Vladimir Zakharov

By Antoine Bouvet, Padhraic Garvey, CFA, Benjamin Schroeder

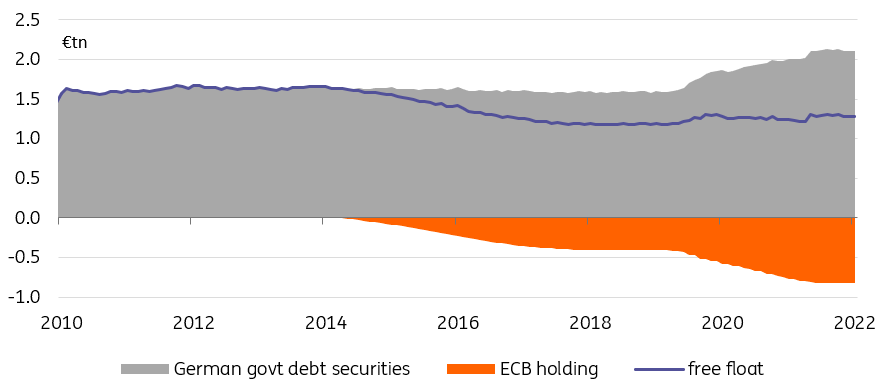

Collateral scarcity is easing

Whilst supply runs its course this week, and the macro-focused participants await US CPI tomorrow, one development that has caught our attention is the sharp tightening of swap spreads. There is often more than one possible driver but one starting point is the German treasury’s decision in late October to boost the amount of bonds lent on the repo market by €54 billion to finance part of its energy support package. Bloomberg reported yesterday that, according to its sources, net issuance of German debt should reach €45 billion in 2023, nearly three times the originally planned €17 billion.

Germany is the euro bond market where scarcity is most acute, so both pieces of news go a long way towards alleviating fears that the last two months of 2022 would see a dash for collateral. Other factors, such as the increased chatter of European Central Bank intervention, or hopes that early targeted longer-term refinancing operation (TLTRO) repayments would release some collateral, might have helped, but we list them only as secondary drivers of the collateral situation.

ECB Purchases And Austerity Have Led To A Scarcity Of German Government Debt (ECB, Refinitiv, ING)

Improving sentiment may play a role, but so do cautious investors

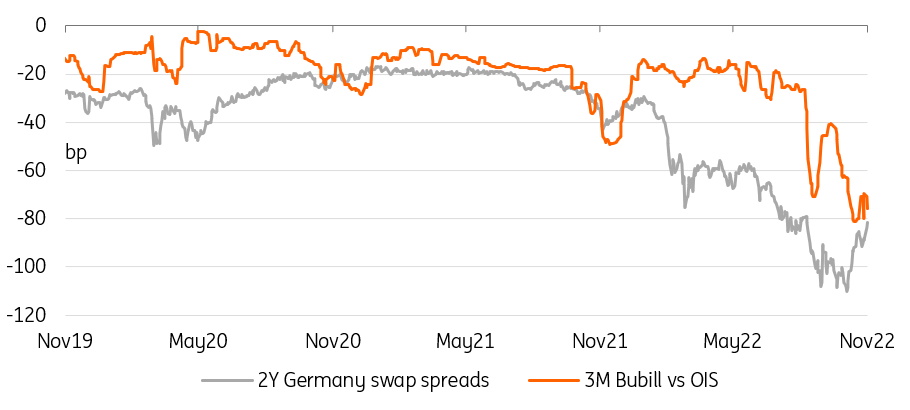

Then there are the macro drivers, including decreased risk aversion after the perceived central bank pivot and generally better performance of risk assets. These feel harder to pin down, in our view. Firstly, it is true that swap spreads tend to widen when risk aversion increases, but regular readers know that we don’t really think there is much of a “pivot” for investors to celebrate. Secondly, collateral scarcity have tended to dominate other factors in the past, so this seems a more logical explanation to us.

Finally, we would not underestimate the effect of near-term debt issuance. Admittedly, this week’s slate is by no means the heaviest of the year, but we expect investors to be particularly reluctant to buy bonds as the end date of this tightening cycle seems to be pushed further away into the future. The barrage of hawkish comments from the likes of Kazaks and De Guindos yesterday attest to this risk.

German Swap Spreads Have Tightened But T-Bills Remain Stretched Against OIS Swaps (Refinitiv, ING)

Today’s events and market view

This week’s supply bonanza continues, with Germany, the UK, and the US all selling 10Y bonds in their respective currencies. The UK sale stands out, being of the green sort, as a topical choice with the COP27 taking place this week in Egypt.

Data releases will be pretty thin on the ground with only US mortgage applications, sales and inventories. The task of keeping investors engaged ahead of tomorrow’s US CPI will befall central bankers. Frank Elderson is the sole ECB speaker on the roster but John Williams and Tom Barkin, of the Fed, and Jonathan Haskel and Jon Cunliffe, of the Bank of England, will more than make up for it.

Bonds staged a significant reversal yesterday, led by the back end. This may be a sign that our supply concerns may have been overstated, but we retain a bias towards higher rates due to the macro outlook and limited risk appetite, and with yet more debt sales scheduled for this week.

At the time of writing, partial US midterm election results were suggestive of a split legislature, with the Democrats retaining control of the senate, and with the Republicans gaining control of the house. Compared to a Republican sweep, we think this result would be less conducive of higher yields.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Be the first to comment