Mongkol Onnuan

My Background

Each investor faces a different set of circumstances. Now 35, I have been investing since I was 22 years old. My first investment in individual stocks was made in the heart of the financial crisis back in May 2009. I purchased 40 shares (80, split-adjusted) of Toronto-Dominion Bank (TD:CA). However, for years before making that purchase, I had been researching the best methods available for both wealth creation and preservation.

I don’t believe in taking unnecessary risks and feel the whims of the stock market are too fickle as far as capital gains are concerned to base my aspirations of financial freedom on. Dividend growth investing stands out as it is far more predictable that a healthy company might increase its dividend by 6% than to make any sort of prediction about stock price volatility in the near term.

On this basis and from my initial foray into the markets with TD, I’ve built a portfolio of over 30 cash flowing equities. My goal is ultimately to have a stock market portfolio which provides enough income to cover all of my expenses.

While some feel that it only requires ten companies to achieve ultimate diversification, I believe there is room for a healthy level of redundancy to avoid the hiccups involved with company-specific performance. Regardless, I endeavor to always own the best-of-breed companies in their respective industries. I can live with slower growth if it means greater security for my invested dollars.

This is a strategy I have researched over time and came to trust because it can work for me both as a young investor and likewise carry me through the decades to come. While it may not turn heads at a dinner party, it has proven its value over the past few hundred years and remains as relevant as ever today in our digital age.

Having noted the above, it is truly a great time to be a dividend growth investor. The companies I own are committed to rewarding shareholders and I love nothing more than to reinvest back into them to further increase the compounding power in my portfolio

Dividend Summary

As a Canadian investor, I prioritize income in CAD. As such, 25 of my dividend sources were paid out in CAD, with the remaining 11 paying in USD.

Please note that all Canadian companies are owned in CAD on Canadian exchanges. KO and JNJ are owned in CAD within my portfolio, though they reside on the NYSE; their dividend payments are provided in CAD.

CAD Dividends

| Company | CAD Payments ($) |

| Toronto-Dominion Bank (TD:CA) | 178.00 |

| RioCan Real Estate Investment Trust (REI.UN:CA) | 66.57 |

| The Coca-Cola Company (KO) | 159.93* |

| Johnson & Johnson (JNJ) | 97.52 |

| BCE Inc. (BCE:CA) | 202.40 |

| Canadian Imperial Bank of Commerce (CM:CA) | 19.92 |

| Corby Spirit and Wine Ltd. (CSW.B:CA) | 11.00 |

| Bank of Nova Scotia (BNS:CA) | 103.00 |

| TELUS Corporation (T:CA) | 72.80 |

| Rogers Communications Inc. (RCI.B:CA) | 27.50 |

| Fortis Inc. (FTS:CA) | 110.18 |

| Canadian Utilities Ltd. (CU:CA) | 104.39 |

| Canadian National Railway Company (CNR:CA) | 32.96 |

| Canadian Pacific Railway Limited (CP:CA) | 9.50 |

| Hydro One Ltd. (H:CA) | 72.70 |

| Chartwell Retirement Residences (CSH.UN:CA) | 15.30 |

| Metro Inc. (MRU:CA) | 5.50 |

| Brookfield Renewable Partners L.P. (BEP.UN:CA) | 123.19 |

| Brookfield Renewable Corporation (BEPC:CA) | 56.19 |

| Brookfield Asset Management (BAM:CA) | 4.22 |

| Brookfield Infrastructure Partners L.P. (BIP.UN:CA) | 14.59 |

| Brookfield Infrastructure Corporation (BIPC:CA) | 7.78 |

| A&W Revenue Royalties Income Fund (AW.UN:CA) | 19.00 |

| Enbridge Inc. (ENB:CA) | 21.50 |

| Saputo Inc. (SAP:CA) | 5.40 |

*KO pays twice in Q4, so its dividend is effectively double what I would get from a single payment.

USD Dividends

| Company | USD Payments ($) | Div Change (%) |

| Waste Management, Inc. (WM) | 27.63 | |

| McDonald’s Corporation (MCD) | 27.14 | 10.14 |

| Yum! Brands (YUM) | 18.90 | |

| Yum China (YUMC) | 3.98 | |

| Visa Inc. (V) | 5.74 | 20.00 |

| AbbVie Inc. (ABBV) | 63.45 | |

| Microsoft Corporation (MSFT) | 7.52 | |

| Mastercard Incorporated (MA) | 2.92 | |

| Apple Inc. (AAPL) | 3.45 |

Dividend Totals

I was fortunate to set a new quarterly income total for my portfolio. I brought in C$1,541.04 and U$160.73, combining for a currency-neutral $1,701.77. In comparison with the $1,531.06 from Q4 2021, my dividend income has grown by a healthy 11.15%.

Notching a double-digit dividend growth rate is the result of focusing on the three main methods of growing passive stock income:

- Organic dividend growth by high-quality companies.

- Reinvesting dividends received.

- Adding fresh capital to buy more dividend-paying stocks.

The investments made earlier in the year continue to ship me additional cash flow to keep the dividend growth engine running.

From a bird’s eye view of 2022, the four quarters have combined for $6,395.88:

My goal for the year was to hit $6k, so I’m comfortably ahead of where I projected at the beginning of the year.

Market Activity

Looking at the investment world from a high level over the next few decades, I believe one of the biggest areas of growth will be infrastructure. As populations swell and middle classes emerge in developing economies, the need for energy, data centers, and other forms of large-scale infrastructure is going to increase substantially.

As such, I took the opportunity to invest further in two high-quality energy and infrastructure companies:

| Company | Shares Purchased | Annual Dividend Rate | Projected Forward Annual Income |

| Brookfield Infrastructure Corporation (BIPC:CA) | 15 | U$2.16 | C$54.00 |

| Fortis Inc. (FTS:CA) | 20 | C$2.26 | $33.90 |

Since I take the BIPC dividends in CAD despite them being paid in USD, I’ve added a conservative 25% boost from FX. This will fluctuate, but it should remain favourable for the foreseeable future.

So, I made two minor increases to positions I already own. In summary, they’ll kick off ~$21.98 quarterly, ~$87.90 annually.

Since I highlighted an earlier purchase of BIPC in my Q3 article, I’ll cover a few of the high points for FTS this time around.

Fortis Inc. (FTS:CA)

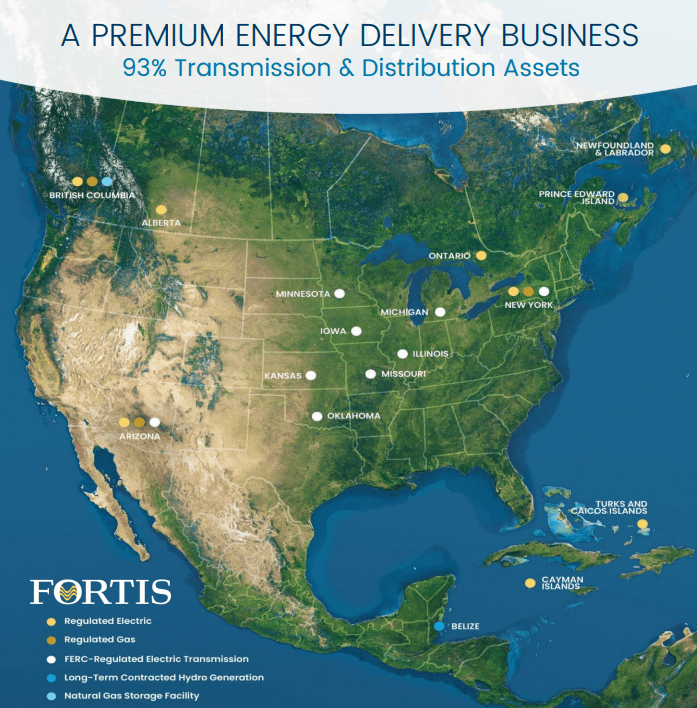

As one of the premier electric and utility gas companies in North America, FTS serves over 3 million customers. Of its utility assets, 99% are regulated and can be relied upon for consistent, rising returns.

In their December 2022 Retail Presentation, they highlighted the diversified nature of their energy delivery business:

FTS December 2022 Investor Presentation

The company has a long history of delivering on its vision. Most recently, its 2022-2027 capital plan projects a 6.2% CAGR with low risk. As the electrification of the overall grid persists with electric vehicles coming online as a secular growth story, FTS will be one of the companies meeting those needs.

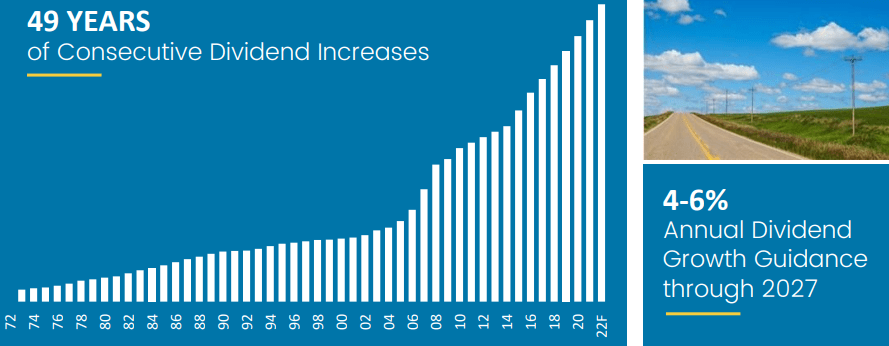

As an investor, one of the top features that has kept me invested since 2015 is the reliable dividend. Likewise, the company provides exceptionally transparent dividend guidance to shareholders:

FTS December 2022 Investor Presentation

FTS boasts 49 consecutive years of dividend raises and is further projecting 4-6% increases all the way out to 2027. This timeline will take them well past their coronation as a Dividend King.

It’s also what helps me sleep easily each time I add fresh capital to this dividend powerhouse.

Conclusion

I set yet another record in Q4, closing out the year in style. Finishing with a +$1.7k pop provides me plenty of cash to continue reinvesting in the best opportunities I can find.

I’m excited to see what 2023 has in store for us. While life has been nothing but a roller coaster since early 2020, I do feel like we’re on the tipping point of some positive momentum:

- There is a real possibility of peace in the next few months between Russia and Ukraine. What that will look like and how the negotiations will shake out remains to be seen, but I am hopeful.

- The likelihood of further COVID lockdowns is severely lessened. Even with numbers undoubtedly set to rise through the colder months of the year, we have mechanisms (e.g., vaccines) in place to dampen the severity.

- Inflation is a beast that continues to run rampant, but the increased interest rates are likely to start working their way into the economy in the coming year. It’ll just take some time.

Remain optimistic, remain invested. Be ready for the possible recession to come, but don’t be afraid to pull the trigger when opportunities present. I’ll be nibbling on the way down, and backing up the truck when the time comes.

Thank you for reading.

Be the first to comment