Mongkol Onnuan

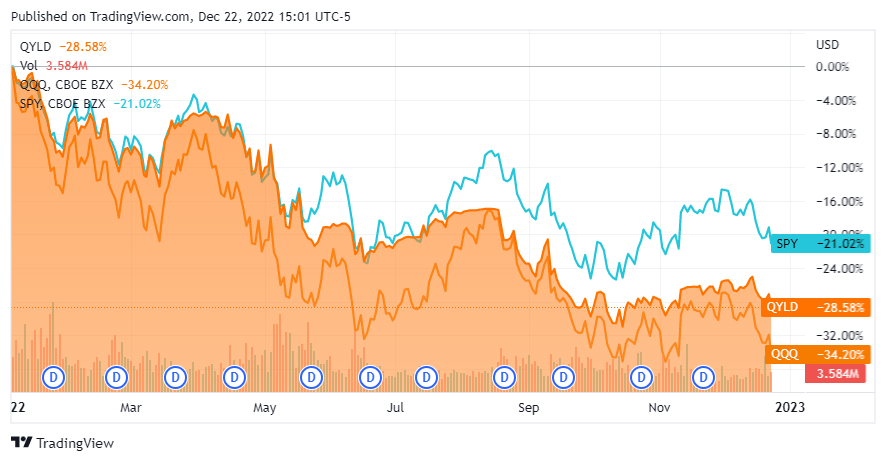

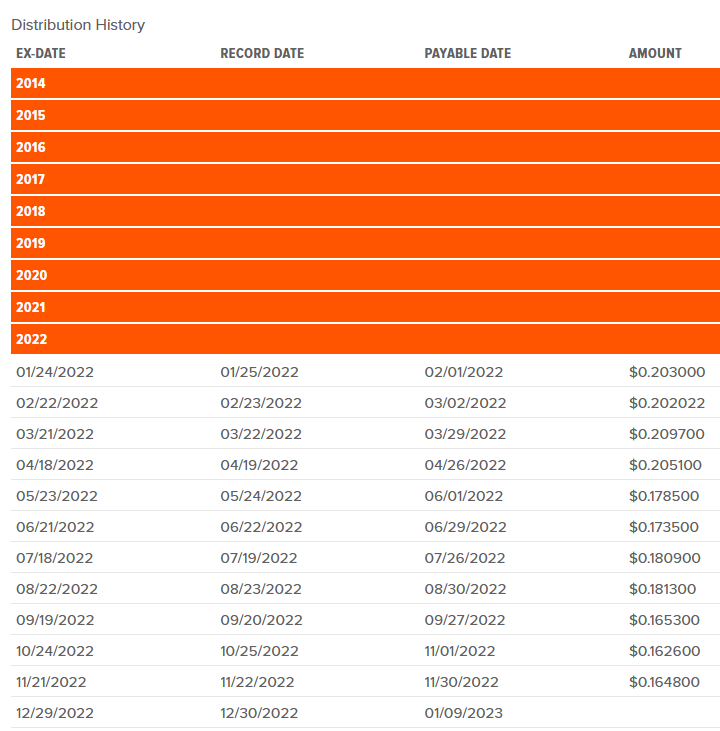

Some investors love the Global X Nasdaq 100 Covered Call ETF (NASDAQ:QYLD) for the large double-digit yield it pays, while others dislike the idea of capping the upside potential through writing covered calls. QYLD isn’t an investment vehicle that will meet everyone’s investment needs and is geared toward investors looking for a reliable stream of income. QYLD’s methodology is intriguing because its monthly distributions aren’t predicated on dividends or capital appreciation. Covered Calls are written on the asset base, and the premiums are paid to investors through monthly distributions. The S&P 500 is back in a bear market for the holidays, and the Nasdaq has fallen more than 34% YTD. Regardless of the macro indicators, the bottom line is that 2022 has been a bust, and many portfolios have seen better days. The silver lining for QYLD is that it continues to prove many of the critics wrong, as its mechanics haven’t proved to be riskier than the overall market. QYLD tracks the Nasdaq 100, which is represented by the Invesco QQQ ETF (QQQ), and has outperformed it by 5.62% while throwing off $2.03 across 11 monthly distributions in 2022. As the year winds down, QYLD will be going ex-dividend on 12/19/22 and paying its final 2022 distribution on 1/9/23. While 2022 has been a difficult investment environment, I believe it’s been positive for QYLD because we have seen that it will hold up in a bear market. The downside risk isn’t extrapolated past its relative index on a pure price methodology, and it will continue providing a never-ending income stream for its investors.

Seeking Alpha

QYLD has been a better place to hideout than big tech during the downturn

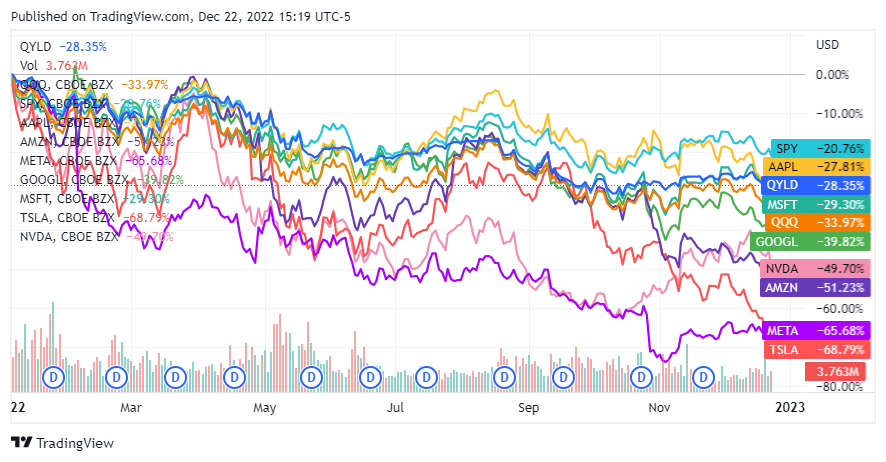

Big tech consisting of Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), Tesla (TSLA), and NVIDIA (NVDA) led the markets to new highs, then drove the market into bear territory. Buying the dip hasn’t worked, and investors who have held throughout 2022 have seen their portfolios decline in value. Regardless of the investment narrative that you want to believe, from a sector rotation out of tech to inflation and the Fed Funds Rate increase, it doesn’t change the fact that the most popular stocks are down between -27.81% to -68.79% in 2022. The big concern was that if a bear market occurred that QYLD would implode due to its mechanics. This has been proven to be a false narrative as QYLD isn’t a levered fund, its simply writes covered calls on its assets to generate larger levels of income for its investors. Looking at the graphs above and below, QYLD has relatively outperformed the QQQ for most of the year and many of the big tech names. Investors have gotten a bear market that doesn’t want to go back into hibernation, and through the volatility, QYLD hasn’t broken down worse than its underlying index while still paying larger distributions.

Seeking Alpha

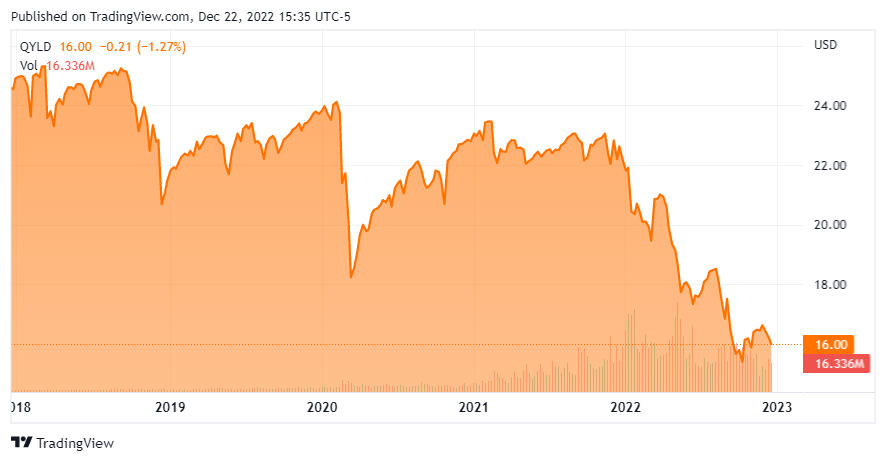

Based on what we have seen after the Covid crash, QYLD can recover when the market turns. The downturn in March of 2020 wasn’t a prolonged bear market as the government threw everything at the problem to get the economy going again. QYLD had dropped from $24.11 on 2/10/22 to $18.23 on 3/16/20 and, over the next year, recovered to $23.45 on 2/16/21. The market hasn’t stopped falling in 2022, and there could be more downside ahead of us in 2023. Even after the mini-crash in 2018, where QYLD went from $25.24 on 9/10/18 to $20.68 on 12/17/18, QYLD still recovered into 2020, surpassing $24. QYLD isn’t going to regain any of the ground it lost until the market turns. Its recovery has also historically taken longer than the traditional market. The important thing is that QYLD hasn’t remained at depressed levels when the market recovers. There is no reason for me to believe that QYLD won’t recover when the market rebounds, and if it takes over a year to get back to a more normalized level, QYLD will continue generating monthly distributions for its investors.

Seeking Alpha

Throughout 2022, QYLD has generated $2.03 per unit in distributions with another one on the way to close out the year

Regardless of if you’re bullish or bearish on QYLD, the distributions generated can’t be disputed. Over the past 11 months, QYLD has generated $2.03 per unit in distributions. This is a 9.09% yield on its price at the beginning of 2022 of $22.29. QYLD has 1 more distribution to pay for December of 2022, and if its average of $0.18 per share is paid in the last distribution, QYLD will have paid $2.21 per unit over the course of 2022. This would be a 9.92% yield on the $22.29 starting price at the beginning of 2022 or a 13.78% yield on a trailing twelve-month (TTM) methodology using today’s closing price of $16.04.

Global X

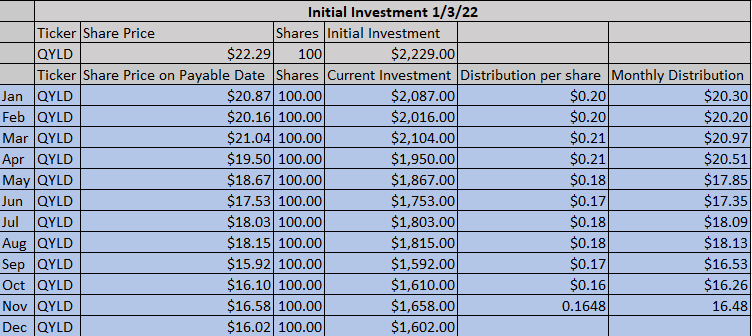

Some investors use QYLD as a current income-generating vehicle and take the distributions as cash, while others reinvest each distribution. If you were to have purchased 100 shares of QYLD on 1/3/22, the initial investment would have cost $2,229. Assuming you were taking the distributions as income, QYLD would have generated $2.03 in distributions, generating a 9.09% yield on the current investment. The initial investment would have declined by -$627 for an initial investment ROI of -28.13%. After factoring in the $202.67 of distributions paid, the total losses would be -$424.33 which is a total ROI of -19.04%. Since no new units were created, based on a TTM methodology, QYLD would have a $252.61 forward projected annual income or a forward yield of 11.33%.

Steven Fiorillo, Seeking Alpha

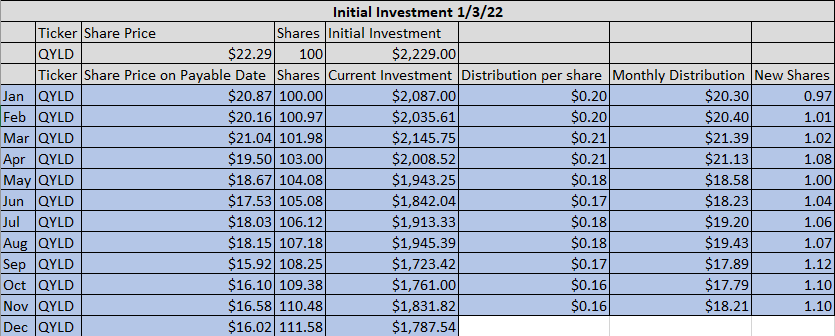

In the scenario where the investor was reinvesting the distributions, the initial shares would have grown to 111.58. The current investment would be worth $1,787.54 for a total ROI of -19.81%. You would have generated $212.54, which would have purchased the additional 11.58 shares, adding an additional $29.26 in future income based on the TTM distribution. The current yield on investment based on what has been distributed through the 11 monthly distributions would be 9.54%.

Steven Fiorillo, Seeking Alpha

Everything is based on perspective as to which methodology is better, as everyone’s investment thesis is different. At the end of the day, the total ROI, if you had taken the distribution, is higher than if you had reinvested them due to the declining unit price of QYLD. If you had taken the income, your investment would be down -19.04%, and if you had reinvested the distributions, your investment would be down -19.81%. On the other hand, the person who had reinvested the distributions would have added 11.58 units of QYLD and increased the forward projected annual income by $29.26 due to the additional units. Either way, this investment has outperformed QQQ and big tech in a down market and continues to generate income each month.

Conclusion

I am still bullish on QYLD and continue to reinvest each distribution. I have added to my position throughout 2022, and I plan on continuing to add into 2023. QYLD is strictly an income investment for me, and investors should understand that the upside potential is capped due to the covered call methodology. If you’re looking for a fund that can generate capital appreciation and either replicate or outperform the market when the downturn ends, QYLD isn’t a fund to consider. As we have seen in the past, QYLD will slowly grind higher when the market turns, but it won’t keep pace with traditional index funds. QYLD is part of an overall income strategy within my portfolio. While I wish the markets weren’t down as much as they are, I am happy that QYLD has proven that it can withstand a bear market and not deviate outside of the losses of the underlying index it tracks.

Be the first to comment