wildpixel/iStock via Getty Images

Investment Summary

Midway last year we opined that Qiagen N.V. (NYSE:QGEN) lacked conviction for adding additional equity risk in long-biased portfolios. With “bullish and bearish factors on both sides of the investment debate“ this supported a hold thesis, opting to wait on acting on either directional view [long, short]. After reporting its Q4 FY22 numbers, the stock has met our price objective of $49. Subsequently, QGEN’s growth percentages reflected a performance, that, per CEO Thierry Bernard’s language “again, exceeded [its] outlook“.

Data: Author’s previous analysis on QGEN

Before we continue with the Q4 results analysis, we’d note that QGEN’s portfolio has derisked substantially with the wind-back in reliance on COVID-related revenues. In fact, it’s worth noting that ~75% of the Q4 result stemmed from non-COVID segments. For this reason, management are constructive on the QIAstat, NeuMoDx and QIAcuity trio, seeing this now as “a menu play” rather than a COVID play – a classification that is potentially accretive to the installed base, and new registrations.

QGEN Q4 analysis

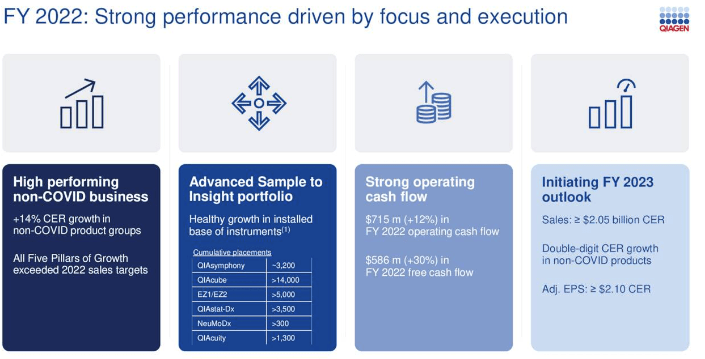

Looking at the results in greater detail, QGEN marked numerous cumulative milestones across its main divisions; namely, >3,200 cumulative placements of its QIAsymphony system, 14,000 in the QIAcuity division, and has 5,000 EZ1 and EZ2 systems in the field. Tied to the derisking points above, the QIAstat-Dx system also observed 3,500 placements by year’s end, illustrating the growth excluding COVID-19. With respect to management’s “menu” comments, the NeuMoDx platform continued to penetrate accounts and signifies ~10% market share. It now claims a broad assay menu with 16 CE-IVD tests, having cumulatively placed over 300 platforms in laboratories worldwide.

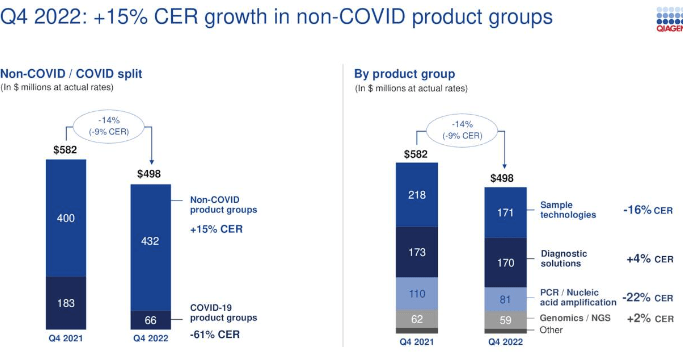

Switching to the quarterly numbers, it was another mixed period for the company. Top-line sales were reported at $498mm, a 14% YoY decrease with ~500bps of FX headwinds baked in. Ex-COVID segments outpaced internal expectations, reporting a 15% increase, driving full-year ex-COVID sales growth of 14% in [constant currency, (“cc.”)], in-line with guidance. On the contrary, Q4 COVID-related sales decreased 60% YoY in cc. and saw a decline of 30% for the full-year, totalling $470mm, illustrating our derisking points from above. It pulled this down to adj. EPS of $0.50, in-line with estimates, with growth compressed by FX cross rates.

Moving down the P&L, gross margins were flat at 67.7% and benefited from better sales mix from QIAstat-Dx numbers, yet adjusted operating margin compressed ~300bps YoY to 30.6%, as the firm diverted capital toward its growth initiatives. In particular, R&D investment lifted ~50bps YoY to 8.9%, and the firm lost ~200bps of leverage at the SG&A line.

Exhibit 1.

Data: QGEN Q4 Investor Presentation

Observing cash flows, CFFO lifted by 12% YoY to $750mm and reflected the revenue upsides above. It pulled this to FCF of $586mm, a growth schedule of 30% YoY. Related to the FCF movement, QGEN diverted capital away from PP&E investments, and managed to retire $433mm in net debt, now at $443mm on the balance sheet. Subsequently, leverage tightened to 0.5x from 0.9x same time last year, a sound move given the current rates climate.

With respect to the divisional highlights, important takeouts include the following:

- Consumables revenue was down 11% in cc. terms, balanced by 600bps YoY growth in instrument sales, reflecting a normalization toward pre-pandemic trends. As mentioned, this fits with QGEN’s non-COVID growth.

- Revenues in the sample technologies business contributed ~33% to the top-line and captured high single-digit growth for both Q4 and full-year, hitting the FY22 sales target of $750mm. Importantly, the diagnostic solutions product group also generated ~33% of top-line sales and grew ~21% YoY cc., underlined by upsides in the QuantiFERON franchise. Supporting this was $85mm in FY22 sales for QIAstat-Dx and >50% of this originated from non-COVID.

- Related to earlier discussion, we observed the drag of COVID-related sales in the NuMoDx division where ~2/3 of its revenues were obtained from testing, but still met the $80mm sales target.

- It’s also important to note the 20% cc. YoY gain in the PCR product line, in particular via the QIAcuity segment that exceeded internal guidance of $55mm for the period.

Exhibit 2. Non-COVID upsides [note: CER = cc.]

Data: QGEN Q4 Investor Presentation

Subsequent to the growth numbers listed, management expect $2.05Bn in revenues, projecting a sharp decrease in COVID-related to $200–$210mm. It looks to pull this down to adj. EPS of $2.10, with ~$0.30 dilution from its Verogen acquisition.

Valuation and conclusion

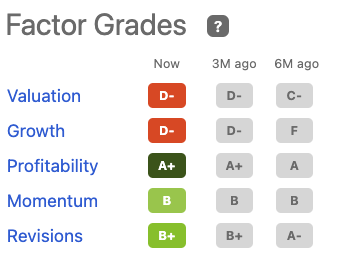

In the last publication, we had guided to a $44–$49 target range “suggesting the stock could be fairly valued”. With shares at the upper end at range the stock is trading at 23x trailing GAAP earnings, a 5% discount to the sector. As it stands, QGEN is also trading at 3.2x book value on a forward EV/EBIDA of 14.6x. Looking to management’s estimates of $2.10 per share at the bottom in FY23, this looks to a price target of $48. Alas, and again, we suggest the stock could be fairly valued trading at these ranges. This target is supported by the quant factor grading [Exhibit 3].

Exhibit 3. QGEN Seeking Alpha factor grades

Data: Seeking Alpha

As QGEN continues to reorganize its portfolio post-COVID management remain optimistic on FY23 growth numbers. Here we are guiding to a fair value 23x P/E and see it currently trading at a premium to the implied $48. Without the scope for valuation upside in this analysis, we reiterate our hold rating on the QGEN stock price.

Be the first to comment