da-kuk

As we enter a new year, I’m in a mood to check some of my earliest work to see how things worked out. In particular, I want to write about companies where my advice offered people the opportunity to make outsized risk adjusted returns, because, as you should know by now, I’m an inveterate braggart. Anyway, I think my “switch to calls” call on Rapid7 Inc. (NASDAQ:RPD) fits the bill. Way back in the Fall of 2018 I recommended investors who insisted on staying long here switch to calls in an article with the very unoriginal title “Rapid7: Switch to Calls.” I was cautious on this stock and since I wrote about it, the shares are down about 13% against a gain of about 32.7% for the S&P 500. I find this somewhat gratifying. In terms of the calls I recommended in lieu of stock, the stockholders did slightly better than the call holders, but the call holders earned their return with far less capital at risk. I think earning $12 on $4 at risk is better than earning $15 on $37 at risk. Anyway, now that the shares have come down in price, and the company has obviously published a great deal of financial data since I last reviewed the name, I thought I’d check back. I want to see if it makes sense to buy, hold, or sell by looking at the financial history here, and by looking at the stock as a thing distinct from the business. Also, I want to write about call options, because they are a great tool to use when going long companies like this. If a company is losing money, doesn’t show any signs of paying a dividend anytime soon, why would an investor not employ calls if they can get them at a reasonable price?

My regular readers know that I’m absolutely obsessed with trying to make their reading experience as pleasant as possible. One of the many ways I do this is by presenting a thesis statement near the beginning of each of my articles. I do this so an investor can get the highlights of my thoughts about a given company so they won’t then be obliged to wade through an entire piece. You’re welcome. There’s no need to throw around words like “hero.” Anyway, I think this stock is un-investable. I think this because the disconnect between revenue and net income remains as strong as ever. The more this company sells, the more it loses. Owners are compensated by whatever’s left after paying everyone else, so income is what matters, and this company has none. In spite of this, the shares remain very expensive in my view. This is a bad combination from my perspective. Thus, I myself wouldn’t waste capital here. That written, When I last presented a similar sentiment, the shares went on to hit a peak of ~$138 before crashing back to Earth. For that reason, you’d be forgiven for being skeptical of my “avoid” talk here. If you think history can repeat itself, and you want to go long here, I would strongly recommend buying calls in lieu of shares. These give you much of the upside at a fraction of the cost of shares.

Financial Snapshot

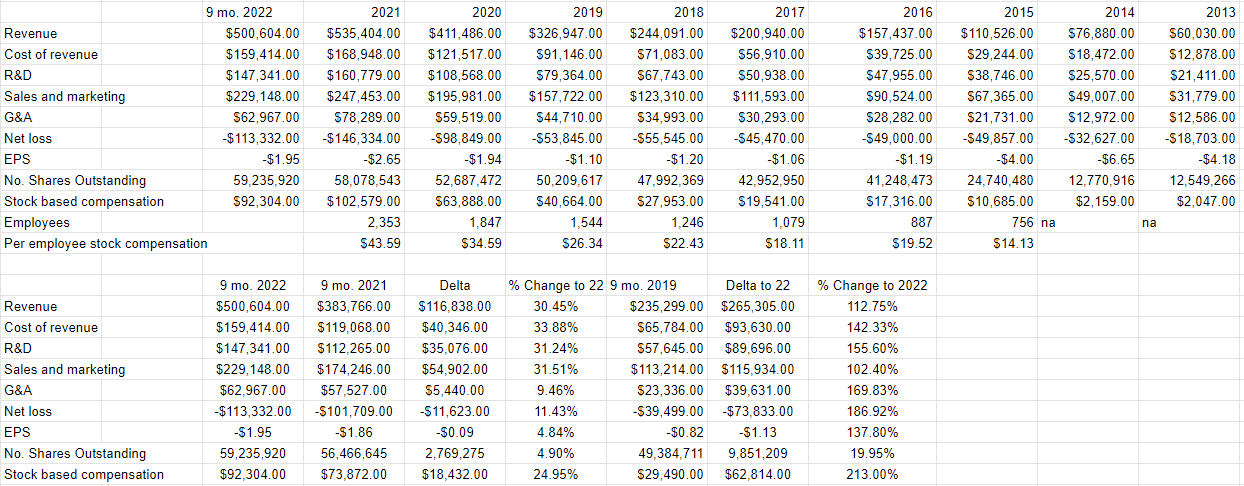

The financial story remains bad in my estimation. Specifically, revenue and net losses keep growing. In other words, it seems that the more this company sells, the greater are its losses. This is troublesome in my estimation, because owners of the company aren’t compensated by sales. They’re compensated for whatever’s left over after employees, landlords, and suppliers get paid. We also can’t forget that various governments need to wet their beak. I mean, they need a taste. Anyway, for the stats nerds out there, I ran a correlation between the revenue and net income. There is a very strong (r=-0.93) negative relationship between the top and bottom lines here. That is very troublesome in my view because it raises an uncomfortable question for the company. If growing sales won’t lead to profits, what will?

If you’re worried that the news is all bad at Rapid7, though, fret no further. One bright spot is that stock based compensation has grown at a CAGR of about 38% between 2015 and the end of 2021, while stock based compensation per employee has grown at a CAGR of about 17.5% over the same time period. So, shareholders may have been losing money at a rapid rate, at least we can all take some comfort in the fact that employees are being treated well. Additionally, as a refugee from a large software company myself, I assume that this stock based compensation is spread around very fairly at the organisation.

Zeroing in on the most recent period, the trends we’ve seen for years seem to be intact unfortunately. Revenue during the first nine months of 2022 was 30.5% higher than it was during the same period in 2021, while net loss has expanded $11.6 million, or 11.4%. Additionally, dilution is continuing apace, given that the shares outstanding has grown by 2.76 million, or 4.9% from the year ago period. Things look even more stark when we compare the first nine months of 2022 to the same period pre-pandemic. Revenue and net loss for the first three quarters of 2022 were higher by 112.75% and 186.9% respectively.

Another bright spot that I can write about in a less tongue in cheek manner is the capital structure. I’ll admit that the company has a relatively strong balance sheet. Specifically, cash and short term investments represent fully 30.7% of the value of the convertible notes on the balance sheet. Although this is a loss making machine, I think it has enough capital to survive for a few more years at least.

That written, in my view, in order to make this a worthwhile investment, the shares would have to be very attractively priced.

Rapid7 Financials (Rapid7 investor relations)

The Stock

If you subject yourself to my stuff on a regular basis for some reason, you know that I consider the “stock” and the “business” to be distinct from each other. The business sells an “insight platform” that enables their customers to improve cyber security. The stock is a speculative instrument that gets buffeted by a host of factors, some of which have nothing to do with what’s going on with the company. One of the things that affects the performance of a given stock, for example, is the crowd’s ever-changing views about the desirability of “stocks” as an asset class. There’s no way to prove this definitively, as it’s an obvious counterfactual, but it’s possible to make the case that some portion of Rapid7’s 69% decline over the past was caused by the S&P 500 dropping 17.5% over the same time period. The stock might also be impacted by the pronouncements of a fashionable analyst or, stranger still, the behaviour of central bankers.

So, this is why I consider the stock as a thing distinct from the business. The former is often a poor proxy for what’s going on at the company, and I think it’s possible to profitably exploit this disconnect. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. What I want to see in this regard is a stock that the crowd is somewhat pessimistic about that goes on to exceed expectations. When the crowd is pessimistic, the shares are cheap, which is why I try to buy only cheap stocks. Now, I consider this to be a fine investment at the right price, and I want to work out whether we’re near that price or not today.

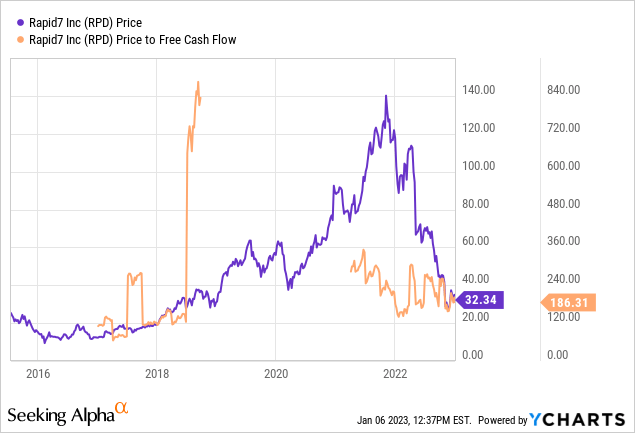

In my previous piece, in case you’ve forgotten, I suggested people stay away because shares were changing hands at a price to free cash flow of 613 times. Fast-forward to the present, and the shares are actually much cheaper on a price to free cash basis, but “cheaper” is certainly not the same as “cheap.” I think 186 times free cash flow is still morbidly expensive. In my view, either the stock has to fall further, or the free cash flow will have to explode higher. I think the former is far more likely.

Source: YCharts

Options As Alternative

When I last reviewed this stock, I made similar points. The shares were excessively priced, which was troublesome in light of the fact that this seems to be a perpetual loss maker. In spite of my problem, the shares went on to rise even further, indicating that just because I think something is too speculative to invest in doesn’t mean the market always agrees. Thus, I think it’s fair to suggest that the shares may very well rise in price from current levels, in spite of the awful financial performance and egregiously expensive shares.

So, if you’re one of the people who insist on taking a long position here, I think calls would be the best way to do that. In my previous missive on this name, I suggested that people who insisted on going long here manifest that perspective by buying call options in lieu of shares. Specifically, I recommended the May 2019 calls with a strike of $40, and call writers were asking $4 for these at the time. These were just under $3 out of the money and had about eight months of time value at the time I made the recommendation. On the day of expiry, the shares were trading at about $52, so they finished about $12 in the money. Over the same time period, the stockholder earned about $15, as the shares climbed from $37 to $52. Call holders did better on percentage return basis, even though they earned a slightly smaller absolute dollar return. This is obviously because the investor who bought the calls put up only about 11% of the capital that the stockholder did. So, in my view, earning $12 on a $4 investment is better than earning a $15 return on a $37 investment. In my view, having the option (pun intended) to participate in any upside while exposing yourself to much less risk is, by definition, a better way to “play” a particular investment.

With that in mind, I would recommend those of you who have the temerity to disagree with me about this investment manifest that perspective by buying call options. These offer most of the potential upside here, at a fraction of the risk. In particular, if I were to have a bullish perspective on this stock, I’d buy the August call with a strike of $35. This is currently priced at $5-$6.80. Even if the investor accepts the asking price, they’re still only putting up about 20% of the capital that the stockholder is, and, similar to the case above, has a great chance of capturing the vast majority of potential upside. If, as I suspect, the shares languish from current levels, the call owner will lose capital, but there’s a very real chance that they’ll lose far less than the stockholder. So, if you insist on buying this company that seems to lose more the more it sells that’s trading at 180 times free cash flow, I’d do so with calls.

Be the first to comment