sefa ozel

The last 5 years have been an absolute rollercoaster ride for oil producers and refiners, within the space of 2 years we saw prices briefly turn negative as COVID lockdowns all but brought oil consumption to a standstill amid a glut in supply as Saudi Arabia and Russia faced off through OPEC, then prices rocketed back up to set new record highs as COVID-related supply constraints hit and Russia invaded Ukraine.

Unfortunately, for the oil industry, it appears the Fed is going continue to hike interest rates as it grapples with skyrocketing inflation, sending the US right into a recessionary environment, potentially setting off another consumption slump for oil.

So what should firms do to prepare themselves for a recession?

And more relevant to investors, how can we tell which firms are well prepared to face a recession, vs those who will need to make tough decisions and face downsizing or even closure, due to the changing nature of the business cycle? For investors looking to place their money into some of the top 100 US firms to de-risk their portfolios and invest in safer mega-cap stocks, I’ve created the Ranking Recession Readiness series to assist with differentiating safer firms from higher risk ones.

Ranking Recession Readiness is a series of articles I’m authoring based on academic research along with advice from business leaders who took their firms through the Great Recession of 2008, to help investors identify which top 100 US firms are positioned to strive through a downturn, and which firms will stumble.

This article will be looking at Exxon Mobil Corporation (NYSE:XOM), and considering how the oil giant is prepared to handle a recession, based on the advice from 2008.

A full breakdown of the methodology and explanation behind the calculations is available in my introductory article, Ranking Recession Readiness: Is Google Prepared For The Recession?

(Data & prices correct as of pre-market 13th July, 2022)

(The Top 100 US Firms referred to can be found on this Seeking Alpha screener)

Want to skip the articles and dive right into the data? You can download my data and calculations here and see how the Top 100 US Firms compare on Recession Preparedness

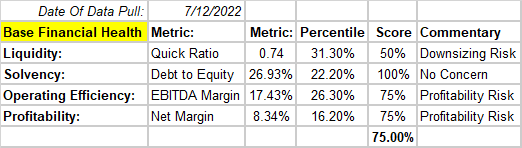

XOM’s Base Financial Health

First, we start assessing XOM’s basic overall financial health, looking across the firm’s liquidity, solvency, operating efficiency, and profitability. Here we get a good sense of how the firm is performing in today’s current climate, and if it is potentially heading into the recession with any concerning financial metrics.

Author

First off is the quick ratio, also known as the “acid test”. This is a worst-case-scenario metric looking at how a firm would be able to cover its debts should they be called on to pay them down quickly. Unfortunately, we see here a large gap between the business’ liquid assets and its debts, presenting a large risk compared to the rest of the top 100 US firms.

The firm’s debt to equity is not a concerning size in comparison to the top 100 US firms, with ~27% considered well below average for the peer group.

EBITDA margin and net margin are both quite low, though I’ll be lenient in only penalizing the metrics as profitability risks at this stage.

We round off the base financial health with a score of 75%, showing the firm holds a profitability risk in its current operations, but by no means is it at a major risk of downsizing or facing downsizing risks in today’s operating climate.

Next, we will look a little closer at XOM’s obligations and how they’re structured.

Author

Firstly, short-term debt is equivalent to 11% of XOM’s long-term debt, this ratio is within the largest 10% of ratios for the peer group, and while 11% is only a minor figure, it puts a strain on the firm’s finances as it works to service this debt. This however is offset by the firm’s 38X covered ratio, suggesting that the short-term debt is merely a profitability risk rather than a downsizing or operational risk. So we rate ST/LT debt as a profitability risk, and mark the covered ratio as a “no concern”. Lastly, the current ratio is considered low for the peer group showing the firm is running quite close to its limits, so we will mark that down as a profitability risk.

We now move on to XOM’s dividends and review how they are affecting the firm’s finances.

Author

While cash flow is excellent for the business and covers the firm’s dividends within normal bounds, we already know that XOM’s net margins are very low compared to the peer group and the earnings coverage of dividends presents a very large risk to the firm’s continued operations.

While this can be explained by a large earnings payout ratio, we need to score this in the context of the top 100 US firms.

Lastly, we move to the firm’s future financial outlook to consider what the future may hold for XOM.

Author

Revenue growth of 3.89% is low, and while we have been lenient up until now, we need to mark the outlook down given how skinny the firm’s margins are. With that said, we see earnings are expected to grow, and therefore, the implied net margin improvement is excellent at 300%, and gives us a good indication that the firm’s financial health is expected to improve.

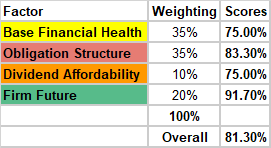

Finally, we bring all the scores together, weight them, and then get a sense of how XOM’s overall financial health looks.

Author

81.3% is passable, though it indicated there are more areas of risk compared to the top 100 firm’s peer group. I see the largest risks being the firm’s quick ratio, dividend affordability, and margins.

Now that we have a sense of how XOM is positioned heading into a recession, let’s take a closer look at the balance sheet and see how XOM is prepared to take on a downturn.

Assessing XOM’s Recession Preparedness

The advice from veterans of the 2008 Great Recession was to minimize debts before a recession hits, and to build a stockpile of cash that can sustain the business through a downturn.

Collating the relevant metrics for XOM, we paint the following picture.

Author

We immediately see the debts the business has accumulated, along with the cash stockpile meant to carry XOM through a recession. We know that XOM’s debt serviceability is very good, but let’s see what happens when we compare these figures to the top 100 US Firms list and assign scores to these metrics.

Author

XOM’s balance sheet, unfortunately, scores poorly when compared to the top 100 US firms list, and XOM earns a -11.77% recession readiness score, ranking it 48th in the peer group.

This score is mostly driven by significant ST/LT debts, low cash levels relative to debt, and a very poor quick ratio indicating the firm would struggle in a worst-case scenario for a recession.

However, this analysis of the balance sheet does not tell the whole story for XOM, so let’s look more closely at some more qualitative elements of the firm.

A Deeper Dive Into XOM’s Recession Readiness

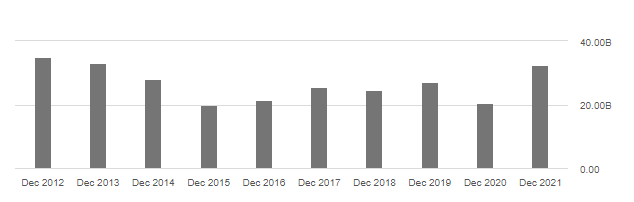

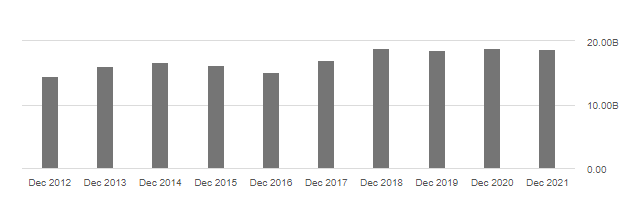

In the advice themes from the 2008 Great Recession, business leaders spoke about minimizing risk to customers’ financials by reducing accounts payable, and reducing inventory due to the cost of holding unsold stock.

Seeking Alpha

Here we see XOM’s accounts receivables have fluctuated, probably more to do with market cycles than internal operations. Total receivables in the most recent report sit at $42.14B, making up 54% of total current assets, and 11.87% of total assets, one of the highest ratios of receivables to current and total assets of all the firms I’ve written about so far.

Seeking Alpha

Inventory, meanwhile, came in at $22.17B in the MRQ, representing 28.7% of total current assets and 6.25% of total assets, again, very high ratios compared to other companies I’ve covered.

These two metrics combined represent 82.7% of total current assets and 18.1% of total assets, unfortunately, ratios that represent a large risk to the firm as these could very easily become areas of equity losses for XOM.

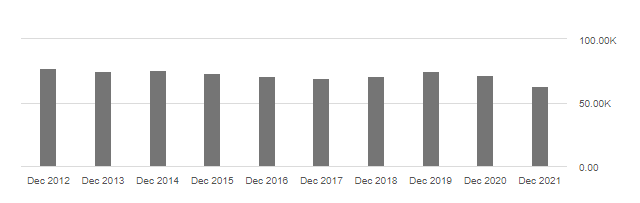

The next piece we look at in-line with advice from 2008 is related to employees. 2008 managers encourage very aggressive cost-cutting in the event of a recession, but recommended avoiding layoffs as after a recession ends, it is expensive to hire and train new employees, making a return to normal operations more expensive and more difficult.

Seeking Alpha

For XOM, employee counts have fluctuated, possibly in line with the market.

While we can’t predict exactly whether a firm would engage in layoffs during a recession, we can attempt to gauge a likely scenario of whether the firm would need to or not, based on revenue and profitability per employee.

With 63,000 employees, XOM derives $4,909,000 from each employee, and $421,000 in net profits per employee. This indicates that XOM is very efficient in generating revenue and income with its current staff levels, and shouldn’t necessarily require layoffs.

Finally, the last piece of advice from the 2008 Great Recession was that firms should consider investing in CAPEX during a recession, while the opportunity cost of capital is lower.

XOM would appear to benefit greatly from improved efficiencies from CAPEX projects, which would in turn improve overall profit margins; however, the capital required for projects for a firm the size of XOM may be too great, given the low cash balance on hand for the firm, and credit is likely to get tighter.

It’s difficult to say whether XOM could access the capital required for such projects, and so, therefore, I couldn’t give a clear answer on this front.

Closing Remarks

I largely consider XOM more exposed to the risks of a recession compared to its peers in the Top 100 US Firms list, largely due to its low quick ratio, low cash balance, tight profitability margins, and excessive exposure to risks associated with high levels of accounts receivable and inventory.

The Recession Readiness Score would indicate XOM is a HOLD at first glance, however, its qualitative aspects push my thinking toward a SELL rating.

Of further risk to investors, in the case of a recessionary scenario where XOM’s profits are severely impacted, there is a very real chance the firm may need to consider cutting dividends in order to maintain a healthy financial profile.

I note, however, that this article does not address in detail the current oil market situation, with the price of oil likely to remain elevated for some time, perhaps regardless of a recession.

I’d like to know your thoughts on how a recession will likely impact oil prices, while the Ukraine war carries on and OPEC struggles with increasing output.

If you have any questions or would like to see any particular Top 100 US Firms assessed for their recession readiness, please leave a comment and let me know (I always do my best to monitor and respond to genuine comments!).

Be the first to comment