AutumnSkyPhotography

QUALCOMM Incorporated (NASDAQ:QCOM) stock has recovered impressively since our previous update in November 2022. Accordingly, QCOM formed its lows, outperforming the S&P 500 (SPX) (SPY).

The return of buying sentiments in growth and tech stocks has also lifted the gloom over QCOM and its semi-peers as investors bet on an earlier-than-expected Fed pivot.

Bears could point out that the company’s mixed FQ1 earnings release didn’t inspire confidence in a strong recovery yet. Moreover, its FQ2 outlook suggests persistent weakness in its downstream customers, impacting its growth drivers across its critical business categories.

Investors should note that its previous RFFE category has been embedded across its other three reported categories from FQ1. In addition, Qualcomm’s FQ2 outlook indicates a 2.4% QoQ decline in its QCT segment, suggesting that the macroeconomic headwinds impacting China and downstream inventory digestion are still a challenge.

Despite that, it saw strong growth in its automotive vertical, with Qualcomm posting a 58% YoY increase. However, it’s also critical to note that it accounted for just 5.8% of its QCT revenue. Therefore, we believe investors will still likely focus on whether Qualcomm could execute a recovery in its handsets vertical in H2, which has likely been priced into its recent recovery.

Arch-rival MediaTek’s (OTCPK:MDTKF) recent earnings release suggests that the weakness is broad-based but affected the lower-end tier more significantly. As such, Qualcomm’s close partnership with Samsung (OTCPK:SSNLF) with its AI-accelerated chipset on its Snapdragon 8 Gen 2 platform is critical to maintaining its market leadership.

MediaTek highlighted that it expects to gain market share in the premium Android segment, indicating more intense competition for Qualcomm. Apple’s (AAPL) ability to weather the slowdown in China better in 2022 suggests the resilience of its supply chain relative to the other leading Android players.

QCOM has largely shrugged off the recent weakness related to its frosty supply relationship with Apple as the latter looks to build its cellular modem chip. However, Apple’s endeavors are likely delayed until at least 2024. Nevertheless, we believe investors have looked past such challenges, given its diversified exposure.

Management seems in control and demonstrated that the company has costs levels to pull, as it articulated a 5% reduction in non-GAAP OpEx, relative to FY22’s annualized run rate. Hence, it should help to mitigate the near-term impact on Qualcomm’s prized profitability margins, providing some much-needed respite in the current correction.

Accordingly, the consensus estimates suggest Qualcomm’s adjusted EBT margins should bottom out in June 2023 (FQ3) before reversing higher. Hence, investors are urged to pay attention to a better H2CY23 performance, in line with a better H2’23 GDP performance in China. In addition, MediaTek’s management commentary indicates an inflection point in its operating performance from CQ2’23. Hence, we believe Qualcomm’s commentary is credible, helping the company to perform/surpass the Street’s lowered performance bar.

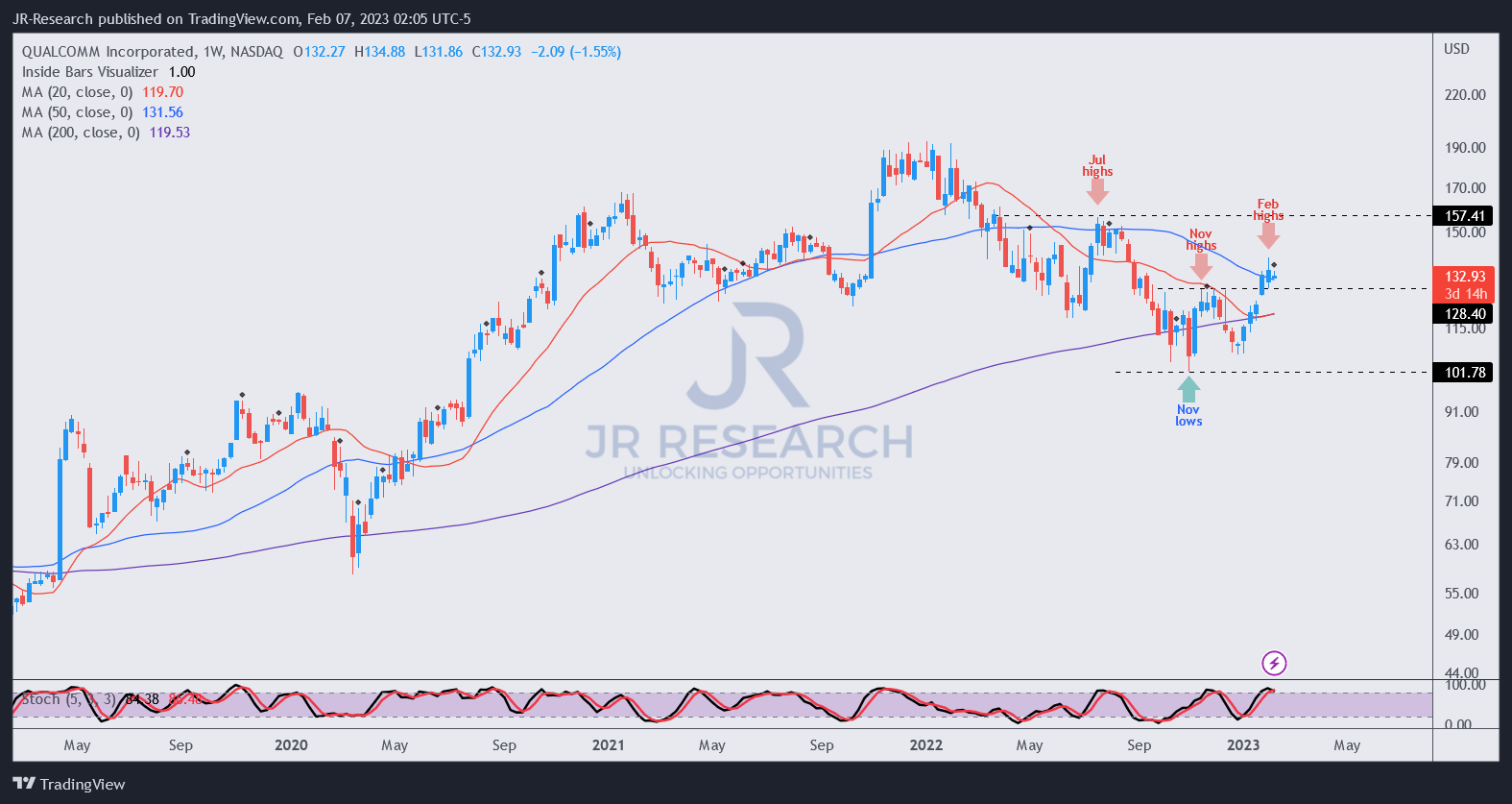

QCOM price chart (weekly) (TradingView)

QCOM’s resurgence from its November lows (up 37% through last week’s highs) re-tested its previous November highs.

The price action is constructive, even though we expect a near-term consolidation, as it closes in against its 50-week moving average or MA (blue line).

QCOM was previously rejected in July 2022 at the 50-week MA but at a “lower valuation” due to subsequent cuts by Wall Street analysts in its forward earnings estimates.

As such, Qualcomm’s NTM adjusted EBITDA multiple of 10.3x has normalized against its 10Y average of 9.9x.

Retaking its July highs and regaining decisive control over its 50-week MA will be critical for QCOM to recover its uptrend bias.

But, a pullback will help to improve investors’ reward-to-risk further, as QCOM’s near-term optimism has likely been priced in.

Rating: Hold (Revise from Buy).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment