Investment thesis

Purple Innovation (PRPL) business will be hit because of the current coronavirus pandemic and make its path to profitability uncertain in the near term. We also believe that the pandemic will hurt many of its 175 competitors in the mattress-in-a-box industry. Therefore, while Purple’s revenue will decline in 2020, we expect its strong balance sheet and strong brand to cushion it into the future.

Introduction

Purple Innovation is a popular company that manufactures and sells mattresses. The company sells its mattresses and sleeping accessories through the internet. It has also started to increasingly sell its products through wholesalers in the United States.

The bed-in-a-box industry is highly competitive. According to Michael Magnuson, there are more than 175 such companies in the United States, which sell very similar products. These companies compete with already-established brands in the US like publicly-listed Tempur-Sealy (TPX) and Sleep Number (SNBR).

Like all industries, the online mattress sector has been hit by the current coronavirus pandemic. In a recent update to investors, Purple withdrew the guidance it issued in February. It has also furloughed its employees in a bid to preserve cash.

We believe that the market for online mattresses is there. Data shows that the mattress industry in the United States is worth about $32 billion and is expected to reach $43 billion in 2024. Most of these sales are concentrated in traditional retailers. Still, as more people shop online, the share of bed-in-a-box industry will take more market share.

The current pandemic has left more than 26 million Americans out of work, according to the latest jobless claims data. The implication is that more people will not be buying mattresses – and other discretionary – products any time soon. As a result, I expect most unprofitable bed-in-a-box mattress firms to fight for survival. A good example of this is Casper (CSPR), whose stock has dropped by more than 40% after its IPO. A report published in 2019 found that Casper had a market share of 37% while Purple had a share of 32% in the online mattress industry.

At the same time, I expect some companies, that have a good balance sheet to emerge stronger because competition will be reduced. In the long-term, we expect that Purple will emerge stronger. However, we also expect more volatility in the near term.

Purple Innovation path to profitability uncertain

Other than the hit by the coronavirus pandemic, we believe that Purple’s path to profitability will be relatively longer. In the past four years, the company has made losses worth more than $16 million, and I expect the losses to continue.

While the management has done a good thing in furloughing employees and reducing marketing, the reality is that the company will continue losing money because of other costs. Also, the company’s wholesale arm will likely see reduced sales this year because most wholesale outlets are not operating.

The wholesale segment is very important for Purple. In the most recent quarter, the segment contributed 36% of the total revenue compared to just 25% a year before. In the earnings call, the company said:

“The revenue increase was primarily due to an increase in wholesale revenue driven by an increase of over 800 stores as compared to the same period last year.”

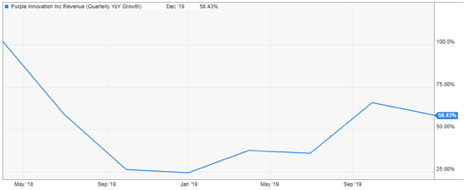

We also expect the direct-to-consumer business, which brings a higher margin to take a hit. In fact, recent data show that fewer people are visiting the company’s website. Although it is impossible to use this data as a measure of revenue, it is a sign of how hard the company could be hit.

Source: SimilarWeb

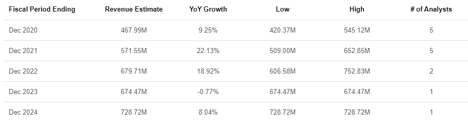

Therefore, while the company is saving money on R&D, employee salaries, and sales and marketing, we expect these savings to be offset by a significant decline in revenue. We also believe that the current revenue estimates by analysts to be relatively optimistic. As shown below, data compiled by Seeking Alpha shows that analysts expect the company’s revenue to grow to $467 million this year.

Source: Seeking Alpha

Going by the expected slowdown in wholesale and DTC and the fact that Purple’s revenue was slowing before the crisis, we expect the revenue to fall to less than $400 million.

Source: YCharts

Worse, we expect that it will take years for Purple to improve its margin. Before the crisis, Purple Innovation had a gross margin of about 47%, which is almost the same as that of Casper. This gross margin is significantly lower than that of Sleep Number, which had a gross margin of 68%. Sleep Number had a net profit margin of 8%.

Therefore, even if Purple is able to greatly improve its revenue, its net profit margin will continue being low. This is partly because the low-margin wholesale revenue is becoming a major part of its total revenue mix.

What about Purple balance sheet?

We believe that many companies will weather the current pandemic. The companies that will particularly do well are those that have strong brands and a strong balance sheet.

Fortunately, due to its strong marketing in recent years, Purple is a well-known brand among the young people. This brand popularity will help the company emerge strong even as other competing companies struggle. In fact, going by the loss-making of Purple and Casper, we believe that many of the 175 bed-in-a-box companies will not survive the pandemic. This will be in line with what the New York Times (NYT) reported a few weeks ago about the challenges most startups are facing. In the report, Mike Jones, a venture capitalist said:

“There’s no doubt that this will be a time of weeding out of start-ups that can’t survive.”

Looking at the balance sheet, things are a bit promising. The company ended the quarter with more than $33 million in cash and short-term investments and just $35 million in debt. The management has also reduced its marketing and employee-related expenditure in a bid to preserve cash.

Also, the fact that Purple has minimal debt, and the fact that interest rates have been brought lower, the company could also benefit by raising more debt. Therefore, although Purple will be hit in the short term, we expect the company to have more flexibility to raise money if need be. The company could also preserve cash by halting or scaling down the ongoing projects such as the East Coast Manufacturing facility.

Therefore, Purple’s strong brand among millennials and its strong balance sheet could help it weather the current storm. We also believe that it is positioned better than Casper, whose valuation has dropped to less than $200 million.

Final Thoughts

Purple is a strong brand that has been hit hard this year because of the pandemic. We expect the sales growth to plummet since very few people are buying mattresses during the lockdown. Also, we believe that the fact that many wholesalers are closed will hurt its fastest-growing segment. In the long-term, we expect the company’s strong brand and strong balance sheet to help it weather the current storm.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment