Roman Tiraspolsky/iStock Editorial via Getty Images

In our last Ralph Lauren Corporation analysis (NYSE:RL), following the company investor day, we emphasized how we were expecting a 32% Market Cap Return Over the Next 3 Years. No sooner said than done, since September 2022, the company’s total return was 37.68% (including its quarterly dividend payment) outperforming the S&P 500 performance which was up by only 9.47%. In our initiation of coverage called The Polo Horse Starts To Gallop, our buy investment summary was supported by: 1) a positive outlook on the fashion sector thanks to an expected positive pricing delta versus raw material inflationary pressure, 2) a supportive free cash flow generation, 3) new platforms to engage a young clientele with initiatives such as ‘The Lauren Look‘ and 4) an ongoing buyback.

Mare Evidence Lab’s previous publication

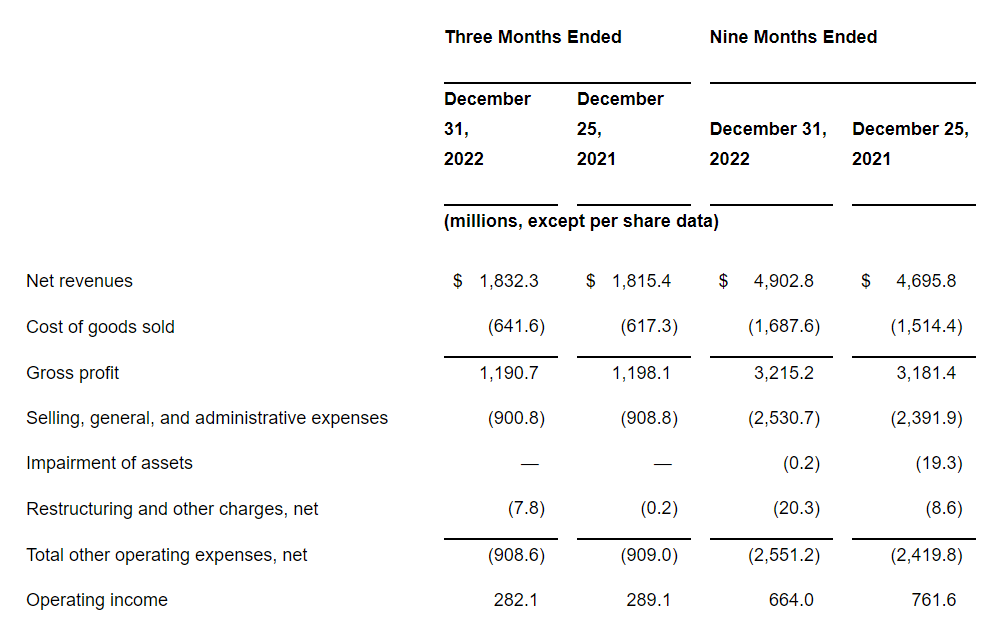

Looking at the company’s nine-month results, Ralph Lauren’s turnover increased from $4.69 to $4.9 billion. However, net income fell nearly by 15 percentage points from $575.5 million to $490.4 million. In the three months, top-line sales in North America grew by 1% to $938 million, while in Europe Ralph Lauren reached $469 million in revenue. There was also a slight improvement in Asia with a plus 1%, which rose to $386 million. Q3 gross profit stood at $1.2 billion with a gross margin of 65%. Going down to the P&L, the company’s operating margin reached 15.4%. During the period, foreign currency negatively impacted revenue growth by approximately 630 basis points. Here at the Lab, we are not surprised by the negative FX implication and on the contrary, we are positively impressed by Ralph Lauren’s profitability results. On a long-term basis, we were forecasting an operating profit margin of 15%+ for the 2025 numbers, reporting that this might be achieved at constant currency, but not at the current rate. In our internal estimates, we were expecting a minus 170 basis points on the company’s EBIT margin. However, as already mentioned, on a reported basis, the American fashion group delivered an EBIT margin of 15.4% thanks to discipline in its operating expenses (and beating Wall Street analyst estimates). During the call, the CEO also decreased its CAPEX forecast from a mid-point at $300 million to $245 million.

Ralph Lauren financials in a Snap

Related to our investment thesis, the company is continuing to deliver on the younger generation, looking at the press release, Ralph Lauren’s social media followers are exceeding 51 million with a positive trajectory. In addition, to support its stock price development while investing in strategic growth initiatives, the company returned $560 million to shareholders by combining its ongoing buyback and its quarterly dividend payment.

Ralph Lauren dividend and buyback

On the negative side, as also reported in Capri Holdings’ latest update, the company’s inventory reached $1.2 billion and was up by 33% versus last-year end quarter. Here at the Lab, we are currently monitoring this negative trend and we suggest to our followers check our “Implications Of Nike’s Profit Warning” analysis.

Conclusion and Valuation

The company reiterated its Full Year 2023 outlook on sales with growth >5% and an adj. EBIT margin of 13.5% to 14.0% in constant currency. This is very much in line with our internal estimates. On the 2025 outlook, despite some macro challenges, in the Q&A, the CEO confirmed its financial targets. Concerning the valuation, last time we slightly decreased our buy rating to $130 per share due to FX evolution and rising macro risks. Today, based on the latest accounts release, we fully confirmed our outperforming rating. The risk paragraph is already included in Mare Evidence Lab’s initiation of coverage.

Be the first to comment