YinYang

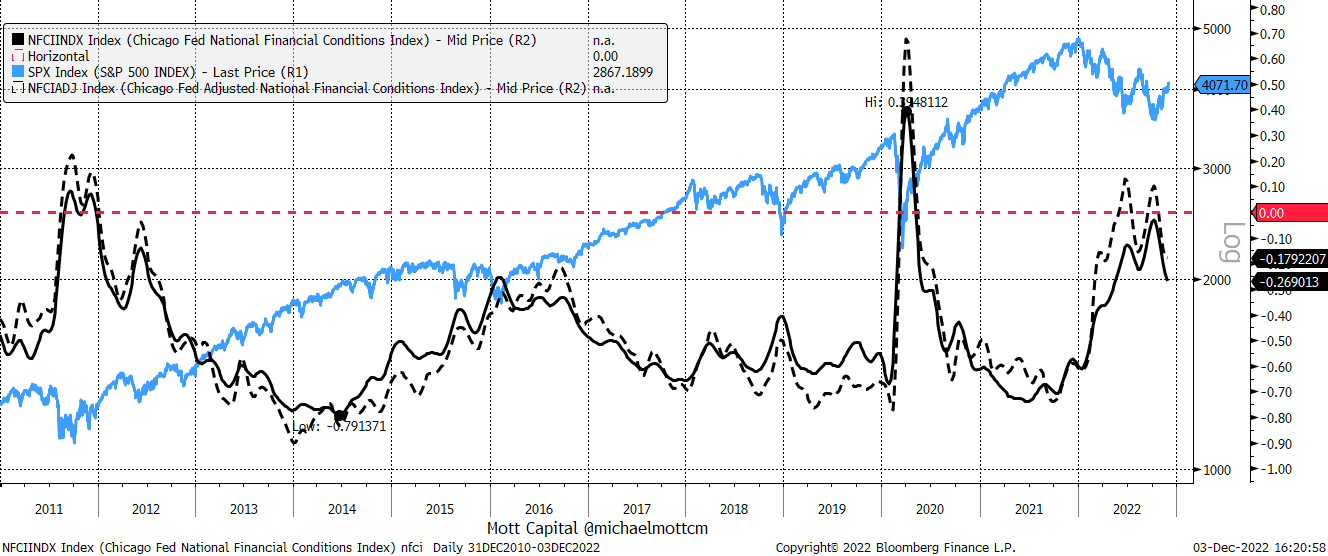

Powell’s appearance on Wednesday was not only jaw-dropping but raised a lot of questions. Instead of pushing back against the recent easing of financial conditions, Powell made the same comments as he did at the November FOMC meeting and even stressed caution on overtightening.

This market has come to a point where anything that is not more hawkish than expected is dovish, leading to a big pop in the S&P 500 following Powell’s appearance. While Powell said almost nothing new, he didn’t say enough to cause the market’s recent easing of financial conditions to reverse.

It was shocking to hear because at every point before November 30, when financial conditions had eased too much, Powell would push back against the market. But this time, he didn’t, and by not pushing back, he is telling the market he is okay with the recent easing of financial conditions.

The real question is why Powell would be okay with financial conditions easing. It is the exact opposite of what he has been saying about his desire to raise rates into restrictive territory.

Bloomberg

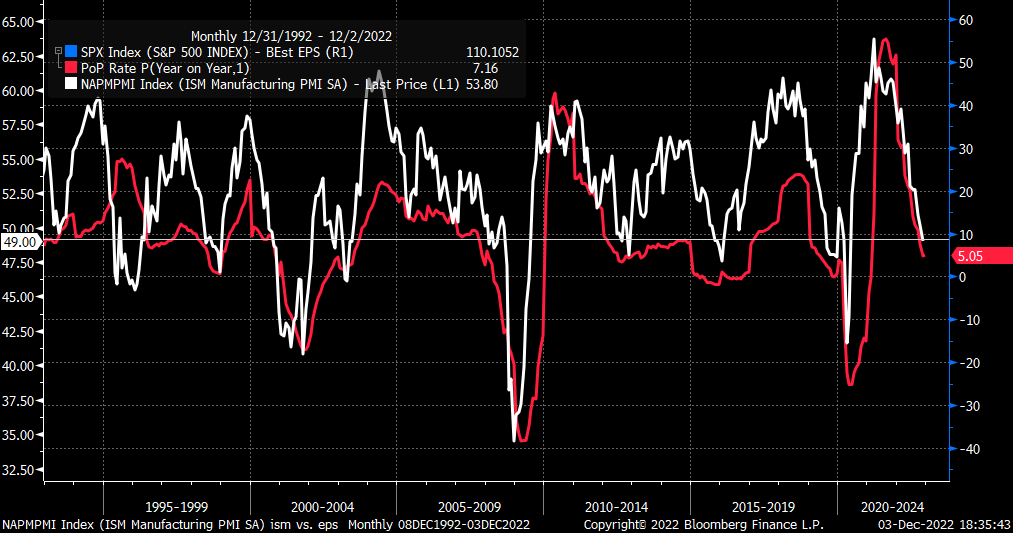

What is even stranger than that is that the jobs data on Friday showed stronger-than-expected non-farm payroll numbers. But, wages rose by 0.6% month-over-month, the hottest reading since January 2022. They also increased by 5.1% year-over-year, while last month’s numbers were all revised higher.

Meanwhile, the ISM manufacturing data was weaker than expected, suggesting the US economy is inching closer to recession. The ISM report noted that the reading of 49 indicated that the REAL GDP growth in the fourth quarter was around 0.1%.

The move in the ISM report indicates that S&P 500 earnings growth could turn lower in 2023 and perhaps go negative. The relationship between the ISM manufacturing survey goes back a long time, and they, too, tend to track each other very well.

Bloomberg

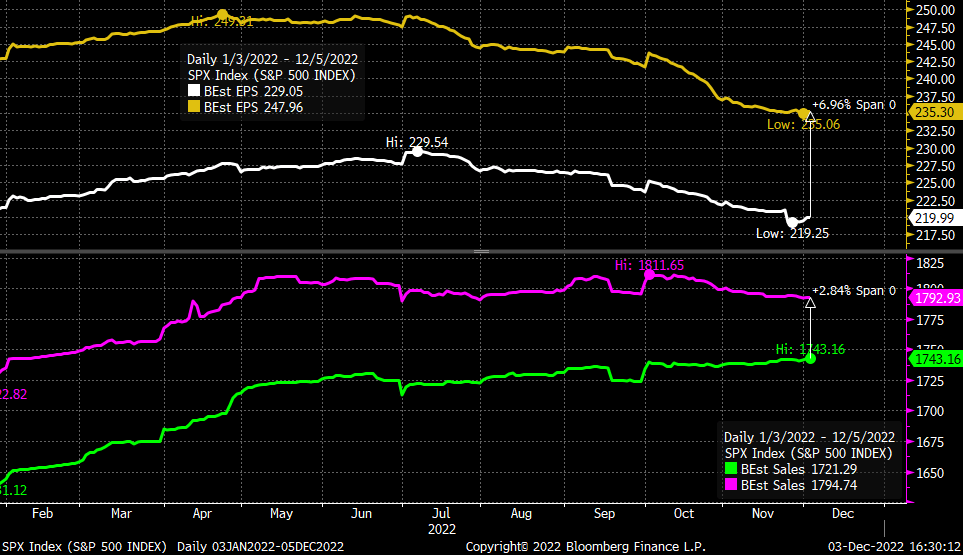

The slowing growth and higher wages suggest the recent changes in attitude from the bond market. The data suggest the economy could be very close to or is in a recession, which is likely to squeeze margins for companies and earnings. Earnings estimates do not reflect margin compression and are still pricing a lot of margin expansion.

Analysts’ estimates suggest that earnings in 2023 are expected to grow by around 7%, while sales are expected to rise by about 3%. Currently, analysts’ estimates are pricing in margin expansion in 2023. For there to be margin expansion, costs will need to be reduced; otherwise, earnings estimates are too high and need to be slashed.

Bloomberg

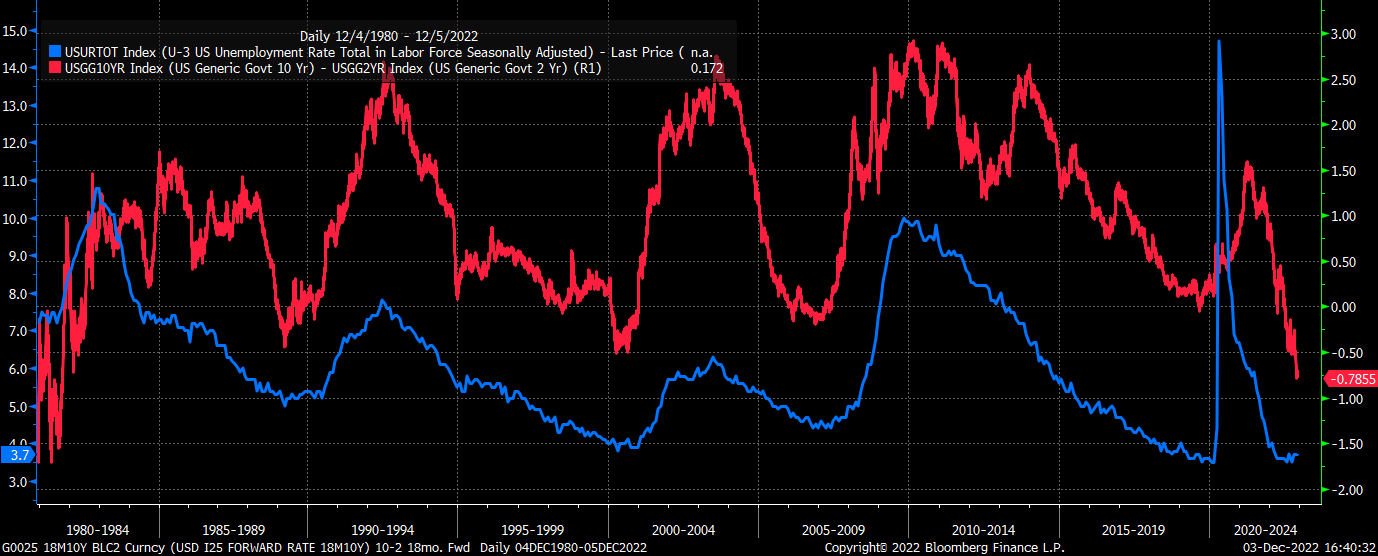

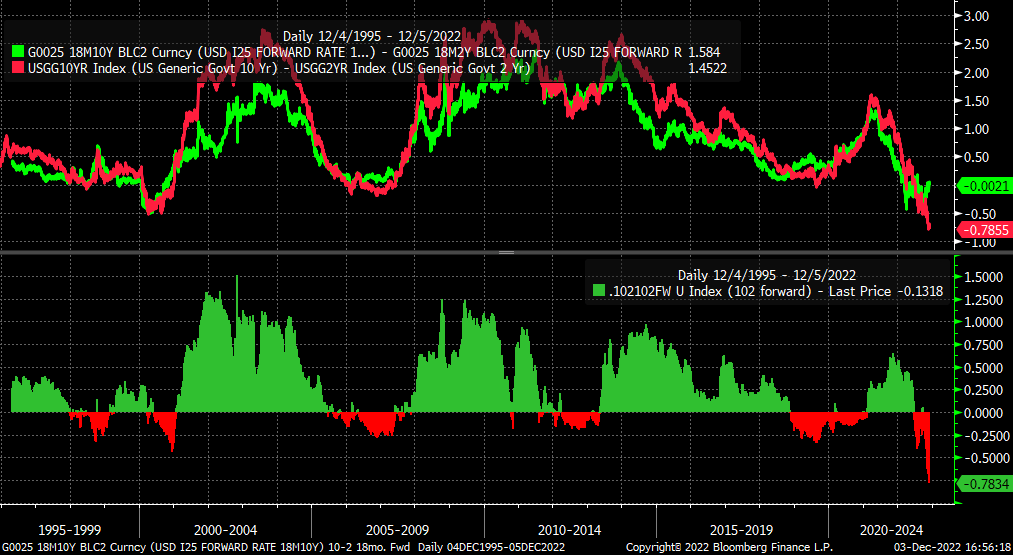

Cutting costs usually starts with letting workers go, and the best gauge for the unemployment rate may be the spread between the 10-year and 2-Year Treasury yield spread. In recent times the spread between the 10-year and 2-year yield tends to rise just before the unemployment rate starts to increase as the market anticipates the eventual rate-cutting cycle the Fed is about to embark on.

The current inversion is the deepest it has been since the early 1980s, and it tells us that unemployment is likely to stay low for some time longer. The current yield curve inversion has even stopped falling yet.

Bloomberg

But the yield curve inversion that has started to turn higher is the 10-year minus 2-year 18-month forward curve. This forward curve tends to lead the 10-2 year nominal curve by 6 to 12 months, and currently, that forward curve has returned to a neutral level near 0% as the nominal 10-2 yield curve is trading well below the forward curve.

Bloomberg

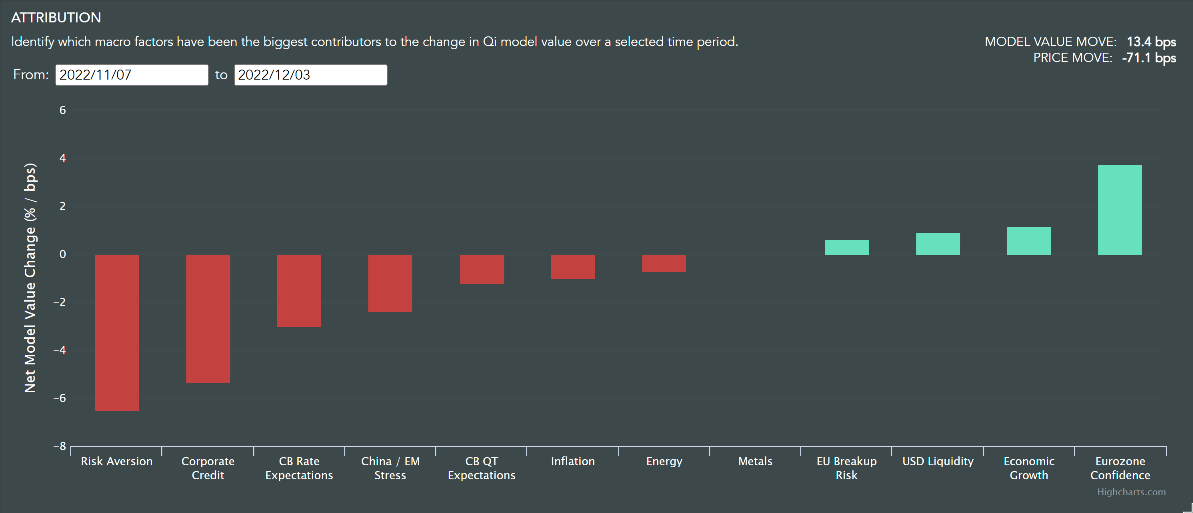

The forward curve suggests that the unemployment rate may be significantly higher over the next six months as companies look to shed the rising cost of wages as the economy slows. The data from Quant-Insight shows that the biggest drive in the recent move lower in the 10-year rate is risk aversion. An indication that the market is getting much more cautious and shifting into a risk-off regime.

Quant-Insight

Should the dollar continue to weaken and rates continue to fall, it would suggest that risk-off is taking hold. Eventually, the equity market will catch on to the risk-off sentiment, and that bad news is, again, bad news.

Be the first to comment