Justin Sullivan

By The Valuentum Team

Qualcomm (NASDAQ:QCOM) is one of our favorite semiconductor ideas. The company is a leader in 5G technology, and we are huge fans of its large licensing business, which is incredibly lucrative. Qualcomm offers investors a nice combination of dividend growth and capital appreciation upside potential, aided by its stellar cash flow generating abilities and bright longer term growth outlook that’s underpinned by secular tailwinds. Shares of QCOM yield ~2.3% as of this writing and our fair value estimate, derived through our enterprise cash flow analysis process (we’ll cover that in detail in this article), stands at $177 per share of Qualcomm. Shares are trading at $127 per share at last check.

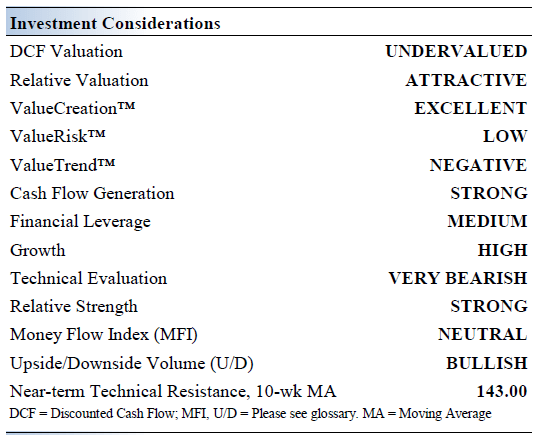

Qualcomm’s Key Investment Considerations

Image Source: Valuentum

Qualcomm is focused on revolutionizing the telecommunications, mobile phone, and automotive industries among others. The company develops breakthrough technology by investing heavily in R&D, and either licenses that technology out or supplies that technology in the form of semiconductor components and related software. Qualcomm was founded in 1985 and is headquartered in San Diego, California.

We view Qualcomm’s longer term growth outlook quite favorably as the company is well-positioned to capitalize on numerous secular tailwinds such as the Internet of Things (‘IoT’) trend, the proliferation of 5G-capable smartphones, the rollout of 5G networks, the rise of autonomous and semi-autonomous vehicles, and more.

Taking a step back, Qualcomm’s outlook turned positive following its agreement with Apple Inc (AAPL) to drop all pending litigation and the formation of a multiyear licensing and chipset supply agreement that was announced back in April 2019. Its strength in 5G has Qualcomm well-positioned for growth moving forward and likely played a role in the settlement. Additionally, Qualcomm concluded a lucrative patent dispute with Huawei in July 2020, though headwinds remain due to Western sanctions. Reaching these deals removed some of the clouds hovering over Qualcomm’s stock price and longer term outlook, which we appreciate.

Automotive Ambitions

In April 2022, the New York-based investment firm SSW Partners acquired Veoneer in partnership with Qualcomm. Here’s why that deal is significant for Qualcomm and how the acquisition unfolded.

First, SSW Partners purchased Veoneer through an all-cash deal with an equity value of ~$4.6 billion, though total cash considerations stood at ~$4.7 billion when including the $0.1 billion termination fee paid to Magna International Inc (MGA). Subsequently to that acquisition, SSW Partners sold Veoneer’s Arriver business unit to Qualcomm, the unit that focused on advanced driver assistance systems and autonomous driving solutions. The duo relatively easily outbid Magna International for Veoneer.

Until the Tier-1 supplier business is sold off, SSW Partners is operating that part of Veoneer’s operations. However, please note that Qualcomm is still recording the financial performance of these non-Arriver operations under the variable interest model and here is an important note from Qualcomm’s latest 10-Q SEC filing on the issue:

We have agreed to provide certain funding of approximately $300 million to the Non-Arriver businesses while SSW Partners seeks a buyer[s], of which approximately $150 million of funding remained available to the Non-Arriver businesses at June 26, 2022. Such amounts, along with cash retained in the Non-Arriver business, are expected to be used to fund working and other near-term capital needs, as well as certain costs incurred in connection with the close of the acquisition.

Although we do not own or operate the Non-Arriver businesses [namely the Tier 1 supplier business], we have determined that we are the primary beneficiary, within the meaning of the Financial Accounting Standards Board accounting guidance related to consolidation [ASC 810], of these businesses under the variable interest model.

By bringing in SSW Partners to run the Tier-1 supplier business, Qualcomm can focus on integrating the automotive technology side of Veoneer’s operations without being forced to also operate a business that is clearly outside of Qualcomm’s strategic focus. Qualcomm has made scaling up its automotive business a top priority given the increased computing power demanded by modern automobiles along with lucrative opportunities available in the realm of self-driving and assisted driving technology.

This deal for Veoneer’s Arriver operations is part of a much bigger strategy that has been slowly unfolding for some time. Back in January 2020, Qualcomm unveiled its Snapdragon Ride automotive platform that enables self-driving activities and enhanced safety features. By 2023, vehicles equipped with its Snapdragon Ride platform are expected to be available.

Two years later, Qualcomm launched Snapdragon Ride Vision System in January 2022 and this offering aims to further optimize the implementation of semi-autonomous and fully-autonomous driving activities, particularly as it concerns the vehicle’s cameras that help enable these options. Vehicles equipped with its Snapdragon Ride Vision System are expected to be available in 2024. Here we will caution that development timetables could get changed due to supply chain issues, geopolitical tensions, and other factors.

Earnings Update

On July 27, Qualcomm posted third quarter earnings for fiscal 2022 (period ended June 26, 2022) that beat both consensus top- and bottom-line estimates. The company has been firing on all cylinders of late. Management issued guidance for the current fiscal quarter during Qualcomm’s latest earnings update that called for the company’s strong growth momentum to carry on in the fiscal fourth quarter, though its near term forecasts were a little lighter than what Wall Street wanted to hear.

Before covering Qualcomm’s near term guidance, let’s take a look at its rock-solid financial position. Qualcomm’s GAAP revenues grew by 36% year-over-year last fiscal quarter and hit $10.9 billion. Its strong sales growth was primarily driven by 45% growth at its Qualcomm CDMA Technologies (‘QCT’) segment, which designs and supplies semiconductor components and related software. Revenue growth here was widespread with sales of its handset, radio frequently front-end, automotive, and Internet of Things offerings all performing quite well.

Pivoting to its Qualcomm Technology Licensing (‘QTL’) segment, which licenses out Qualcomm’s technology, this segment posted 2% year-over-year sales growth last fiscal quarter. While the firm’s QCT segment generates the bulk of its revenues, its QTL segment is incredibly lucrative with segment-level operating margins of 71.1% while its QCT unit had segment-level operating margins of 31.9% last fiscal quarter. During the first three quarters of fiscal 2022, Qualcomm spent ~18% of its revenues on R&D expenses, highlighting management’s commitment to innovation.

Due to widespread strength across its business, Qualcomm’s GAAP operating income more than doubled year-over-year to reach $4.5 billion (please be aware that not all of Qualcomm’s revenue and expenses are assigned to its QCT and QTL segments) last fiscal quarter. Its GAAP diluted EPS rose by 86% year-over-year to reach $3.29, and its non-GAAP diluted EPS rose by 54% to hit $2.96 in the fiscal third quarter.

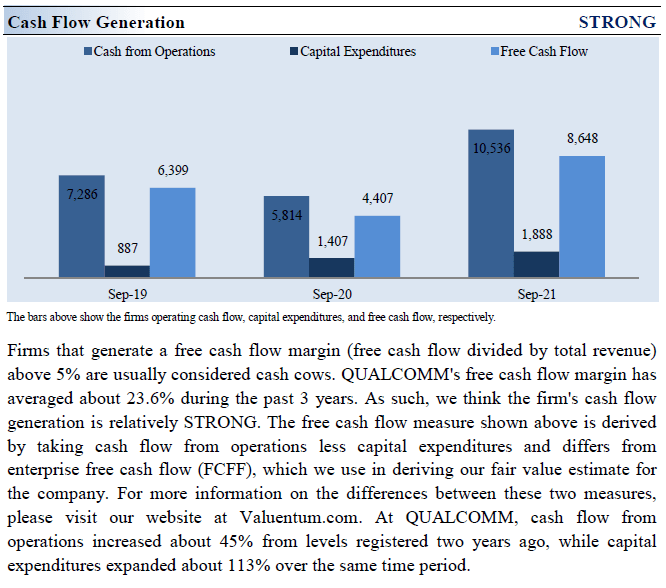

Qualcomm generated $6.0 billion in free cash flow during the first three quarters of fiscal 2022 (defined as net operating cash flow less capital expenditures). The firm spent $2.4 billion covering its dividend obligations and another $2.6 billion buying back its stock during this period. We appreciate Qualcomm’s strong cash flow generating abilities. At the end of the fiscal third quarter, Qualcomm had a net debt load of $8.7 billion (inclusive of current marketable securities and short-term debt). Its $6.8 billion in cash-like assets on hand at the end of this period provides Qualcomm with ample liquidity to meet its near-term funding needs.

Looking ahead, Qualcomm expects to generate $11.0-$11.8 billion in revenue (represents 22% year-over-year growth at the midpoint) in the current fiscal quarter. Its near term revenue growth is expected to be entirely driven by its QCT segment, though its QTL segment is expected to remain highly profitable. Qualcomm expects to post $3.00-$3.30 in non-GAAP diluted EPS (up 24% year-over-year at the midpoint) and $2.53-$2.83 in GAAP diluted EPS (up 9% at the midpoint) in the fiscal fourth quarter. As the company’s near term guidance is still calling for double-digit revenue and earnings growth, we see investor fears over Qualcomm’s growth trajectory as overblown.

Qualcomm’s Economic Profit Analysis

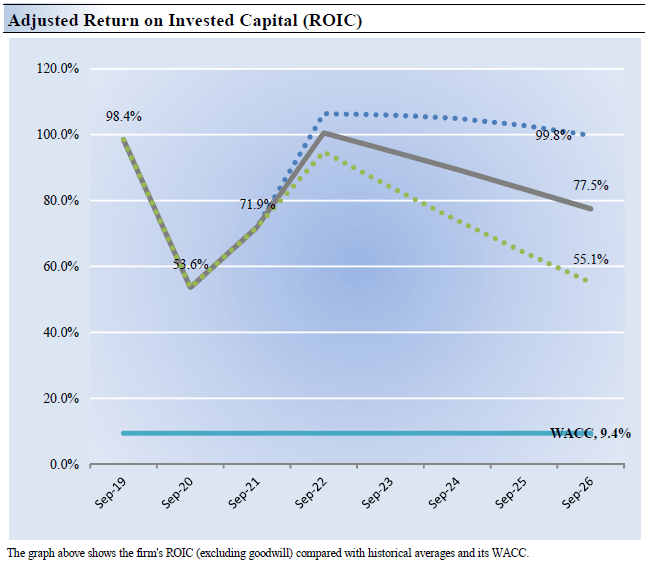

The best measure of a firm’s ability to create value for shareholders is expressed by comparing its return on invested capital [‘ROIC’] with its weighted average cost of capital [‘WACC’]. The gap or difference between ROIC and WACC is called the firm’s economic profit spread. Qualcomm’s 3-year historical return on invested capital (without goodwill) is 74.6%, which is above the estimate of its cost of capital of 9.4%.

In the chart down below, we show the probable path of ROIC in the years ahead based on the estimated volatility of key drivers behind the measure. The solid grey line reflects the most likely outcome, in our opinion, and represents the scenario that results in our fair value estimate. Qualcomm has historically been a solid generator of shareholder value and we expect that will continue over the coming fiscal years.

Image Source: Valuentum

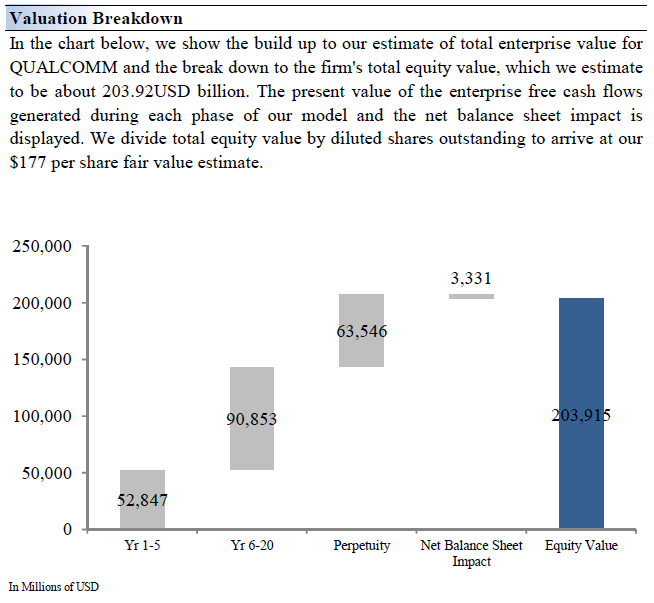

Qualcomm’s Cash Flow Valuation Analysis

Image Source: Valuentum

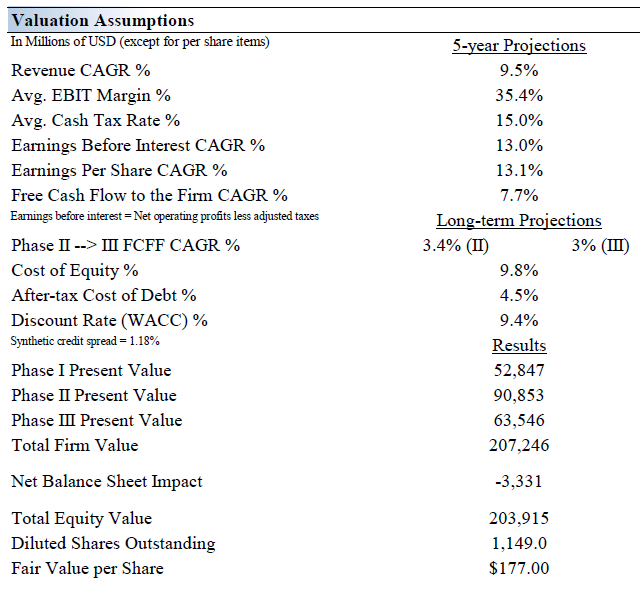

Our discounted cash flow process values each firm on the basis of the present value of all future free cash flows, net of its balance sheet considerations. We think Qualcomm is worth $177 per share with a fair value range of $142-$212. The near-term operating forecasts used in our enterprise cash flow models, including revenue and earnings, do not differ much from consensus estimates or management guidance.

For reference, our model reflects a compound annual revenue growth rate of 9.5% during the next five years, a pace that is lower than the firm’s 3-year historical compound annual growth rate of 13.9%. Our model reflects a 5-year projected average operating margin of 35.4%, which is above Qualcomm’s trailing 3-year average. Beyond Year 5, we assume free cash flow will grow at an annual rate of 3.4% for the next 15 years and 3% in perpetuity. For Qualcomm, we use a 9.4% weighted average cost of capital to discount future free cash flows.

Image Source: Valuentum Image Source: Valuentum

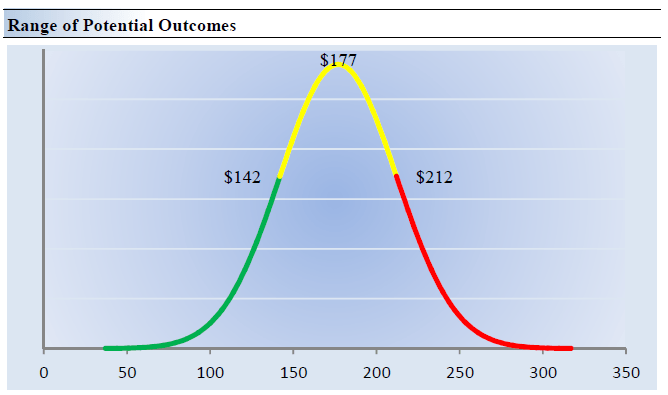

Qualcomm’s Margin of Safety Analysis

Image Source: Valuentum

Although we estimate Qualcomm’s fair value at about $177 per share, every company has a range of probable fair values that’s created by the uncertainty of key valuation drivers (like future revenue or earnings, for example). After all, if the future were known with certainty, we wouldn’t see much volatility in the markets as stocks would trade precisely at their known fair values.

In the graphic up above, we show this probable range of fair values for Qualcomm. We think the firm is attractive below $142 per share (the green line), but quite expensive above $212 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the firm, in our opinion. Shares of QCOM are trading below the low end of our fair value estimate range as of this writing, indicating its shares are undervalued or “cheap.”

Dividend Analysis

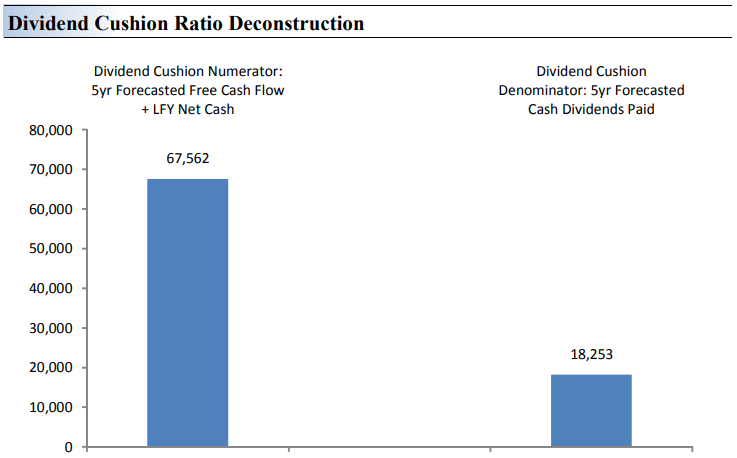

Dividend Cushion Ratio Evaluation (Image Source: Valuentum)

The Dividend Cushion Ratio Deconstruction, shown in the image above, reveals the numerator and denominator of the Dividend Cushion ratio. At the core, the larger the numerator, or the healthier a company’s balance sheet and future free cash flow generation, relative to the denominator, or a company’s cash dividend obligations, the more durable the dividend. In the context of the Dividend Cushion ratio, Qualcomm’s numerator is larger than its denominator suggesting strong dividend coverage in the future.

The Dividend Cushion Ratio Deconstruction image puts sources of free cash in the context of financial obligations next to expected cash dividend payments over the next 5 years on a side-by-side comparison. Because the Dividend Cushion ratio and many of its components are forward-looking, our dividend evaluation may change upon subsequent updates as future forecasts are altered to reflect new information.

Downside Risks

Please be aware that there are downside risks to our thesis on Qualcomm. For instance, should a competitor leap past Qualcomm’s technological expertise in the realm of 5G, that would undercut a large portion of its licensing business and negotiating abilities. Qualcomm was able to secure the aforementioned lucrative deals with Apple and Huawei largely because those companies didn’t have much choice if they wanted to develop 5G-capable smartphones. When it comes to the eventual rollout of 6G technologies, it will be essential for Qualcomm to be a leader in that space, because if it fails to do so, large parts of its business could quickly become irrelevant.

Another key downside risk for Qualcomm involves trade tensions between the US and China. Qualcomm’s market share in China has plunged in recent years due to Western sanctions on major Chinese tech giants. There is not much Qualcomm can do other than comply with Western sanctions and seek growth opportunities elsewhere. Qualcomm has also been contending with major supply chain headwinds during the COVID-19 pandemic. However, its management team has done a stellar job navigating these hurdles while keeping the firm’s growth runway intact by securing deals with multiple suppliers for the same products. We view Qualcomm’s growth outlook quite favorably, but we caution our readers that there are numerous obstacles the firm will need to overcome.

Concluding Thoughts

As the complexity of technology accelerates, Qualcomm sets out to solve the problems such complexity poses, and providing advancing technology at significant scale is one of the firm’s mantras to continue to transform its business and the world. The company is targeting lucrative opportunities across the board with an eye towards supplying semiconductor components to support the IoT trend, enable 5G handsets and equipment, and cater to the growing computing power needs of the automotive industry.

Qualcomm is incredibly shareholder friendly and has returned tens of billions to shareholders since fiscal 2003 via share repurchases and dividends. The firm is a tremendous free cash flow generator though it has a sizable net debt load, partially of product of substantial share repurchases seen in recent fiscal years. Competing capital allocation decisions, from share buybacks to potential M&A activity, need to be monitored. The core of Qualcomm’s licensing model remains intact after recent agreements with Apple and Huawei.

The company’s strength in 5G has Qualcomm very well-positioned moving forward. We view Qualcomm’s dividend growth potential and capital appreciation upside quite favorably.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

Be the first to comment