago. Also, it’s better to plan for longer and have some surplus left for your heirs or any other causes than running out of money in your 90s.

- The answer to the above question lies in the realistic estimate of expenses in retirement. If they underestimate, it can prove to be a big problem because that means that they would not have saved enough. If they overestimate it, they will end up with a much higher savings goal that may be unachievable or unrealistic. Sometimes it becomes disheartening and self-defeating when the goals appear to be totally out of reach. So, goals need to be realistic and achievable. Many financial experts suggest planning for about 75% of your pre-retirement expenses. We think it’s too high a target for most folks, and actual expenses in retirement may actually be much lower. Nonetheless, they should make an honest assessment of their estimated expenses in retirement.

Let’s make some more assumptions about John and Lisa’s situation.

- They currently carry a mortgage on their house and have 20 more years to repay in full. By maintaining the status quo, they will be taking the mortgage payments a few years beyond their retirement at 62. They definitely do not want to see themselves taking any debt into retirement. They decide that they will make slightly higher payments each month on the mortgage so that they’re able to pay off the house in 15 years instead of 20 years. They will pay $150 extra every month to pay off the loan by the time they are 60. This decision is very personal, as some would consider it wise to invest any extra dollars rather than pay off the mortgage early. But this is not a huge amount, and either way, it is not going to impact their goals much. But we are of the opinion that for most people, it’s better to take that extra burden off of your mind in retirement. It just helps you sleep better.

- John and Lisa decide that they will not carry any type of debt into retirement, be it car loans or credit cards.

- They will also need to save for college tuition fees for their kids. They will put $1,200 each month for the next ten years into their college savings fund. Anything above and beyond, their kids will need to work part-time or raise student loans.

- They currently have one new car on the five-year term loan. They will continue to make existing payments on this car. However, once this car loan is fully paid, they would start putting away $400 a month for a future car so that they would not need to finance another car whenever they need to replace it.

- Most importantly, they decide that they both will increase their current 401K contributions to 16% of their earnings. Now, 16% contribution sounds like a lot (up from 6%), but after some tax savings, it may be closer to 13%. Also, once the college expenses of their kids are squared off, they will bump the savings rate to 20%. This will definitely require some hard choices and sacrifices, but this is fundamental to reaching their retirement goals.

- John and Lisa also think that once they’re fully retired, they would move to a suburb that’s further out, and in the process, they should be able to buy a newer and smaller house with less to pay in property taxes and house maintenance. Also, they may even save some tidy amount left over. However, since this decision is so far out in the future, they would not count on any savings at this point and make their retirement financial planning independent of any such decision.

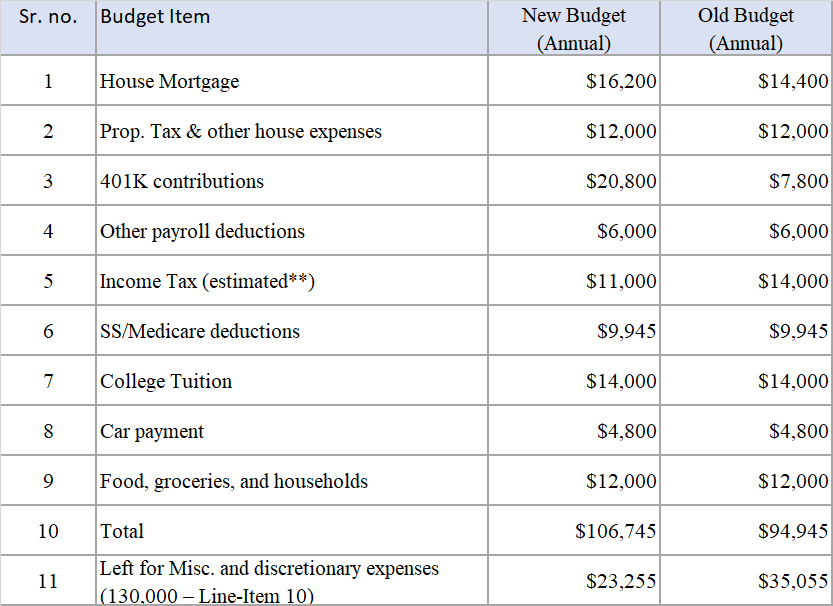

Table 1: John and Lisa’s New Budget (estimated) vs. Old

Author

** The author is not a tax expert/consultant. This estimate is just to provide a broad idea for the purpose of demonstration; the actual amounts could vary.

Estimation of Expenses in Retirement

To know the total savings requirement, they will need to first estimate their expense in retirement.

There are several ways to work out an estimation of expenses in retirement. Different people in similar situations will probably come to different conclusions. That’s why it’s important to keep some flexibility, and one should plan for a 10%-20% variation from year to year. We list some of the ways to get started:

- One method that we recommend and may be more accurate is to take your current household gross income and subtract all the expense items that you’re pretty sure that you would “not” incur in retirement. Also, don’t forget to add any additional expenses that you may have in retirement that you do not incur currently. It basically means figuring out how much of the money currently goes into items that will no longer be needed. Also, add any additional expenses that you do not have currently but may have during retirement. Then, adjust this remaining amount for inflation for the number of years that are left prior to retirement. This method will ensure that you are able to maintain your current lifestyle into retirement.

- Another method may be to multiply your current gross income by some percentage, like 70% or 80%. This is something many financial planners suggest, and sure, it works for many. However, in our view, it’s highly generalized, and for most folks, this results in an inflated savings goal that may seem unachievable.

Based on the first method, this is what John and Lisa came up with:

- When they retire, they will no longer need to put 16% or 20% savings contributions into their 401Ks or retirement funds.

- Assuming that they would not have any earned income in retirement (unless they decide to work part-time), they will not be putting any more money into Social Security/Medicare deductions (usually 7.65%).

- Their tax bracket may change to a lower slab, so they would need to account for that reduction.

- Besides, they will not have work-related expenses, like commuting, new clothing, dry-cleaning expenses, etc.

- They would be done with kids’ college education by then, which will cut down another $12,000 – $14,000 a year.

- They will not have the house mortgage payments anymore (monthly mortgage $1,200 or $14,400 yearly), based on the assumption that they plan to pay it entirely by that time.

- They will not have the current medical premiums that get deducted from their paychecks. However, they need to come up with extra dollars for the first three years (age 62 to 65) for some kind of private health insurance. Even after age 65, when they would be eligible for Medicare, they will need to earmark some extra dollars for buying supplemental Medicare plans. These supplemental Medicare insurance plans help payout for deductibles, copayments, and other costs that may not be covered by the basic Medicare plans (Part A and B).

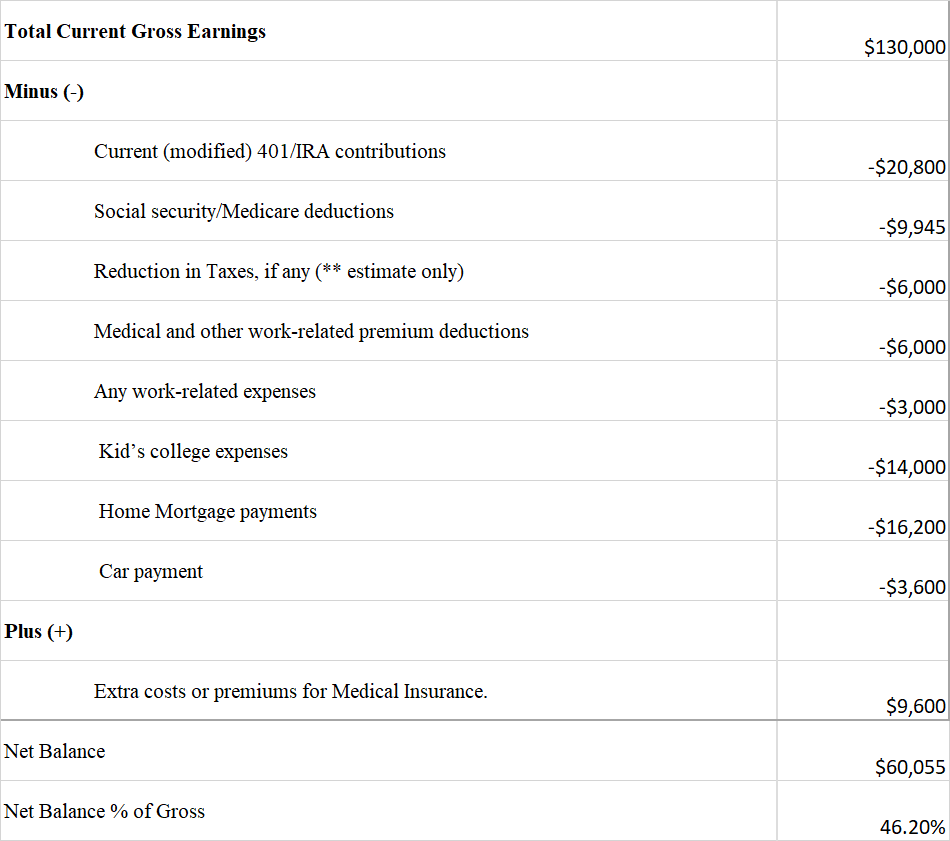

Table 2: Expenses in Retirement (broad estimates)

Author

In the above example, it’s easy to see that nearly 55% of their current gross income goes to expense items that they will no longer have to support or need in retirement. However, these are not universal numbers and can vary greatly based on individual situations. For example, in retirement, you may develop a couple of expensive hobbies, so your expenses may not go down that much. That said, for John and Lisa, it means that they should only require roughly 45% of their current gross income to support their existing lifestyle. However, to err on the side of caution, we would increase it to 50% of their current gross income, which comes to $65,000 a year based on today’s dollars. However, due to inflation in the next 17 years (assuming a long-term average of 3% a year), they will require roughly $107,000 a year. This is assuming that the current bout of extremely high inflation (nearly 8% to 9%) would not last; otherwise, we are going to have much bigger problems. Please note that we have also provided an emergency cash reserve of $50,000, as well as $72,000 extra for health insurance expenses for the first three years.

Table 3: Expenses in retirement after inflation

|

50% of the current gross income: |

$65,000 |

|

Inflation-adjusted Amount (17 years later): |

$107,435 |

|

Total: (Approx.) |

$107,000 a year |

How Much Savings are Needed?

Since John and Lisa have worked out their yearly expenses budget in retirement, they can easily determine how much of the total savings they would need by the time they retire.

Important Caveat: We are assuming that social security benefits will be available in the current form for the couple in 2039 (17 years from now). However, this may change. If there are any changes or reductions in the social security benefits (which is entirely possible that far in the future), such changes will impact the workings of this model presented here.

In fact, John and Lisa have a few options to consider with regard to the optimal age when they should draw on Social Security:

- Since they’re planning to retire at 62, they will need to fund private health insurance for the first three years before they become eligible to enroll in Medicare health benefits. Private health insurance is often quite expensive unless they are eligible for Obamacare. Even after 65, as mentioned earlier, they will need to provision for extra expenses on supplemental Medicare insurance premiums.

- Option-1: One of them would withdraw Social Security benefits at 62 but delay the other spouse’s benefits until the age of 70. The spouse who is expected to have larger benefits (of the two) should preferably delay the withdrawals. This can be researched and estimated based on the SSA’s (Social Security Administration) benefit statements or on their website. The rest of the income needs (from age 62 to 70) could be met from the investment portfolios.

- Option-2: Both John and Lisa could delay taking the Social Security benefits until the full eligibility age of 67 years (or 66 years and ten months). They could withdraw the entire income needed from their investment portfolios from 62-67 until they start taking the Social Security benefits. In this option, their withdrawal rate will be quite high during these initial five years, after which it will drop drastically.

- Option-3: Though there may or may not be an actual need, still one of them may choose to work part-time for a few more years and delay the social security withdrawals for both of them. The biggest advantage may be that they will be able to get health insurance from the employer and avoid paying for private insurance. This will also help bridge the income gap, and this will allow them to defer SS withdrawals by a few more years.

Each of the Options above has its pros and cons and should be considered carefully on an individual level. If you expect to live a long life, then it would be better to delay Social Security withdrawals until the age of 67 years (or even 70 years). Also, as explained above, the spouse whose Social Security benefits are likely to be larger should preferably delay the withdrawals.

For the purpose of this article, we will consider option 1 in detail. They would withdraw roughly 5%-6% from their portfolio from 62-70 years of age. Even though a withdrawal rate of 5%-6% may seem to be too high; however, as it’s demonstrated in the table below, they could easily afford this since it’s for a limited window of 8 years, after which the withdrawal rate would fall significantly to less than 2%. They could obviously withdraw more once in a while for emergencies or some special occasions.

Let’s consider Option 1 in more detail:

Both John and Lisa retire at 62. They do not opt for part-time work. Let’s assume that John will take Social Security benefits starting at age 62, and the approximate benefits work out to be $2,400 per month or $28,800 per year (after counting inflation increases). Since Lisa will wait to withdraw SS benefits until she is 70, her benefits will be much higher at approximately $3,600 a month (or $4,500 a month after counting inflation increases).

By doing some reverse calculations, here is what they would need:

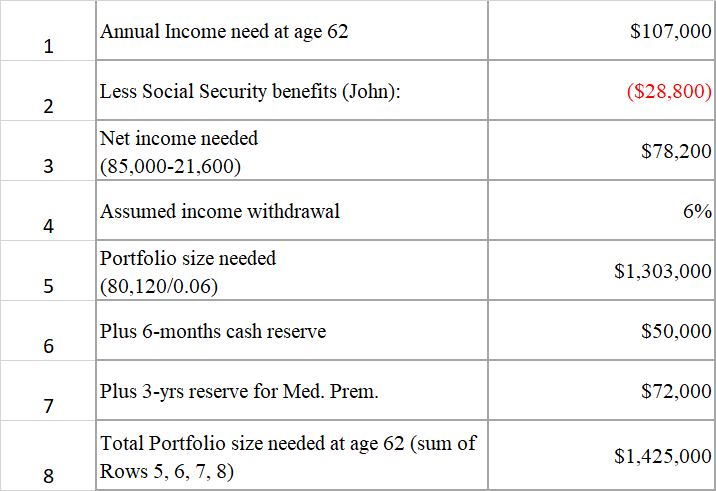

Table 4: Calculation of savings needed

Author

So, this couple will need roughly $1.5 million at the time of their retirement at 62 years of age (in future dollars in the year 2039). As the calculations below will demonstrate that they can easily reach their target if they can get at least 7.5% average annual returns over the next 17 years. We think it’s very reasonable and doable to get at least 7.5% average annual returns (this is average return, not sequential). If they are lucky and get a couple of percentage points higher, then their savings capital would be much higher. In fact, we will show in the later section how to achieve 10% returns safely on a long-term basis.

Investment Returns Calculations (Age 45-62)

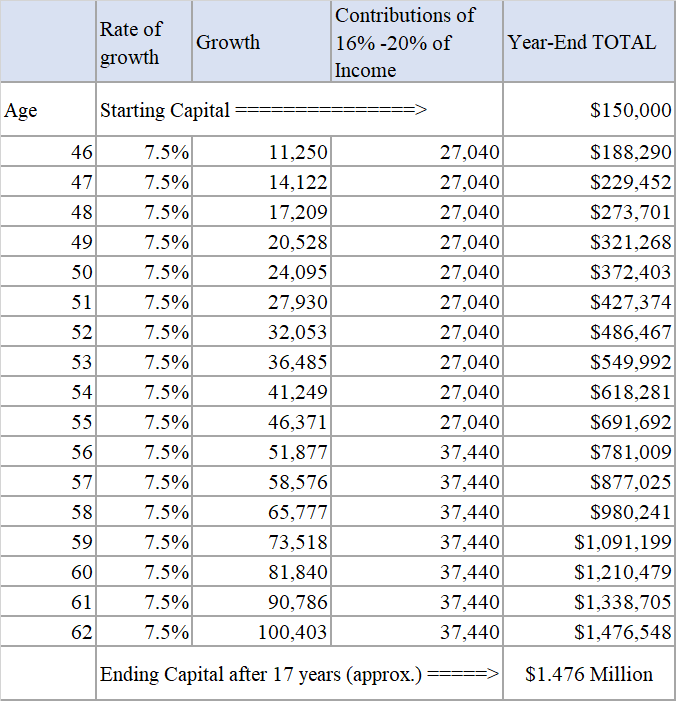

As is clear from above, John and Lisa have defined their savings target. Now they need a plan that could get them from $150,000 to $1.5 million-plus in 17 years. They assume that their investments would grow at a very conservative rate of at least 7.5% a year for the next 17 years, while they contribute 16% – 20% of income every year along with employer’s matching (assuming 80% on the first 6%). Also, their annual income is likely to increase with time, but to be on the conservative side, let’s assume it to be constant at $130,000.

At this point, John and Lisa want to make their assumptions as safe and achievable as possible. Even though they will target 10% annual returns, to provide an extra margin of safety, they will calculate the returns on the basis of 7.5%. As you can see below, even with 7.5% returns and a 16% to 20% annual savings rate, John and Lisa would accumulate $1.50 million and meet their savings goal.

Table 5A: Investment portfolio growth from Age 45-62

Author

If they’re able to grow the same level of savings at a rate of 9% or 10% average annual returns, their ending balance would be much higher, as shown in the table below:

Table 5B:

|

Average Rate of Annual Returns |

Ending Balance at 62 |

|

7.0% |

$1.4 million |

|

7.5% |

$1.50 million |

|

9.0% |

$1.75 million |

|

10% |

$1.95 million |

We know from the historical perspective that the stock market, over a very long period of time, can comfortably return 9% to 10% annualized returns. However, the big question mark is getting 7.5% steady growth over 17 years. However, we are not talking of sequential returns, but “average” returns. That means returns may be much higher in some years but lower or even negative in others. The above assumption about growth is a very reasonable expectation over almost two decades. However, there are no guarantees with the ups and down cycles of the market. The market’s ups and downs from year to year can change the outcome. If history is any guide, it can vary greatly depending on how the markets do in the first few years after investment. If there was a big setback right in the first couple of years, it would need time to recapture the losses and come back net positive. However, this is mostly the case when you’re invested in broad indexes. But there are strategies that you can build which can protect you from corrections and big drawdowns. We will address such strategies a little later in section II.

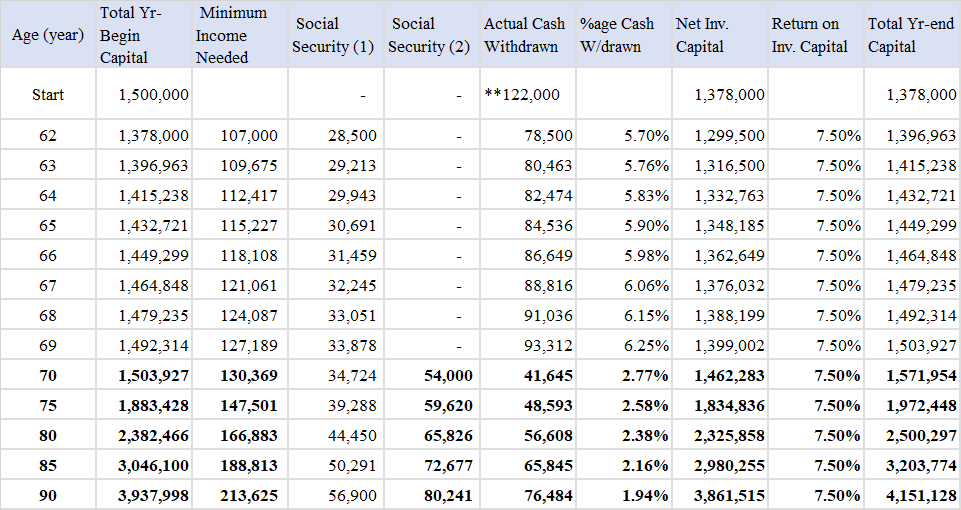

Retirement Years Age 62-90 – Calculation of Growth and Drawdown

For John and Lisa, during their actual retirement years, their strategy looks something like what’s presented below. If everything works out according to the plan, they should never run out of money. In fact, as you would see below, their portfolio would steadily grow after age 70 and more than double in the next 15 years while withdrawing and spending a substantial amount of income. That leaves plenty of scope for margin of error, and in all likelihood, they should never run out of money:

- At the start of retirement, they reserve nearly six months of expenses in cash from the total capital, a total of $50,000. They also reserve in cash $72,000 for medical premiums and expenses during the first three years of retirement. This leaves them with an investment capital of $1,380,000.

- Also, John would start withdrawing from Social Security at the age of 62 at the time of retirement. Due to early withdrawal, he will receive lower benefits compared to the full benefits. We will assume that SS-1 to be $2,400 a month in future dollars (at age 62), with COLA (Cost Of Living Adjustments) increases.

- This will allow Lisa to wait until the age of 70 years to collect and let the Social Security benefits be compounded to a much higher amount. We will assume that the SS-2 will be $4,500 per month, starting at 70 years (in the year 2047), with COLA increases.

- However, at age 70, due to inflation (from age 62-70 years), their expenses would go up each year as well (assumed at 3.0%). Now, this is the average rate of inflation. Sure, the current inflation is running very high, but it should cool down eventually (either by higher interest rates or by a recession, or both).

- They assume that investments of $1,380,000 (after cash reserves) will grow at a realistic and conservative rate of 7.5%. This is addressed in a later section.

Below is the table that simulates the income and withdrawals from the age of 62-95 years. As you can see below, with 7.5% growth, their balance would grow very nicely over the years, which provides them a large margin of error or overspending. However, we’re going to present two tables with 7.5% and 8.5% annual growth rates.

Table 6A: Calculation of growth and drawdown with a 7.5% growth rate

Author

** Cash-reserve of $50,000 plus Med Premium for three years of $72,000.

Note: Some rows (from the age group 72-74, 76-79, 81-84, 86-89, 91-94) have been hidden to keep the table size presentable.

Table 6B: Calculation of growth and drawdown with a 6.0 growth rate

Author

With a 6% annual growth rate, John and Lisa will be doing okay but not great. They are not likely to deplete their investments. As you can see in the above table that investments won’t’ even deplete by the age of 90, but it leaves them not much chance for any excess withdrawals or any mistakes. Anything less than 6% growth would risk depleting the portfolio with time, so a growth rate of 6% is the bare minimum.

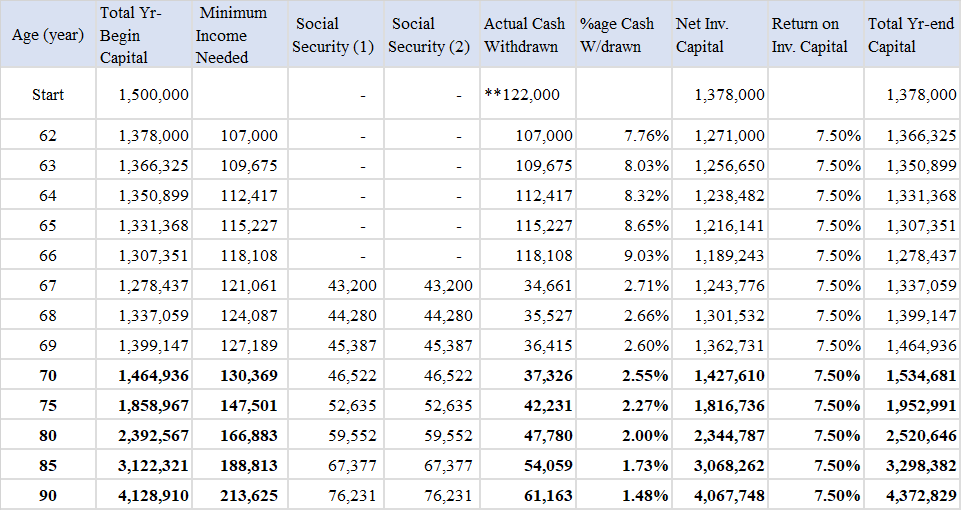

Now, let’s consider another scenario – What if both John and Lisa start withdrawing Social Security benefits at age 67? The overall results will be very similar – however, they would draw on the investment much more rapidly during the first five years of retirement. If the broader markets were to take a deep dive immediately after they retire, then this option may not be too desirable. Below is an example assuming they get 7% annual returns on their investments. We will see the calculations in the table below:

Table 6C: Calculation of growth and drawdown with a 7.5% rate, SS withdrawals at age 67

Author

Part-II: How to Achieve a 10% (or more) Investment Return Consistently

The important word here is “consistently.” The stock market is anything but consistent. The market never moves in a linear fashion. So, it’s important to understand the risks that come with putting all your money in the S&P 500 or any other set of index funds, mainly because in the investment world, ten years is not a very long time frame, and our portfolio will be subject to the risk of the sequence of returns.

Note: Sequence risk, or sequence of returns risk, is defined as the risk that the stock market crashes early in your retirement or just prior to retirement.

So, what’s the alternative? We will admit that there’s no perfect alternative. The volatility will be part of any investment. However, there are ways that we can reduce the volatility to a significant extent. Also, it’s a proven fact that the lower the volatility, the better will be long-term investment returns as well as consistency in returns. With this view, we will suggest a portfolio with two buckets (but preferably with three buckets) that will greatly reduce the risk of the sequential return and improve the consistency of returns.

- DGI Bucket: 40%.

- Rotational Risk-Adjusted Portfolio: 35%.

- Optional/Flexible Bucket: 25% allocation. This is a flexible bucket that could be invested in a variety of types of investments based on your age group. Since the simulations in this article are for folks in their 40s, we would recommend investing this bucket in high-growth technology stocks. Once the investors approach retirement, they could transition this to high-income CEFs (Closed-End Funds) to produce high income.

DGI Bucket: (40% of assets)

The goal of the DGI bucket will be to provide a safe and consistent 4% income in the form of dividends that should increase over time. Since our couple in this article is relatively younger and will still be working for many years, they should just reinvest the dividends automatically. The DGI stocks also tend to have lower volatility, so they would protect and preserve the capital better than the broader market during a correction.

If you’re a passive investor, you could choose to create a portfolio of dividend ETFs. However, if you’re an active investor, you should have a DGI portfolio of individual stocks. Not only would you save the fund fees (however low they may be), but you could buy your positions when they are attractively priced. Also, you would have the flexibility to aim for a higher dividend yield in the range of 4%.

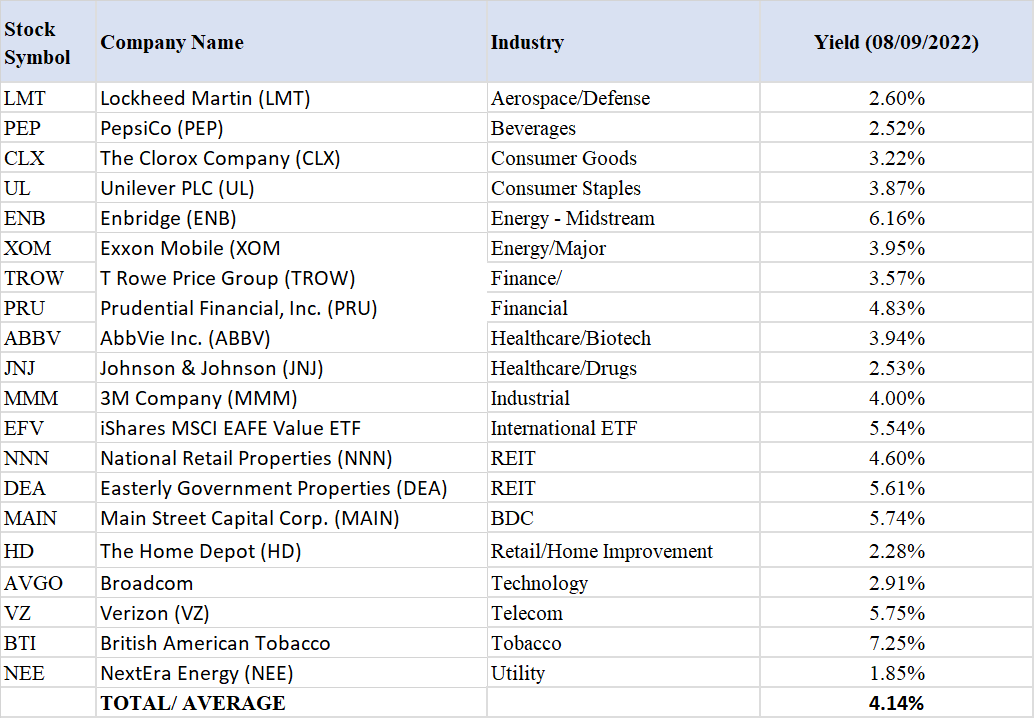

A sample list of 20 DGI stocks with a very attractive dividend yield of over 4% (average) spread over 15 industry segments is presented below. This is not a buy list per se – however, a starting point to do further research and due diligence.

List of Stocks: (LMT), (PEP), (CLX), (UL), (ENB), (XOM), (TROW), (PRU), (ABBV), (JNJ), (MMM), (EFV), (NNN), (DEA), (MAIN), (HD), (AVGO), (VZ), (BTI), (NEE).

Table 7A: A DGI portfolio of 20 Stocks

Author

Rotational Bucket: (35% of assets)

Rotational strategies are an essential part of our overall strategy. They not only provide the hedging mechanism (to preserve capital during panics and recessions) but also provide solid growth of capital on a long-term basis. Due to much lower volatility, this portfolio is likely to outperform the S&P 500 over long periods of time. However, it may underperform slightly during the bull runs.

One of the strategies that we like in the current environment is our Bull-and Bear Rotation strategy (this strategy is part of our NPP Portfolio and our Marketplace service).

The strategy is based on eight diverse securities but will hold any two of them at any given time, based on relative positive momentum over the previous three months. Basically, we will select the two top-performing funds. The rotation will be on a monthly basis. The seven securities are:

- Vanguard High Dividend Yield ETF (VYM)

- Vanguard Dividend Appreciation ETF (VIG)

- iShares MSCI EAFE Value ETF (EFV)

- iShares MSCI EAFE Growth ETF (EFG)

- Cohen & Steers Quality Income Realty Fund (RQI)

- iShares 20+ Year Treasury Bond ETF (TLT)

- iShares 1-3 Year Treasury Bond ETF (SHY)

- ProShares Short 20+ Year Treasury ETF (TBF)

Please note that the last three are long-term and short-term Treasury funds, which are used as hedging securities (TBF being SHORT long-term Treasury).

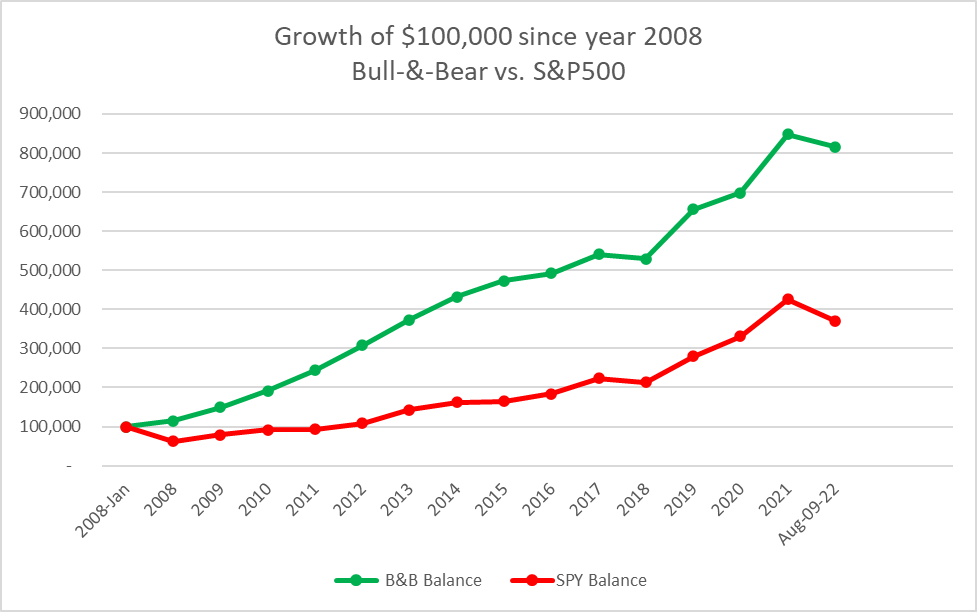

Based on the back-testing results, below are CAGR (Cumulative Annual Growth Rates) and maximum Drawdowns since the year 2008 (Jan.2008 until Jun. 13, 2022). The comparison is provided with the S&P 500.

Table 7B:

|

Duration |

Model – Bull-&-Bear |

S&P500 |

|

|

CAGR |

Since Jan. 2008 |

15.34% |

9.33% |

|

Max Drawdown |

Since Jan. 2008 |

-11.96% |

-48.47% |

Chart 1: Growth comparison for Bull-&-Bear portfolio and S&P500

Author

Note: The above performance results are based on back-testing and provide no guarantee of future results. Also, we do not recommend such a large allocation to this strategy overnight in a lump sum but rather build the position over a period of time.

If you decide to have a large percentage of your assets in rotational strategies, we recommend that you should have at least two rotational strategies to provide reasonable diversification, though it should be determined based on your personal situation in terms of time availability and preferences.

Growth Bucket: (25% of assets)

This bucket could mean different things to investors with different age groups. Younger folks (who are in their 40s) or those who are still in the accumulation phase and many years away from retirement could invest this bucket in high-growth names. However, you should choose these investments rather carefully. There’s a difference between growth stocks and speculative ones. One should invest in such stocks over a long period of time rather than in one lump sum. Also, please note that this bucket has no hedging mechanism, so it will likely have high drawdowns in case of a market correction.

One possible set of criteria to choose good growth stocks:

-

- Market capitalization > $10 Billion (preferably > $20 Billion)

- Forward EPS (3-5 years) Growth Estimates > 10%

- EPS Growth (3-year history) > 7%.

- Revenue Growth (last 3 years) > 6%.

- Revenue growth current year vs. previous year > 6%.

- Price-performance (52 weeks) > Price-performance-52-WK for S&P500 (or Nasdaq-100)

- Price-performance (13 weeks) > Price-performance-13-WK for S&P500 (or Nasdaq-100)

The above criteria can be adjusted higher or lower based on how many stocks come up in the filtered list. Based on the above, currently, the following ten stocks stand out (in our view). However, this is just a filtered list, further research will be needed.

Microsoft (MSFT), UnitedHealth (UNH), Mastercard (MA), Costco (COST), Accenture (ACN), American Tower (AMT), Cigna (CI), Synopsys (SNPS), Pioneer Natural Resources (PXD), Paychex (PAYX).

As investor approaches retirement, they should transition this bucket (at least partially) to high-income securities (CEFs, REITs, BDCs).

Risks to Consider:

Any discussion about stock investments without the associated risks is rather incomplete. Just like with any other strategy, there are certain risks that should be considered while analyzing the above investment strategies and other ideas that were discussed in this article:

- Risks of policy changes (Social security benefits): The retirement planning simulations discussed in this article depend heavily on the social-security benefits and policies as they exist today. It’s always a possibility that some of these policies could change in the future, or some of the benefits may get reduced in some ways, especially for younger workers. It is always a good idea to be aware of such a possibility and have a contingency plan.

- Timing risk: Some of the returns in the stock market depend on when you entered a trade. If you buy a great stock at the peak of the market, returns may still not be that great. It will take a long time before you can expect decent returns. To be clear, we are not advocating timing the market but rather avoiding the market timing. If you are starting a new portfolio (let’s say a DGI portfolio), it may be best to avoid a lumpsum purchase and split it into multiple purchases over a period of time. If you are investing in a 401K plan every pay period, it automatically solves this problem.

- Risk of Sequence of Returns: This risk is more relevant for folks when they are approaching retirement or have just entered into retirement. Investors who are old enough would remember that anyone who invested at the market peak in the year 2000 would have had a tough time recovering from the bear market losses. However, allocating some of the capital to a Rotation strategy (similar to one discussed in the article) can provide the necessary hedge and mitigate this risk to some extent.

- Rotational strategy risks: The rotational strategies work great in a bear market (or large correction) to provide a hedge against a falling market. They do not work very well in a stagnant market. Also, during a bull market, they may work great but still tend to lag the broader market. For these strategies to beat the market in a very significant way, they need to go through a complete cycle of bear and bull markets. Basically, expect them to do wonders on a long-term basis, but not so much in short to medium term.

Concluding Thoughts

We think it will be highly relevant to remind of the old saying that “The time in the market is more important than timing the market.” The sooner you start saving and investing, the easier it will be to reach your goals due to the compounding of investment returns. We cannot emphasize enough the importance of planning for retirement and investing at an early age.

That said, we believe it’s better to be late than never. If you’re already in your 40s, it becomes even more important to consider various options to see how you could reach your goals in a realistic manner. There’s still ample time to make up for any of the lost time. However, the more you delay it, the harder the choices will become.

In the second section of the article, we presented a strategy with three buckets that would not only provide a high level of growth but would also lower the volatility and drawdowns to a significant extent.

Be the first to comment