IGphotography

This is an update on Purple Innovation (NASDAQ:PRPL) – idea that was highlighted to Special Situation Investing members in late September. PRPL – a designer and manufacturer of premium/luxury mattresses and pillows – received a non-binding acquisition proposal from its major shareholder Coliseum Capital (45% stake) at $4.35/share. The offer clearly looked opportunistic and timed at historical share price lows. The bid valued PRPL at 0.6x TTM sales compared to sales multiples of 4x at post-COVID peak and 0.75x pre-COVID. Moreover, shareholder support was highly questionable as PRPL’s six other large shareholders (combined stake of 34%) had a cost basis materially above the offer price. We argued that the merger was unlikely to go through at the initial terms.

Recently, PRPL reported strong quarterly results. Driven by effective cost-cutting measures, the company recorded $12.1m in adjusted EBITDA, outearning 3 out of 4 quarters from last year (which were uplifted by pull-forwarded demand). The management has raised adjusted EBITDA guidance for 2022 – $2m-$7m from the previously estimated range of -$15m to -$2m. Share price has reacted favorably to the earnings release, with PRPL jumping 29% since the announcement. Notably, PRPL has also instituted a poison pill to prevent a creeping takeover by Coliseum. The companies did not provide any updates on a potential transaction, however, recent developments suggest a merger at the previous offer price is now off the table.

Having said that, some arguments suggest a higher bid from Coliseum might be in the cards here:

- Coliseum seems to be highly interested in a potential transaction. Notably, between March and May 2022, the shareholder acquired 11% of PRPL outstanding shares at an average price of $4.49/share. While this is close to the current share price, PRPL’s operational performance and guidance have both improved materially. Coliseum’s stake increase followed a previous purchase of another 14% or ~$147m worth of PRPL stock in Dec’21. Previous stake increases were much more moderate – Coliseum ownership increased from 8m shares in Feb’18 to 17m in May’20, before shareholder sold down 7m shares in a secondary offering in May’21 (at $30/share). Large stake purchases since late 2021 might suggest that the equity holder has been positioning itself for a potential acquisition and might thus make a higher proposal.

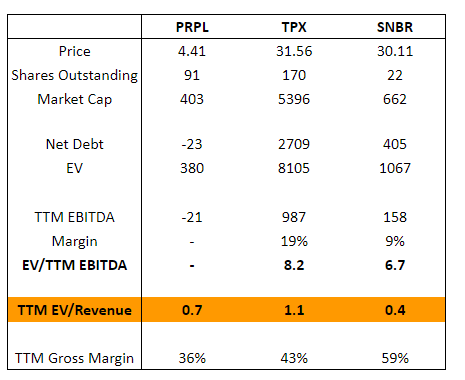

- PRPL currently trades at 0.7x TTM revenues – below closest though larger premium segment-focused peer TPX ($5.3bn market cap) which fetches 1.1x multiple. Though TPX has recorded higher TTM gross margins of 43% compared to 36% for PRPL and has had a higher market share (30% as of 2019 versus 4% for PRPL), PRPL’s sales have grown at a much faster 45% CAGR since 2016 compared to 9% for TPX. Moreover, TPX is much more levered at 2.7x net debt-to-EBITDA ratio compared to a net cash position of PRPL. Applying a 1x multiple to PRPL implies a price target of $7/share. Note that this is still 5x below 2021 peak stock price levels and 4x down from post-COVID peak revenue multiple.

- Even though PRPL’s earnings power is likely to remain suppressed in the short-term amid macroeconomic headwinds, the business has ample growth runway. PRPL is likely to continue expanding, capturing increasing market share in relatively fast-growing $20bn+ US mattress market. DTC sales are expected to benefit from rapid growth in showroom locations (up from 30 to 52 this year) which is still in its early stages. Meanwhile, in the last two quarters PRPL almost doubled its wholesale brick-and-mortar locations, adding around 2100 locations to a total of 4250. Moreover, PRPL is yet to tap into international expansion (only 2% of 2021 revenues) compared to peer TPX (21%). Coupled with recent cost savings efforts, these arguments suggest PRPL’s sales and earnings might be set to materially inflect going forward. Coliseum is clearly familiar with these dynamics and might thus not hesitate to make a higher bid here, more reflective of PRPL’s true prospects.

Purple Innovation Business and Financials

PRPL sells luxury/premium mattresses and beddings through e-commerce, retail showroom (both part of DTC segment) and retail brick-and-mortar wholesale partners (referred to as Wholesale segment). PRPL competes in the mattress market – which is generally a commoditized industry – through a differentiated product and brand. PRPL’s US mattress market share stood at 4% compared to less than 1% in 2016. Notably, the premium and mass premium mattress market segments – where PRPL operates – have seen their market share expand from 23% in 2015 to 30% in 2019.

Notably, PRPL acquired IntelliBed in Sep’22. IntelliBed produces gel grid mattresses – the company previously licensed gel technology from Purple for nearly 25 years. The acquisition is expected to result in synergies given geographic proximity between companies’ facilities as well as the fact that IntelliBed’s offerings will expand PRPL’s higher price point offerings.

Author’s calculations

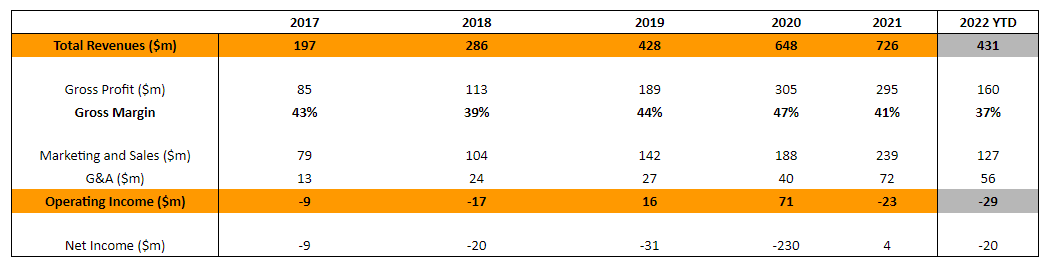

Financially, PRPL’s revenues have grown at a solid 12-50% pace since 2019 starting to normalize this year. Historical gross margins have ranged from 39% to 47%. The company has stated that in a normalized demand environment gross margins should reach 45% versus the current 36% – seems justified given historical performance. The management has also noted that Q3’22 EBITDA margin of 8.5% is likely to increase as well. Since Q1’22, PRPL has implemented numerous cost cutting measures, including headcount reduction and marketing spend decrease.

Relative Valuation

Company Filings

PRPL’s two closest peers are Tempur Sealy International (NYSE:TPX) and Sleep Number Corp. (NASDAQ:SNBR). Unlike PRPL, SNBR sells vast majority of its mattresses through its own stores. Meanwhile, TPX, similarly to PRPL, sells through wholesale and DTC segments, suggesting it is a better reference point when valuing PRPL. TPX’s TTM gross margins have stood at 43% – in line with PRPL’s historical and expected normalized margin levels. While TPX is admittedly larger, the comp is also more levered compared to PRPL’s net cash position, suggesting valuing PRPL at 1x revenues might be the appropriate multiple.

Coliseum Capital Management

Coliseum Capital is a small investment firm, holding several other COVID beneficiaries (e.g. major shareholder in LAZY). PRPL is its 3rd largest position. Coliseum was a participant in the PRPL’s PIPE during PRPL’s listing through a SPAC in 2018. Notably, Coliseum used to lend funds to PRPL at high interest rates – 12% per the 2018 credit agreement.

Conclusion

PRPL currently presents a compelling higher offer investment thesis. Given relative valuation, Coliseum’s stake increases since late 2021 and PRPL’s growth runway, I expect Coliseum to make a higher bid here at a premium to current market prices.

Black Friday Special – Limited time FREE TRIAL

For the next few days only I am opening my premium service for FREE TRIALs – new subscribers can explore SSI at no cost for two whole weeks. The offer expires on the 30th of November. That’s a Black Friday special only, so grab this opportunity while it lasts.

SIGN UP NOW and receive instant access to my highest conviction investment ideas + premium weekly newsletter.

Be the first to comment