Thibault Renard/iStock via Getty Images

The Project $1M portfolio, is my effort to grow a fixed sum of approximately $275,000 into $1M within 10 years. The project was started at the end of 2015, and 2022 was the singularly worst year of the seven years since the inception of the portfolio.

The Project $1M portfolio is structured primarily as a buy-and-hold portfolio. Most core portfolio positions have remained intact since I first added them. The initial selection of positions was based on identifying dominant businesses with protected competitive positions with long runways to grow.

2022 highlighted some deficiencies with portfolio construction as the market aggressively punished a technology-oriented bias. Virtually all core Project $1M positions were sold down in 2022, with relatively little regard to underlying business strengths.

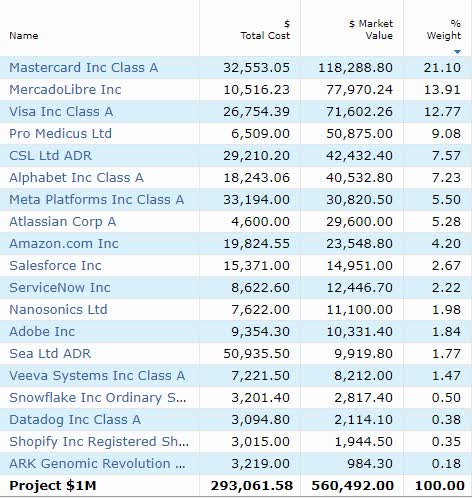

The bear market of 2022 had the effect of significantly concentrating the portfolio even further. The top 5 positions now account for nearly 60% of the portfolio.

An unfortunate effect of 2022 is that Visa (V) and Mastercard (MA) now account for greater than 30% of the overall portfolio! Both offered reasonable capital protection for the ravages of inflation in 2022, which is why I was content to keep both positions unchanged.

2022 in Review

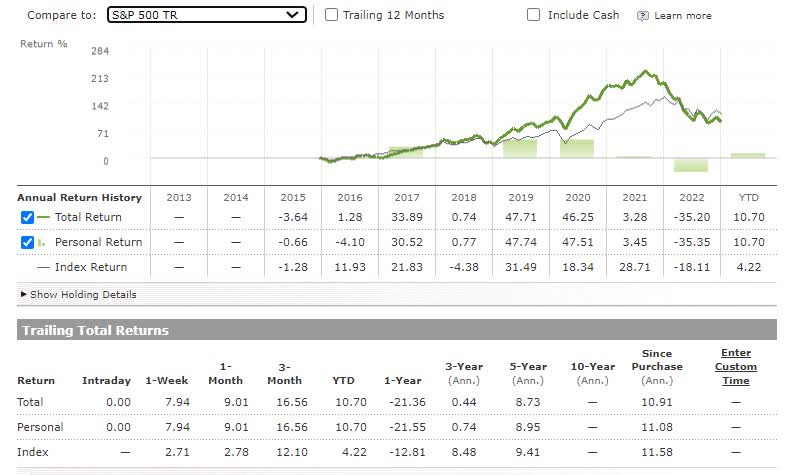

2022 saw a decline of 35% in the Project $1M portfolio value. The portfolio underperformed the S&P500 for the year, in a significant way, which only declined 18%. Still, over the cumulative seven years since inception, the Project $1M portfolio only slightly trails the S&P 500, in spite of the relative underperformance of the last two years,

Project$1M, Morningstar.com

There weren’t many highlights in the portfolio to write home about. Every single holding within the Project $1M portfolio declined for 2022. The best performers in the portfolio were MasterCard and Visa, which had a comparatively good performance last year, declining only 3% each.

CSL (OTCPK:CSLLY) was also a relatively good performer, declining only 7%. Unfortunately, every other component within the portfolio had double-digit declines. The worst offenders were Sea (SE) and Shopify (SHOP), which declined by more than 70% last year.

Project $1M, Morningstar.com

Table created by Author includes Veeva (VEEV), ServiceNow (NOW), Alphabet (GOOGL), Meta (META), Adobe (ADBE), Amazon (AMZN), Salesforce (CRM), Nanosonics (OTCPK:NNCSF), ARK Genomic (ARKG), Pro Medicus (OTCPK:PMCUF).

No downside protection from advertising leaders

Unfortunately, Alphabet and Meta did not hold up as well as I expected, down 40% and 65% for the year, respectively. These businesses were meant to serve as defensive positions, with their dominant market shares, competitive advantages, and continuing tailwinds to digital advertising. The relatively attractive valuation was intended to serve as an anchor for the volatility of the portfolio’s other positions.

Unfortunately, Apple (AAPL) and the Fed had other ideas. Apple’s move to require users to opt-in to share data with applications on the iPhone upended Facebook’s mobile data collection and attribution practices, something from which it still is yet to fully recover.

Apple’s expansion of its own advertising business and a generally skittish advertising market brought about by some of the most rapid interest-rate tightenings in history resulted in neither Meta nor Alphabet providing the defensive attributes for which I had included them into the Project $1M portfolio.

Sea is no MercadoLibre

Still, 2022 exposed some errors of inclusion. I added Sea Limited to the portfolio in 2021. My rationale for the business was that it could be another MercadoLibre, (MELI) dominating the space for e-commerce, digital payments, and digital advertising in a similar manner as MercadoLibre does in South America, albeit in Southeast Asia. I was aware of the more competitive environment and Sea’s heavy dependence on its gaming business.

Still, the gaming business was profitable and growing and was being used to funnel profits into its e-commerce and financial services businesses. My decision to add Sea also coincided with my exit from Alibaba (BABA) and Tencent (OTCPK:TCEHY), neither of which I felt comfortable owning, given the shifting regulatory landscape in China.

Unfortunately, reopening in Southeast Asia has eroded the profitability and demand in Sea’s gaming business without a transition to profitability for either the Shopee e-commerce business or the mobile financial services business during the same period.

While there is still opportunity for Sea, given its large cash balance, it’s an inferior, less dominant business. The lesson learned here is that caution must be exhibited in believing that a clone can be anywhere as good as the original. I have no plans to dispose of the Sea holding, but will not invest any more capital into this position either.

Staying on the course is hard

I opt for a very low churn posture in the management of capital. That means no chopping and changing positions to the extent they continue to perform and execute. In most instances, there was very little fault that I could see in the core performance of portfolio positions, although many declined more than 50%. 2022 was an interesting psychological test. Should the adverse macroeconomic conditions (including high inflation) revert, then I believe this strategy will be well-founded.

Yet, it was not mentally easy to hold this view through 2022, as profitable, growing positions with sustainable advantages were pummelled by the market.

What will 2023 hold?

I made some new additions to the portfolio in 2022 that I plan to build on through 2023. I finally added Shopify, Datadog (DDOG), and Snowflake (SNOW) to the portfolio. I view them all as high-quality, emerging businesses with the potential for substantial cash generation and profitability over the next few years. I am to make these positions larger with time.

With the battle on inflation primarily won by the Federal Reserve, and my expectations for inflation to start winding down towards a sub 3% rate over the next 12 months, I will gradually pair back my holding in Visa in favor of additional investment into other holdings, some of which will include these new additions in 2022.

I don’t believe 2023 can be any worse than 2022. I believe it will be substantially better for the portfolio. In the new year, businesses like MercadoLibre have found a tailwind from the alleged fraud and irregularities discovered with significant competitor Americanas.

Businesses like ProMedicus continue to win substantial new clients and see significant renewals of existing deals with multi-year terms. Finally, high-quality recurring revenue businesses like Atlassian (TEAM) have demonstrated the willingness and ability to put through significant pricing increases on core products. This will improve revenue and profitability over the next few quarters and confirm these businesses’ high switching costs and competitive position with their customers.

With portfolio position valuations an order of magnitude lower than they have ever been within the Project $1M portfolio, I still retain optimism that the portfolio’s goal can still be achieved in the last three years, before the end of 2025.

Bring on 2023!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment