AaronP/Bauer-Griffin/GC Images via Getty Images

Raytheon (NYSE:RTX) reported an above average quarter in Q4 ’22, which was driven by better than expected outlook offset by continued backlog growth in Pratt & Whitney and RMS (Raytheon Missile Systems). Strategically speaking, Raytheon made some key announcements, as they consolidated the Raytheon Missile Systems with the Raytheon Intelligence and Space Segment or RIS for short. The two segments will combine into a singular reporting segment, which is hoped to generate some efficiencies and reduce some of the engineering overlap in the rocket propulsion systems used in either missiles or satellite launch programs.

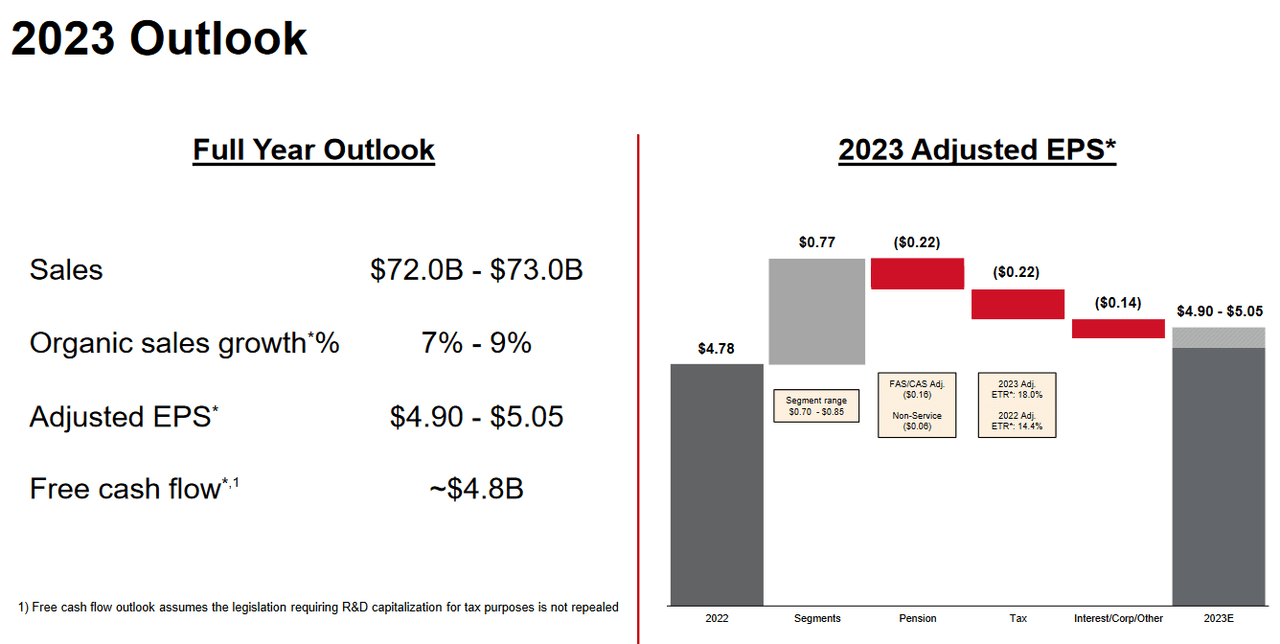

In terms of Q4 ’22 revenue, the company reported $18.09 billion missing consensus by $70 million. The announced outlook for FY’ 23 of 7%-9% growth was what beat expectations and caused the stock price to rally +3.35% in the earnings-fueled session to close just shy of $100 at $99.47. We revise our price target up from $95 to $110 implying a very modest 10% upside to the stock price currently. Furthermore, we expect added revenue/earnings contribution tied to the outlook, but it doesn’t materially alter our stance on the stock, so we maintain our neutral rating on RTX.

Expectation lift was tied to better than expected revenue recognition tied to Collins Aerospace, and also Pratt & Whitney from commercial contract revenue, where they retrofit or sell various aviation components for third-party manufacturers of commercial aircraft. However, the military segment results were weak for both Collins and Pratt and Whitney but expected to improve over the course of FY ’23.

Figure 1. Financial outlook and 2023 commentary

Raytheon Q4 2022 Earnings Presentation (Raytheon)

The outlook was relatively positive at 7%-9% organic growth which was above our long-term revenue growth estimate of 6.45% offering 2 to 3 percentage points of growth upside to our initial growth estimate. Comments on growth levers and staying to the growth target and how they could be back half-weighted in the earnings call helpful in justifying a higher valuation.

Q4 ’22 performance from its consumer aviation division with regards to Collins Aerospace and Pratt & Whitney helped offset some of the weakness in military results. Both Collins Aerospace and Pratt & Whitney reported revenue growth from commercial original equipment growth of +20% and +37% respectively whereas commercial aftermarket revenue from both divisions were up +21% and +11% respectively. Collins Aerospace markets various components found commonly on airplanes such as airplane avionics, space frames, fixed wings, etc.

Pratt & Whitney markets geared turbofan engines or GTFs for commercial aircraft (this part of the business did great). Pratt & Whitney’s military unit sales for After burning Turbo Fan engines for F35, F22, F16 and other military aircraft shrunk for the quarter by -2%. This was due to the delays of the F135 engine for the F35 stealth aircraft, which we discuss in our prior article on Raytheon.

According to J.P. Morgan analyst Seth Seifman:

With guidance for $9.7b of aggregate FCF for 2022-23 vs the $8.9b we expected and plans to buy back stock worth $5.8b over that period vs the $5.1b we expected, Raytheon’s performance and outlook seem to answer the mail in the largest sense.”

Share buyback of $5.8 billion could reduce share count more than expected or by 58 million shares assuming the stock continues to trade in the $100 per share range.

Revising our Raytheon estimate up

Based on the management guidance, and better than expected delivery figures for various other equipment parts from both its Collins Aerospace and also its Pratt & Whitney division the business might not be as militarily dependent and could surprise on earnings results tied to just the commercial aviation component. We adjust our revenue and dil. EPS estimate in our model upwards, and also provide an estimate for next quarter earnings and revenue as well.

We provide a Q1 ’23 revenue estimate of $16.97 billion revenue (mid-point of guidance), which compares to consensus estimates of $16.82 billion. For Q1 ’23 we forecast $1.61 billion net income, and adjusted dil. EPS of $1.10 versus consensus estimates of $1.14 adjusted dil. EPS.

We adjust our valuation upwards from our prior forecast as we embed a more aggressive growth target and adjusted profit margin figure to arrive at a higher price target. We adjust our FY ’25 revenue estimate upward from $81 billion to $84.52 billion with an average growth rate of 8% per year from the prior growth CAGR of 6.45%. We adjust our profit margin target a bit higher to reflect the better margin contribution from various segments. As such, our adjusted profit margin goes up to 11.75% from 11% to arrive at our adjusted net income figure of $9.93 billion, share outstanding of 1.4 billion, and $7.09 adjusted dil. EPS.

Our prior $95 price target moves a bit higher, as we think there’s some room to break above the $100 price level over the course of 12-months. We value the business at the prior multiple, 21x earnings, and apply the firm’s WACC 8.15% to arrive at our price target of $109.43 or basically a $110 price target. Given the very modest +10% upside from current levels we maintain our neutral rating.

Other and final considerations from the quarter

We thought the commentary from Q4 ’22 was upbeat though upon running the calculation to adjust our model up we came away with a slight improvement to our valuation estimate. We like the underlying fundamentals of the business, but wouldn’t chase after the stock, as upside doesn’t seem all that substantial. Growth outlook was promising, efforts to return capital are appreciated, but we still need to see improvement from military contracts and those contracts have to be reflected in terms of recognized revenue. We like the product pipeline, and efforts to reorganize the business to improve efficiency.

The company could easily trade higher on political sentiment assuming Congress passes a budget that increases military spend by greater than 10%. But, based on what we’ve seen in the news, the House has passed a bill referred to as the National Defense Authorization Act or NDAA. While the bill has yet to pass the Senate and will take a couple weeks, it provides additional aid to Ukraine ($800 million) and Taiwan ($10 billion). It’s not as high as what we had hoped for initially, as United States military spending will increase just 8% versus prior year to $858 billion.

Raytheon is a great hedge on the Ukrainian War as any bad news tied to the region is implicit of sales contribution further down the road, and could offset stocks who have negative exposure to the Ukrainian War. We maintain our neutral rating as we demand returns that are better than just 10% in this environment. Also, the stock could be poised for unexpected risk if in the event the War in Ukraine ended sooner than what most political analysts and pundits predict. Without Eastern European tensions the stock would be trading at much lower levels.

Without any further catalysts over the horizon aside from revisiting the prior-thesis of improved deliveries on the military side, and efforts to win more military contracts in foreign markets we cannot base our recommendation on just blind hope. Risk/reward must be more compelling to make a long-term investor want to stay the course as the prospects of returns are a bit limited based on the projected growth/profit expansion into 2025.

Be the first to comment