Vanit Janthra

Industrial giant Prologis (NYSE:PLD) is set to report Q4 earnings in the pre-market hours on Wednesday, January 18.

Since a prior analysis on the stock shortly after their Q3 release, shares have gained nearly 20%. This compares favorably to the 9% gain reported by the S&P 500 (SPY) over the same period.

Heading into earnings, however, the company faces an uncertain backdrop. Economists and most market participants broadly agree that there will be a recession in 2023, though the severity is debatable.

In addition, supply dynamics in the industrial market are shifting to a more oversupplied state. This is likely to increase vacancy rates, and consequently rents, in the coming quarters. In Q3, management conveyed a cautious tone and this tone will likely be reiterated in the current release.

A downbeat release could send shares lower later in the day. Any declines post-release, however, would make for an opportune time to add to current positioning or to initiate a new one.

Market Sentiment On PLD

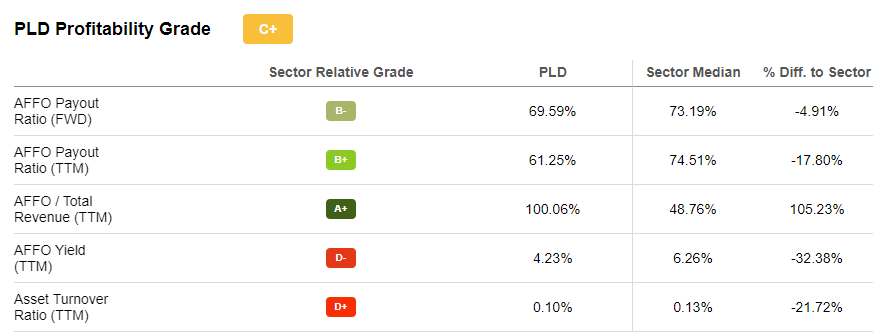

Seeking Alpha’s (“SA”) Quant system currently rates shares a “buy”, with “A” grades on all metrics, except on profitability and earnings revisions.

The poor grades on profitability, however, could be misconstrued due to the poor grades assigned to both the yield on adjusted funds from operations (“FFO”) and the asset turnover ratio. On profitability, these are not necessarily material, yet they are still contributing negatively to PLD’s score.

Seeking Alpha – Partial Snapshot Of PLD’s Profitability Metrics

A better gauge of profitability is EBITDA margins. And on this, PLD far outperforms the sector, with margins of 70% compared to 56% in the overall sector. In addition, at the end of September 30, 2022, PLD had a fixed charge coverage ratio of 13.9x, which signifies a superior ability of the company to service their debt obligations with reoccurring earnings.

Seeking Alpha – EBITDA Margins Of PLD Compared To Sector Averages

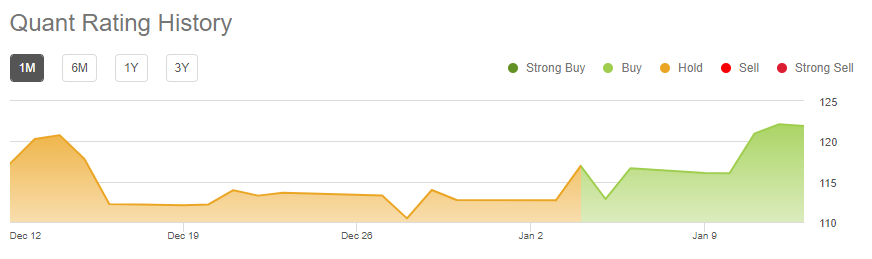

But despite the poor grading currently assigned to profitability, the quant system still has turned more bullish over the past month, with a re-rating from “hold” to “buy”.

Seeking Alpha – Quant Rating History Of PLD

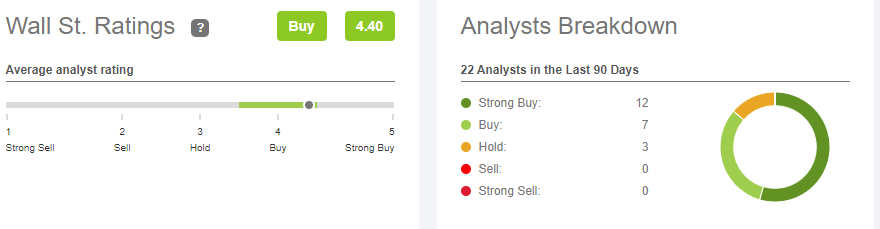

The positive sentiment is also reflected in SA Author sentiment, with most bullish on the stock. This is echoed by Wall Street but even more so. Over the past 90 days, 12 out of 22 analysts on the stock have rated it as a “strong buy”. Furthermore, the current average price target on the stock is about $137/share. This represents about 12% upside from current trading levels.

Seeking Alpha – Summary Of Wall Street’s Sentiment On PLD

Current State Of The Industrial Operating Market

According to a recent market report released by Cushman & Wakefield (CWK), the U.S. industrial market remained strong through 2022, despite a recent cooling in demand. In terms of net absorption, levels were the second highest in 2022, just behind the record set in 2021.

While overall net absorption declined 9.4% in Q4 from the quarter prior, it was still the ninth straight quarter where absorption held above 100 million square feet (“msf”).

Gross industrial leasing did, however, decline in Q4 by 28% and 37% on a QOQ and YOY basis, respectively. Still, for the year, the market logged more than 700msf of new leasing volume. This represents the second-best leasing year in history.

Nevertheless, the recent softening in demand is noteworthy, especially considering current supply dynamics. In Q4, new deliveries hit the market at a pace that was just 5.2% behind the pace set in Q3. This, in-turn, resulted in another quarter where supply outpaced demand.

As expected, this pressured rents during the quarter. Sequentially, average asking rental rates increased just 1% to $8.81psf. On a YOY basis, however, rents are still up 18.6%, which represents the strongest year for annual rent growth.

Despite the rise in new deliveries and the robust construction pipeline, there were signs of pullback in Q4. Construction starts, for example, fell during Q4 due in part to difficulties in securing financing.

For those projects currently under construction, 83% are currently speculative. As these projects begin to deliver through 2023, vacancy rates are bound to tick higher over the next several quarters.

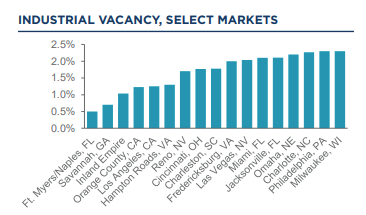

Already, the U.S. vacancy rate ticked up to 3.3% during Q4. Though that’s 20 basis points (“bps”) higher than Q3, it’s still 140bps lower than pre-pandemic levels and more than 300bps lower than the 10-year average of 6.5%.

While vacancy rates did tick higher nationally, in California, which is PLD’s largest market by share, rates continue to hold below 1.5%. This is likely to keep PLD’s overall occupancy rates within near-peak levels.

Cushman and Wakefield Q4 Industrial Market Report – Vacancy Rates By Select Markets

Looking ahead to 2023, the industrial market is likely to be characterized by excess supply growth over demand due to the expected number of projects set to deliver during the year.

This will likely increase vacancy rates, though not to the extent seen in earlier years, such as in the years following the Great Financial Crisis of 2007-2008. As such, the market will probably remain tight in 2023.

In addition, if the construction pipeline continues to fall back through 2023, this could again lead to a shortage of space and lead to another round of record-low vacancy just as companies are reentering the market.

What To Expect On PLD’s Earnings Release

On their Q3 earnings release, PLD maintained their guidance for average occupancy but increased their range for both same-store net operating income (“NOI”) and core FFO, excluding Promotes.

They did, however, reduce their starts guidance and signaled a more cautious approach to deployment in the coming months, with expectations for a greater share of build-to-suit projects, as opposed to those with a more speculative nature.

Lower fund contributions during Q3 were also an indicator of market uncertainty, specifically surrounding valuations. Questions also arose during the conference call relating to the risks of negative leverage, given current cap positioning in relation to market interest rates.

The potential impact of a slowing economic environment combined with an increasing supply outlook will likely be a topic of discussion in the current release. This will be paired with increased scrutiny on the company’s development pipeline.

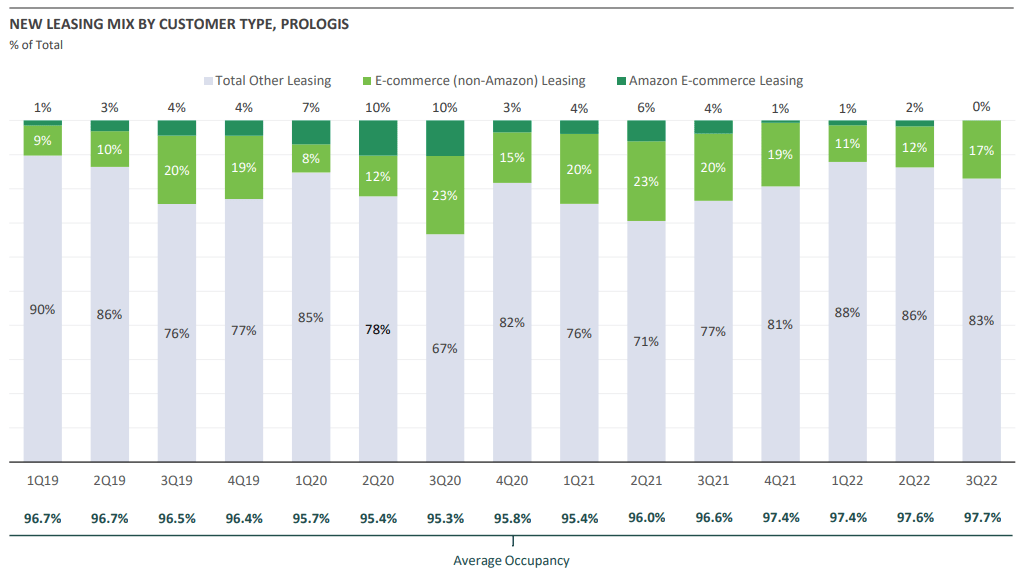

Givebacks or non-renewals from key tenants, such as FedEx (FDX) or Amazon (AMZN), will very likely be additional discussion items raised on the conference call, though this was addressed in the prior quarter.

At that time, PLD had experienced no givebacks by AMZN. And even if they were to lose some space, the churn wouldn’t be impactful simply because of the size of their overall portfolio.

While a pause in AMZN activity was noted, volume was offset by tenants other than AMZN. This contributed to overall activity that continues to hold above pre-pandemic levels.

November 2022 Investor Presentation – Summary Of New Leasing Mix By Quarter From Q1FY19

Why PLD Is Still A Buy

PLD is a global leader that operates in a league of their own. While it commands a premium pricing multiple of nearly 24x forward FFO, this is justified by the superior fundamentals of their business. The company operates in four continents and 19 countries and 2.5% of global GDP flows through their distribution centers.

While vacancy rates have ticked up in recent periods, occupancy still stands at near-peak levels of 97.8%. In addition, the company operates on low leverage and has ample liquidity of over +$5.0B. This positions them favorably to readily capitalize on market dislocations. And in addition to their current development pipeline, the company has an enormous land bank that can be tapped into for future growth.

Rising supply paired with moderating rents will likely instill fear in some investors. This may result in a pullback in shares following their Q4 earnings release. Any pullback, however, would be an opportune time to add to existing positioning or to build a new one. As one of the largest REITs operating in one of the strongest market sectors, PLD is worthy of a staple hold in any long-term-focused portfolio.

Be the first to comment