Artur Plawgo

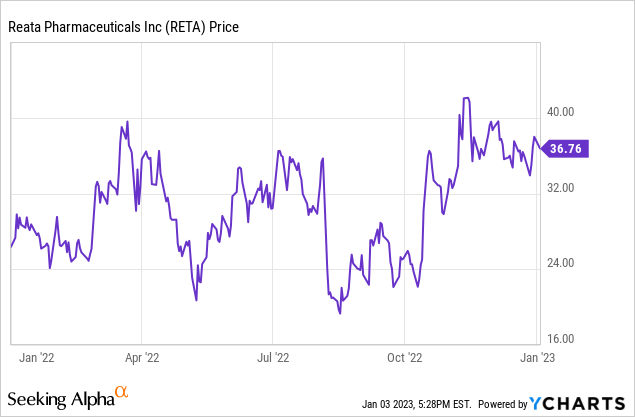

Reata Pharmaceuticals (NASDAQ:RETA) is possibly nearing bringing its first therapy to commercial sales. It has been a long road, with occasional setbacks. Reata’s stock price has swung wildly since it started trading in 2016: it topped $200 per share in late 2019, and for that matter in 2022, where its 52-week low was $18.47 and high was $43.90. It ended the year at $37.99 on renewed confidence that at least one of its therapies will get FDA approval in 2023. I believe that Reata’s setbacks were due to the complicated nature of the metabolic pathways that are preferred therapeutic targets. While the usual risks for a not-quite-commercial stage pharmaceutical company remain, I believe the data built up over time shows Reata’s scientific competence. The stock price should continue to go up (with the usual volatility) as inflection points are reached. Having presented positive Phase 3 data for omaveloxolone for treating Friedreich’s ataxia, the next hurdle is the FDA decision, due no later than February 28, 2023.

Omaveloxolone

Omaveloxolone is an Nrf2 activator. It is a complex small molecule in the oleanane triterpenoid family. Nrf2 activation can break inflammatory cycles that lead to mitochondrial dysfunction and inflammation of neurons. In Friedreich’s ataxia, which is caused by a recessive mutation, the FXN gene is defective. That results in lower frataxin protein production, which impairs mitochondrial functions, which creates a cascade leading to neurodegeneration. Ataxia is the resulting lack of control of muscles. Typically, patients require wheelchairs before or by their early 20s. FA is the most common inherited ataxia, affecting about 5,000 people in the United States and 22,000 globally. The hypothesis was that omaveloxolone would, by Nrf2 activation, break the cycle of inflammation caused by a lack of frataxin. Pre-clinical trial supported the hypothesis and clinical trials showed improvements for FA patients.

The FDA accepted an NDA for omaveloxolone for FA in May 2022. It was given priority review status, but in August a three-month extension was announced to consider data from an extension of the trial. The PDUFA (decision) date is now February 28, 2023. There will not be Advisory Committee meeting. It is highly likely the FDA will approve the therapy, so that likelihood should be built into the current stock price.

Reata has been preparing for commercial sales of the drug. It is given once daily and has Fast Track and Rare Pediatric Disease designation. Although it is likely to have expensive, orphan-drug pricing, it seems likely that insurers in the U.S. will pay, given the outcomes of lack of treatment and relatively small patient count.

Because of its mechanism of action, omaveloxolone may also work for other neurological indications. Reata has said preclinical work indicates omaveloxolone may be applicable to progressive supranuclear palsy, ALS, Parkinson’s, frontotemporal dementia, Huntington’s, Alzheimer’s, and epilepsy. Any revenue beyond FA would be years away, given the time required to conduct clinical trials.

Bardoxolone

Bardoxolone, like omaveloxolone, is an Nrf2 transcription factor that appears to restore mitochondrial function. Its leading indication is now CKD, or chronic kidney disease, when caused by Alport Syndrome. An FDA Complete Response Letter was issued for Bardoxolone for Alport Syndrome CKD (chronic kidney disease) on February 25, 2022. The problem is CKD is slow to develop and EGFR, which was measured in the Phase 3 trial, is not considered a clinical endpoint by all physicians, or the Advisory Committee. This could be fixed by a large Phase 3 trial in Japan in diabetic CKD with a new primary endpoint of dialysis delay. The Japanese Ayame trial follows patients for 3 years and was expected to complete enrollment in 2022. Reata is working with the FDA on next steps, but it looks like acceptable data might be 3 years away.

Bardoxolone is also in Phase 3 clinical trials for CKD caused by ADPKD (Autosomal Dominant Polycystic Kidney Disease) and by diabetes, following positive results from the Phase 2 trials. ADPKD is an inherited kidney disease dependent on PKD1 and PKD2 genes and their various mutations. Its progression leads to the need for dialysis. It does have some treatment options, notably tolvaptan. There may be 300,000 or more cases in the United States. Many go undiagnosed until patients are between 30 and 50 years old. CKD eventually affects about 1 in 10 people, causing nearly 1 million annual global deaths. One in three adults with diabetes have CKD.

Rest of Pipeline

The other potential therapy in the clinical pipeline is RTA 901. It is currently targeted at Diabetic Peripheral Neuropathic Pain or DPNP. This is a condition with several million potential patients, with currently approved therapies leaving much room for improvement in both efficacy and tolerability. RTA 901 is a small molecule that modulates Hsp90. There are no recent updates on RTA 901, but the Phase 1 trial in healthy volunteers had no safety or tolerability issues and exhibited an acceptable pharmacokinetic profile.

Cash and Q3 Results

Reata ended Q3 2022 with cash and equivalents of $436 million, down $45 million in the quarter. Revenue was under $1 million, net loss was $79 million, and EPS loss was $2.16. Guidance was that cash should be sufficient through 2024. Not knowing how fast revenue from omaveloxolone will ramp, I would not rule out a cash raise if the stock price jumps if there is FDA approval.

Conclusion

At one point in time, in 2018, I thought Reata was near having a therapy for pulmonary arterial hypertension (See Reata Pharmaceuticals A Buy On Bardoxolone Data). The market did as well: the stock price was much higher than it is now. Bardoxolone data was not able to get approval for the hypertension indication. Already in that article I wrote about the Alport Syndrome indication. Biology, or life, is likely the most complicated thing in the universe, so perfectly good sounding preclinical or even early clinical data may not work out in large clinical trials. Despite the setback, Reata carried on and is near commercial success with omaveloxolone for FA. There is, however, some possibility that the FDA will not grant approval.

Approval of omaveloxolone would be proof of commercial viability. However, the ramp may be slow, so it is too early to predict reaching cash-flow break even. I would expect, instead, that the R&D budget will be increased to try to take advantage of the opportunity with the drugs currently in the clinical stage pipeline. A preclinical pipeline may be revealed as well. Likely new indications will be added. Additionally there is the possibility that the platform can generate new potential therapies. One reason I have liked and followed Reata, even when I did not own stock, was its focus on mitochondria-related diseases, not typically a target for big pharma companies.

This is all exciting for long-term investors, but how does potential compare to the current stock price? Reata sank 3.4% on the first trading day of the new year, closing at $36.71. That gives it a market capitalization of $1.39 billion. With a good pot of cash in reserve and ramping revenue from omaveloxolone in 2023, I think Reata is in a good position to continue its R&D program and bring further therapies and indications to market. For long-term investors, that is clearly a Buy signal. But some might want to wait until after the FDA decision, to reduce risk. It depends on one’s risk appetite and portfolio structure.

Be the first to comment