Thiago Montoto/iStock via Getty Images

Investment Thesis

Qiagen’s (NYSE:QGEN) early entry into the DNA extraction market allowed it to develop a strong foothold in the field of molecular diagnostics and research. Revenue grew along with the industry since the company’s foundation in 1986, fueled by ground-breaking discoveries in cell biology that enhanced scientists understanding of how cells work and advancements in gene sequencing that opened the door for new research areas but, more importantly, commercialization of these discoveries. The company participated in the 1990s Human Genome Project, which saw the first-ever deciphering of human DNA, a decade-long effort that cost billions of dollars. Today, the same endeavor would cost less than $1000 and take a day to complete.

Despite this progress, I believe we are at the early stages of an emerging market of molecular diagnostics and research. The healthcare industry in the US is starting to embrace molecular diagnostic tests. For example, last November, Natera raised its revenue guidance, noting reimbursement opportunities as insurance companies and key opinion leaders embrace molecular diagnostic tests. In previous articles, I noted that even though most healthcare insurance companies now cover BRCA DNA analysis for women with cancer, only half of these patients undergo such a test, mirroring growth opportunities in unpenetrated markets. The rest of the world is also catching up with the US. For example, the UK is rolling out national cancer and pre-natal screening program for its residents. The United Arab Emirates is undergoing a nationwide endeavor to build the first Arab Genomic reference database.

There is more to Qiagen’s success than chance, instead earned. The Dutch-based company is well-run and has been the target of multiple acquisition attempts from rivals, such as Thermo Fisher Scientific (TMO). According to Bloomberg and the WSJ, it is currently discussing a potential merger with Bio-Rad.

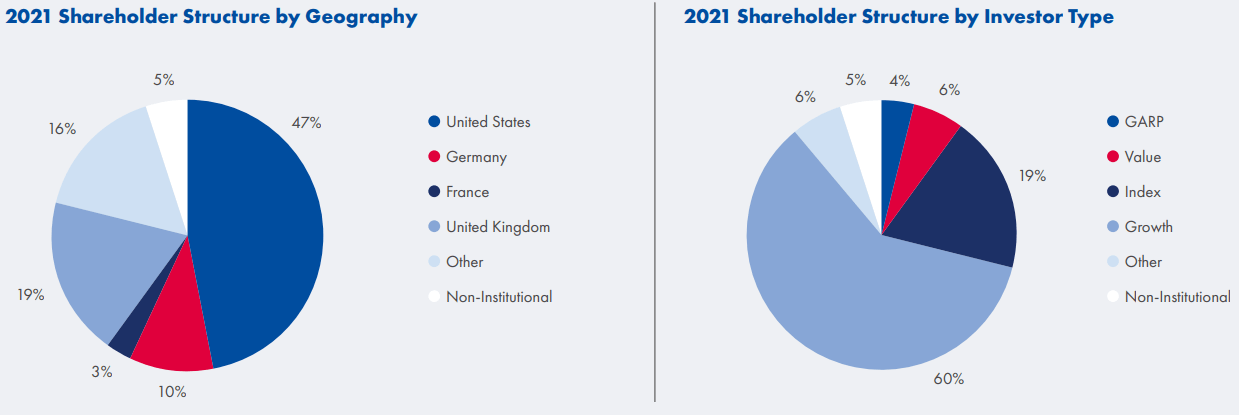

This piece will not discuss the merits of this deal. Nonetheless, if history is any guide, one must consider Qiagen’s activist, growth-oriented, and committed shareholder base. The company’s shareholders voted down TMO’s $12.2 billion proposal in 2020. Below is a profile of Qiagen’s shareholder base as of 2021.

Qiagen

In the following paragraphs, we take a closer look at Qiagen’s revenue drivers, strategy, and financial position, focusing on the latest annual results released last week.

Revenue Trends

Qiagen’s expertise, scale, and business focus earned it a critical position in the fight against COVID in the past twenty-four months. As cases began to drop and testing mandates began to ease, the company’s earnings fell, and we saw these dynamics accelerate in the past few months. Q4 2022 revenue fell 14% to $498 million, down from $582 million in the prior quarter, with full-year 2022 revenue falling 5% to $2,142 million, down from $2,252 million in 2021.

Given its comprehensive COVID product portfolio, this revenue decline touches on multiple business lines. For example, the company’s Sample Technologies business fell 22% (16% cc) from $218 million to $171 million as demand for RNA extraction kits dithered. PCR segment fell 27% (22% cc) as demand for testing slowed. In the molecular diagnostic segment, demand for NeuMoDx, Qiagen’s high throughput workstation, which played a critical role in scaling the COVID test and research, fell by 27% (22% cc). Seeking Alpha Quant Score Ratings mirror these dynamics.

Seeking Alpha

Still, looking closer at Qiagen’s core business, we see a sizable increase in business activity. Non-COVID Q4 and FY 2022 revenue grew 15% and 14%, respectively, on a constant currency basis. This could also be an indicator that the sell-off in the molecular diagnostic lab industry, i.e., Exact Sciences (EXAS), Natera (NTRA), and others, could be overdone.

Management guided for at least $2.05 billion in sales in FY 2023 on a constant currency basis, representing a 4% or about $100 million YoY total sales decline. In FY 2022, Qiagen’s COVID sales were $470 million. Given the pace of its decline (64% in Q4), it is reasonable to forecast a $100 million in COVID sales in 2023. If this is the case, then management is factoring in a 14% increase in core revenue this year, in line with historical averages, as shown below. Thus, I believe management’s 2023 estimates are conservative.

| Segment | 2021 | 2022 | 2023 E |

| Core Segment | $ 1,547 | $ 1,672 | $ 1,906 |

| COVID Sales | $ 704 | $ 470 | $ 100 |

The company is doing well partly because of the way the industry is performing. For example, liquid biopsy diagnostic products are becoming more popular, especially in the US, where they are sold as Laboratory Developed Tests. Payors continue to make supportive coverage decisions led by Key Opinion Leaders’ adoption of molecular diagnostic tests. In Europe, which brings in about a third of Qiagen’s revenue, we see promising national genomics programs that will drive growth. For example, the UK’s National Health Service “NHS” is rolling out a new molecular diagnostic service, while the demand from China, which surprisingly showed a resilient quarter despite lockdowns, is set for further acceleration as the Asian nation reopens.

Balance Sheet

Qiagen hasn’t released its full Q4 and end-of-year 2022 report yet, but if history is any guide, shareholders should expect it in the coming two weeks. In November 2022, the company recorded a debt balance of $2.3 billion, segmented in the table below (figures in 000s).

| 0.500% Senior Unsecured Cash Convertible Notes due 2023 | $ 385,898 |

| 1.000% Senior Unsecured Cash Convertible Notes due 2024 | $ 459,795 |

| 0.000% Senior Unsecured Convertible Notes due 2027 | $ 497,203 |

| 3.75% Series B Senior Notes due October 16, 2022 | $ 299,970 |

| 3.90% Series C Senior Notes due October 16, 2024 | $ 26,976 |

| German Private Placement (2017 Schuldschein) | $ 259,839 |

| German Private Placement (2022 Schuldschein) | $ 359,565 |

| Total long-term debt | $ 2,289,246 |

| Less: current portion | $ 866,040 |

| Long-term portion | $ 1,423,206 |

Our first objective is to weed out debt that has matured since the November 2022 report. First is the 3.75% Series B Senior Notes due October 16, 2022, which I expect has been repaid in cash, if not refinanced. In addition to Series B notes, 60% of the German Private Placement (2017 Schuldschein) tranches matured in October 2022 (the debt consists of tranches with different maturities through 2027.) This brings the total matured debt to $453 million.

The company generated $124 million of operating cash flow during Q4 (which is less than the previous quarter, possibly due to working capital changes. Again, we will know more detail when the company releases its SEC report in the next few weeks. According to my estimates, free cash flow was also moderate during the quarter, standing at about $50 million. This means that its cash balance most likely decreased unless the company refinanced its maturing debts. Nonetheless, this comes from a strong position, with a cash balance of $1.4 billion.

Summary

Qiagen is well-positioned to capture the accommodative tailwinds of an emerging molecular diagnosis and research industry. Its strong relationship with biotech and academic research institutions allows it to have a finger on the pulse of a dynamic industry characterized by rapid technological change, giving it an advantage over smaller players.

The company is not cheap, but not ridiculously priced either, trading at a 23x Forward PE ratio, above the sector average by 17%. In the past few years, we saw an exponential increase in EPS, driven by the economics of scale, strong brand awareness, and prudent acquisitions. Given these dynamics, I believe that Qiagen offers attractive Growth at a Reasonable Price “GARP.”

Be the first to comment