janiecbros Reata

Price is what you pay. Value is what you get. – Warren Buffett

Author’s Note: This is an abbreviated version of an article originally published in advance on Jan. 19, inside Integrated BioSci Investing for our members.

In biotech investing, whenever a company has two crown jewels, the investment risk is deleveraged. After all, when one lead drug fails, there is the other one to boost the fundamentals of your investment thesis. In other words, you have more chances of success with two lead drugs than with one. On that note, Reata Pharmaceuticals (NASDAQ:RETA) is powered by two highly promising medicines known as omaveloxolone and bardoxolone.

Back in February 2022, Reata received a complete response letter (i.e., CRL) for Bardo’s potential utility in Alport’s Syndrome. Nonetheless, there is a huge catalyst this year with omaveloxolone’s Prescription Drug User Fee Act (i.e., PDUFA) set for February. In this research, I’ll feature a fundamental analysis of Reata while focusing on the upcoming regulatory decision.

StockCharts

Figure 1: Reata stock chart

About The Company

As usual, I’ll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in Plano Texas, Reata dedicated its efforts to the innovation and commercialization of medicines to serve the unmet needs of life-threatening orphan (i.e., rare) conditions. I previously noted,

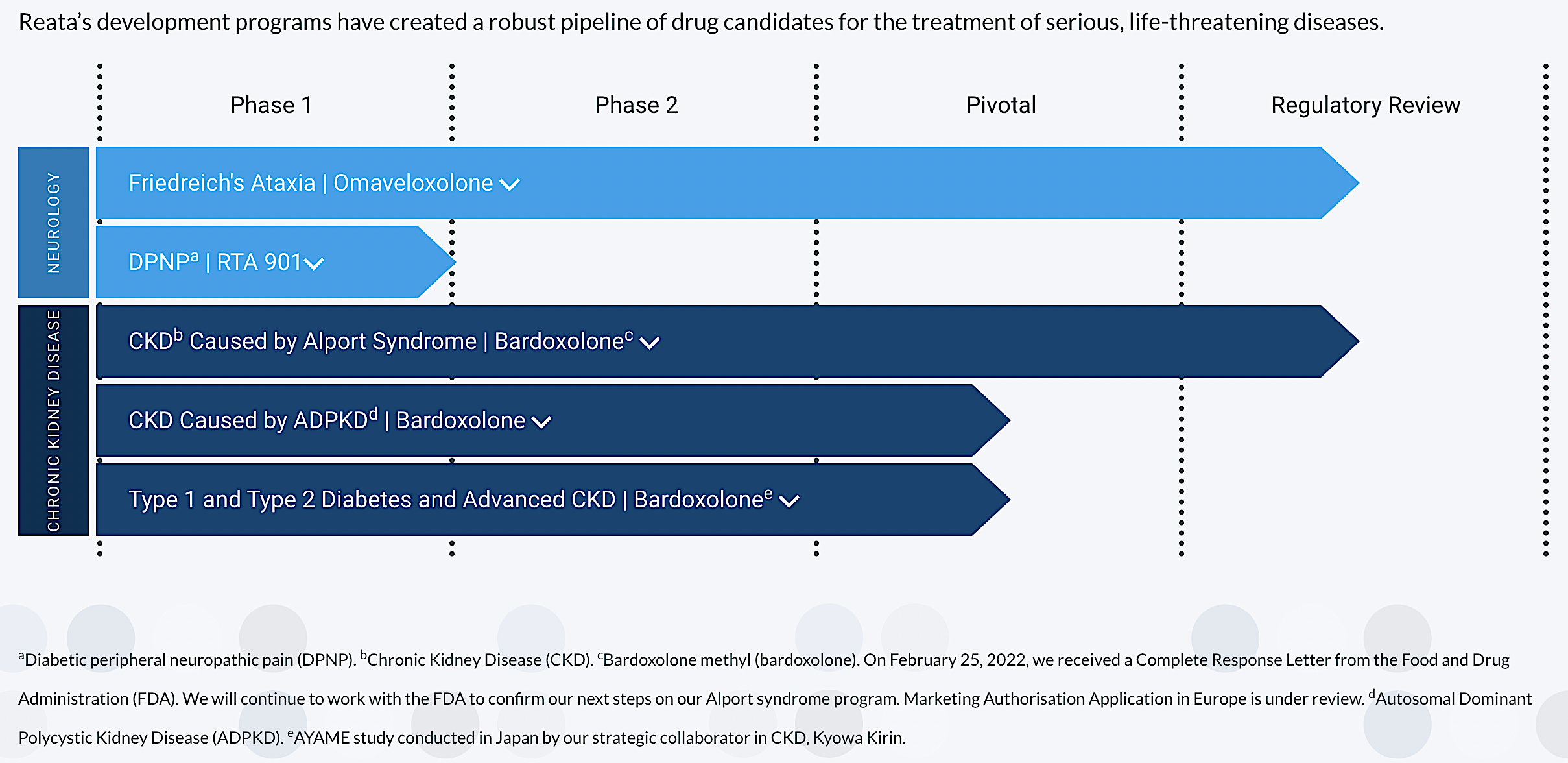

Most orphan diseases manifest symptoms of metabolic abnormality. Hence, it’s strategic that Reata’s technology targets the molecular pathways involving cellular metabolism and inflammation to address those abnormalities. As shown below, Reata’s pipeline is embodied by beauty and ingenuity because it is stacked by two advanced medicines – bardoxolone (Bardo) and omaveloxolone (Oma). By activating the crux transcription factor dubbed Nrf2, Bardo and Oma aroused a cascade of physiologic effects. This includes inflammatory and oxidative stress reduction as well as mitochondrial functional enhancement.

Reata

Figure 2: Therapeutic pipeline

Upcoming Catalysts

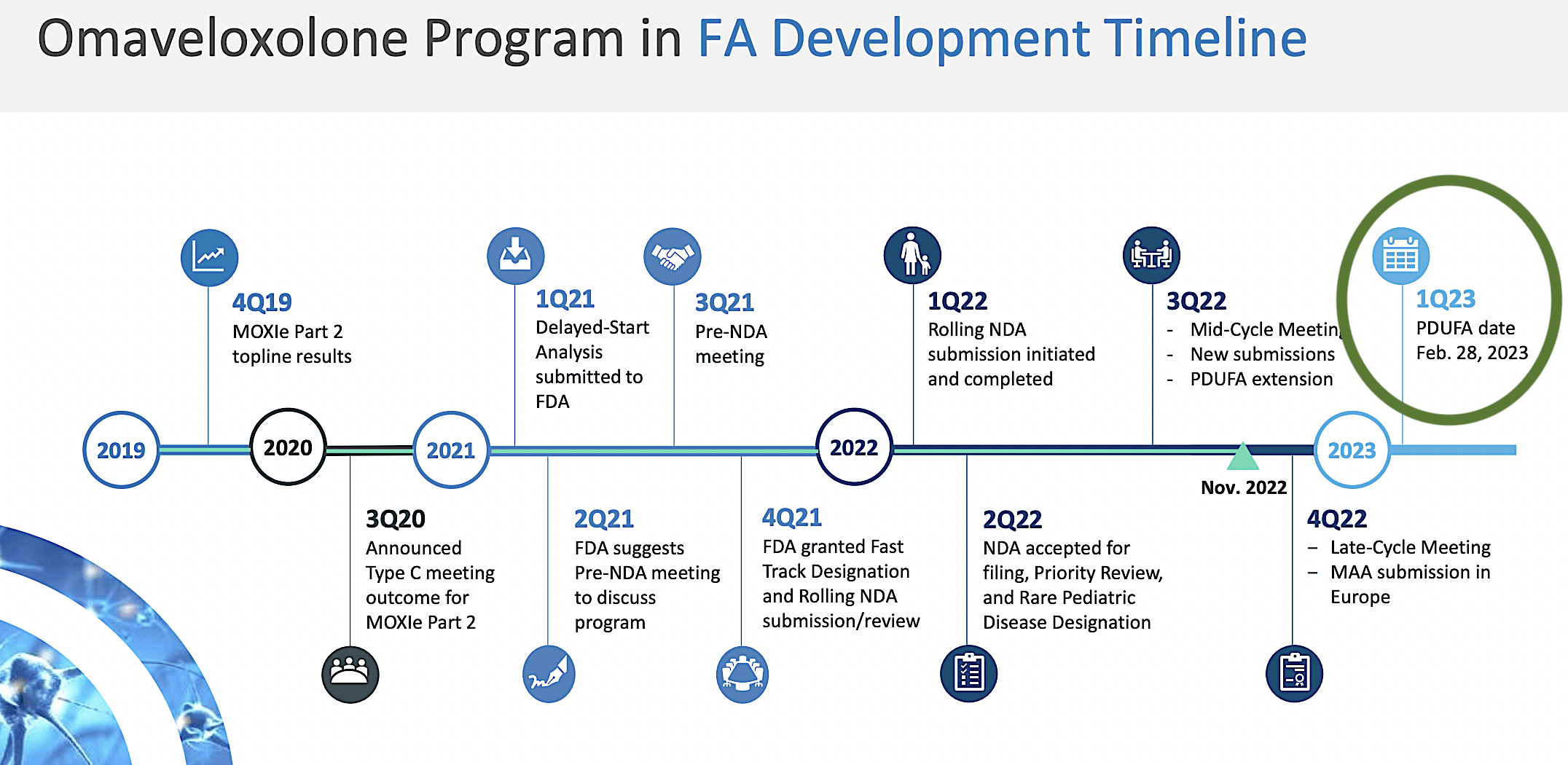

As you know, Oma has the upcoming Friedrich Ataxia PDUFA set for February 28. Notably, all of the developments lead to this climatic experience for Reata. Therefore, the upcoming binary event could be a substantial fundamental improvement for Reata if Oma can gain FDA approval.

Reata

Figure 3: Regulatory milestones

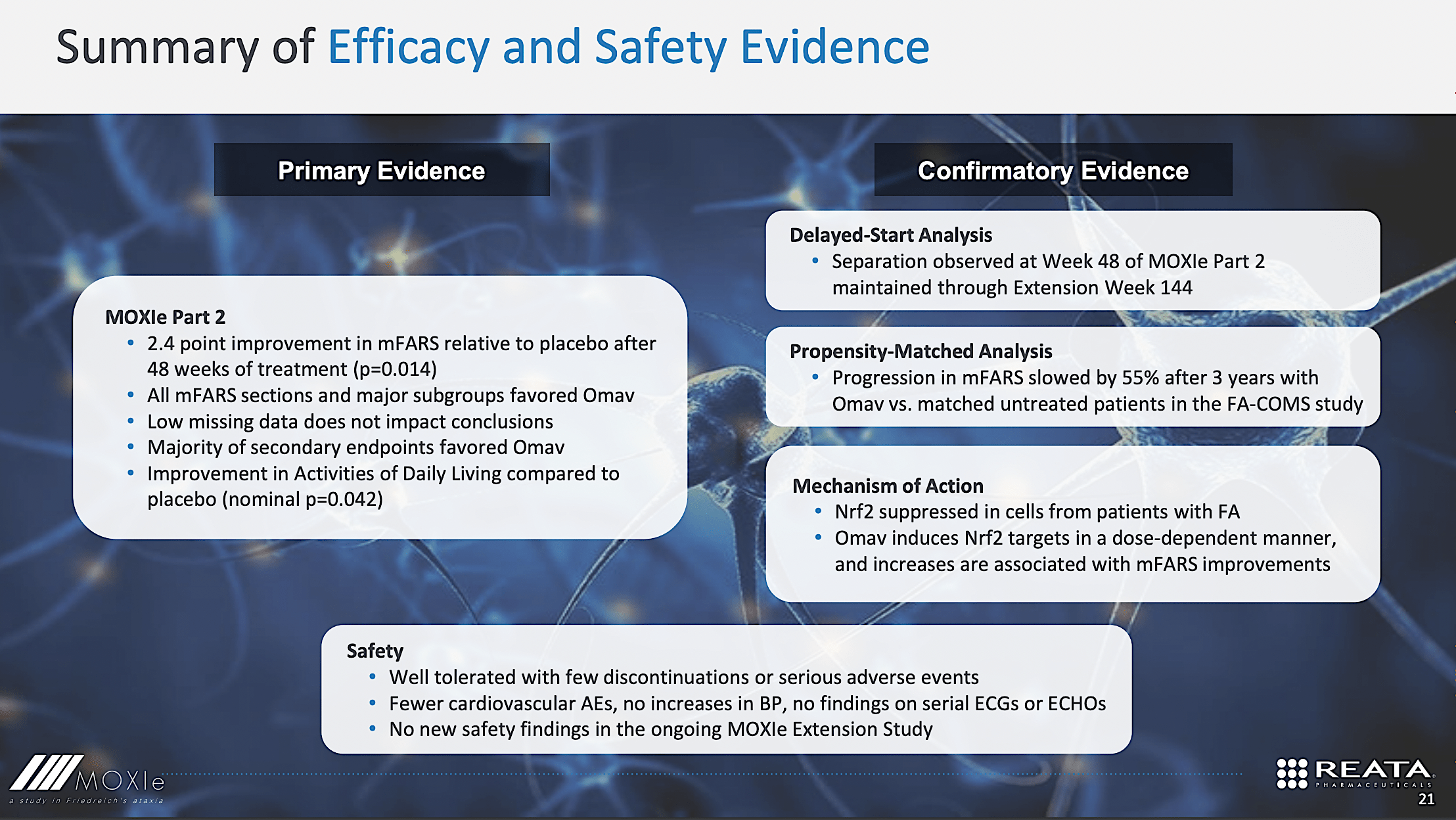

Due to its significant ramifications, you should go through the rationales to forecast the aforesaid event. Accordingly, Reata already completed its late-cycle meeting with the FDA. Evidence of efficacy is now established as shown below. Importantly, the agency neither asks for any additional data nor other development. There is also no advisory committee (i.e., ADCOM) meeting needed. That could be positive for Reata.

Reata

Figure 4: Oma efficacy

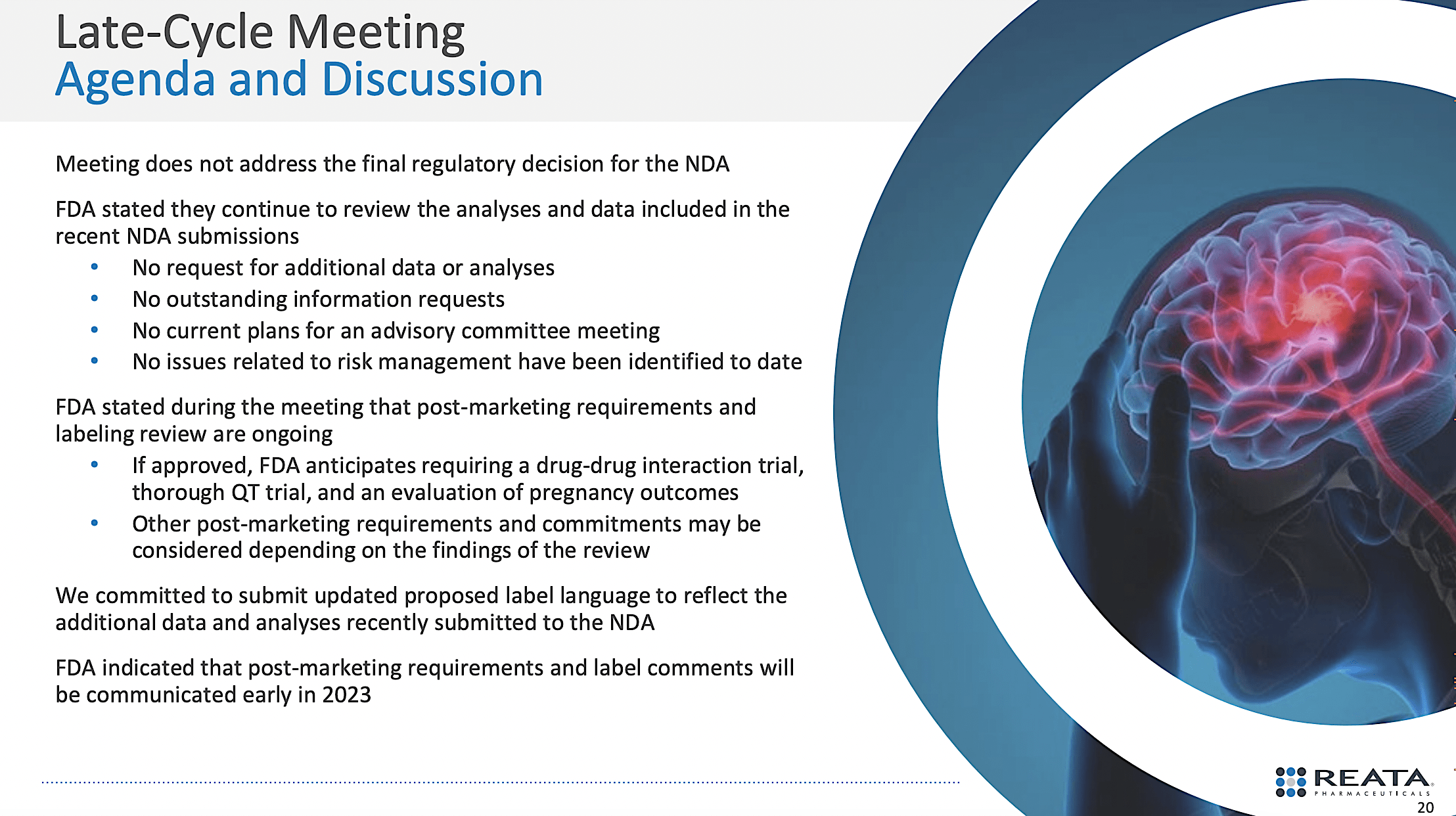

In my experience, whenever there is no ADCOM that usually means two things. First, the drug is nearly certain to gain approval. Second, there is no chance of getting through the FDA’s door. Specifically, the company mentioned this in their Q3 earnings,

During the meeting, the FDA indicated that post-marketing requirements and label review are ongoing. With respect to post-marketing requirements and commitments, FDA stated that if Oma is approved, they anticipate requiring a drug-drug interaction trial with CYP3A4 modulators, a thorough QT trial, and an evaluation of pregnancy outcomes. FDA stated that other post-marketing requirements and commitments may be considered depending on the findings of the review.

Reata

Figure 5: Late cycle meeting with the FDA

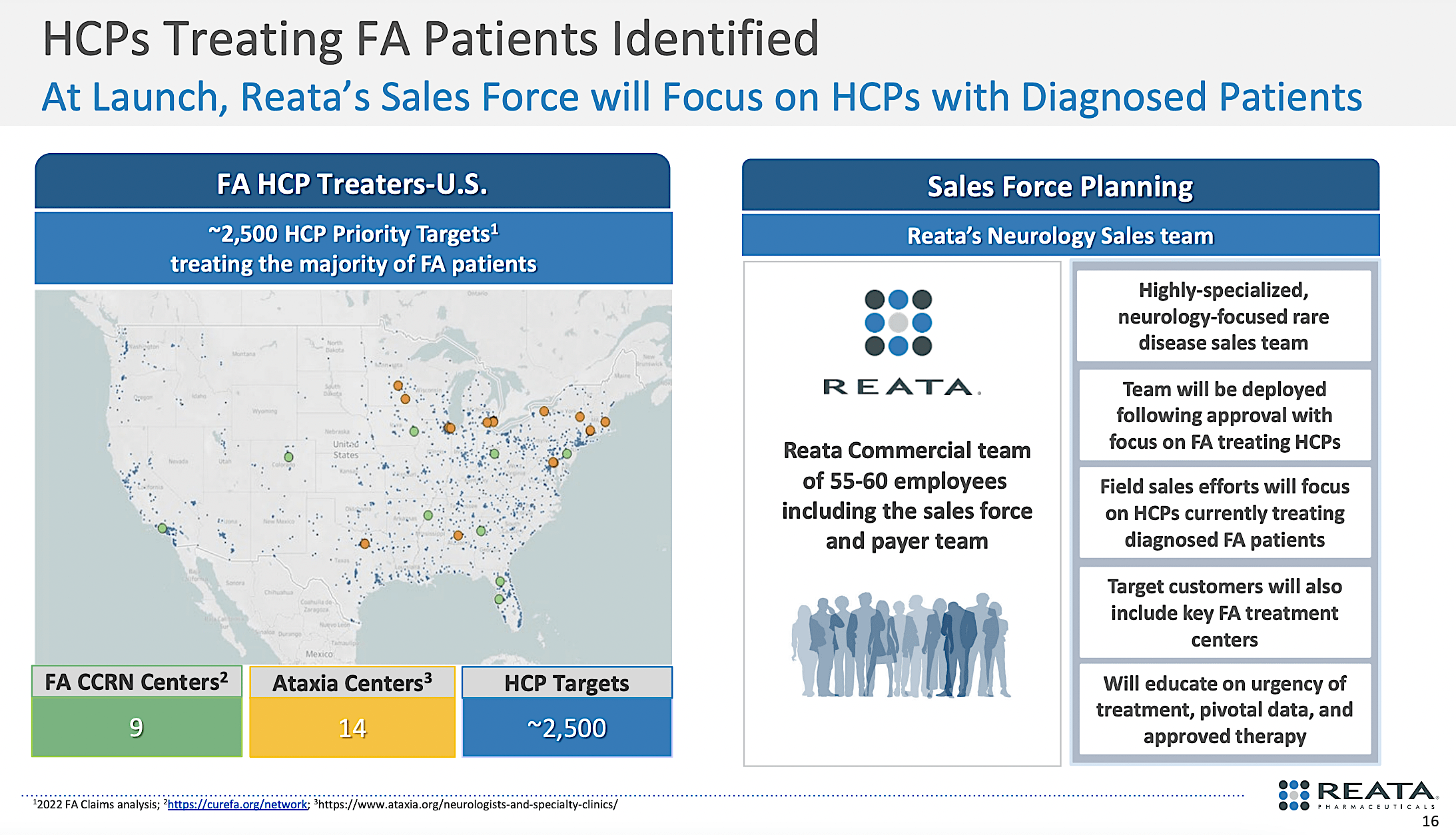

Launch Preparation

Though you do not know if Oma would be approved, it’s prudent that Reata is preparing for Bardo’s upcoming launch. That way, the company can be ready should approval comes. Notably, Reata built a sales team of 55-60 reps. As a group, the said professionals will target roughly 2.5K patients, 14 ataxia centers, and 9 FA CCRN Centers. You can argue that is a small team.

While that is true, Reata is launching its drug with an in-house team for an orphan condition, i.e. FA. Therefore, Reata could be successful with a limited number of reps that are highly specialized. After all, an orphan disease only occurs in a limited number of patients.

Reata

Figure 6: Oma launch preparations

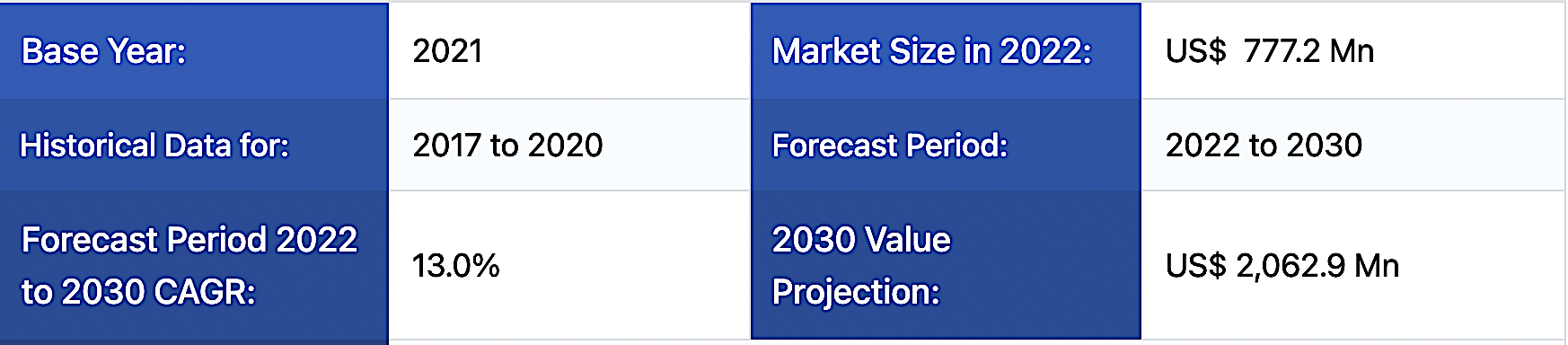

Estimated Market

According to Coherent Market Insights, the global ataxia treatment market is estimated to be $30.8M in 2021. Growing at 9.4% CAGR, it is expected to reach 47.3B by 2028. Of that total market, FA is projected to account for $777.2M in 2022 and expand to over $2.0B by 2030.

You might be wondering why such a disease with a small prevalence (i.e., less than 200K cases per year) would garner such a substantial market. The answer is in the premium reimbursement to foster innovation in this space. On average, an orphan molecule gets reimbursed at $140K annually.

Coherent

Figure 7: Estimated market

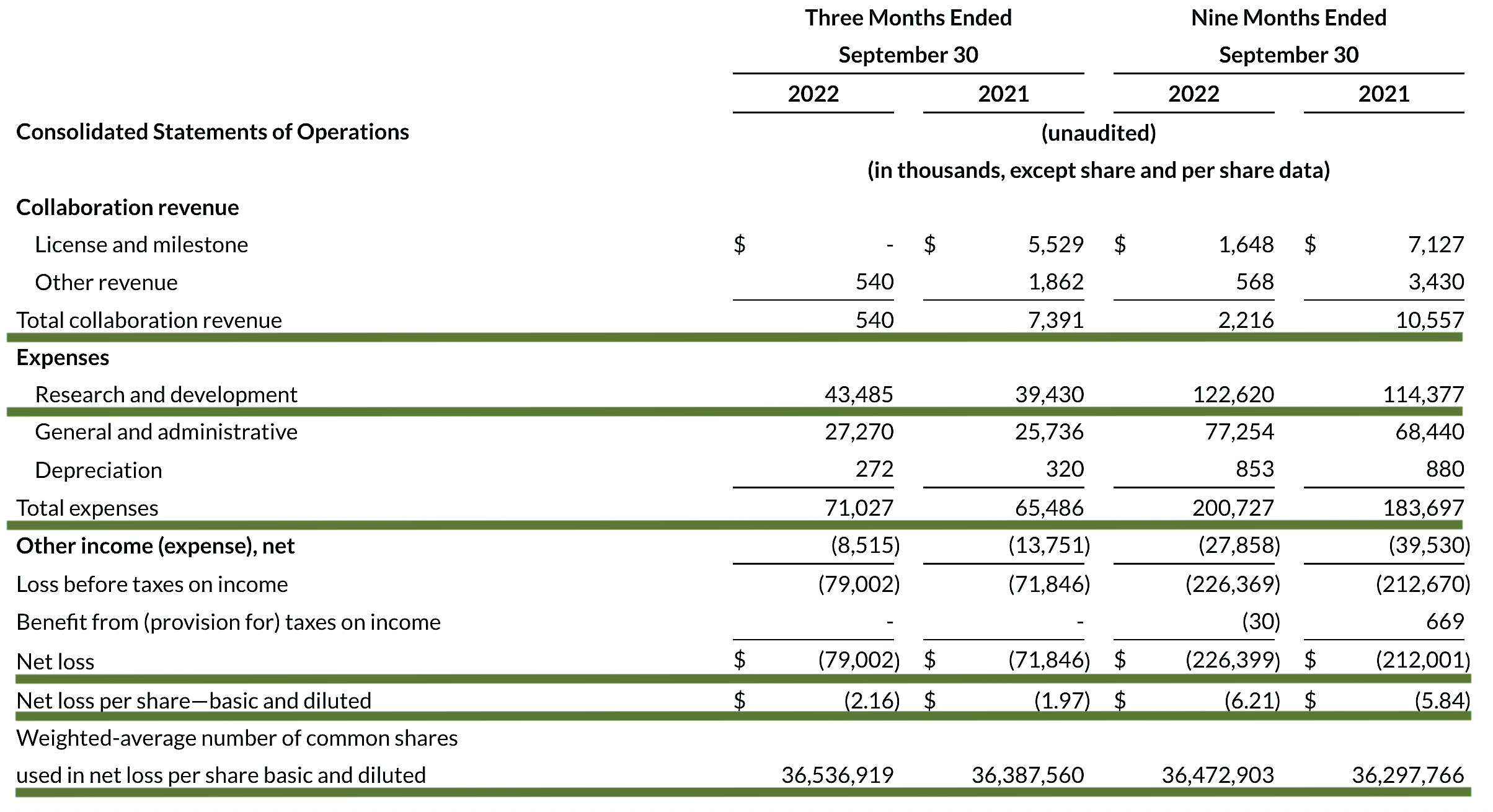

Financial Assessment

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll assess the 3Q2022 earnings report for the period that ended on September 30.

As follows, Reata procured $540K in revenue compared to $7.3M for the same period a year prior. As Reata is a developmental-stage company at this point, revenue should not be meaningful. That being said, let us assess other more meaningful metrics. Accordingly, the research and development (R&D) for the respective periods registered at $43.4M and $39.4M. I viewed the 10.1% R&D increase positively because the money invested today can turn into blockbuster results. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $79.0M ($2.16 per share) net losses compared to $71.8M ($1.97 per share) net declines for the same comparison. As you can see, the R&D increase cuts into the bottom-line earnings.

Reata

Figure 8: Key financial metrics

About the balance sheet, there were $435.9M in cash, equivalents, and investments. Against the $71.0M quarterly OpEx, there should be adequate capital to fund operations into 1Q2025 (i.e., 6 quarters of cash runway). Simply put, the cash position is robust relative to the burn rate. If Oma gains approval and thereby launches into the market, you can expect the burn rate to be higher.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with a thesis regardless of its fundamental strengths. More importantly, the risks are growth-cycle dependent. At this stage in its cycle, the main concern for Reata is whether Oma would gain FDA approval for FA by February. Moreover, there is a risk that Reata would not gain approval for its other lead drug, Bardo. That aside, Reata might burn substantial cash as the company prepares for an upcoming launch.

Conclusion

Reata Pharmaceuticals is an intriguing company because it has highly promising lead drugs (Bardo and Oma). Despite Bardo’s regulatory setback last year with the FDA, Oma is going to the Agency again for the orphan condition (Friedrich Ataxia). If approved, Reata’s fundamentals could be substantially improved. While there are certainly great risks, Reata has a decent chance of making a successful turnaround in the future. If so, your efforts will be justified. Your patience will be rewarded.

Be the first to comment