Brett_Hondow/iStock Editorial via Getty Images

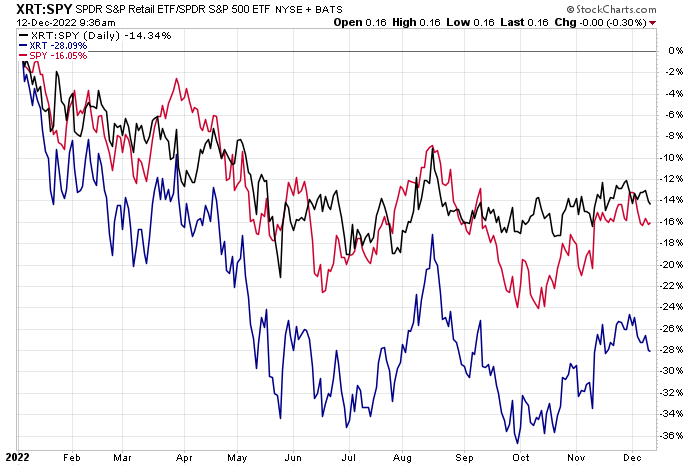

Retail stocks are not off to a hot start to December relative to the S&P 500. The group is down a few percentage points, as measured by the SDPR S&P Retail ETF (XRT). There are big concerns regarding how the consumer will fare now and in 2023 as excess savings continues to dwindle amid an environment where the Personal Saving Rate has dipped to its lowest level since 2005. Will Rent-A-Center (NASDAQ:RCII) buck the trend? Let’s investigate.

Retail Stocks Continue To Underperform In 2022

Stockcharts.com

According to Bank of America Global Research, Rent-A-Center is a leading omni-channel lease-to-own provider primarily serving credit-constrained consumers. Rent-A-Center comprises four operating segments: (1) Acima: virtual and staffed LTO solutions for retail partners in stores and online, (2) Rent-A-Center Business: ecommerce platform and nearly 2,000 company-owned stores, (3) Mexico: over 100 company-owned lease-to-own stores, (4) Franchising: several hundred franchised stores under Rent-A-Center, ColorTyme, and RimTyme names.

The Texas-based $1.3 billion market cap Specialty Retail industry company within the Consumer Discretionary sector trades at a high 79.4 trailing 12-month GAAP price-to-earnings ratio and pays a high 5.7% dividend yield, according to The Wall Street Journal. The company declared a $0.34 dividend earlier this month after beating on both top and bottom-line estimates back in early November. In September, though, the management team cut guidance leading to a massive 17% slide.

Upside potential in the name stems from better sales related to its recent partnerships and better penetration with existing customers. Still, a weak macro landscape is a risk while cannibalization between its channels is a possible problem.

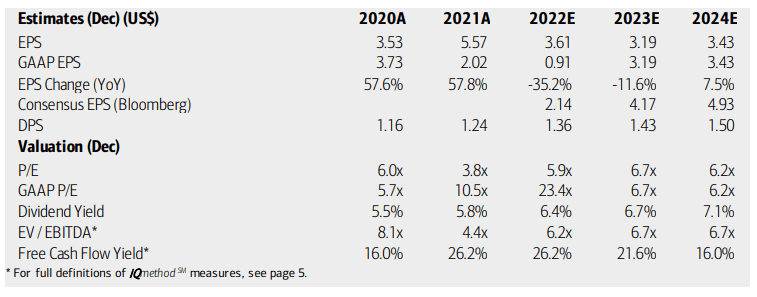

On valuation, analysts at BofA see earnings falling sharply in 2022 followed by a smaller per-share profit decline next year. A modest recovery is expected in 2024. The Bloomberg consensus forecast is more upbeat than BofA’s projection. The firm’s operating and GAAP P/Es appear low when using forward estimates, while its dividend yield should be on the rise. With a low EV/EBITDA ratio and very high free cash flow yield, I like the value story even with all the consumer risks.

RCII: Earnings, Valuation, Dividend Forecasts

BofA Global Research

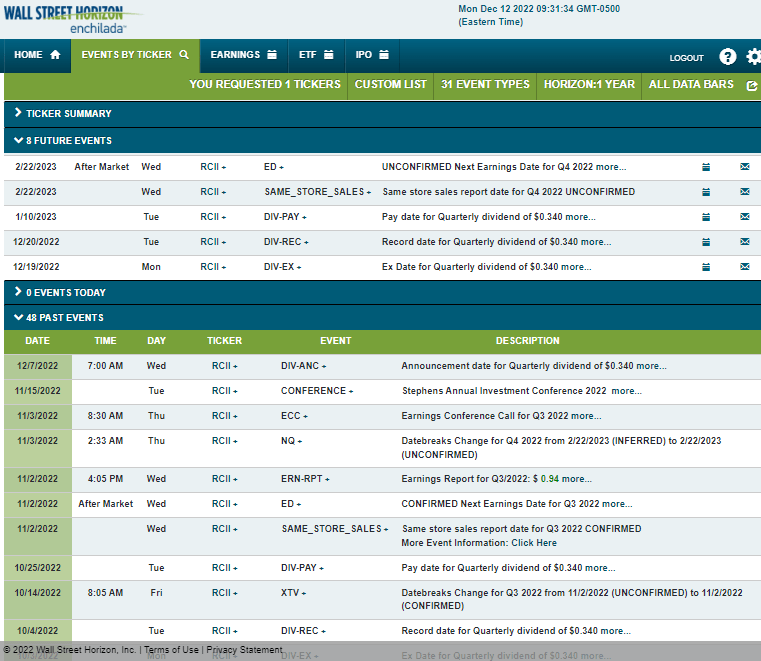

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Wednesday, February 22 after market close. Before that, the stock trades ex-div on Monday, December 19.

Corporate Event Calendar

Wall Street Horizon

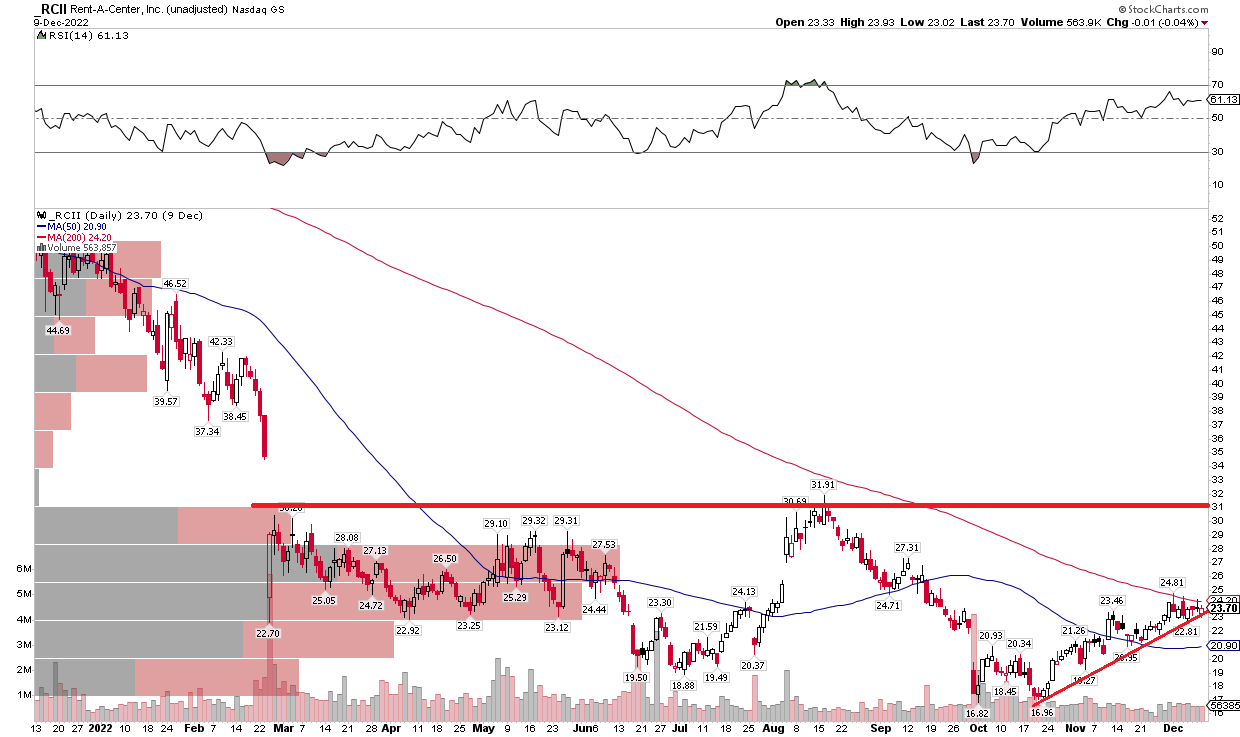

The Technical Take

With a cheap valuation amid a very uncertain macro landscape, what does price action say? RCII has recovered in a big way from under $17 in October to a key range in the low to mid-$20s. Notice in the chart below that there’s a high volume of shares traded in the $23 to $28 range, so this pause is to be expected. Moreover, the stock is finding some trouble at its falling 200-day moving average. Watch for a few more bucks of upside if shares climb above $25 with a final resistance spot near $32. I see modest support near $21.

RCII: Shares Rally Off The October Lows

Stockcharts.com

The Bottom Line

While risky, I like RCII’s value case here. The chart has consolidated recently after notching fresh YTD lows in October, so that price action is not ideal, but I think the valuation outweighs the chart here.

Be the first to comment