The CAC 40 is the most influential benchmark of performance in the French economy. It is a stock market index, which was founded back in December 1987. It contains the top 40 French stocks operating within the Euronext Paris. It’s the primary securities market in France, and Europe’s second-biggest exchange after the London Stock Exchange in terms of market capitalisation. For those looking to get a barometer of performance in the world’s fifth-largest economy and across the continent, the CAC 40 index is an excellent starting point.

Current factors affecting the CAC40

{kind=link}

Think of the CAC 40 in the same terms as the Dow Jones Industrial Average used in the US stock market. The index selects the leading French stocks ranked by value and market capitalisation – more on them shortly. The CAC 40 tracker is named after the Compagnie des Agents de Change (CAC) – the organisation which first launched and managed the Paris Stock Exchange in the early 19th century.

The CAC’s history with financial trading dates back considerably further than this. In fact, there are records of it handling stock trades as far back as the 16th century. Its officially licensed brokers undertook trading activities on the Paris Stock Exchange for centuries until the dissolvement of the CAC as a consequence of the new Stock Market Reform Act, passed in January 1988.

The CAC was quickly replaced with an incorporated Societe des Bourses Francaises, which was deployed to monitor and operate the Paris Stock Exchange, at least until the merger of the SBF with other leading European stock exchanges in Amsterdam, Brussels and Lisbon in the autumn of 2000 – the formation of the Euronext N.V.

Nevertheless, the tradition of the CAC in French financial trading endured in the form of a new national index labelled the CAC 40. It is known as a capitalisation-weighted index. The overall value of the index is influenced by the fluctuation of individual share prices listed within the CAC 40. Those with the highest market cap hold the biggest influence on the index overall. This is the same as other notable national stock market indices such as the FTSE 100 and the S&P 500.

The make-up of French listed companies in the Euronext CAC 40 is determined on a quarterly basis by the Index Steering Committee. The Conseil Scientifique conduct review meetings on CAC 40 companies every three months to rank their overall performance within the Euronext Paris. Each stock is given a ranking based on their free market capitalisation and share turnover in the previous 12-month trading window. The Conseil Scientifique then hand-picks the top 40 performing companies form the Euronext CAC 40 index. This provides an accurate benchmark for French corporations, given that most stocks included in the CAC 40 are domiciled in France.

Interestingly, former French president Jacques Chirac remarked during a speech in 2010 that almost half (45%) of all listed shares within the CAC 40 are owned by overseas investors. A figure that is more than any other major European index. This is an indication that many of these French corporations are multinationals and don’t focus exclusively on the domestic market.

The top 10 companies in the CAC 40

Below, we’ve provided a snapshot of some of the leading publicly listed corporations and industries included in the CAC 40 at the time of writing. This should help you get a feel for why the CAC 40 index has such a multinational appeal among financial traders:

Market cap: $228.9bn as of August 2020

Annual revenue: €53.65bn as of December 2019L

VMH is short for Louis Vuitton Moet Hennessy. This corporation specialises in luxury goods across the spectrum, including fashion, cosmetics and fine wines and spirits. Although it is headquartered in Paris, LVMH has a string of subsidiaries that operate all over the world, managing a total of 75 illustrious brands. All of which contribute to the overall annual revenue of the corporation, displayed above.

Market cap: $180.7bn as of August 2020

Annual revenue: €29.87bn as of December 2019

L’Oreal is a major component of the CAC 40 index. For well over a century, the Clichy-headquartered corporation has been the most influential cosmetics firm on the planet. With over 88,000 employees specialising in skin and hair care, as well as perfumery, its subsidiaries like Maybelline, Garnier and Lancôme are household names in all four corners of the globe.

Market cap: $100.3bn as of August 2020

Annual revenue: $176.3bn as of December 2019

Established in the fallout of World War 1, Total was formed in March 1924 under the guise of ‘Compagnie Francaise des Petroles’ (CFP) – the ‘French Petroleum Company’ in English. Although CFP – which rebranded to Total in 1985 – started out as a French-focused oil company, it has since acquired stakes in multiple ventures and is now regarded as one of the world’s seven ‘supermajor’ oil corporations.

Market cap: $128bn as of August 2020

Annual revenue: €37.6bn as of December 2019

The original limited company of Sanofi was established in 1973 and, despite a merger with Aventis in 2004, the French multinational continues to sit at the top table in terms of pharmaceutical research and development, both in terms of prescription and over-the-counter treatments. It has been working towards Phase 1 of clinical testing of a possible COVID-19 vaccine, which could be approved for emergency use in 2021.

Market cap: $63.8bn as of August 2020

Annual revenue: €70.4bn as of December 2019

Airbus’ CAC 40 inclusion is of little surprise, given that its operating head office is in Toulouse, France, and it is the world’s biggest manufacturer of airliners. The corporation’s core civil aeroplane manufacture business is carried out under the umbrella of its French corporation Airbus S.A.S. Its shares are not only traded as part of the CAC 40, they are also available on the German and Spanish stock markets.

Market cap: $73.1bn as of August 2020

Annual revenue: €15.9bn as of December 2019

The brainchild of Francois Pinault, this luxury retailer has expanded immeasurably in recent decades, securing controlling stakes in some of the biggest retail brands in Europe, notably Gucci and Yves Saint Laurent. Today, Kering has a distinct focus on sustainability as well as luxury goods. It is not afraid to acquire brands all over the globe, with China’s Qeelin brand secured in 2012 and the British Christopher Kane brand bought out in 2014.

- Hermes International (EPA: RMS)

Market cap: $86.2bn as of August 2020

Annual revenue: €6.88bn as of December 2019

One of the most respected high fashion brands to come out of France, Hermes was established in 1837 by Thierry Hermes. Forbes Magazine ranked it as the 33rd most valuable brand on the planet in 2019. This is no surprise, considering that Hermes also has a 35% stake in the iconic Jean-Paul Gaultier French fashion house.

Market cap: $52.06bn as of August 2020

Annual revenue: €55bn as of December 2019

A truly global French banking group, BNP Paribas is the biggest in the entire eurozone. Alongside Credit Agricole and Societe Generale, BNP Paribas is one of three French banks to adopt a multinational presence. Today, it operates across 72 nations and, in terms of overall assets, ranks as the eighth largest bank in the world. You’ll find BNP Paribas listed on the Euronext Paris and the Euro Stoxx 50 index, as well as the CAC 40.

- L’Air Liquide (EPA: AI)

Market cap: $76.8bn as of August 2020

Annual revenue: €21.9bn as of December 2019

Industrial gas giant L’Air Liquide started out at the beginning of the 20th century following innovation from Georges Claude. Although its primary headquarters remain in Paris today, Air Liquide also has sizeable divisions worldwide, including Japan, America, China and the United Arab Emirates. It’s now the world’s second biggest supplier of industrial gases in terms of annual revenues.

Market cap: $48.39bn as of August 2020

Annual revenue: €124.9bn as of December 2019

Founded over two centuries ago, this financial services corporation has expanded immeasurably in the last 50 years, thanks largely to multiple acquisitions including Compagnie Parisienne de Garantie, the Drouot Group and The Equitable. The insurer rebranded as AXA in 1999. At the turn of the previous decade, AXA was dubbed one of the most influential multinationals based on its corporate control over financial stability worldwide.

Many of the above companies have been a part of the CAC 40 index since the outset, due to their importance and value to the French, European and global economies. Of course, it’s not always been plain sailing for these corporations and the CAC 40 index as a whole. Given that the business activities of the above companies are largely outside of France, they are often vulnerable to economic, health and political headwinds felt throughout the continent and elsewhere in the world.

The following factors have had an influential impact on the overall value of the CAC 40 in the 33-year history of the index:

Economic booms

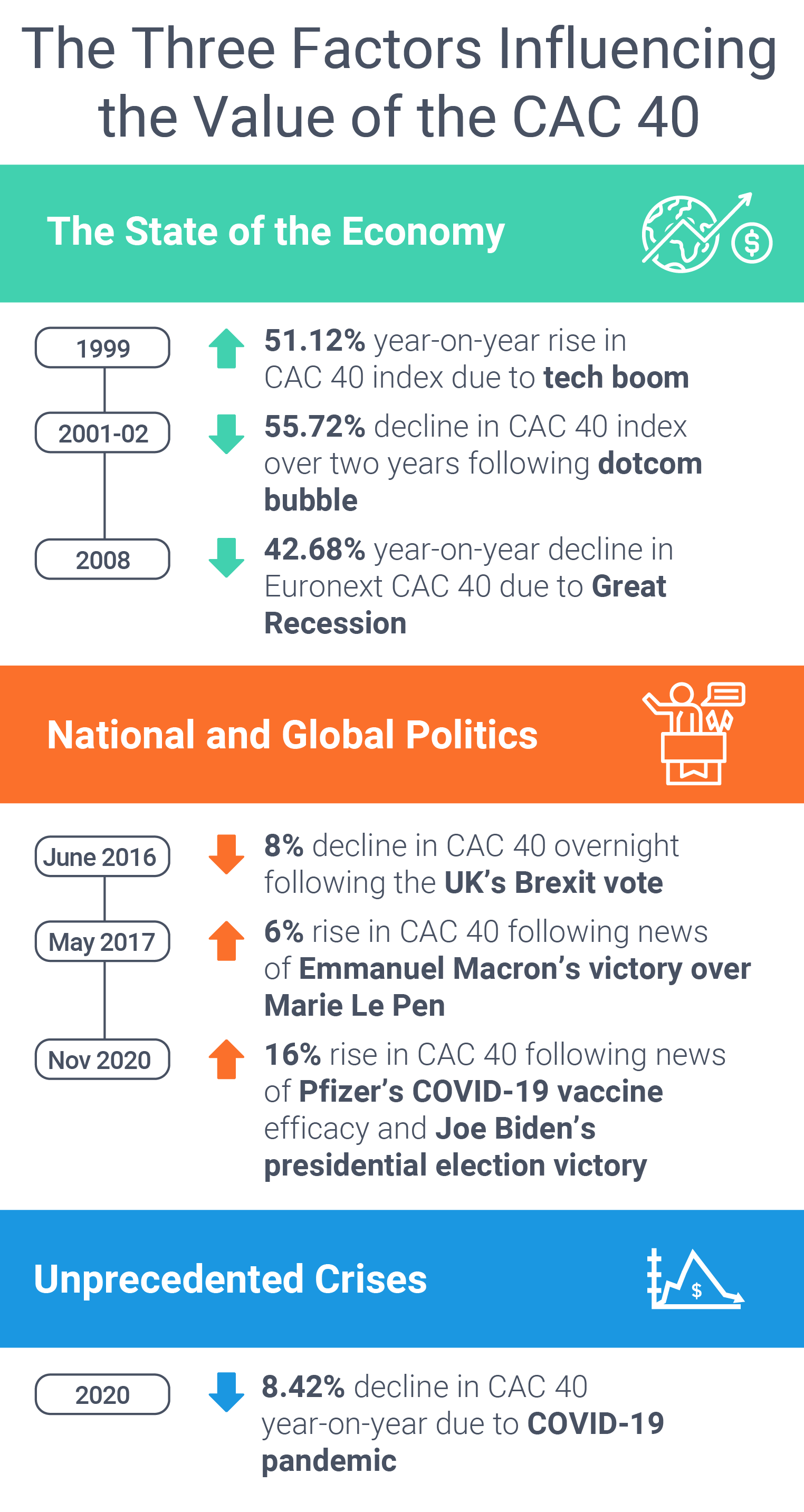

When the going is good with the national and global economy, the CAC 40 fares well. In fact, the CAC 40 reached its all-time-high value around the time of the dotcom bubble in September 2000. The bubble was generated following immense financial speculation from investors in internet-based corporations, given the surge in adoption of internet technologies. The CAC 40 followed suit with other major indices like the Nasdaq Composite, with many of the top 40 multinationals listed on the Euronext Paris capable of making their mark online along with the US ‘Silicon Valley’ upstarts.

It’s also worth noting that the CAC 40 has proven to be particularly influenced by the policies set by the European Central Bank (ECB). The ECB differs to other central banks like the Bank of England as it defines the monetary policy for the entire eurozone. Subsequently, the strength of the euro can underpin or weaken the value of the CAC 40. A strong, competitive euro against other major currency pairs is a green light for multinationals within the CAC 40, enabling them to import more cheaply from nations outside the eurozone. Conversely, a weaker euro increases the competitiveness of French exports and those sold anywhere else from within the eurozone.

Seismic political changes

The financial markets and multinational corporations appreciate stability. It’s the watchword for most bullish stocks. Therefore, when a nation experiences a period of political instability or the potential for a major change in power, it’s no surprise that indices like the CAC 40 experience uncertainty and volatility.

When we talk about seismic political changes, we’re primarily talking about a marked change in ideology. It’s the threat of one political party’s fiscal or monetary policy being usurped for another’s policies which sit at the other end of the spectrum. The most relevant case of politics having a major impact on the CAC 40 was the 2017 presidential election in France, which became a straight fight between Emmanuel Macron and Marie Le Pen. It took some time for the financial markets to accept that the far-right-wing contender Le Pen had a credible chance of becoming France’s next president. As Le Pen’s popularity grew, so too did the instability and underperformance of the CAC 40, which was considerably lightweight compared to the German DAX index.

The reason being that Le Pen’s political standpoint was to remove France from the European Union over time and adopt a more nationalist approach to the French economy. There were fears that the markets would riot in this scenario, with the CAC 40’s multinationals having to battle with the increased bureaucracy of trading on new terms with the rest of the EU. As it turned out, Emmanuel Macron was the eventual winner, which resulted in a period of renewed stability for the CAC 40.

Unforeseen national and international crises

Arguably the first major international crisis to strike in the history of the CAC 40 was the 2008 global recession. Back in 1929 when America’s Wall Street Crash hit hard across North America, the Paris Bourse was rather less affected, highlighting just how independently the two stock markets operated almost a century ago. Wind the clock forward to 2008 and the aftershocks of the Lehman Brothers’ collapse were felt far more severely in the CAC 40, given that the markets are far more integrated based on the rise in French multinationals.

It would also be remiss not to mention the implications of the ongoing COVID-19 global pandemic on the CAC 40 tracker at the present time. In fact, the fall in the value of the CAC 40 index was greater in the first few weeks of France’s self-imposed coronavirus lockdown restrictions than the initial decline post-Lehman Brothers collapse in September 2008. With profit expectations and forecasts being slashed significantly by a string of CAC 40-listed corporations, it’s little surprise that the index has fared badly as a result.

The COVID-19 pandemic also played its part in this year’s oil crisis, with global demand for fuels and crude oil falling off a cliff. Lockdown measures paused manufacturing, while a global downturn in air travel also eroded confidence in the industry further. The sharp decline in oil and gas prices harmed Total, one of the CAC 40’s biggest corporations in terms of market cap, so it’s easy to see why global crises affecting specific industries can also move the CAC 40 needle and indeed the CAC 40 future price.

How do these external factors rank in terms of impact?

Of the three major external factors that the Euronext CAC 40 is sensitive to, which one is most likely to have a damaging impact on the index long-term? Below, we rank the potency of each external factor on the CAC 40 index from the least influential to the most influential:

1. Seismic Political Changes (least influential)

How the French economy should be handled is one of the biggest talking points in the lead-up to a French presidential election. There is no doubt that investors in leading French multinationals within the CAC 40 look to the political agendas of respective candidates to decide where next to invest. The outcome of a political election can often be a turning point for the outlook on stock indices like the CAC 40.

We’ve already touched on how the potential of a far-right, nationalist president in the shape of Marie Le Pen caused uncertainty amongst the CAC 40 multinationals, but what was the impact of president Macron’s success in the May 2017 election?

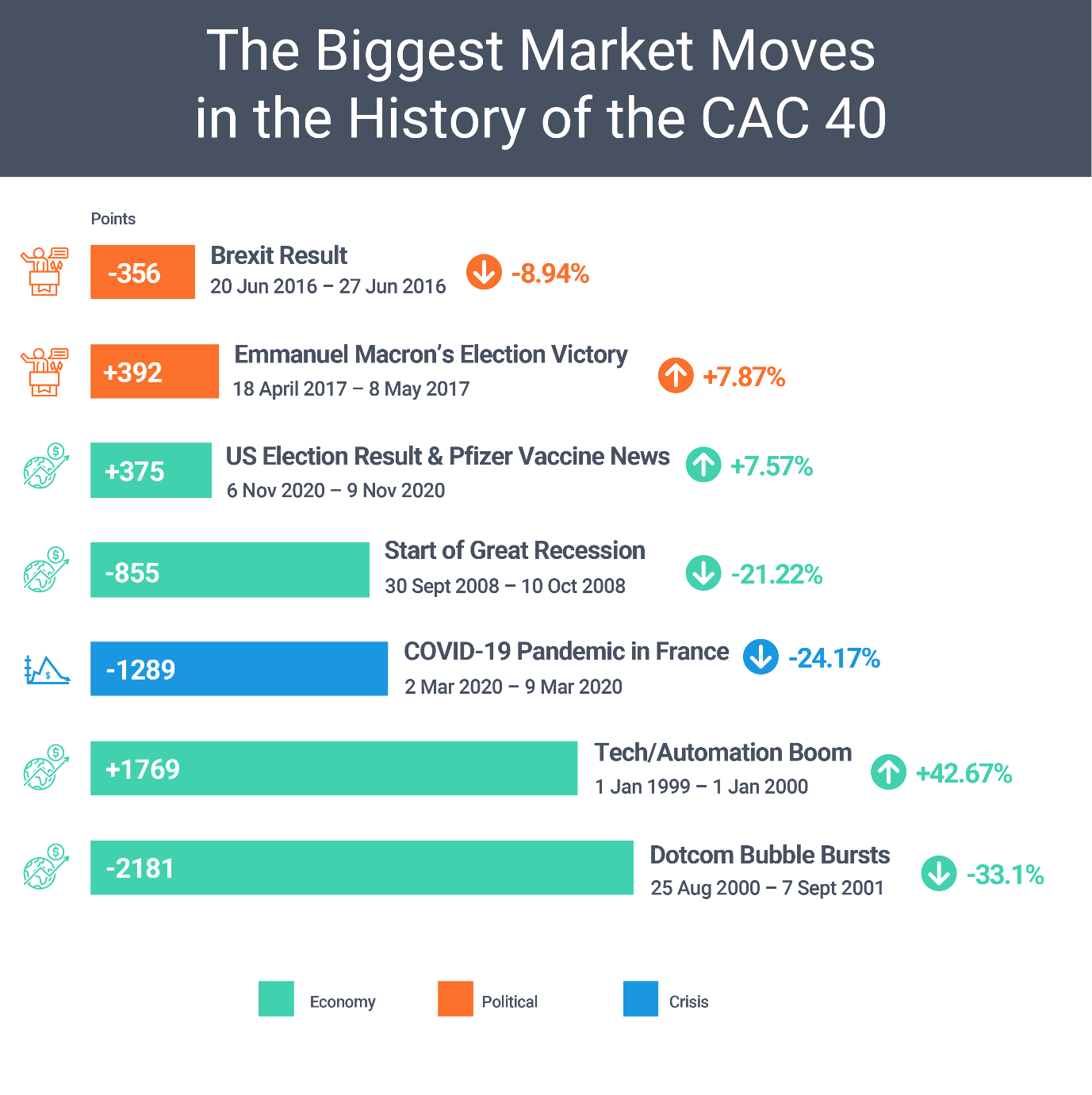

Prior to the first round of voting in the 2017 election, an influential pollster called that centrist Emmanuel Macron was the most likely candidate to win. This was following weeks of reports suggesting that Eurosceptics Marine Le Pen and Jean-Luc Melenchon were garnering support across the country. The biggest fear in the financial markets was a run-off between Le Pen and Melenchon on 7 May, which would result in a major sell-off in French bank stocks, as well as government bonds.

In the two weeks surrounding Macron’s run-off against National Front leader Marie Le Pen, the CAC 40 price surged by 6%, reaching its highest point in nine years. It was up a whole percentage point on the day of Macron’s victory too. Yet the positivity surrounding the CAC 40 was short-lived, with French stocks plateauing on the basis of Macron’s likely inability to implement his reform agenda.

The CAC 40 index even rose by 2.4% between November 3-4 on the news of Joe Biden’s recent victory in the US presidential election, combined with the positive news surrounding the Pzifer vaccine. With several French multinationals having a presence stateside, the new centre-left administration’s approach to tackling the coronavirus crisis will help these brands to regain their footing. However, the rise in the CAC 40 is also due to the impasse in the Congress, preventing the Democrats from fully implementing their suite of new tax and regulatory proposals.

2. Unforeseen National and International Crises

The COVID-19 pandemic is one of the biggest global challenges in the last century. It was inevitable that the necessary lockdown restrictions would result in recession for 2020. In France alone, the OFCE believes the initial nationwide lockdown led to a decline of 32% in GDP. In February 2020, the Euronext CAC 40 was priced at highs of 6,111. By the time President Macron was forced to announce a nationwide lockdown a month later, around 39% of the value in France’s top 40 corporations had been wiped out.

March 12, 2020 saw the most substantial fall in the history of the Paris Stock Exchange, by some 566 points. In fact, the initial plunge in the value of the CAC 40 index was sharper than the one felt by the collapse of the Lehman Brothers, which sparked the 2008 global recession. Although the short-term impact of COVID-19 on the CAC 40 ranking was more severe than the 2008 recession, the reality is that this is a health and economic crisis rather than a banking crisis.

According to data from the OFCE, profit expectations among CAC 40 companies for 2021 had been cut by 13.4% between February-May 2020. Yet the CAC 40 index was down as much as 39% at one time during this period, suggesting something of an overreaction in the market. At the time, coronavirus was still a very new disease and vaccines were a distant prospect.

Furthermore, the decline in the index had also priced in additional geopolitical headwinds, including the oil industry’s price crash, which saw Total SE’s share price more than halve from €50 in January to a low of €21 in mid-March.

Like the Total share price, the CAC 40 index has demonstrated signs of recovery in recent months, based largely on the positive predictions of effective vaccines being ready for mass implementation by the end of 2020, and talk of normal life returning by the middle of next year. It has rebounded from its March low of 3,754 to 5,476 on November 19 – a recovery worth around 31% of the index’s overall value.

3. Economic Boom and Bust (most influential)

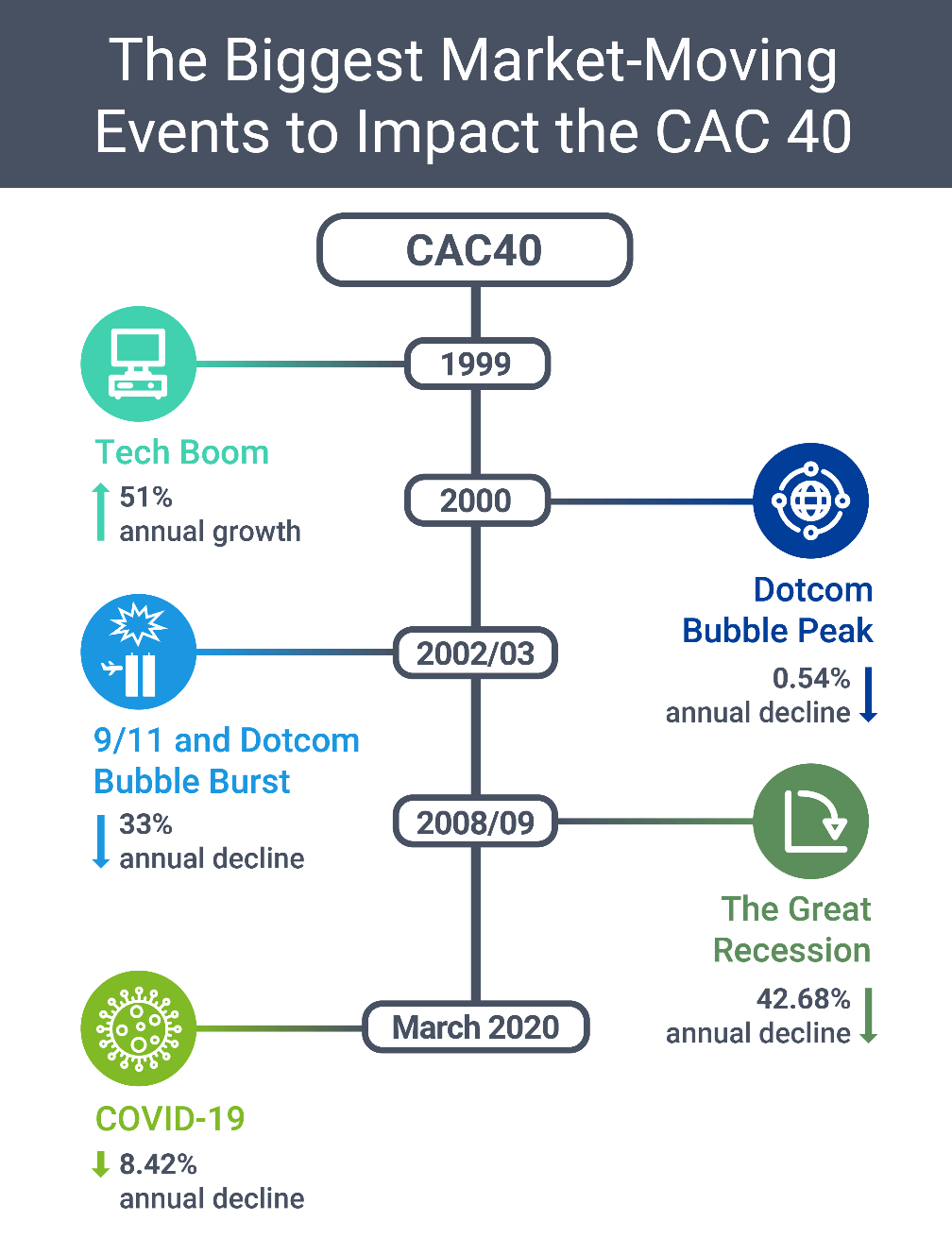

Over the years, the CAC 40 index has moved in a similar vein to other major stock indices across the world, most notably the German DAX and the British FTSE 100. All the leading indices were enjoying tremendous growth around the turn of the new millennium, buoyed by a wave of tech automation and the mainstream emergence of the internet. Between 1999 and 2000, the Euronext CAC 40 was up by over 40%, scaling all-time highs of 6,922 in July 2000.

Despite the massive positivity surrounding the internet boom, the so-called ‘dotcom bubble’ burst in 2001, with many of the tech stocks listed in indices such as the US Nasdaq going to the wall. Even well-established blue-chip tech giants like Intel lost around four-fifths of their value at the time the bubble burst. The ripple effects were felt in the CAC 40 also. This, along with the fallout following the terrorist atrocities of the 9/11 attack in New York, saw the CAC 40 decline by over 38%.

In the UK, the FTSE 100 index was down by 31.3% in 2008, when the Great Recession of 2008 struck. The CAC 40 followed suit, registering a more damaging decline of 43% during 2008 – its worst run in its 20-year existence. Trillions of dollars were wiped off share values, including those in the CAC 40. LVMH saw its share price halve by the end of 2008.

What are the biggest issues to have ever affected the French economy?

For the full picture of the French economy and the CAC 40 index since its launch in 1987, we’ve put together a timeline of the key fundamental events that have influenced the rise and fall of the CAC 40 and France’s most integral multinational corporations:

- 1999 – index buoyed by the arrival of automation (up 29%)

The 1990s and the dawn of the new millennium was a breakthrough era for machine automation and artificial intelligence. We’re not just talking about NASA’s first automated robots on Mars either. The late 90s saw automation and AI become fully intertwined with business process management.It was starting to have an impact with some of the leading French multinationals in the CAC 40 too. Renault, which has long been France’s biggest car manufacturer, received investment in its robotics automation subsidiary from Comau. The deal helped improve efficiencies in terms of chassis and mechanical assembly for Renault and the Fiat Group, with Comau the subsidiary for Fiat’s manufacturing apparatus. Within six months of the deal, Renault’s share price had risen by over 65% to over €53.

- 2000 – all-time highs achieved during the ‘dotcom bubble’ (up 12.5%)

Like the NASDAQ composite and other major stock indices, the CAC 40 enjoyed a boom period around the turn of the millennium, as the dotcom bubble took hold. Both the NASDAQ and the CAC 40 spiked in 2000, with the CAC 40 reaching an all-time high of 6,922.33. This price point has yet to be surpassed some 20 years on.At the height of the dotcom boom, high-potential start-ups could go public with an initial public offering and secure substantial sums of investment without even having made a cent in revenue. In fact, losing money was the hallmark of a dotcom start-up with high-growth potential in the eyes of some giddy investors.

- 2002/03 – ‘Dotcom bubble’ bursts and the global fallout from 9/11 (down 38%)

Unfortunately, too many dotcom start-ups burnt through their capital too fast, causing rising panic in the stock markets. Even the biggest and most established tech brands including Dell and Cisco were entering sizeable ‘sell’ orders into the market. The mass panic which ensued caused the bubble to burst, with the stock market losing over a tenth of its entire value in a matter of days.The market capitalisation of so many promising tech stocks had diminished to such an extent that they were eventually worthless. By February 2003, the CAC 40 index had fallen from its all-time high of 6,922.33 down to just 2,754. It was a more gradual decline than the NASDAQ, but it was a decline nonetheless. The markets were not only dealing with the dotcom bubble bursting. They were also coming to terms with the geopolitical fallout from the 9/11 terrorist attack in New York City.

- 2004-07 – steady economic recovery underpinned by domestic investment (up 42%)

The four years after the global fallout from 9/11 and the dotcom bubble were a period of consistent growth, as major CAC 40 stocks solidified based on improving exports and fresh investment in the French economy.In fact, much of this fresh investment was derived from foreign investors, with around 50% of the CAC 40 index held overseas.

- 2008-09 – index hit by 2008 recession’s subprime crisis (down 43%)

By the summer of 2007, the CAC 40 tracker had almost retraced its steps to pre-dotcom bubble levels. It had peaked again at around 6,117, but disaster was only a matter of months away for the global economy. 2008 saw the Great Recession rear its head, with the US subprime crisis affecting all four corners of the globe.The crash of major stock indices outside the US underlined the increasing globalisation of all the leading stock markets, with the growing number of French multinationals in the CAC 40 more likely to be affected by headwinds outside Europe.

- 2013 – CAC 40 surges despite ongoing recession in France (up 11%)

In May 2013, the French economy entered its second recession in four years, with Q1 2013 recording a 0.2% contraction – the same contraction experienced in Q4 2012. Yet, despite record unemployment and flagging business confidence, the CAC 40 index performed admirably well during this year.This year is further proof that the CAC 40 was becoming a more accurate barometer of the global economy, rather than the French economy exclusively. With other major stock indices like the NASDAQ experiencing sustained growth during 2013, so too did the CAC 40, underpinned by its multinationals.

- 2018 – return of global volatility in the markets (down 12%)

Comparing year-end values for the CAC 40 index between 2017 and 2018 revealed a 12% year-on-year decline. It marked the first year of a sustained decline in the market cap of leading CAC 40 stocks since 2011. The return of volatility to the stock markets was largely due to rising interest rates in America and the continued trade war between China and the US – the world’s economic superpowers.At the end of 2018, overseas investors continued to own well over two-fifths (42.2%) of the total market capitalisation of CAC 40 companies, at a combined value of €557 billion.

- 2020 – onset of COVID-19 pandemic causes short-term pain (down 39%)

The arrival of COVID-19 in France and the rest of mainland Europe sparked the biggest daily decline of the Euronext CAC 40 in the index’s history. It fell by a staggering 566 points, which equated to a 13.7% fall in the space of 24 hours. The index plummeted for depths of 3,754 on March 18, a 39% fall from its February high of 6,111, with the continent’s lockdown restrictions taking hold.

The severity of the decline to CAC 40 was also due to the global oil crisis which ensued following the initial COVID-19 lockdown. Fortunately, the positivity surrounding the prospects of multiple coronavirus vaccines in 2021 and a return to a more normal way of life has helped French multinationals to plan for the next 12 months with a greater degree of certainty. As of November 2020, the CAC 40 has recovered around 80% of the value lost in March.

Be the first to comment