Sundry Photography

Pure Storage, Inc. (NYSE:PSTG) offers organizations a leading cost-effective and efficient data storage solution that can assist them in lowering costs and improving long-term performance. PSTG maintains its leadership in the storage-as-a-service market; in fact, they recently released a new fully managed service for Portworx® Enterprise, which will provide users with a Kubernetes-ready data plane that can be simply integrated into their containerized applications. This will put the company in a good position to capitalize on opportunities in the rapidly growing Kubernetes market, which is being driven by increased adoption of cloud-native apps and automation of data management.

PSTG also highlighted their continuous market share gain, as seen by their record customer base, and celebrated another record in its subscription annual recurring revenue. Finally, despite today’s macro headwinds, management continues to provide a favorable outlook for FY 2023 and remains fundamentally stable, making Pure Storage, Inc. stock appealing.

Q3 Overview

PSTG finished Q3 2023 with a solid performance. To begin, revenue increased to $676.1 million, up from $562.7 million in Q3’22. Second, the company announced a record subscription ARR of $1 billion. Third, it reported a record $1.6 billion in remaining performance obligations (“RPO”), up from $1.4 billion in Q4’22. PSTG has expanded its customer base to over 11,000 customers, of whom 58% are Fortune 500 companies, and has maintained a Net Promoter Score of 85.2%. Fifth, owing to its effective marketing spending, PSTG is able to boost its operating margin, as indicated in the image below.

PSTG: Improving Operating Margin (Source: Data from SeekingAlpha. Prepared by the Author)

Finally, despite the fact that Pure Storage, Inc. is still in its early stages of profitability, management is actively buying back its stock, as quoted below.

We would expect that share repurchase volume will increase next quarter. We have approximately $100 million remaining from our $215 million share repurchase program. Source: Q3’23 Earnings Call Transcript

In fact, Pure Storage, Inc. purchased 900,000 shares of their own stock for around $24.5 million this quarter. Finally, as seen in the image below, they continue to increase their cash flow from operations, which has contributed to their improving free cash flow (“FCF”) margin.

PSTG: Improving FCF Margin (Source: Data from SeekingAlpha. Prepared by the Author)

In fact, looking at Pure Storage, Inc.’s trailing Price/Cash Flow of 11.91x and compared to its sector’s median of 19.23x, it presents a positive catalyst.

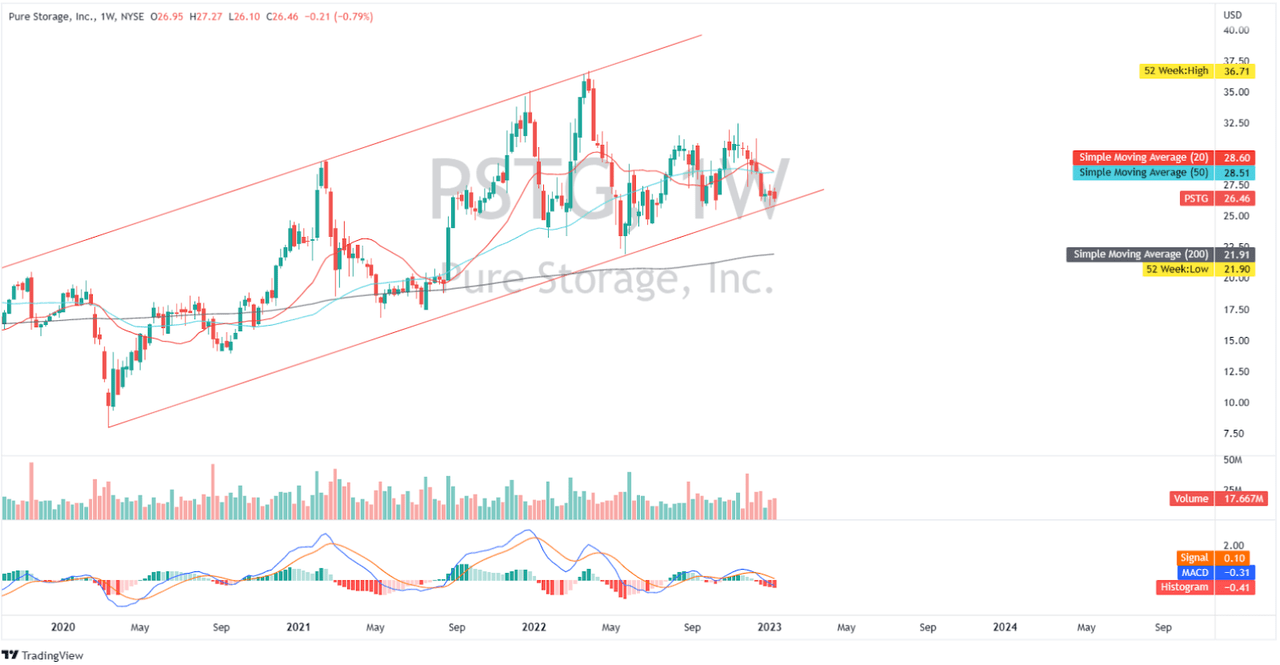

Trading Near Logical Support

PSTG: Weekly Chart (Source: Author’s TradingView Account)

PSTG is near the lower trend line at the upward channel, as indicated in its weekly chart, suggesting that we might see some bounce here. However, its MACD signal (below its Signal Line) and the potential 20-day crossing below its 50-day simple moving average indicate that negative pressure remains. So, if the price breaks around $25, I will be wary. If this occurs, I believe the next solid support to monitor is around $21.

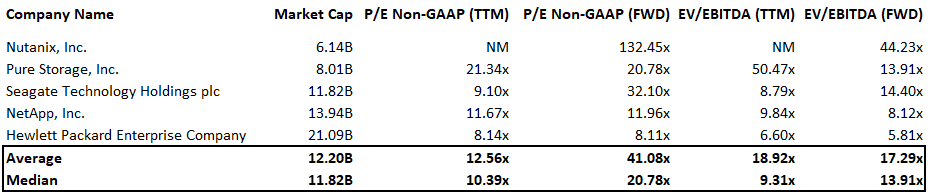

Fairly Valued

PSTG: Relative Valuation (Source: Data from SeekingAlpha. Prepared by the Author)

Peer group: Nutanix, Inc. (NASDAQ:NTNX), Seagate Technology Holdings (NASDAQ:STX), NetApp, Inc. (NASDAQ:NTAP), Hewlett Packard Enterprise Company (NYSE:HPE).

Looking at the image above, we can see that the peer group appears to have a negative analyst outlook, as seen by their 41.08x average forward P/E and 12.56x average trailing P/E. PSTG, on the other hand, trades at a trailing normalized P/E of 21.34x and a positive forward P/E of 20.78x, making it more appealing than the average peer at the time of writing.

While both HPE and Pure Storage offer storage solutions, PSTG is the only one that focuses on data storage solutions. In fact, PSTG trades at only $8.01 billion in market cap and is constantly gaining share in the storage market. According to management, they continue to lead the industry, as stated below.

Pure continues to lead the industry in product innovation having released a record number of new products and services this year, including FlashArray//XL, FlashBlade S, Pure Fusion, Portworx data services and Evergreen//Flex. We are proud to share that this innovation has once again been recognized with Gartner’s highest rankings in their magic quadrant, Pure was named the leader for the ninth consecutive year for primary storage and a leader for distributed file systems and object storage, significantly increasing flash blades ranking year-over-year. Source: Q3’23 Earnings Call Transcript

Moving forward, PSTG finally gaining some momentum towards profitability as shown in its forward EV/EBITDA of 13.91x.

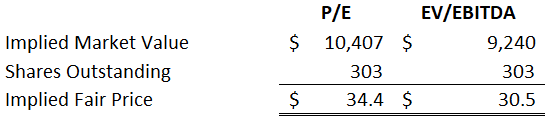

PSTG: Relative Valuation (Source: Prepared by the Author)

Using a conservative implied P/E of 38.84x and an implied EV/EBITDA of 16.57x, estimated earnings per share of $1.27, EBITDA of $525.43 million in FY’23, and a 10% discount, we can arrive at an average fair price for Pure Storage, Inc. of $32.5. This implied a reasonable discount to take into account. Additionally, considering the expert’s high expectations of $47, today’s consolidation seems to be a good time to buy. Caveat, this appears to be too optimistic, especially given a potential recession which may have an influence on the company’s strategy to maintain its share repurchase activities, which will have an impact on its valuation.

PSTG: Gross Margin and Revenue Growth Trend (Source: Data from SeekingAlpha. Prepared by the Author)

In fact, PSTG despite its effort to transition towards recurring revenue posted fluctuating growth figure and operating margin.

Conclusive Thoughts

Despite this, I believe Pure Storage, Inc. is now in a better position to achieve long-term profitability. In fact, management expects total gross margin to continue growing and sees no further benefit from the transitory variables listed below.

During the first half of the year, our operating profits also benefited from less travel, higher attrition and slower than anticipated hiring. We do not expect that our operating profits will continue to benefit from these tailwinds next year. Source: Q3’23 Earnings Call Transcript

In fact, management presented a bullish projection for its non-GAAP operating margin of 15.6%, up from 10.8% in FY’22 and 2.7% in FY’21.

Pure Storage, Inc. maintains a liquid Balance Sheet, especially considering its record cash and cash equivalents amounting to $795.9 million. Additionally, Pure Storage, Inc.’s total debt declined to $752.1 million, down from $915.4 million recorded in FY’22. With its expanding FCF catalyst, I expect we will see a continued share repurchase as well as some expansion plans aligning with its growing total addressable market in both storage and storage as a service. As a result, this excellent quarter overcomes the risks of a potential recession, making Pure Storage, Inc. an appealing investment as of this writing.

Thank you for reading and good luck!

Be the first to comment