JHVEPhoto

When PulteGroup, Inc. (NYSE:PHM) jumped 4.2% after reporting Q3 2022 earnings last week, I sifted through the transcript of the earnings call looking for the nuggets of good news that helped drive the gain. What I found was a sinking reality, recognizing a future of declining margins and sales. The presumed good news included the potential to hold on to share (in a declining market) and a strong balance sheet that leaves PulteGroup with ample flexibility to navigate the challenging market. Management cautioned analysts on the call: “The reality is that we can’t be margin proud, but rather, we need to protect our share of sales within the markets.”

During this housing downturn, PulteGroup will work to maintain market share at the cost of margins. The company is adding base price changes to its toolkit of incentives. Management announced it will find “price at a community level where we can sell homes. We will do the best we can to protect backlog, but we won’t sit on inventory.” With mortgage rates soaring to 7%, incentives like rate locks and mortgage buydowns no longer work well. Pulte must mark down base prices in order to move inventory and protect market share: “…we’ve really focused the majority of our energy on pricing to what we believe current market conditions are. So price rollbacks and price drops.”

According to Pulte, the results for Q3 “reflect the benefits of the strong demand and pricing conditions that existed at the end of 2021 and into the first few months of 2022.” Accordingly, there is little point in extrapolating insights from those numbers. They call out from a market in the distant past. Pulte’s guidance provided clues to the challenges ahead.

Guidance

Pulte guided down Q4 deliveries to 8,000 homes, which implies 28,263 for the year. This is significantly below the 30,000 to 31,000 range the company anticipated just one quarter ago. An increase in cancellation rates combined with lower demand and Hurricane Ian in Florida motivated the guidance reduction. Cancellations soared in Q3 to 24% from 10% in the prior year and 15% in the prior quarter. Management expects “that market dynamics will remain challenging for some or all of 2023” (I corrected transcription with earnings call recording).

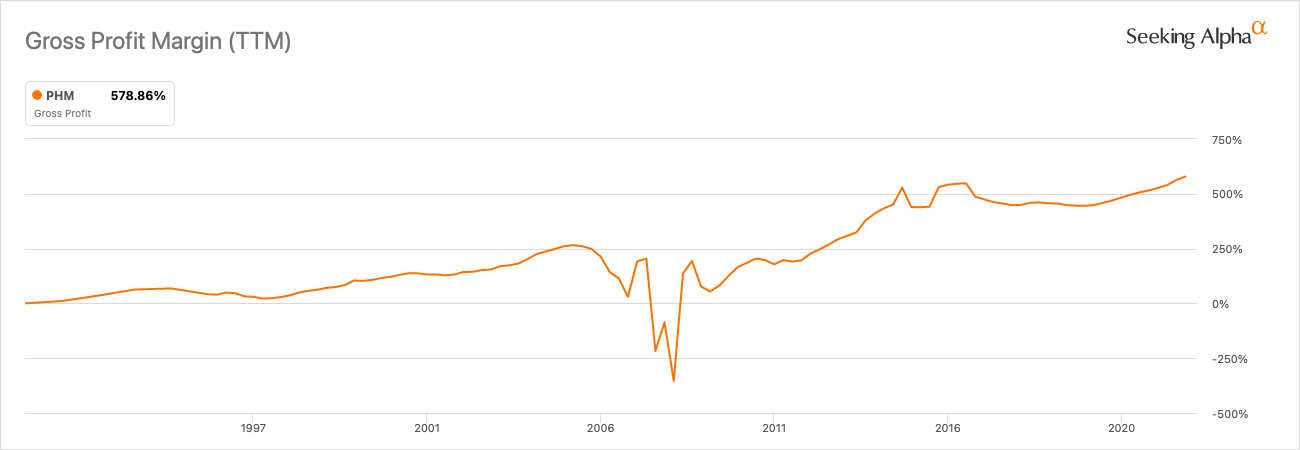

On the margin side, Pulte delivered the following guidance in Q2: “we are raising our margin guide for the third quarter and now expect to realize gross margins of approximately 30%. At the present time, we are maintaining our prior guide for fourth quarter gross margins to be in the range of 29.5% to 30%.” Pulte hit its guidance for Q3 with a 30.1% gross margin but dropped guidance to 28% for Q4 (a 120 basis points increase over the prior year). Given market conditions and Pulte’s strategy, these margins are likely to continue to decline. Fortunately, over the years, Pulte has worked margins up to company record levels. The company has room to maneuver.

Gross profit margin for PulteGroup, Inc. is at company highs after years of steady improvement. (Seeking Alpha)

Valuation

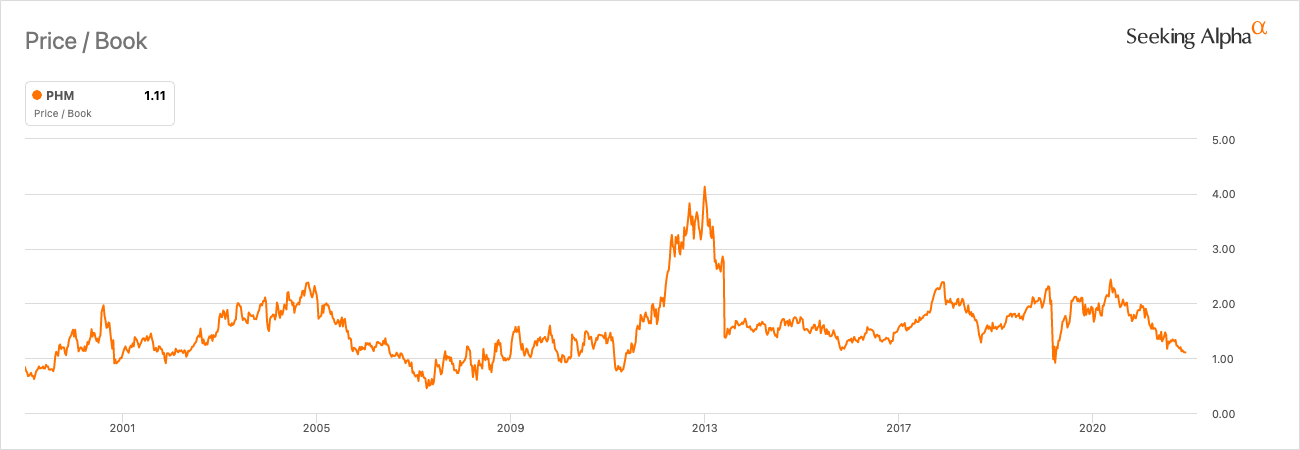

A 1.0 price/book ratio is considered typical recession-level pricing for home builders. While PHM’s price/book ratio has declined all year, it has not quite hit 1.0. Once price/book hits that level (or breaks below), shares start to look a lot more interesting. Note how PHM neatly bounced from around the 1.0 level during the brief pandemic-driven crash and pivoted around the 1.0 level during the housing crash of the Great Financial Crisis (‘GFC’). Of course, declining housing prices will force the stock to chase book value downward. Pulte guided to an ASP (average sales price) of $550-$570K, representing a 15% year-over-year increase at the midpoint. However, the company also acknowledged that “ASP is likely to come down.”

Price/book has steadily declined to historic lows and recession-level pricing. (Seeking Alpha)

Capital Allocation

Home building is capital intensive, so one of the big positives from Pulte’s conference call was to hear that the company has flexibility in its options for capital allocation thanks to good balance sheet management and a pullback in land spend. Pulte anticipates land spend dropping “materially” next year after walking away from $24M in deposits and pre-acquisition land spend and $800M in previously planned spend on land.

Management will review the dividend, extend its share repurchases, and examine leverage. Pulte has $291M In cash and spent $975M in the first 9 months of the fiscal year buying back stock, including $180M in Q3 (at an average $41.2/share, right around current prices). The last two years have been a bonanza for shareholders, with Pulte allocating $1.045B in 2021 and $1.084B so far in 2022 to share repurchases and dividends. Ongoing positive cash flow could provide a lower buffer for PHM.

Demand Environment

Pulte experienced a significant decline in the demand environment. Net new orders fell 28% year-over-year. Absorption rate fell from 3 homes per month a year ago to 2 homes per month in Q3. This decline compares unfavorably to the 17.6% nationwide year-over-year decline in new single-family home sales.

Pulte noted that the buyers still in the market want a home they can close in 30 to 90 days. The rise in mortgage rates is likely motivating the desire to move quickly. As a result, Pulte is increasing the spec homes it builds. This shift will make the company more vulnerable to falling demand, so they will have to tread carefully. With home builder sentiment on prospective sales back to levels last seen during the trough of the housing crash from the GFC, I expect Pulte to indeed proceed with caution.

Pulte reported that 65% of its units under construction were sold while the remainder went to spec. Pulte is moving fast relative to Q2 which started with just 64 spec homes. During that quarter, the company moved spec share up to 25-30% of construction.

The Trade

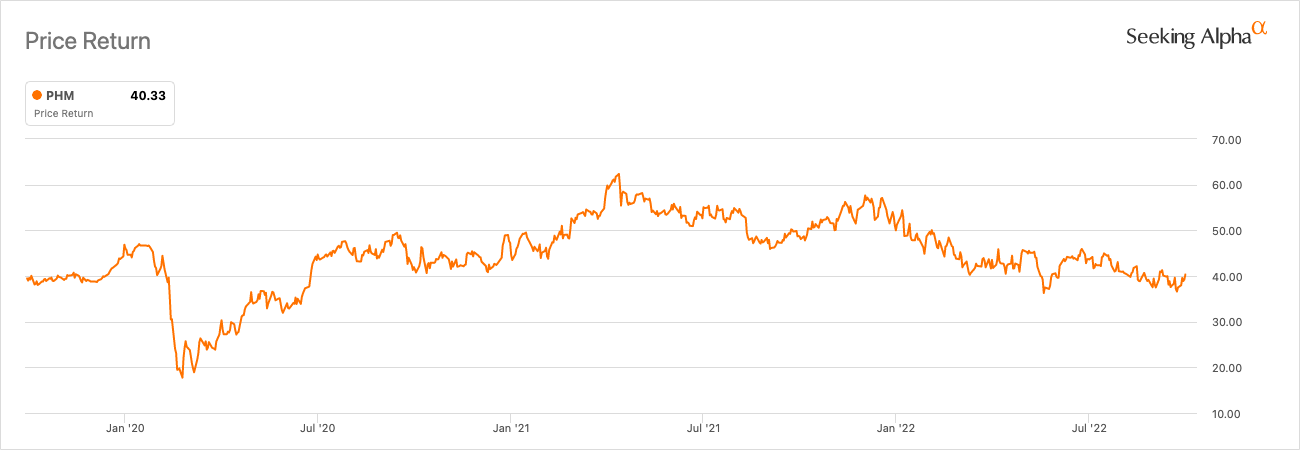

The current market environment puts my seasonal trade on home builders on hold for now. While PHM is enticing given its neat bounce from support at its June lows, I want to wait things out as long as possible into the seasonal cycle.

PHM bounced off the June lows as part of what looks like for now a multi-year pivot around the $40 level. (Seeking Alpha)

Be careful out there!

Be the first to comment