sommart

Article Thesis

Realty Income (NYSE:O) has seen its shares pull back quite a lot in recent months. And yet, the company’s underlying performance remains highly compelling. This combination of operational progress and a dropping share price has made O one of the best values in years, and its dividend yield has risen to a quite attractive level as well. Since Realty Income also has a history of outperforming during economic downturns, Realty Income looks like a nice pick at current prices.

Realty Income’s Operational Progress Remains On Track

Realty Income is one of the largest REITs by market capitalization, but that doesn’t mean that the company has become slow-moving due to its size. Instead, Realty Income’s management has continued to grow the company at a sizeable pace, which includes heavy acquisition spending that is partially financed via the issuance of new shares. That does dilute shareholders in theory, but as the acquisitions that Realty Income made had a large enough impact on company-wide profits, funds from operations continued to grow even on a per-share basis, where the increased share count is accounted for.

Realty Income is a retail-focused REIT, but that doesn’t mean it suffers from e-commerce competition. Instead, most of its tenants are resilient versus the threat of Amazon (AMZN) and others. Drug stores, post offices, restaurants, fitness clubs, grocers, dollar stores, and so on are way more resilient versus online competition compared to retailers that sell books or apparel. Luckily, Realty Income focuses on the first group of tenants, which is why it continues to do well even though some other retail REITs (think lower-quality mall owners) are struggling.

Realty Income generated hefty 75% revenue growth during the most recent quarter. That was driven by its VEREIT acquisition to a large degree, but even when we back that out, Realty Income would have grown at a nice pace. Acquisition spending totaled $1.7 billion during the second quarter alone, and management is now expecting acquisitions of around $6 billion for the full year. In the recent past, Realty Income has increasingly moved into foreign markets with its acquisitions, which also held true during the most recent period. In Q2, Realty Income spent around 40% of its investments outside of the United States. Due to the strengthening US Dollar, which makes acquisitions in other markets, such as the EU or the UK, cheaper, the increased offshore spending makes sense. For comparatively few Dollars, Realty Income can acquire assets, and in case the US Dollar starts to weaken again over the coming years, rent proceeds that are then translated from Euros or British Pounds to US Dollars will be rising.

But Realty Income is even growing when we back out both the VEREIT acquisition and its “normal” acquisition spending. Organically, Realty Income is growing via rising occupancy rates, i.e. getting more tenants at a fixed portfolio size, and by growing its lease rates on existing properties. Both of these trends remained intact in the recent past [emphasis by author]:

“Finally, the health of our real estate portfolio remains strong as we finished the quarter with occupancy at 98.9%, the highest occupancy rate in over 10 years, while also achieving a 105.6% recapture rate on our releasing activity. I am proud of the collective efforts of our One Team as we continue to generate value for all of our stakeholders.”

The rising occupancy rate shows that the pandemic only was a (benign) short-term issue for Realty Income. Even better, occupancy rates are currently higher than they were before the pandemic, as the Q2 occupancy rate was the highest over the last decade. It looks like Realty Income’s tenants are neither being replaced by Amazon nor are they fearing the ongoing economic downturn — the result of Realty Income’s focus on resilient, non-cyclical, oftentimes essential businesses when it comes to its leasing activity.

Realty Income recaptured 106% of its previous rents when releasing properties. This drives Realty Income’s cash flow and profit from existing locations, especially since Realty Income’s triple-net lease model means that its own expenses aren’t growing meaningfully. A large portion of Realty Income’s additional revenue from rent increases is thus flowing through to the bottom line, making this organic growth via rent increases highly profitable and therefore attractive.

Overall, between the major VEREIT acquisition, its normal property acquisitions, and organic growth, Realty Income managed to grow its normalized funds from operations by 15% during the most recent quarter — with the increase in its share count already being accounted for. REITs generally aren’t growth vehicles, so a mid-teens profit growth rate is extremely compelling on a relative basis, I believe. Of course, growth will not always be this high and should slow down to some degree once the VEREIT takeover has been lapped. But still, with several growth drivers in place, investors can expect Realty Income to continue to offer solid growth both on a business-wide basis and on a per-share basis.

Over the last five years, Realty Income grew its funds from operations per share by 5% annually — even though that time frame included the pandemic. It would not be too surprising to see Realty Income generate somewhat higher growth during normal times, although it should be noted that the pandemic was not much of a headwind for Realty Income. Nevertheless, the company expects this year’s FFO per share to grow by 11%, which is well above the average over the last couple of years. But even if Realty Income’s growth slows down to the 5% range in 2023 and beyond, that would make for a very solid investment, I believe, due to Realty Income’s current valuation and starting dividend yield.

Realty Income Stock: The Best Value In Years

Price is what you pay, and value is what you get. As shown above, investors get a lot of (steadily growing) value by buying Realty Income. And yet, the price for its shares has come down quite a lot in recent months, and Realty Income’s current valuation is very undemanding:

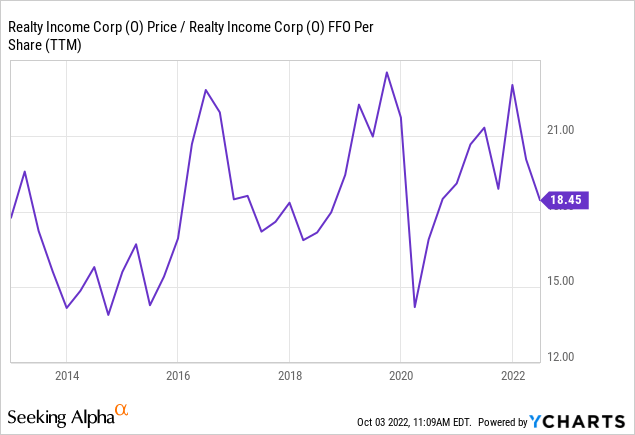

Over the last decade, Realty Income’s FFO multiple has moved between 14 and 23. Over the last six years, Realty Income’s FFO multiple mostly was above 18, with the FFO multiple dropping below 15 for a very short period of time only — during the midst of the initial COVID-induced equity market sell-off. On a forward basis, Realty Income is currently trading at 14.5x its funds from operations. That is, at least compared to the last five years, a well-below average valuation. In 2014 and 2015, Realty Income was trading at a similar valuation for a while, and those with perfect timing were able to buy O at a similar valuation during spring 2020 for a very short period of time as well. But overall, Realty Income used to be much more expensive, on average, meaning that the current inexpensive valuation makes for an attractive buying opportunity.

That’s also showcased by the company’s above-average starting yield of 5.1%. Over the last couple of years, Realty Income often traded with a yield of around 4%, sometimes as low as 3.5%. Investors barely had the chance to buy Realty Income with a yield of more than 5% over the last decade, with the COVID bear market being a short-lived outlier.

If one were to buy Realty Income today, locking in a starting dividend yield of 5.1%, and if Realty Income were to grow its FFO and dividend by 5% a year going forward — in line with the last five years — one could reasonably expect 10% annual returns, all else equal. If Realty Income’s valuation were to increase, e.g. to 17x FFO over the next 5 years, total returns could be in the low-teens range. Since Realty Income is trading at a below-average valuation right now, multiple expansion would not be surprising at all, I believe. But the good thing is that it’s not needed — even without multiple expansion tailwinds, O could generate highly compelling total returns going forward.

Summing It Up

Realty Income is a high-quality REIT. It has a great total return track record, has hiked its dividend for more than 25 years in a row throughout all kinds of crises, it remained resilient during the pandemic, and the real asset nature of its business offers compelling inflation protection.

Its tenants are safe from the Amazon threat in most cases, and demand for its properties remains high and resilient, showcased by the decade-high occupancy rate even during the current environment, where an economic slowdown is pretty foreseeable.

And yet, this quality REIT was sold off along with the broad market in recent weeks, which has made its shares slump to an FFO multiple of less than 15. That makes Realty Income one of the best values in years, and investors also get a pretty nice starting yield of more than 5%. In combination with regular dividend growth, that’s pretty compelling.

I do believe that there’s a good chance that Realty Income will deliver total returns of 10% a year going forward. In a more bullish scenario, where its FFO multiple expands to the high-teens again, total returns would be even higher. At current prices, this sleep-well-at-night REIT looks worthy of investment.

Be the first to comment