Art Wager/E+ via Getty Images

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on April 13th.

Real Estate Earnings Preview

Hoya Capital

Real estate earnings season kicks off this week, and over the next month, we’ll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies which will provide the first look into how the real estate industry is adapting to the shifting macro environment. This report discusses the major themes and metrics we’ll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders. (Note: Companies that have not yet confirmed an earnings date are in italics)

Hoya Capital

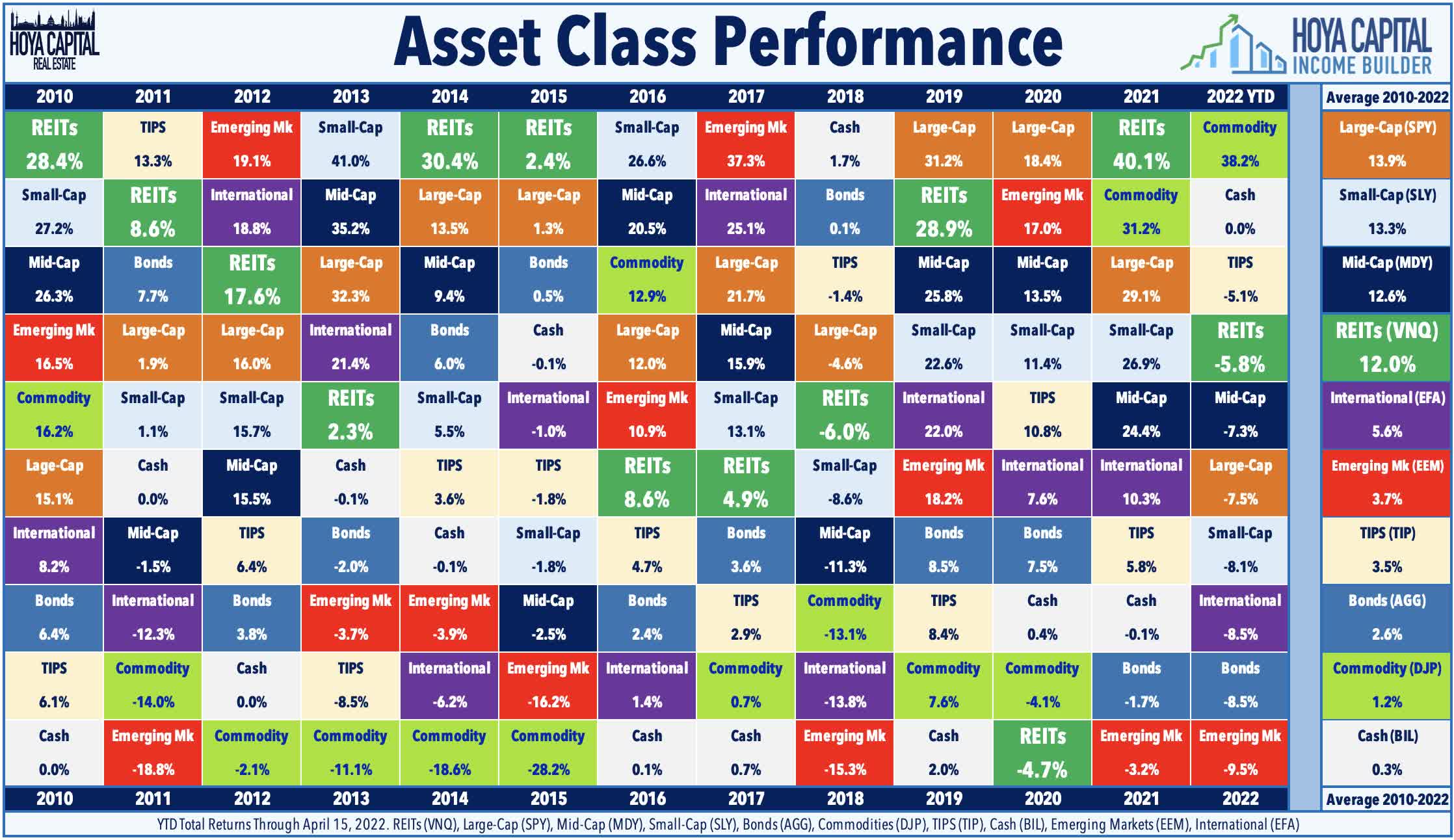

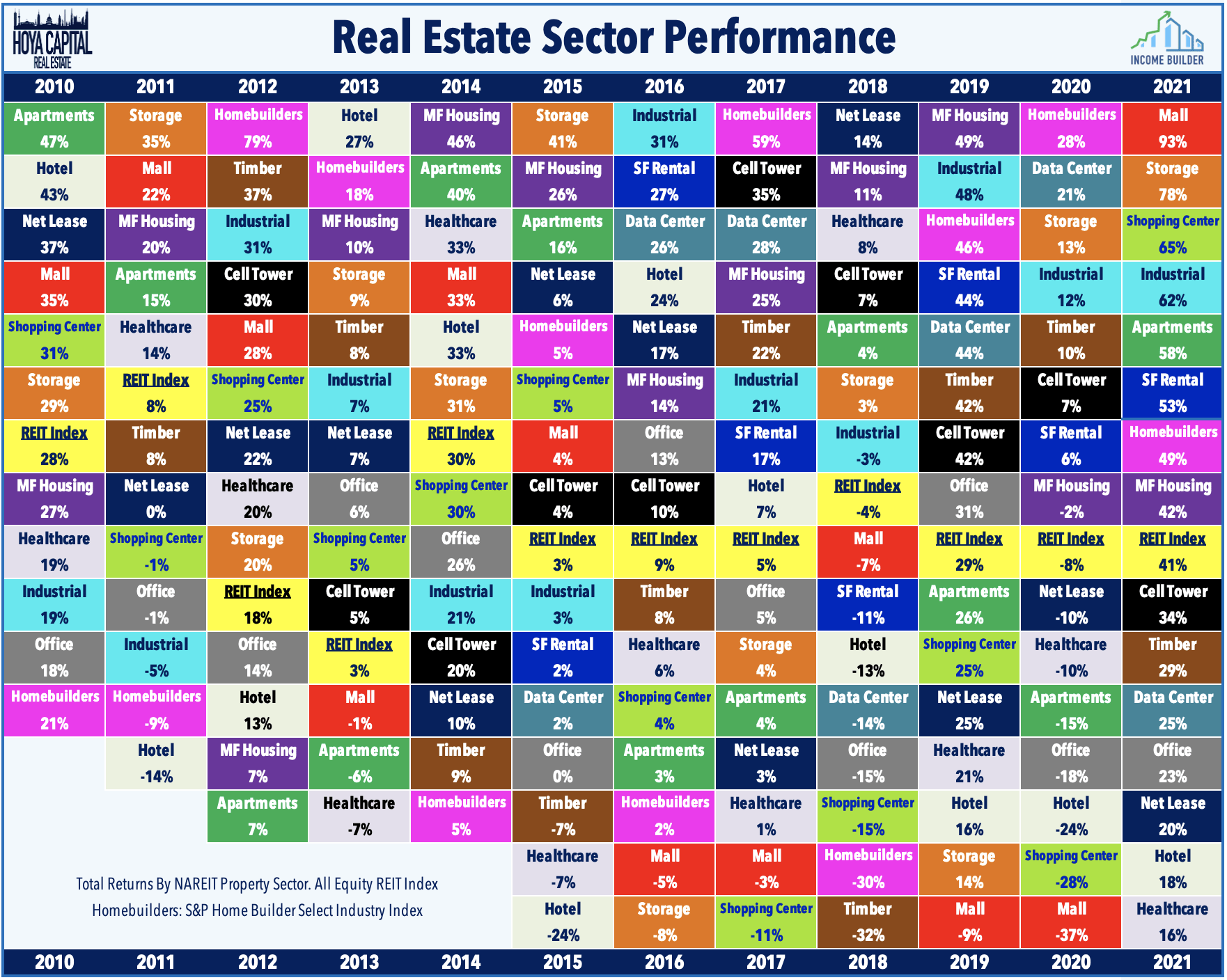

Despite the historic surge in interest rates over the past quarter driven by expectations of Fed tightening, REITs enter first-quarter earnings season with some momentum at their backs. Having lagged for most of this year, the broad-based Vanguard Real Estate ETF (VNQ) jumped ahead of the S&P 500 on a year-to-date performance in early April. Through fifteen weeks of 2022, Equity REITs are now lower by 5.8% this year on a total return basis while Mortgage REITs have slipped 7.8%. This compares with the 7.5% decline on the S&P 500 and the 7.3% decline on the S&P Mid-Cap 400. At 2.83%, the 10-Year Treasury Yield has climbed 132 basis points since the start of the year on expectations of monetary tightening.

Hoya Capital

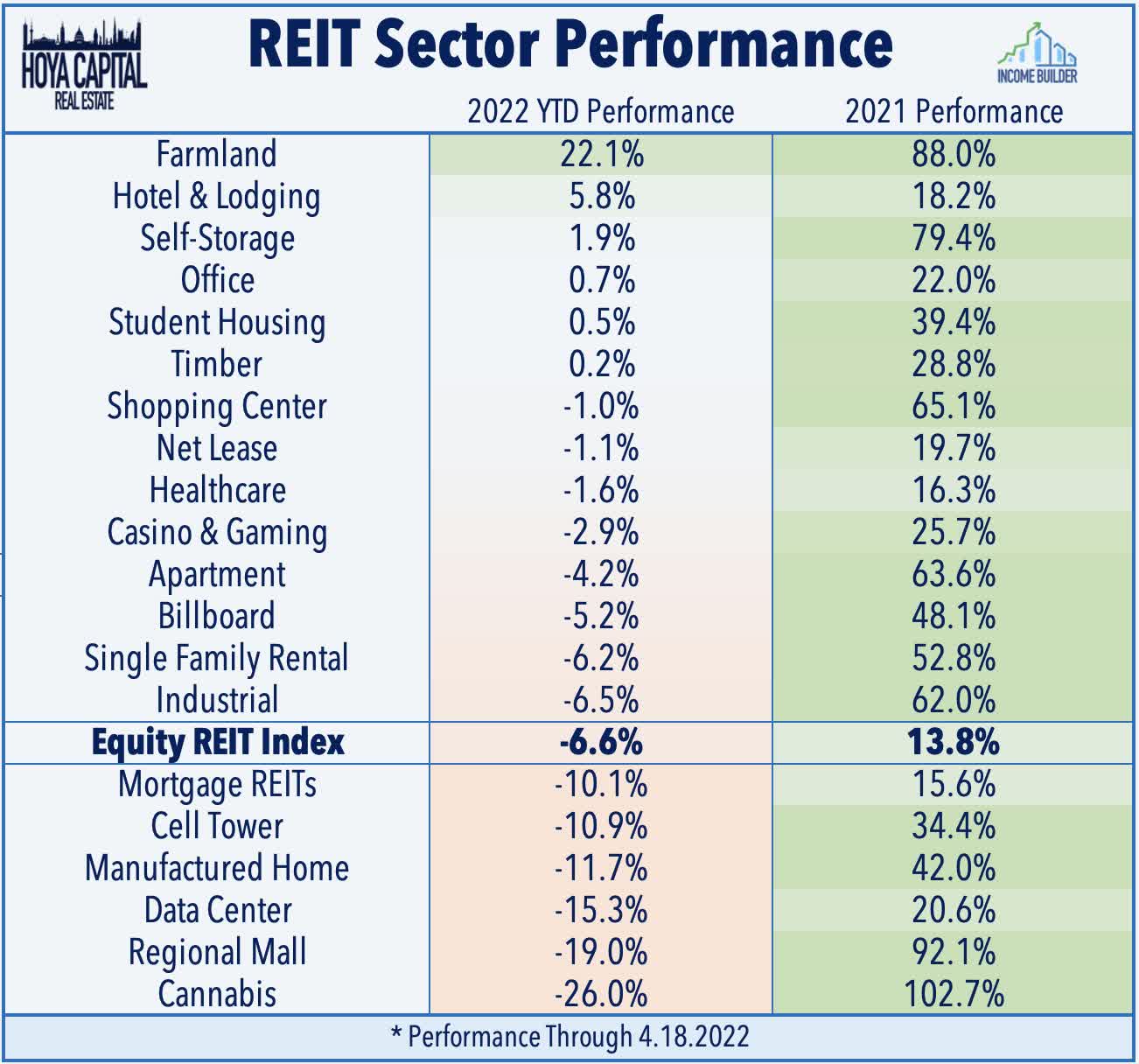

At the start of first-quarter earnings season, just six of the nineteen REIT sectors are in positive territory for the year, led on the upside by the farmland, hotel, self-storage, office, and student housing REIT sectors. Large-cap technology REITs – which have increasingly dominated the market-cap-weighted equity REIT indexes – have uncharacteristically lagged over the past two quarters amid an intra-sector rotation from growth to value and the slump in cell tower and data center REIT sectors have skewed the broad-based returns lower by more than 2 full percentage points so far this year.

Hoya Capital

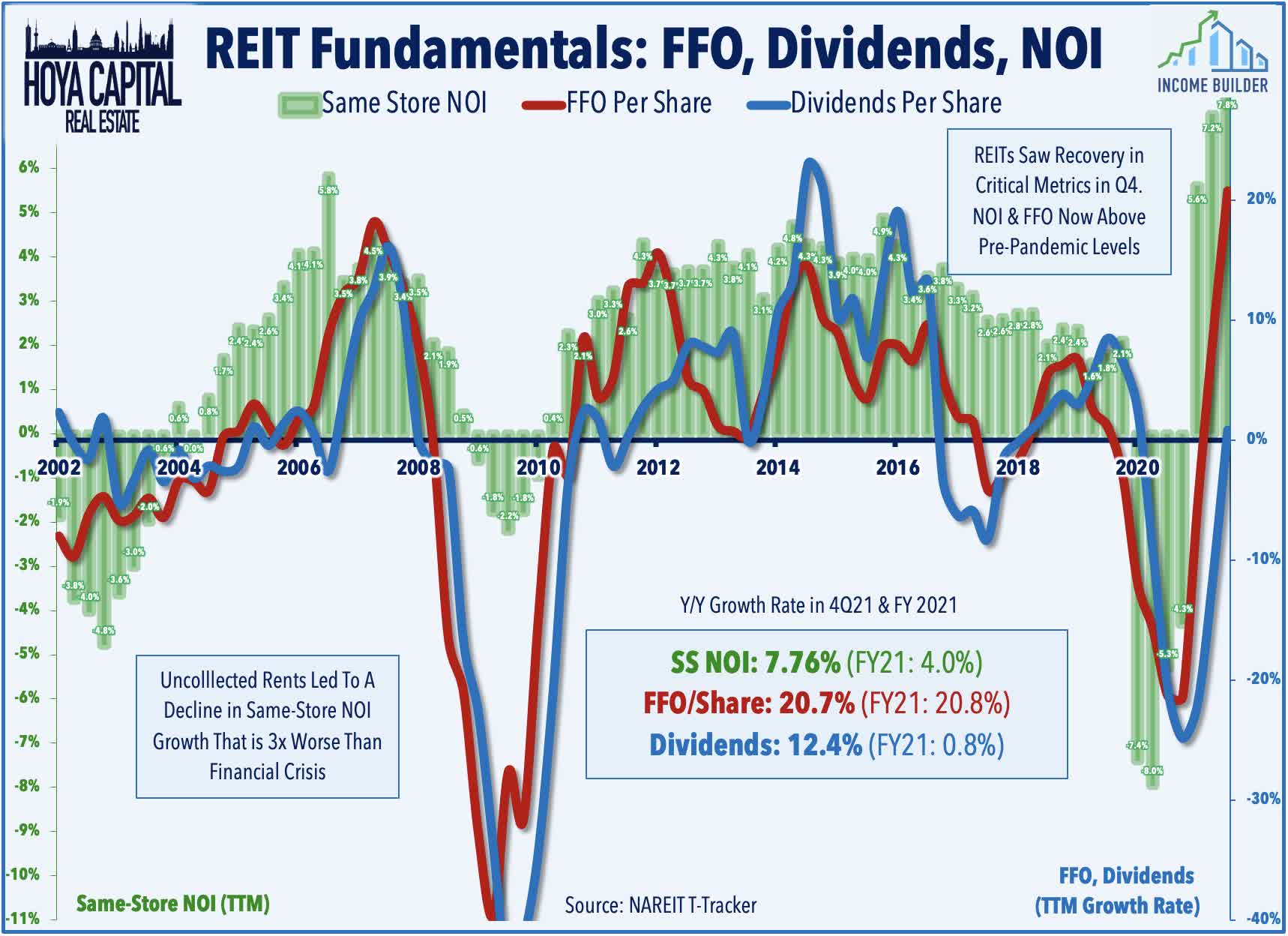

As discussed in our Real Estate Earnings Recap, the REIT sector is coming off a solid fourth-quarter earnings season in which roughly 90% of equity REITs beat consensus FFO estimates while more than 75% of the REITs that provide forward guidance beat their full-year outlook. Dividend hikes have been among the prevailing themes of early 2022 with over 60 REITs already raising their payouts so far in 2022, outpacing the record-setting pace seen last year. Critically, the initial outlook for 2022 was impressive across most property sectors, reflecting a high degree of confidence among REIT executives that the growth momentum will be sustained beyond the initial post-pandemic recovery and amid the rising rate environment. Below, we discuss the major themes we’re focused on this earnings season.

Hoya Capital

Tech and Industrial REITs Earnings Preview

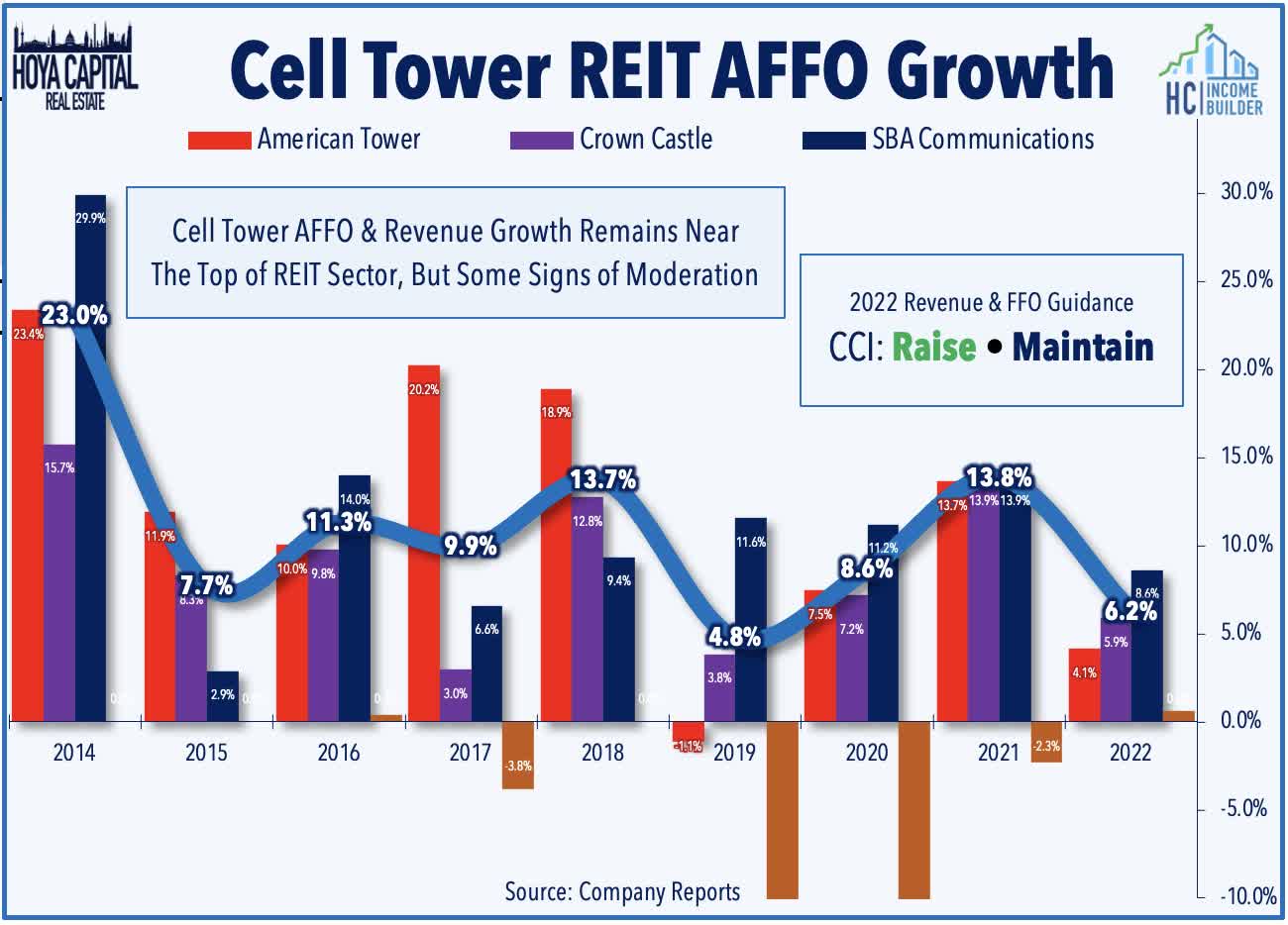

Cell Towers: Cell Tower REITs – a perennial performance leader in the real estate sector – have uncharacteristically lagged this year, briefly dipping into “bear market” territory for just the second time in history. Several factors are behind the recent slump including potential competition from Low-Earth-Orbit satellite networks, delays in 5G deployment related to airline interference, and broader tech-related weakness. We’re focused on updated AFFO guidance and the outlook for U.S. organic growth, and any commentary around the pace of 5G deployment. Crown Castle (CCI) kicked off tech REIT earnings on Wednesday with in-line results with no major changes to its outlook – modestly raising its full-year revenue growth outlook but maintaining its FFO guidance.

Hoya Capital

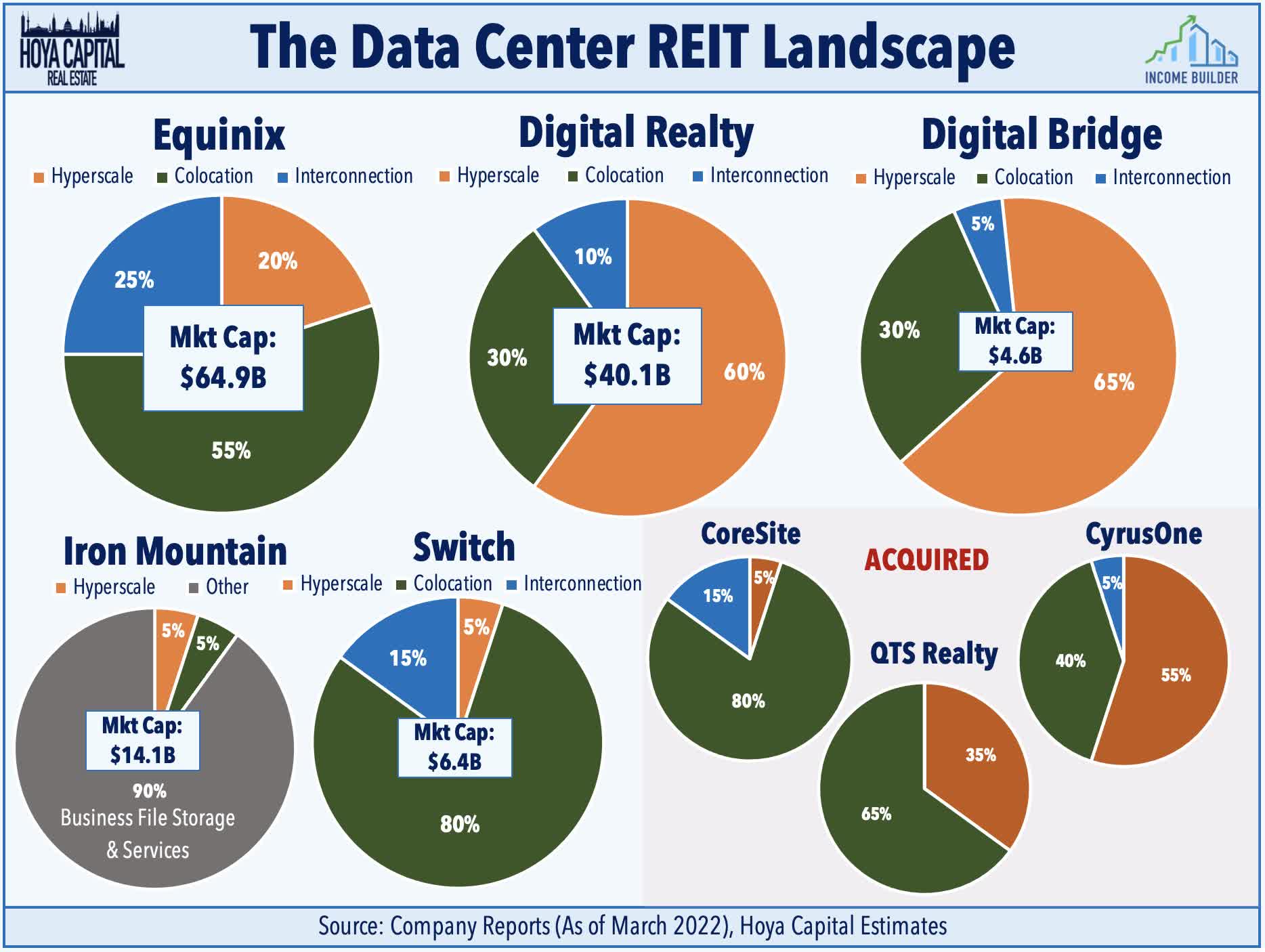

Data Center: Data Center REITs- a perennial performance leader in the REIT sector also dipped into “bear market” territory earlier this year for the just third-time in the past ten years. Data center demand and fundamentals remain resilient and were remarkably unaffected by the pandemic and subsequent reopenings, but that’s precisely the issue as investors have rotated into more pro-cyclical sectors. The complexion of the sector changed dramatically after two REITs were taken private while COR was acquired by AMT, but DigitalBridge (DBRG) and Iron Mountain (IRM) have matured into serious players. We’re watching leasing and pricing metrics and for commentary regarding M&A amid rumors of takeover interest in both Switch (SWCH) and Cyxtera (CYXT) as we have yet to see any major deals over the past year from either Digital Realty (DLR) and Equinix (EQIX).

Hoya Capital

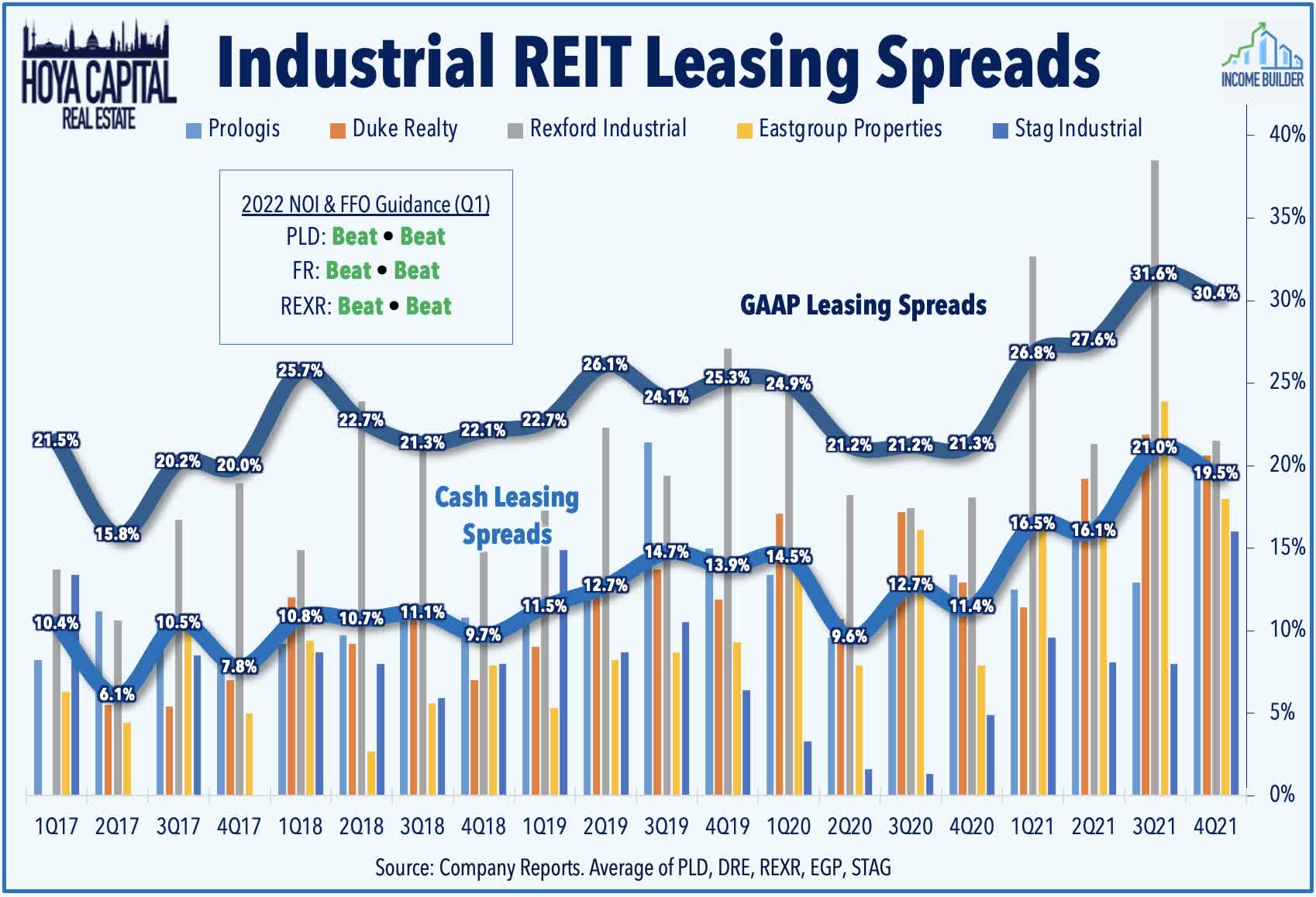

Industrial: On the front lines of the historic supply-chain shortages, Industrial REITs outperformed the broad-based REIT Index for the sixth consecutive year in 2021, but had been uncharacteristically lagging in early 2022 before a trio of strong results this week from Prologis (PLD), Rexford (REXR), and First Industrial (FR), all of which raised their full-year FFO and NOI growth outlooks on incredible rent growth. Rexford recorded releasing spreads of 71% and 57%, on a GAAP and cash basis, respectively, and yet was still able to end the quarter with record-high occupancy at 99.3%. PLD recorded rent spreads on renewed leases were +37% (+42% in the U.S.) with several markets seeing 65%+ rent increases. PLD noted that its average rents on existing leases are 47% below market, equating to $2 per share of embedded earnings growth as these leases renew at current market rates.

Hoya Capital

Residential REITs Earnings Preview

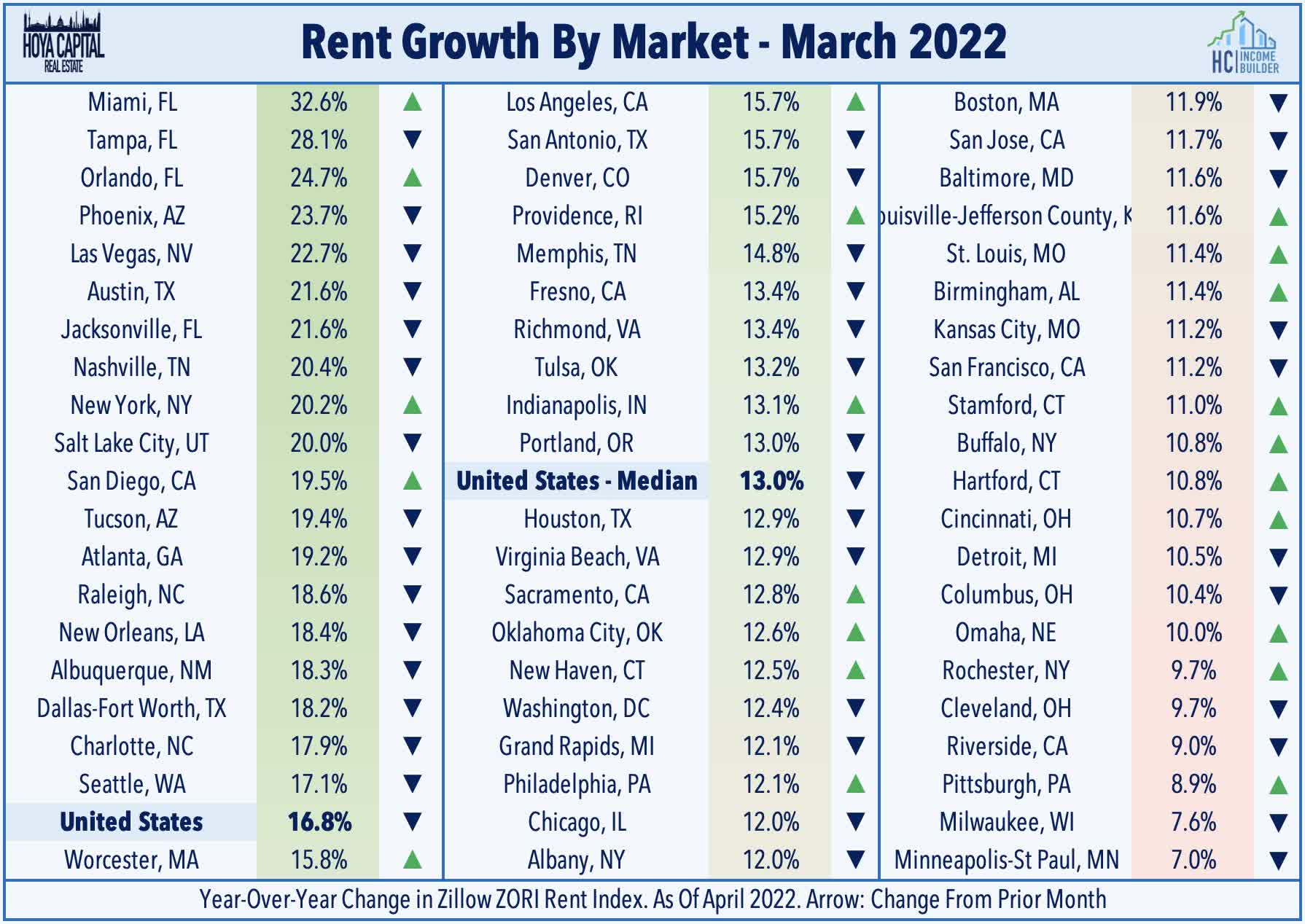

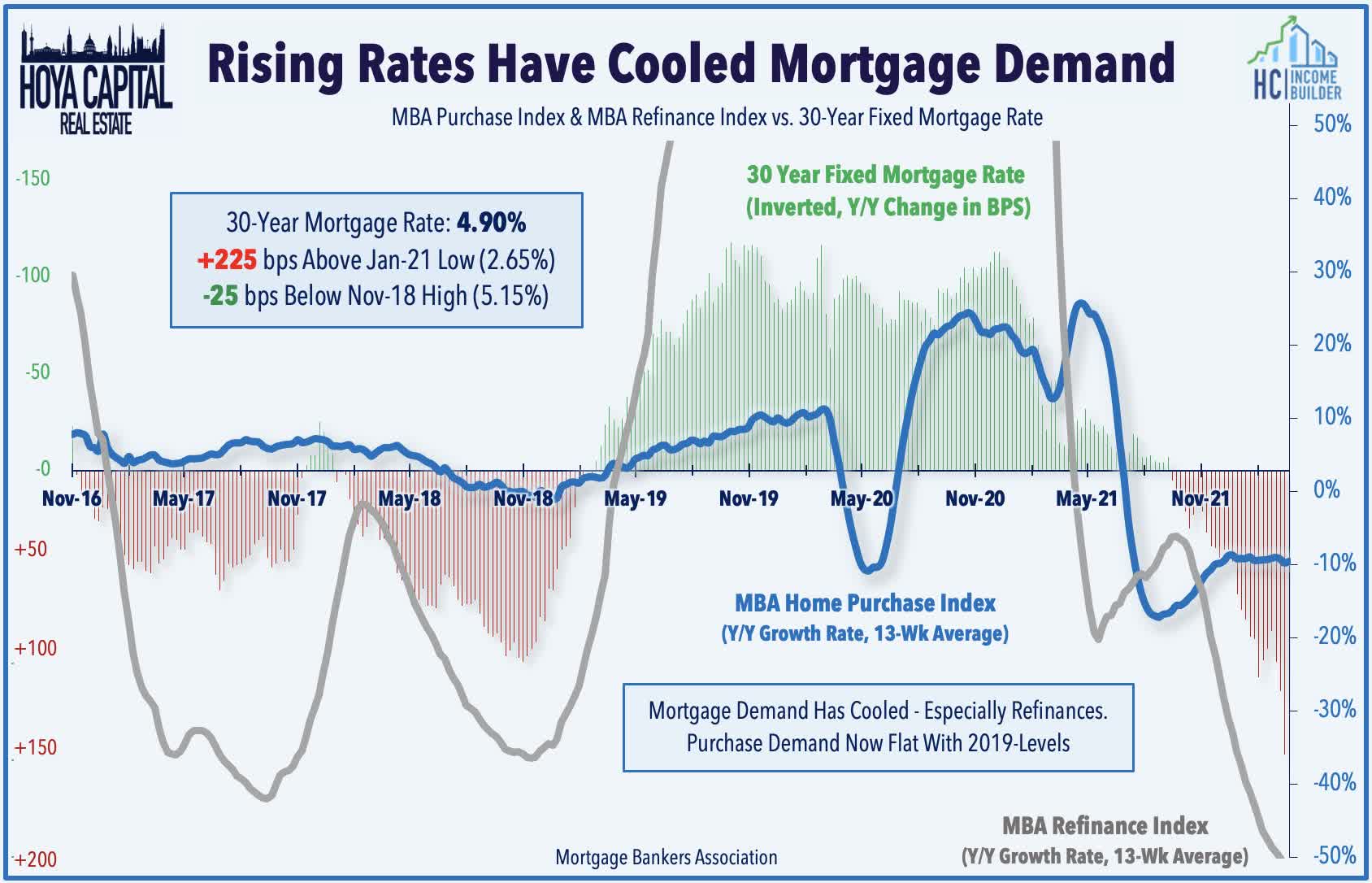

Apartments: Rents are soaring at the fastest pace on record in essentially every major market across the country. After rising nearly 20% in 2021, renters should prepare for double-digit growth again in 2022. Riding the rental boom, Apartment REITs reported stellar earnings results last quarter, ending 2021 with record-high occupancy rates with the momentum accelerating in 2022 with 15% earnings growth this year. Apartment REITs have exhibited restraint in rental rate increases on existing tenants – sometimes rent-control-related – as the gap between new lease rates and renewals continues to imply substantial embedded NOI growth ahead. We’ll again be watching leasing results and listening for commentary on how the surge in mortgage rates is expected to impact demand.

Hoya Capital

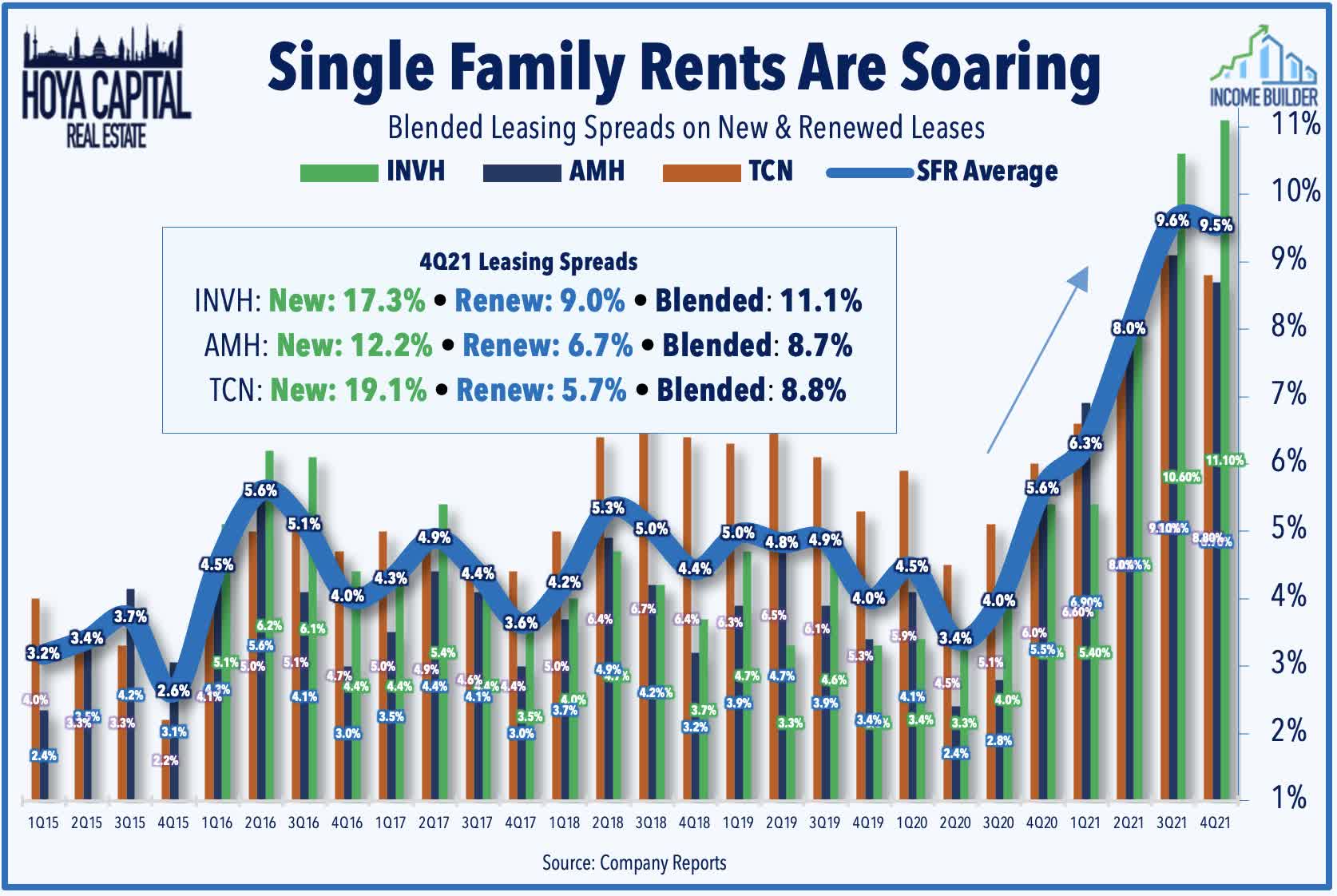

Single-Family Rentals: Single-Family Rental REITs have been one of the best performing property sectors since their emergence onto the scene in the mid-2010s, outperforming the REIT Index for three straight years entering 2022. Despite the double-digit surge in rental rates over the past year, rising mortgage rates have tilted the affordability scale further towards renting – particularly in the suburbs. Powered by the historic surge in rents, SFR REITs reported earnings growth of nearly 20% last year and have delivered dividend growth of over 30% per year since 2019. We’re focused on leasing spreads and how rising mortgage rates may affect the acquisition environment given our view that rising rates will likely accelerate the expansion of institutional ownership across the single-family space and the maturation of “built-for-rent” single-family development.

Hoya Capital

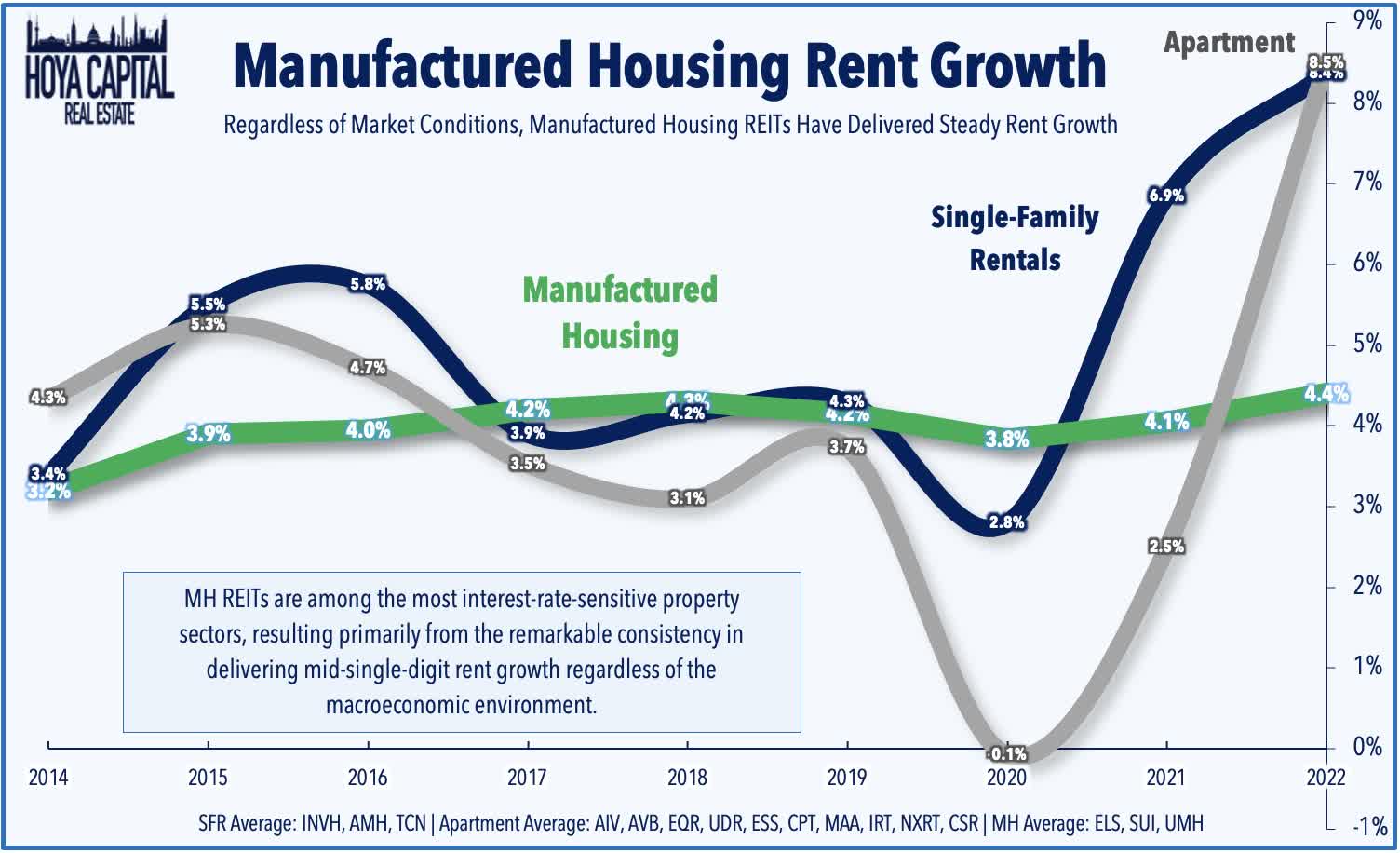

Manufactured Housing: Manufactured Housing REITs have emerged over the past decade from relative obscurity into several of the most well-run publicly-traded property owners in the world, but have uncharacteristically stumbled in early-2022. MH REITs are among the most interest-rate-sensitive property sectors, resulting primarily from the remarkable consistency in delivering mid-single-digit rent growth regardless of the macroeconomic environment. Equity LifeStyle (ELS) kicked off the earnings season on Monday afternoon with a strong report, raising its guidance across all of its metrics – a strong read-through for Sun Communities (SUI). ELS now sees FFO growth of 7.9% – up considerably from its initial guidance last quarter of 6.3%. It also sees NOI growth of 6.8% – up 90 bps from its prior guidance of 5.9%, powered again by strong performance in its RV and marina segment.

Hoya Capital

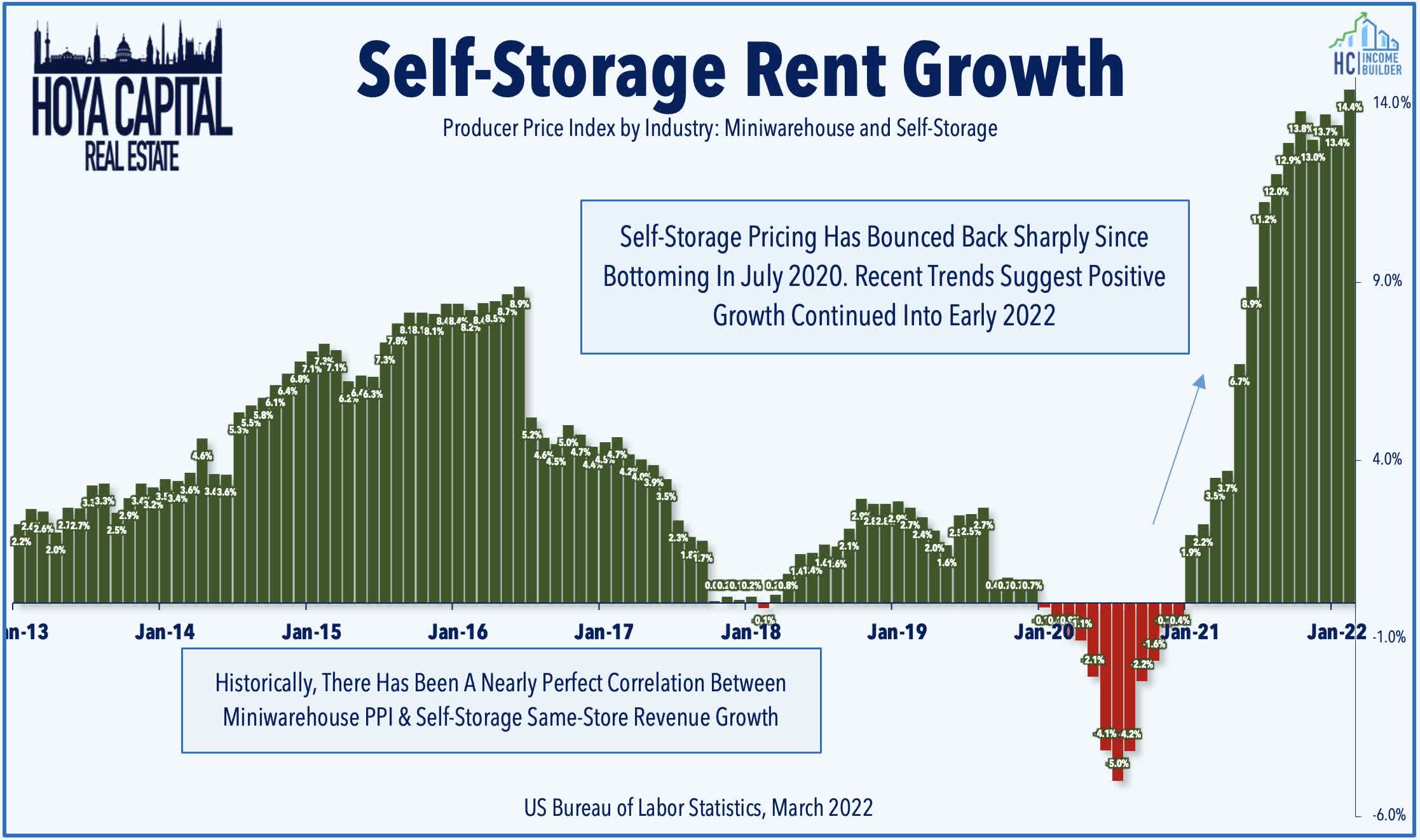

Self-Storage: Self-storage REITs – which delivered the most impressive rebound of any property sector throughout the pandemic – have built on their gains in early 2022 following a jaw-dropping 80% surge last year. Stumbling into the coronavirus pandemic with challenged fundamentals and an outlook for near-zero growth amid oversupply challenges, self-storage demand soared over the past year, powering record occupancy increases, and rent hikes. Storage demand is closely-correlated with housing market turnover: specifically home sales and rental turnover. The surge in mortgage rates this year appears likely to slow turnover and temper storage demand. That said, storage REITs have been persistently under-estimated over the past two years, so we’re interested to see if the streak of “beat and raises” can continue and whether a potential moderation in occupancy can be offset by rent growth.

Hoya Capital

Healthcare & Office REITs Earnings Preview

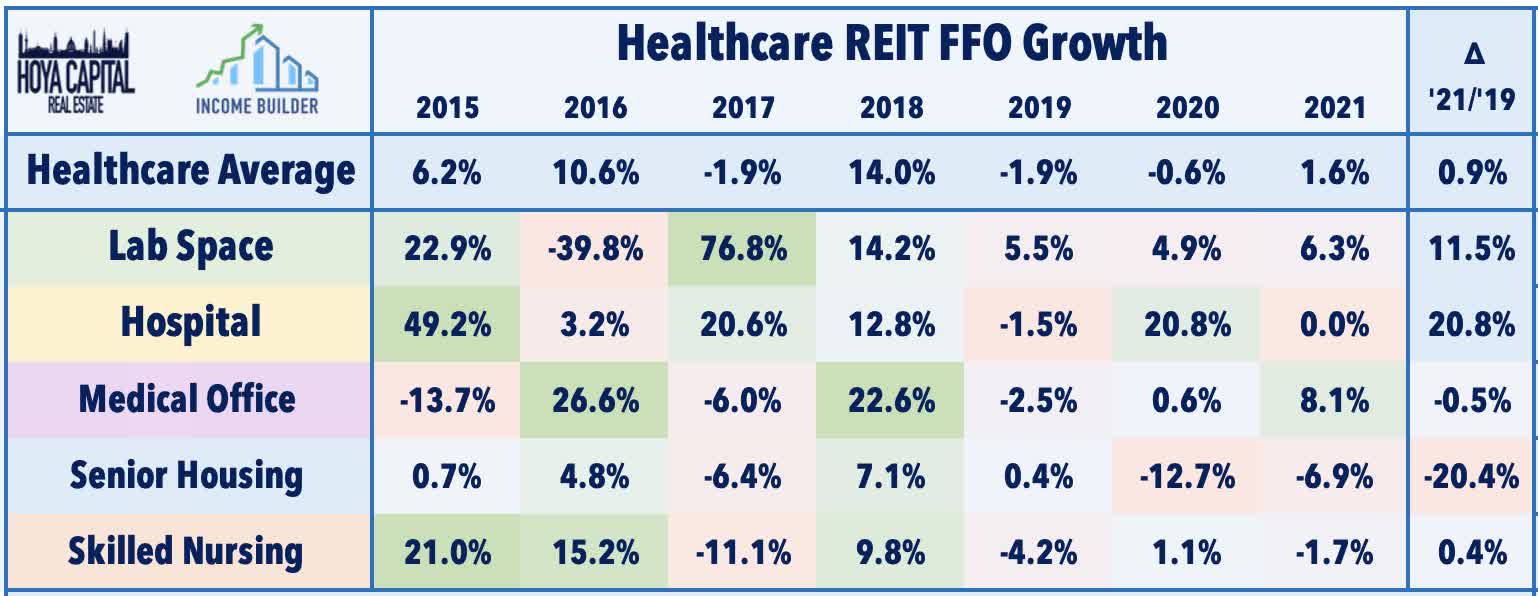

Healthcare: Healthcare REITs- which were the weakest-performing property sector in 2021- have been one of the better-performing REIT sectors in early 2022, lifted by an improving fundamental outlook for senior housing. Interim updates from Welltower (WELL) and Ventas (VTR) showed that while the path back to “normal” was slowed by Omicron, the recovery still had positive momentum deep into Q1. With nursing staff shortages likely to persist, and with a dimming outlook for significant further COVID relief funds, caution is warranted for Skilled Nursing and “public-pay” healthcare REITs and we’ll be watching for signs of further operator stress from the SNF REITs, but we expect another solid quarter from lab space and medical office sub-sectors.

Hoya Capital

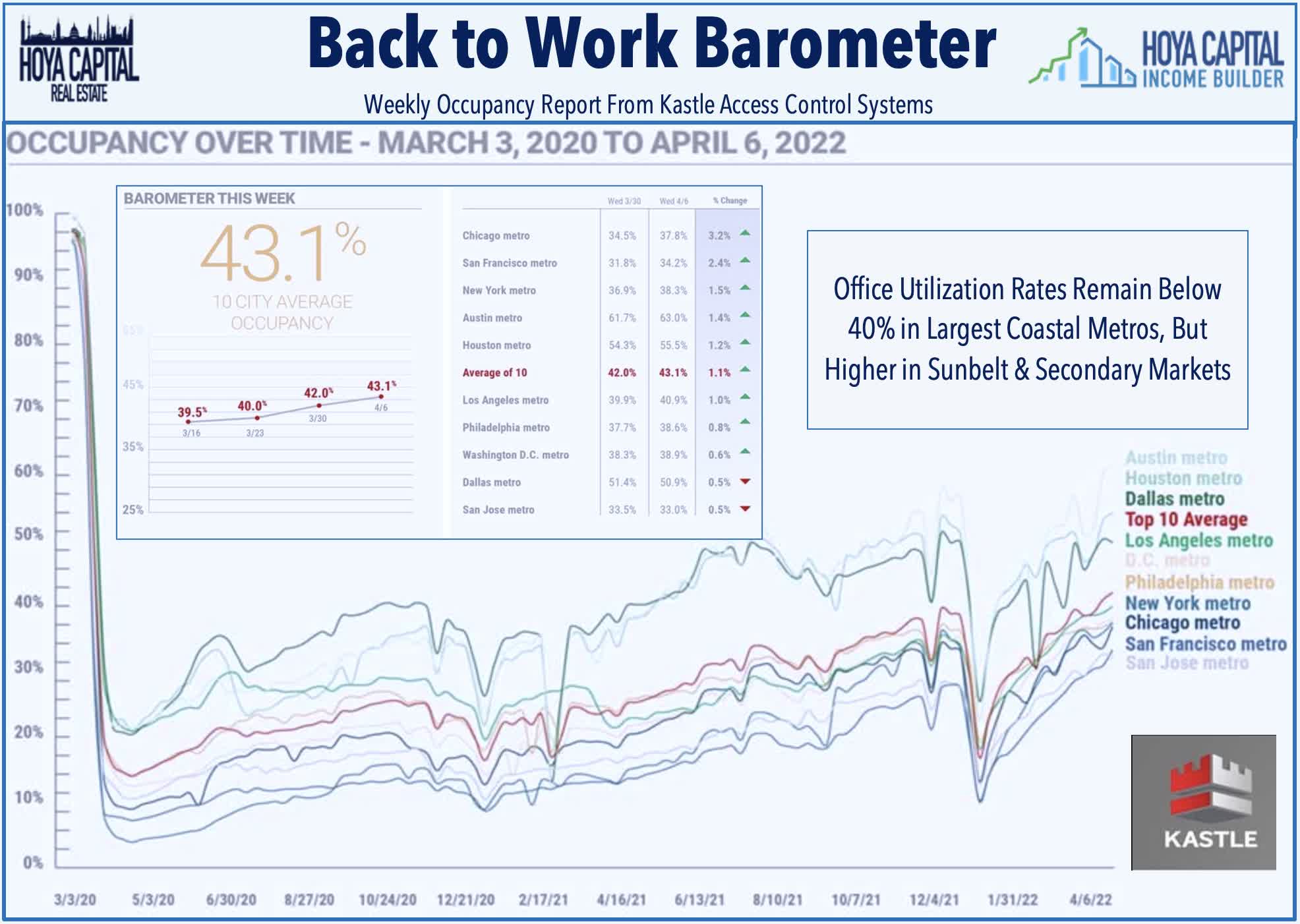

Office: Office REITs – which lagged over the prior two years from persistent pandemic-related headwinds – have also been among the better-performing major property sector in early 2022. Two years into the pandemic, office utilization rates finally appear to be picking up in a critical window in which many corporations are transitioning to “hybrid” work environments. Office leasing demand – and earnings results from these office REITs – have been surprisingly resilient, however, particularly for REITs focused on business-friendly Sunbelt regions and specialty lab space. We’re focused on leasing trends and updated expectations of when “normalization” will occur – and what exactly “normalization” looks like. We see significant mispricing between the handful of Sunbelt-focused office REITs and the Coastal-focused REITs.

Hoya Capital

Retail Real Estate Earnings Preview

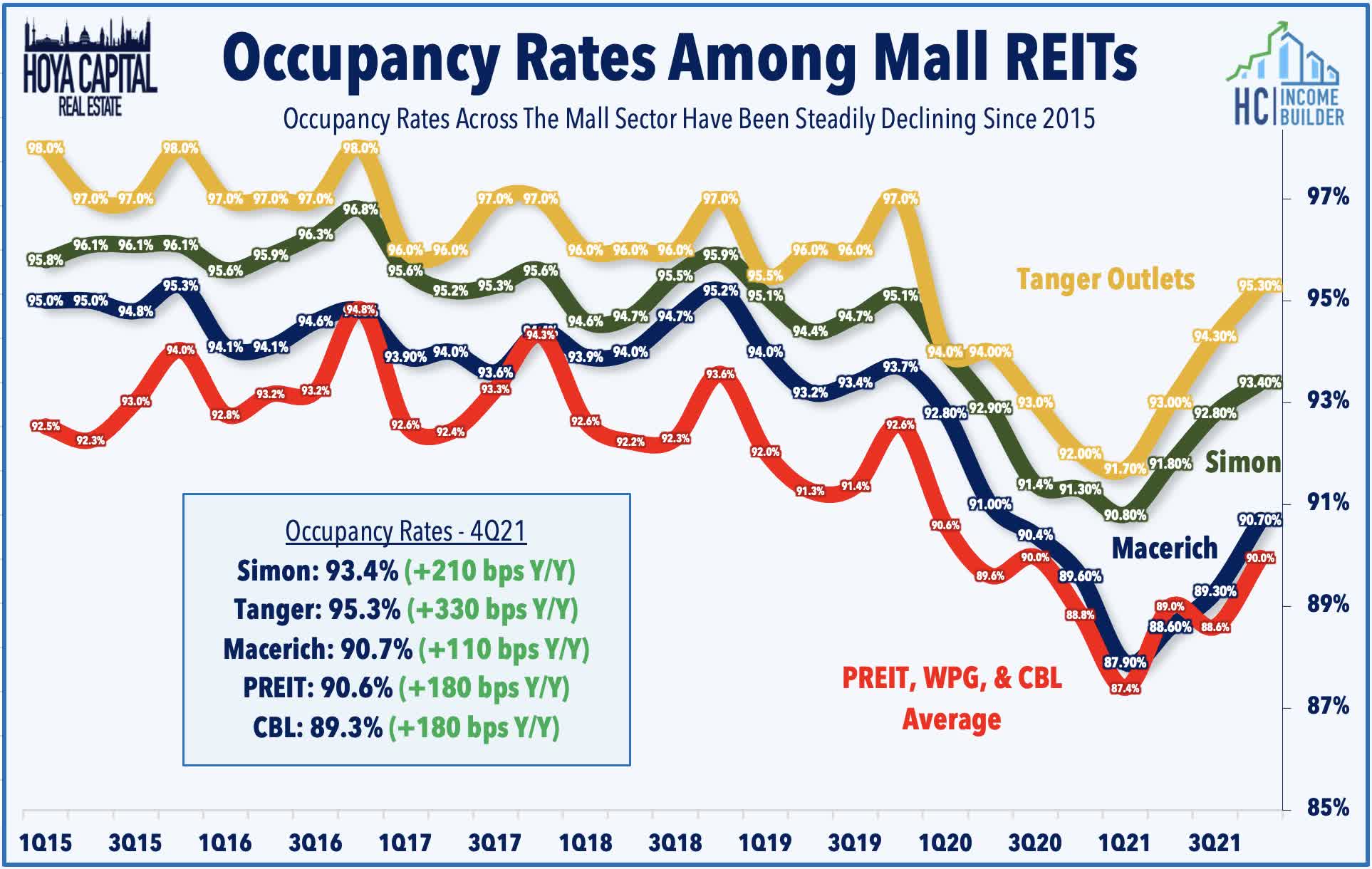

Malls: Mall REITs were the best-performing major REIT sector in 2021 – nearly doubling in value amid hopeful signs of stabilizing fundamentals – but are back at the bottom of the REIT sector in the performance tables this year as rising gas prices has led to a cooldown in retail spending. Traffic and sales levels at higher-end mall properties were back to pre-pandemic levels during the holiday season while store openings outpaced closings for the first time since 2014. We’re focused on leasing spread this earnings season – which remained weak last quarter despite improving NOI and FFO trends – and want to see rental rates stabilize before we can officially call the bottom.

Hoya Capital

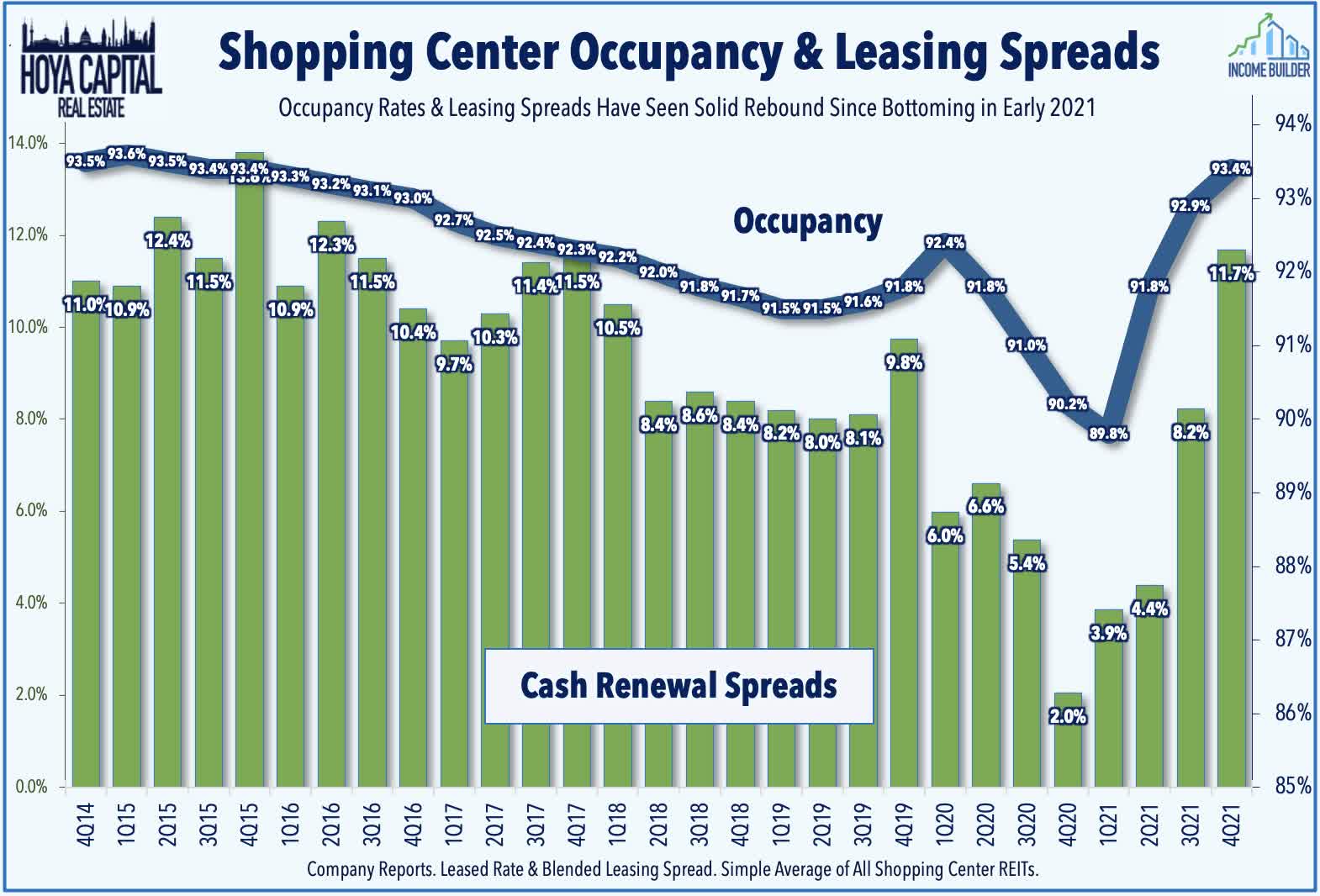

Shopping Centers: Unlike their mall REIT peers, Shopping Center REITs entered 2022 with fundamentals that are as strong – or possibly even stronger- than before the pandemic with a full recovery now complete. Occupancy rate trends and leasing spreads have been especially impressive with rents rising by double-digit rates last quarter, indicating clear signs of pricing power for the first time since the mid-2010s. Like their mall REIT peers, however, worries over slowing consumer spending have tempered the upside. We’ll be focused again on leasing spreads and occupancy rates which – unlike mall REITs – appeared to definitively bottom in early 2021.

Hoya Capital

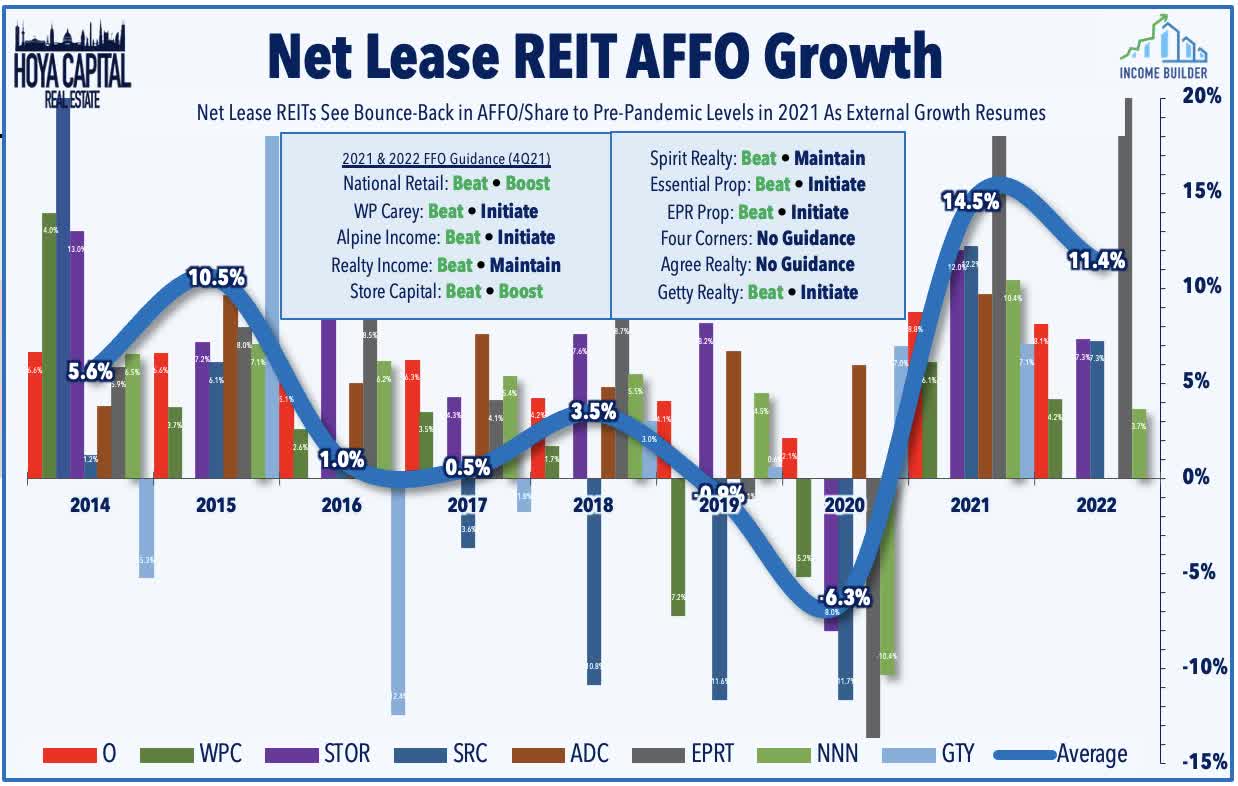

Net Lease: Net Lease REITs – understood to be one of the more “bond-like” and rate-sensitive REIT sectors – have actually held up rather well in 2022, consistent with our analysis earlier this year that net lease REITs actually outperformed the REIT sector during the prior Fed rate hike cycle from 2015-2019 after significantly underperforming in the 18-months prior – a similar backdrop to the current dynamic. Critically, the “rates” that matter for REITs are long-term rates, not the Fed Funds rate, and the tightening cycle is beginning with the 10-Year Yield already closer to its post-GFC peak than its lows. We’re interested in commentary regarding the inflation protection of existing and new leases and how the interest rate and inflation environment may impact acquisition activity in 2022.

Hoya Capital

Hotel & Casino REITs Earnings Preview

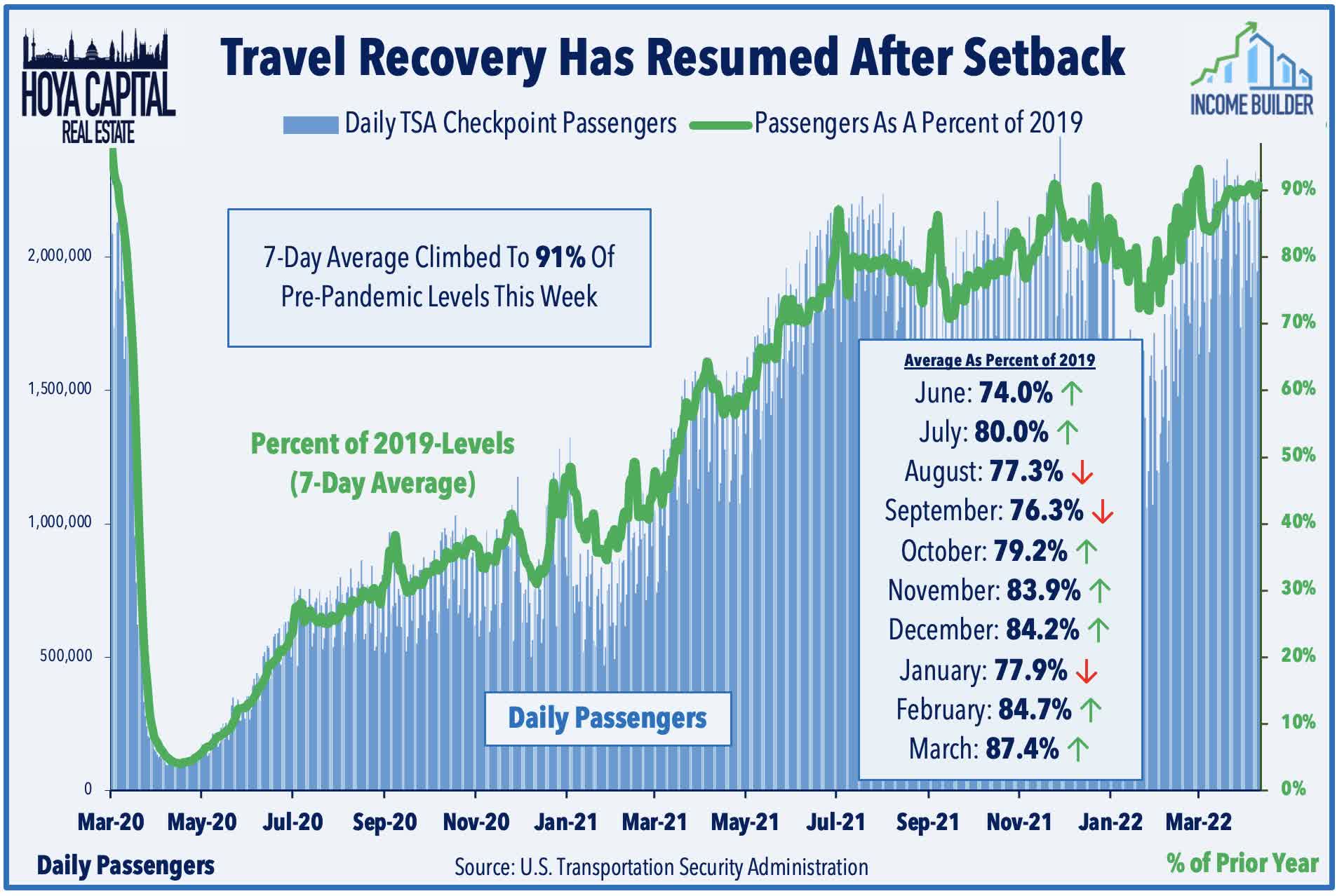

Hotels: Hotel REITs – the top-performing major property sector this year – entered 2022 with positive fundamental momentum and reasons for cautious optimism following four-straight years of underperformance. Masks are off and Spring Break is back – for many – but Sunbelt and leisure-focused markets continue to substantially outperform Coastal business-focused markets. Leisure travel is above pre-pandemic levels, but business demand remains depressed. Recent high-frequency data has been encouraging, contrasting with the gloomy attitude in confidence surveys. TSA Checkpoint data rebounded to 90% of pre-pandemic levels last week while average national hotel occupancy is back at its 20-year average. We’re interested in updated expectations from hotel REITs and whether these REITs expect to see the surge in deferred travel that was expected last summer.

Hoya Capital

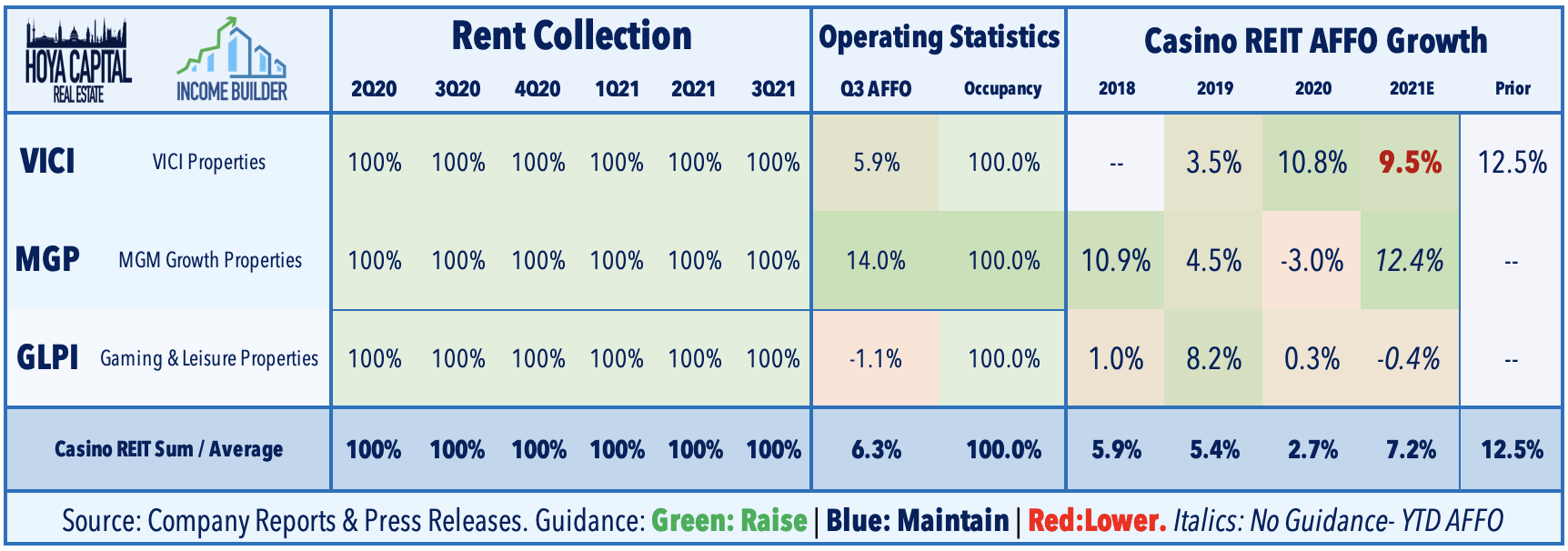

Casinos: Las Vegas is one of the hotel markets that continue to see relatively strong demand as resilient leisure demand has offset the continued slump in group and convention demand. Despite their ultra-long term triple net lease structures, casino REITs provide excellent inflation hedging characteristics. VICI Properties, in particular, has one of the most inflation-hedged lease structures of any REIT. VICI Properties (VICI) will complete its acquisition of MGM Growth (MGP) in early 2022, which will give the firm a dominant competitive position in the critical Las Vegas market. We’re interested to hear discussions over Realty Income’s (O) move into the casino real estate business with its acquisition of Encore Boston Harbor from Wynn Resorts for $1.70B. On that topic, we’re focused on commentary about future growth opportunities – and whether these REITs are looking internationally or at other related property sectors.

Hoya Capital

Homebuilders & Timber Earnings Preview

Homebuilders: What have you done for me lately? Despite being steady-handed leaders throughout the pandemic, homebuilders are again a deeply unloved sector, trading at deep discounts to historical and market multiples – including mid-single-digit P/E ratios – despite double-digit earnings growth expected over the next several years. Rising mortgage rates are sure to slow demand at the margins and cool home price appreciation, but do little to alter the long-term secular tailwinds related to a decade of underbuilding across suburban markets and the market share gains accruing to public builders that have the critical scale to compete in the low-margin building business. With P/E valuations in single digits, homebuilders have a relatively low hurdle to beat, so stronger-than-expected results could spark a significant rebound.

Hoya Capital

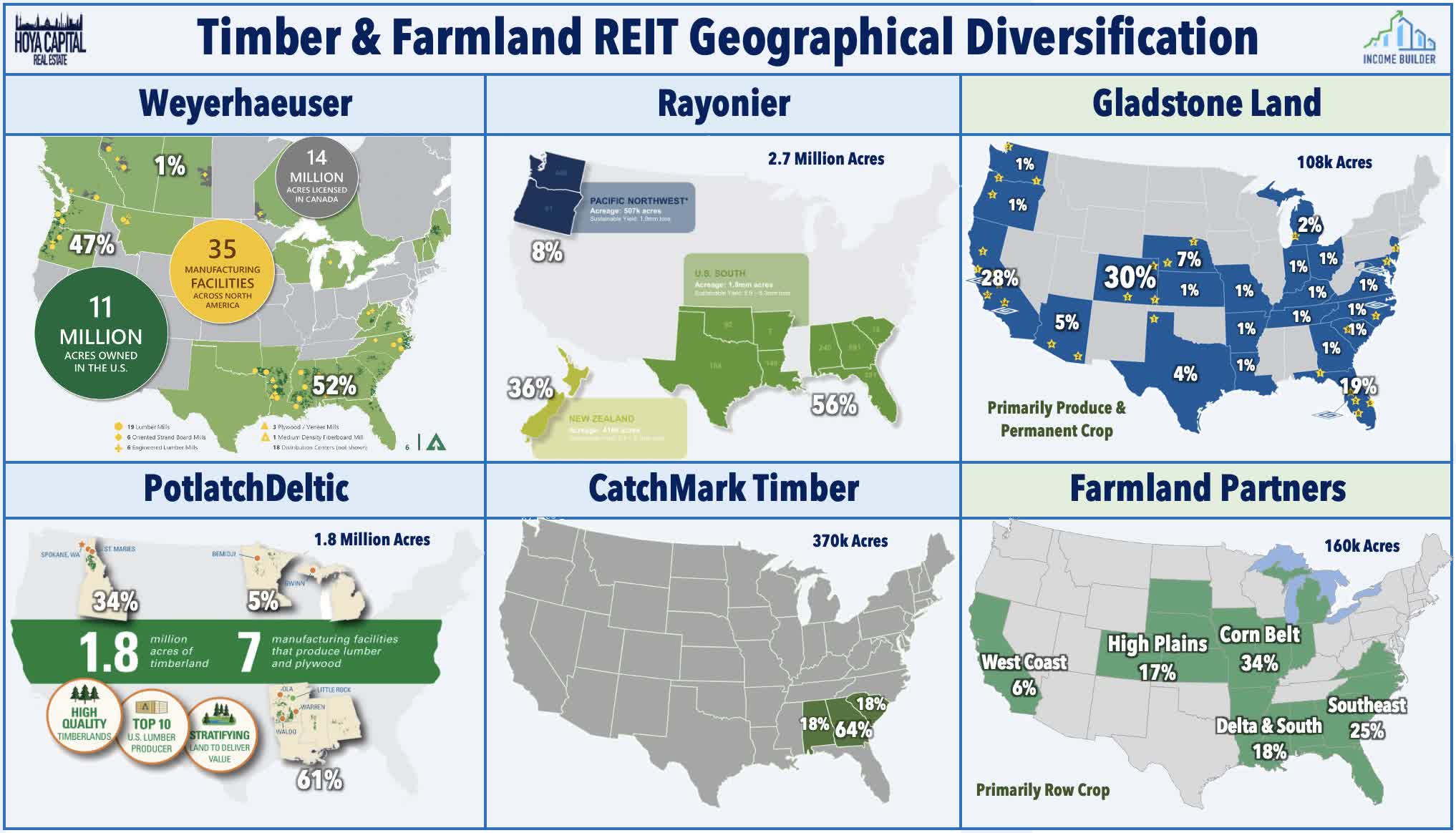

Timber & Farmland: Publicly-traded landowners – specifically timber and farmland REITs – have been among the best-performing real estate sectors this year amid concerns over persistent inflation and soaring commodities prices. Amid the ongoing conflict with Russia – which is among the world’s largest exporters of agriculture, gasoline, and timber products – the importance and value of North American production has become evident. Buying land has been a “hot trade” over the past year, and valuations appear rich for farmland REITs with implied cap rates in the 2-3% range, but valuations of higher-quality timber REITs remain quite attractive. We’re also in the final development stages of a new custom “Landowner Portfolio” strategy on Hoya Capital Income Builder, which will launch later this week.

Hoya Capital

Specialty REIT Sectors Earnings Preview

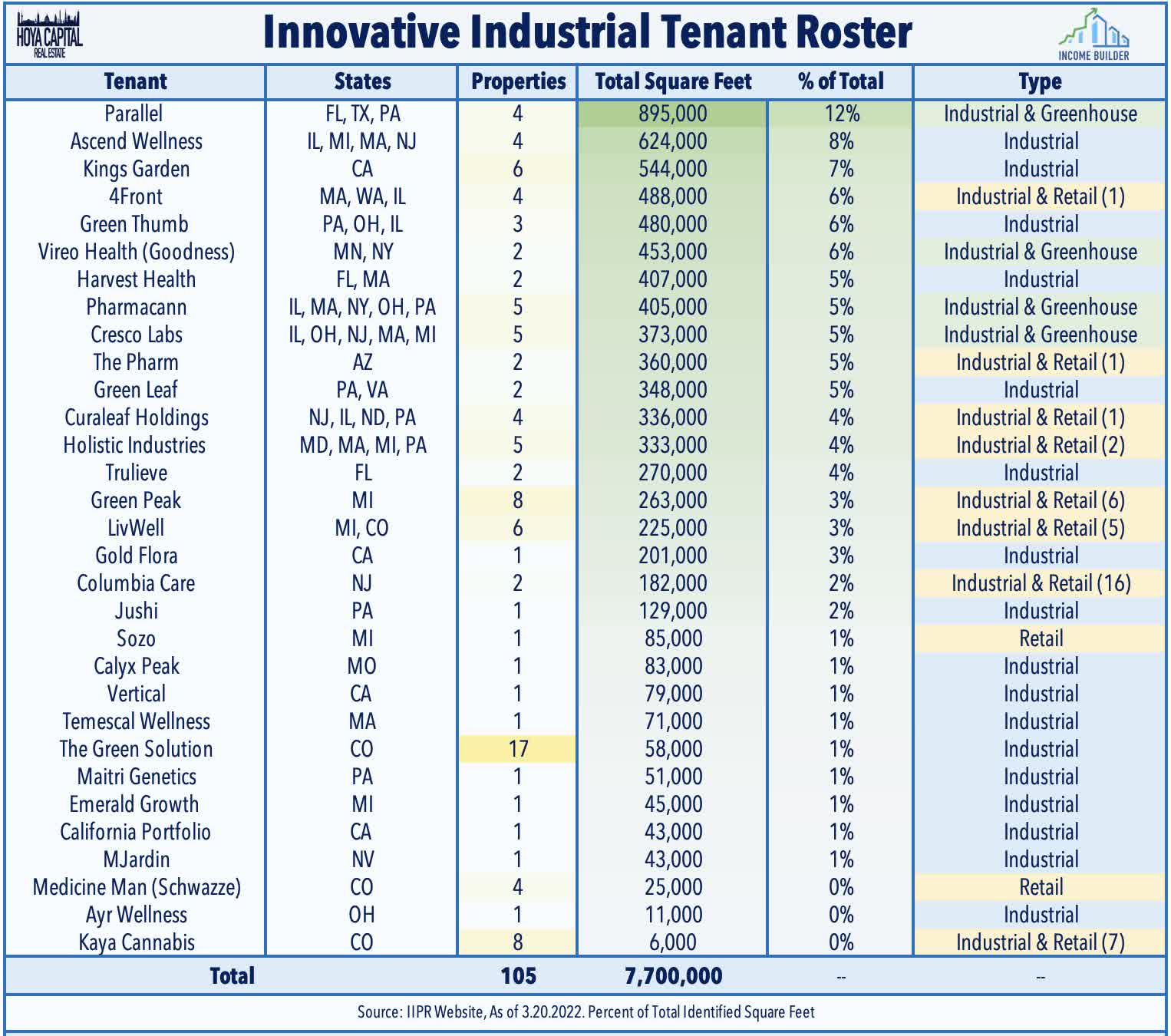

Cannabis: Cannabis REITs – the best-performing property sector over the past half-decade – have stumbled in early 2022, pressured by the broader growth-to-value rotation and uncertainty over progress on federal legalization. Innovative Industrial (IIPR) dipped 10% last week following a report published by Blue Orca Capital, a “short activism” firm that has historically focused its activism on Asia-based technology companies. Blue Orca critiqued the sale-leaseback model through which IIPR provides financing to operators to build out the facility into a cultivation facility – and focused the balance of its thesis on the credit quality of IIPR’s tenants – a valid concern that we’ve highlighted but certainly nothing groundbreaking. IIPR responded to the short report with a press release noting that the report contained “numerous false and misleading” statements about IIPR. We’re interested in hearing an extended commentary on these concerns from IIPR.

Hoya Capital

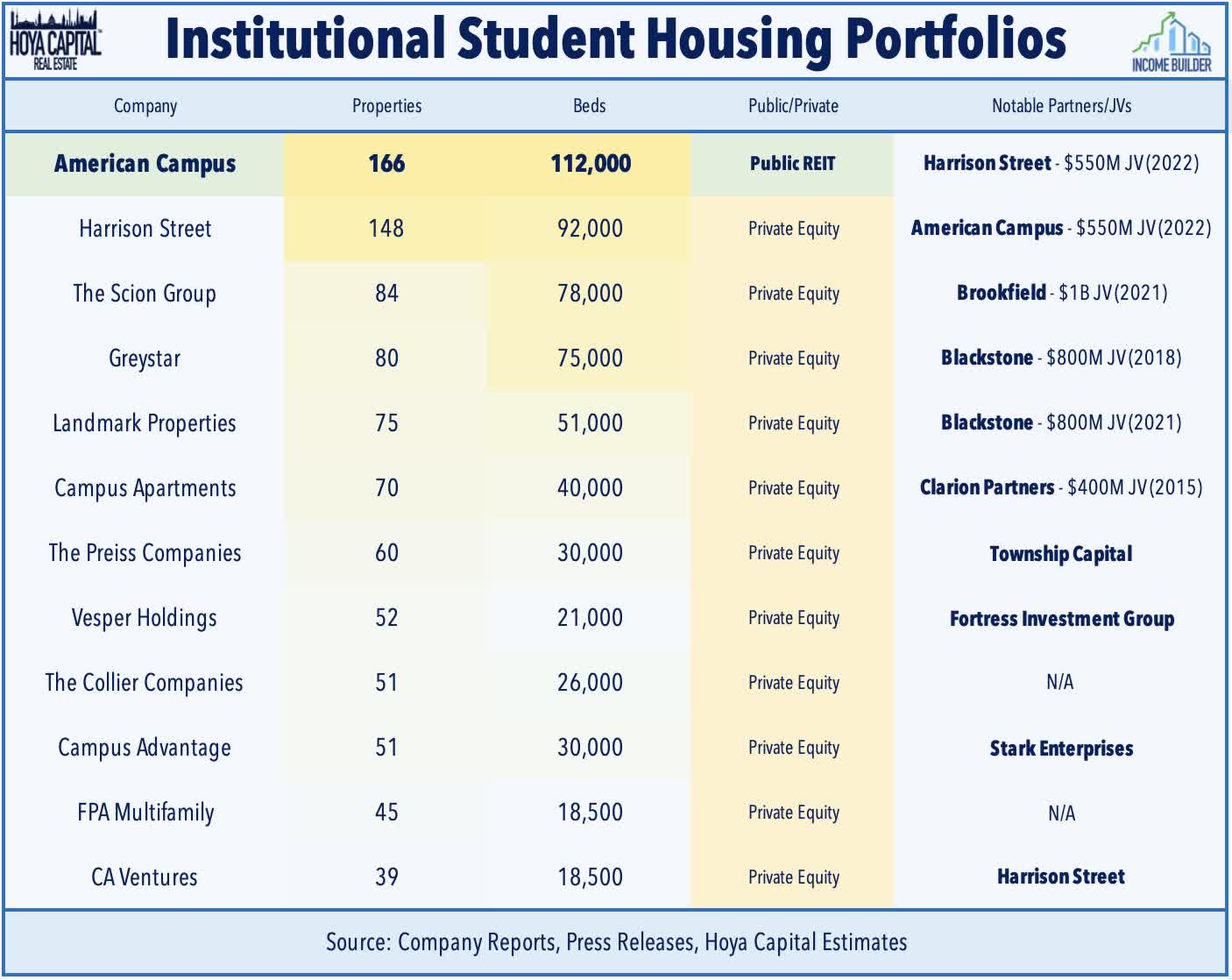

Student Housing: American Campus (ACC) – which we own in the REIT Focused Income Portfolio – surged more than 12% on Tuesday after agreeing to be acquired by Blackstone for $65.47/share, a 14% premium to Monday’s close. As a condition of the transaction, ACC agreed to suspend the payment of its quarterly dividend, effective immediately. The deal is expected to close in Q3. In our report published to Income Builder earlier this year, we commented: “Given the abundant amount of private institutional capital targeting student housing assets and the history of acquisitions of student housing REITs (Greystar’s 2018 acquisition of EDR and Harrison Street’s 2015 acquisition of Campus Crest) we place the likelihood of ACC being acquired at ~30% with a projected price around $65.”

Hoya Capital

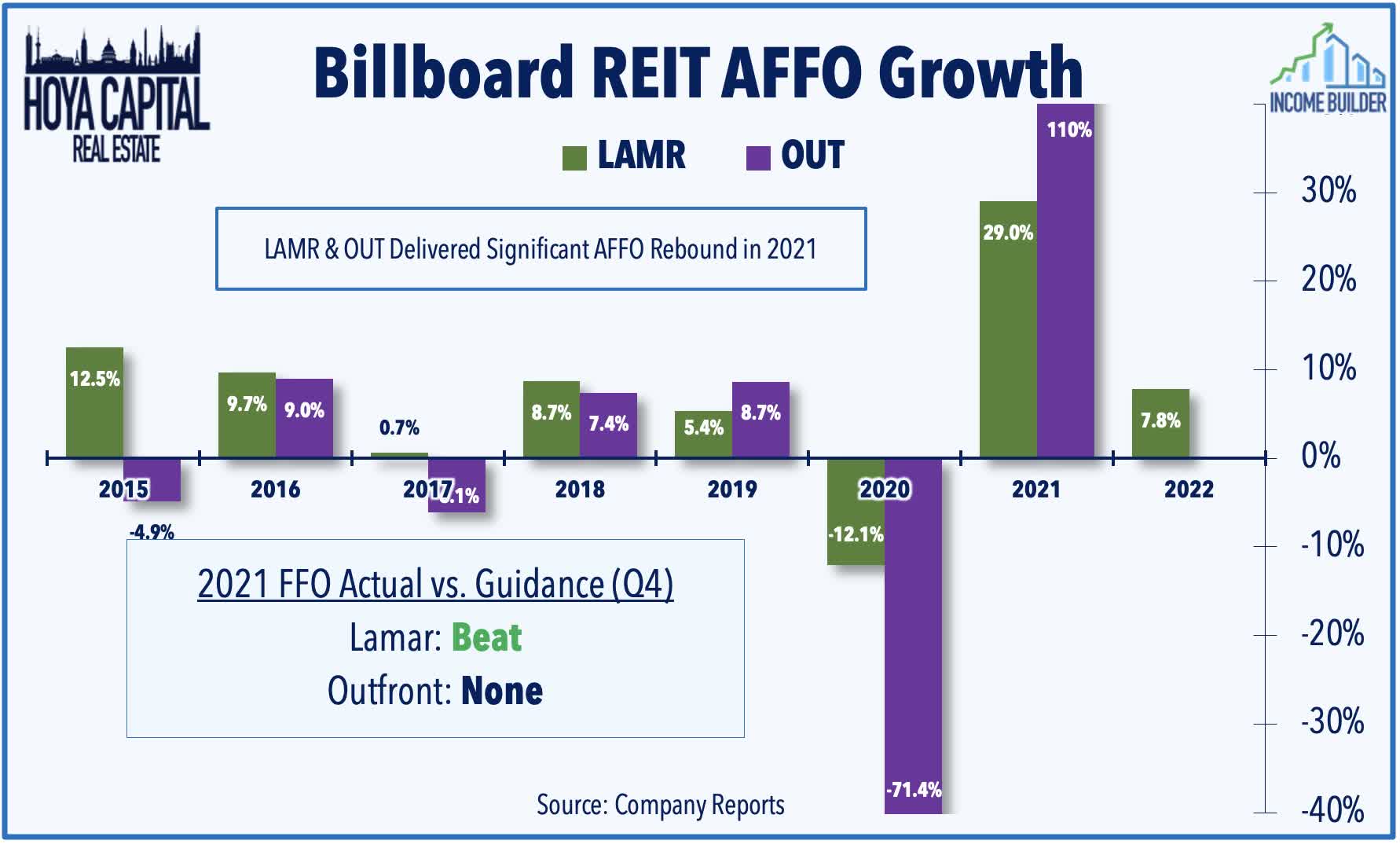

Billboards: Lamar Advertising (LAMR) was among the standouts last earnings season, reporting strong results which included a 10% dividend hike to $1.10, which is above its pre-pandemic rate of $1.00. LAMR recorded full-year FFO growth of 29%, which was 13% above its pre-pandemic level in 2019, a rather remarkable turnaround over the past 18 months. Outfront (OUT) reported impressive momentum with its AFFO back above pre-pandemic levels in Q4 and tripling its dividend to $0.30, but the outlook for LAMR – which has less exposure to public transit advertising than OUT – continues to be more favorable. We’re focused on the updated outlook for 2022 and commentary on the status of the digital display roll-out, which was slowed down by the pandemic.

Hoya Capital

Key Takeaways: Real Estate Earnings Preview

Real estate earnings season kicks off this week, and over the next month, we’ll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. Despite the historic surge in interest rates over the past quarter driven by expectations of Fed monetary tightening, REITs enter the first-quarter earnings season with some momentum at their backs. We continue to emphasize the importance of diversification across property sectors and market cap tiers, and the importance of focusing on property-level fundamentals. We’ll see updated guidance from most of the REIT sector, which will be our primary focus and we’ll provide real-time commentary throughout the earnings season for Income Builder members.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Prisons, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Be the first to comment