Deagreez

Quad/Graphics, Inc. (QUAD) recently delivered beneficial guidance including FCF close to $70-$100 million and announced cost reduction initiatives related to manufacturing, automation, and technology. In my opinion, if management successfully connects to new clients in financial services and packaging services for food products, future free cash flow will likely trend north. Even taking into account existing risks from the replacement of printed content with digital content or failed new strategies, I believe that QUAD appears undervalued.

Massive Target Market

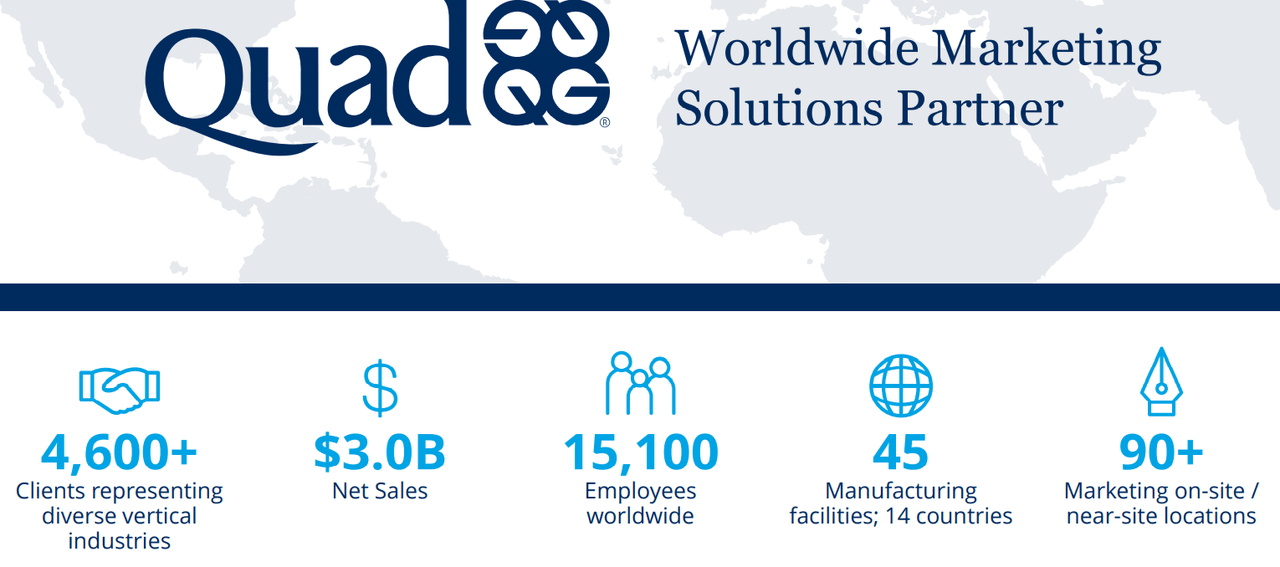

With a client portfolio that includes some of the best-known brands in the United States, Quad/Graphics, Inc. appears to be one of the leading companies in terms of services and comprehensive marketing.

It started functioning in 1971 as a graphic service, and the company expanded its services to the marketing area in 2014, achieving impeccable growth and successful business development. I believe that the number of clients these days is one of the best figures to show what QUAD achieved.

Investor Presentation Investor Presentation

QUAD is dedicated to the positioning of brands from different sectors in the corresponding markets. It also facilitates the entire management in a service integrated into marketing services. This includes content creation for different types of platforms, media positioning, creating packaging and brand values, interior and graphic design for businesses, and printing brochures and articles. I believe that the know-how accumulated by QUAD will likely enhance future sales growth.

According to Dun & Bradstreet First Research, the revenue of the marketing industry in the United States is concentrated by 40% in the 50 largest industries in the area, with more than 38,000 customer establishments and an annual profit estimated at $110 billion. Considering the number of clients reported by QUAD, I believe that the company has a promising future. In my view, there are still a lot of clients to contact, and a lot of market share to acquire.

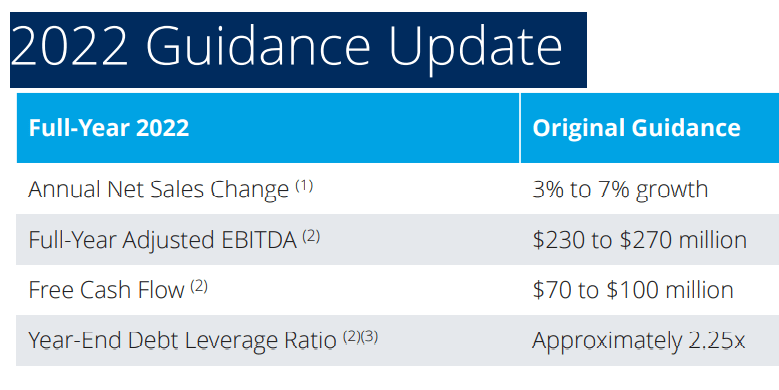

QUAD Reports 9% EBITDA Margin And An FCF Margin Close To 7.6%, And Expects 2022 EBITDA Of $230-$270 Million

It is a pity that many analysts are not covering QUAD. I couldn’t really find a lot of revenue forecasts or free cash flow forecasts. With this in mind, I believe that including previous FCF/Margin ratio and EBITDA margin figures makes a lot of sense. I want to be sure that readers understand that my financial models include financial figures that are not far from the company’s previous figures.

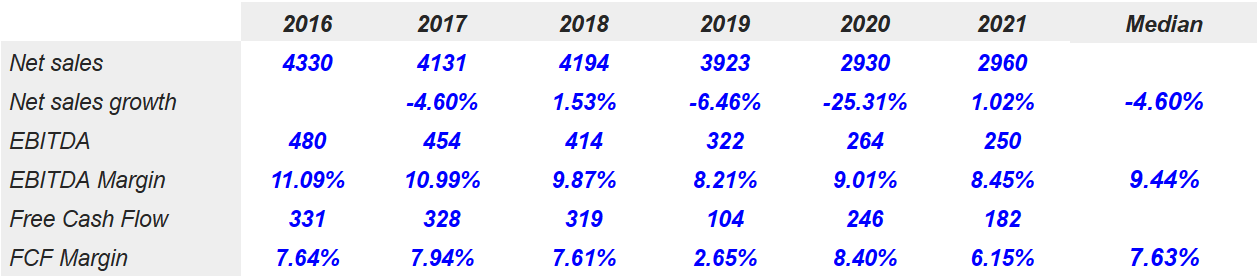

2021 net sales were equal to $2.960 billion with net sales growth of 1.02%. In addition, 2021 EBITDA stood at $250 million with an EBITDA margin of 8.45%. 2021 free cash flow was equal to $182 million with an FCF margin of 6.15%.

Seeking Alpha

In 2022, the company expects adjusted EBITDA margin of $230-$270 million, FCF of $70-$100 million, and net sales growth close to 3%-7%. My numbers are a bit less optimistic than what QUAD reported.

Q3 2022 Call

QUAD Appears To Have A Stable Balance Sheet

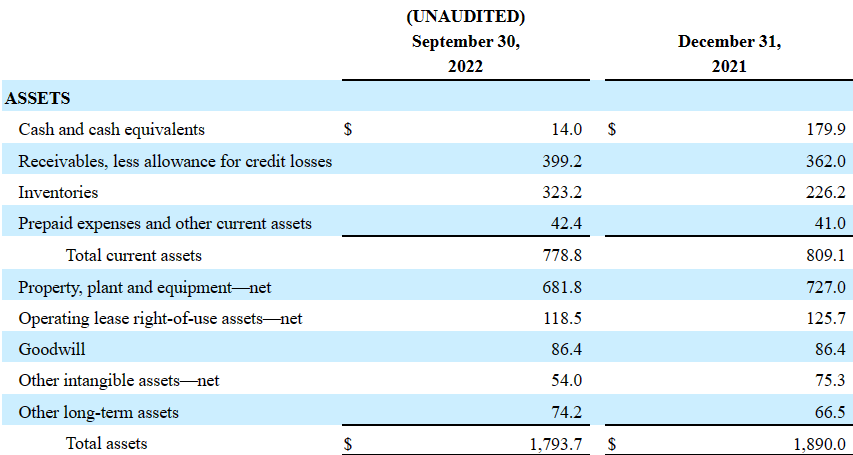

As of September 30, 2022, QUAD reported $14 million in cash, accounts receivable worth $399.2 million, inventories of $323.2 million, and total current assets close to $778.8 million, which is close to the total amount of liabilities. I am not concerned about the company’s liquidity ratios.

Property is worth $681.8 million, and QUAD reports operating lease rights of use assets of $118.5 million and total assets worth $1.7937 billion. The asset/liability ratio is close to 1x, so I would say that the balance sheet appears stable.

10-Q

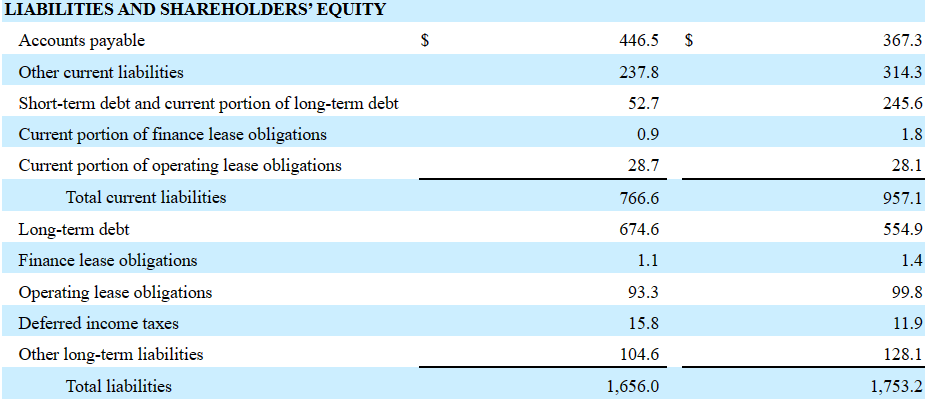

QUAD’s list of accounts payable is equal to $446.5 million, with other current liabilities of $237.8 million and total current liabilities of $766.6 million. Long term debt is not small; equal to $674.6 million. Besides, other long-term liabilities are equal to $104.6 million, and total liabilities stand at $1.656 billion.

10-Q

More Successful Content, Successful Expansion, And More Cost Reduction Initiatives May Lead To A Valuation Of $7.77 Per Share

The company’s objectives for the coming years include the acquisition and expansion of new customer accounts, including the marketing strategy service, the creation of content and positioning, the expansion in key areas of the industry, such as technology, financial services, and packaging services for food products. Considering the know-how accumulated by QUAD in the acquisition of new customers, I would be assuming, under this case scenario, that the company’s strategy will be successful.

Due to the particularity of the marketing industry, in which strategies include the recording and analysis of consumer data, together with the creative and artistic design of the contents, talented employees play a great value in the performance of the companies in this field. Currently, Quad’s employee base is made up of more than 15,100 people at its facilities in the USA, Europe, Asia, and South America, serving 4,600 clients around the world. If the number of employees creeps up, I would be expecting revenue growth.

In addition to its financial strategies and the development of its business model, the company has future objectives in relation to its employees and its relationship with the environment. In relation to its employees, the company has created The Future of Work at Quad program. This implies making office hours more flexible and integrating remote work into its daily activities together with training courses for its employees in different areas of development within the company. If employees feel more valued, I would be expecting better results and more potential clients being more contacted.

As far as the environment is concerned, Quad has forged alliances with local agencies and educational establishments with the aim of reducing the environmental impact of its operations. In the same way, the management has added the company to different specialized programs such as Forest in Focus, the Wisconsin Focus Energy program, or becoming one of the financing companies of the USA government’s Better Plants Program. Also, the company is currently developing its EnviroTech brand, where it develops products with renewable resources. I believe that these initiatives will likely bring more investors. As a result, the cost of equity may diminish, which would bring the company’s fair price up.

Finally, I am quite optimistic about the company’s cost-reduction initiatives related to manufacturing, automation, and technology. If the initiatives are successful, I would be expecting free cash flow margin improvements, which may lead to higher fair prices.

The Company believes it will continue to drive productivity improvements and sustainable cost reduction initiatives into the future through an engaged workforce and ongoing adoption of the latest manufacturing automation and technology. Through this strategy, the Company believes it can maintain the strongest, most efficient print manufacturing platform to remain a high-quality, low-cost producer. Source: 10-Q

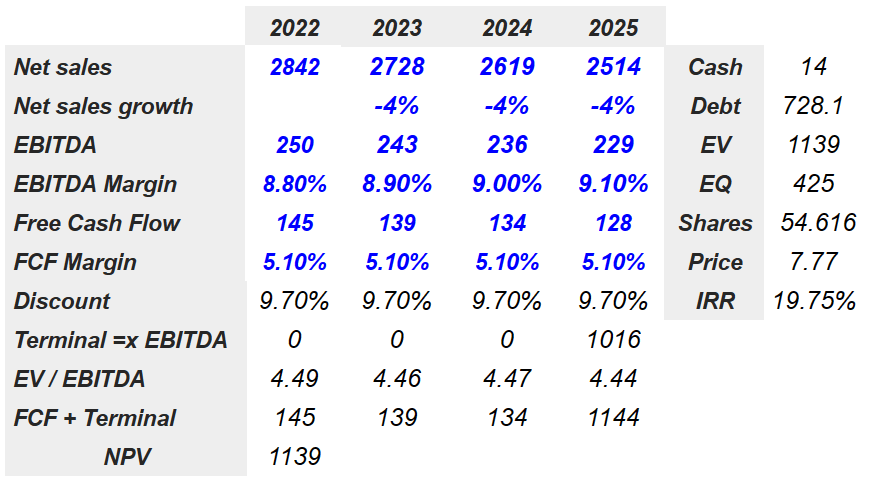

Under the previous conditions, I assumed 2025 net sales of $2.514 billion, with net sales growth of -4%. 2025 EBITDA would stand at $229 million, accompanied by an EBITDA margin of 9.10%. In addition, the free cash flow will likely be around $128 million with an FCF margin of 5.10%.

If we assume a discount of 9.70% and EV/EBITDA of 4.44x, 2025 terminal value would be $1.016 billion, and the enterprise value would be $1.139 billion. Besides, with cash of $14 million and debt of $728.1 million, I foresee an equity value of $425 million, implied fair price of $7.77 per share, and an IRR of 19.75%.

Chatool’s DCF Model

The Replacement Of Printed Content With Digital Content Among Other Risks Could Bring The Price Down To $2.5 Per Share

Although QUAD is positioned as a promising and stable company, financially and in relation to its business model, it is interesting to note the risks that QUAD may suffer. In addition to possible variations in the price of paper and ink, the variations in the costs of raw materials and their transportation, and the replacement of printed content with digital content, the company directly depends on the renewal of current contracts with its primary customers as well as the acquisition of new customers.

In the same way and according to QUAD’s own reports, changes in regulations or delays in postal deliveries can permanently alter the normal functioning of operations. QUAD may suffer from complications in its operations outside the USA or human errors while assessing new strategic initiatives.

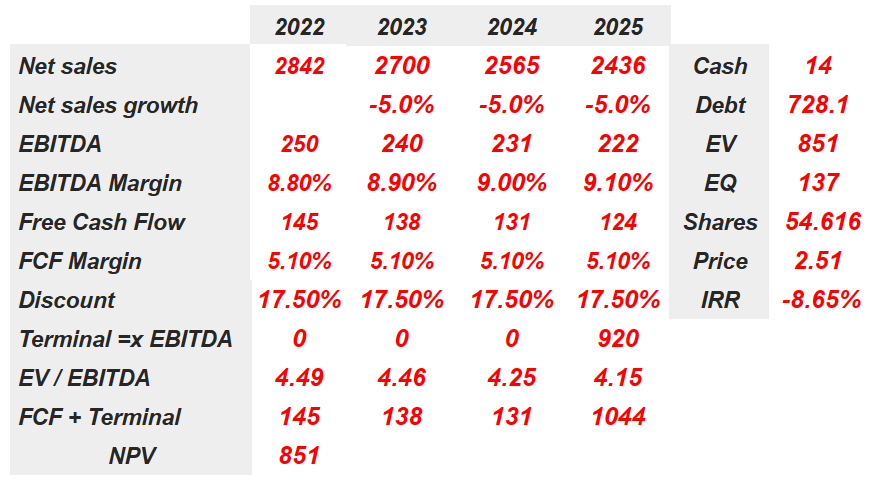

Under this case, I included 2025 net sales of $2.436 billion with net sales growth of -5%. 2025 EBITDA would be around $222 million with an EBITDA margin of 9.10%. 2025 free cash flow would be $124 million with an FCF margin of 5.10%.

With a discount of 17.50% and an EV/EBITDA multiple of 4.15x, the implied enterprise value would be $851 million. With cash of $14 million and debt of $728.1 million, the implied equity valuation would be $137 million. Finally, the fair price would be $2.5 per share with an internal rate of return of -8.65%.

Chatool’s DCF Model

Takeaway

QUAD reported 2022 guidance of about 3%-7% sales growth and FCF close to $70-$100 million. In the last quarterly report, management included cost reduction initiatives related to manufacturing, automation, and technology, which may enhance future free cash flow generation. In my view, further expansion in segments like financial services and packaging services for food products will likely bring revenue generation. Even considering risks from regulators and replacement of printed content with digital content wouldn’t explain the current market price. I believe that QUAD appears undervalued.

Be the first to comment