Joe Raedle

Introduction

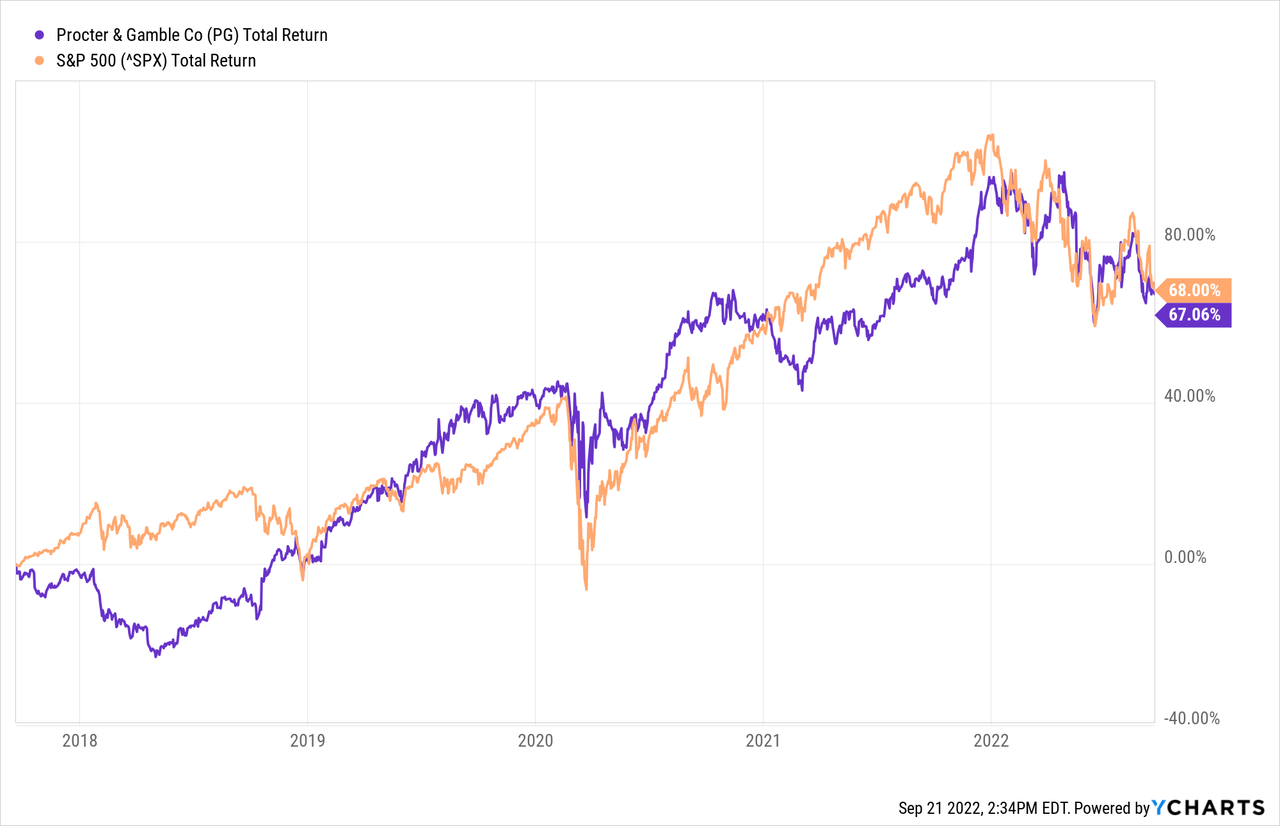

Procter & Gamble (NYSE:PG) has experienced strong growth over the past 5 years. The total return is comparable to that of the S&P 500. The company falls into the consumer goods industry, a defensive one. Procter & Gamble is one of the largest in this field, allowing it to pass the high inflation costs on to their customers.

Procter & Gamble is Ray Dalio’s largest exposure in Bridgewater, and other investors also own Procter & Gamble stock.

In my opinion, the stock is worth buying because it can withstand the inflationary period well, the company pays dividends and repurchases consistently, and the valuation is reasonably in line.

Company Overview

Procter & Gamble has been around since 1837 and has grown to become one of the largest consumer goods companies in the world with over $80B in sales. Many brands are known to the public not only in the United States but also internationally.

In general, consumer goods are quite competitive. Consumers are picky and remain sticky to their product. Procter & Gamble offers defensive consumer goods and is divided into the following 5 business segments:

- Beauty:

- Conditioners, shampoos, styling aids, and treatments

- Head & Shoulders, Herbal Essences, Pantene, and Rejoice brands.

- Antiperspirants and deodorants, personal cleansing, and skin care products:

- Olay, Old Spice, Safeguard, Secret, and SK-II brands.

- Conditioners, shampoos, styling aids, and treatments

- Grooming:

- Shave care products and appliances

- Braun, Gillette, and Venus brand names.

- Shave care products and appliances

- Health Care:

- Toothbrushes, toothpastes, and other oral care products

- Crest and Oral-B brand names.

- Gastrointestinal, rapid diagnostics, respiratory, vitamins/minerals/supplements, pain relief, and other personal health care products

- Metamucil, Neurobion, Pepto-Bismol, and Vicks brands.

- Toothbrushes, toothpastes, and other oral care products

- Fabric & Home Care:

- Fabric enhancers, laundry additives, and laundry detergents

- Ariel, Downy, Gain, and Tide brands.

- Air care, dish care, P&G professional, and surface care products

- Cascade, Dawn, Fairy, Febreze, Mr. Clean, and Swiffer brands.

- Fabric enhancers, laundry additives, and laundry detergents

- Baby, Feminine & Family Care:

- Baby wipes, taped diapers, and pants

- Adult incontinence and feminine care products

- Always, Always Discreet, and Tampax brands

- Paper towels, tissues, and toilet papers

- Bounty, Charmin, and Puffs brands.

PG Earnings Figures And Outlook

Procter & Gamble has grown well in recent years, with an average revenue growing 4.7% annually over the past 4 years. Non-GAAP earnings grew on average 8.3% over the same period. Excellent growth, the EPS growth is partly made possible by their share buyback program.

Inflation is an important theme in 2022, and Procter & Gamble can pass on the higher costs in their products. Procter & Gamble has increased their prices by 8% and recent quarterly figures show that revenue came in $110M above expectations. However, their gross margins have been hit by higher commodity and freight costs. Reduced sales in Russia and lockdowns in China also affected the result.

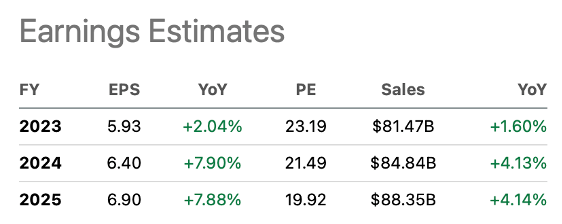

The outlook for fiscal year 2023 was disappointing. Revenue growth of 2% and EPS growth of 4% is expected for fiscal year 2023. Expected EPS is 1.3% below what analysts expected.

Nevertheless, I see it positively, the EPS growth has been adjusted downwards, but the expected EPS growth for the coming years is still a solid 7%.

Earnings estimates (SA PG Ticker Page)

Procter & Gamble can price inflation in their products, and I expect the higher costs (raw material costs and freight costs) will be corrected.

Shipping rates are expected to fall further. It is currently 3x more expensive to ship a container from Shanghai to Los Angeles. This is mainly due to the huge imports we saw this year.

Freight costs are expected to fall less sharply than those of sea shipping. Truck companies can’t expand their truck fleet because the chip shortage slowed truck production. As a result, transporters have to transport a larger amount of products with the same number of trucks. Even if demand declines, I expect truck costs to fall only slightly.

Overall, higher transportation costs impacted Procter & Gamble’s results. Procter & Gamble can pass these costs on to their customers. Because the company has an incredible amount of well-known and trusted brands in their portfolio, I don’t expect them to lose market share. Also, every consumer goods company has the same problem with rising costs.

Management remains focused on delivering value for the customer, the company and their shareholders. Proctor & Gamble is shareholder friendly and they show that by paying a high dividend and buying back shares.

Dividends And Share Repurchases

Procter & Gamble is known for its consistent dividend payments. Over the past 10 years, the dividend has increased on average 5.1% annually. The dividend is now $3.65, which equates to a dividend yield of 2.7%.

Dividend Growth (PG SA Ticker Page)

The dividend is well backed by Procter & Gamble’s free cash flow. The dividend payout ratio, in this case calculated with free cash flow rather than profit, is around 0.65 this year. The dividend is sustainable for the coming years.

|

Year |

Dividend $ in B |

Repurchase of stock $ in B |

Net income $ in B |

FCF $ in B |

Dividend / FCF |

|

2018 |

$ 7.30 |

$ 7.00 |

$ 9.80 |

$ 11.20 |

0.65 |

|

2019 |

$ 7.50 |

$ 5.00 |

$ 3.90 |

$ 11.90 |

0.63 |

|

2020 |

$ 7.80 |

$ 7.40 |

$ 13.00 |

$ 14.30 |

0.55 |

|

2021 |

$ 8.30 |

$ 11.00 |

$ 14.30 |

$ 15.60 |

0.53 |

|

2022 |

$ 8.80 |

$ 10.00 |

$ 14.70 |

$ 13.60 |

0.65 |

A share repurchase program is also part of returning profits to shareholders. Procter & Gamble has implemented a robust share repurchase program in recent years. In 2022, a total of $18.8 billion was returned to shareholders in the form of dividends and share repurchases. But since free cash flow is $16 billion, it won’t be sustainable in the long run. I expect management to return their entire free cash flow to shareholders. In this case, a sustainable repurchase yield is 1.5%.

Valuation Metrics

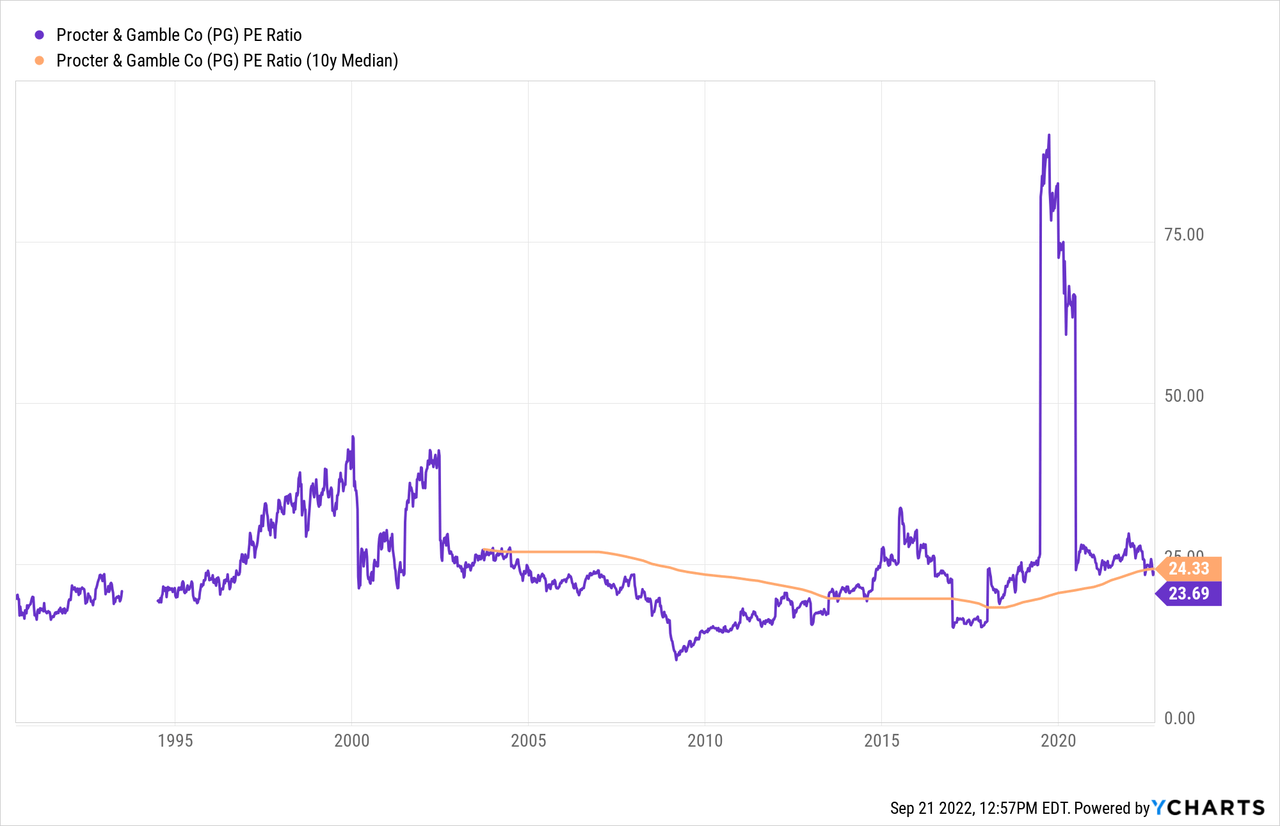

The valuation metrics keep insight in the stock valuation simple, the PE ratio is currently 23.7 and the 10-year median average is 24.3. This shows that the shares are slightly undervalued compared to the historical average.

More than 20 analysts expect non-GAAP EPS to grow in the coming years but are lowering their expectations. Earnings per share is expected to be $6.90 by 2025, at current stock price, this represents a forward PE ratio of 19.9.

If we assume the 10-year average PE ratio of 24.3, the share price will be $168 at the end of 2025. The current share price is $137, and including dividend, through the end of 2025, one can expect a pre-tax return of 31% (11% pre-tax return YoY).

The Fed is pursuing a hawkish policy to lower inflation. The 10-year government bond yield now stands at 3.6%. Procter & Gamble’s 10-year average PE ratio is 24.3 (inverse is 4.1%). Investors should ask themselves: should I choose a safe government bond with a yield of 3.6%, or should I buy PG stocks with an earnings yield of 4.1%, whose EPS is expected to rise about 7% per year in the coming years? PG stocks are more attractive, but EPS growth for the coming years is uncertain.

Still, I think Procter & Gamble is worth buying because it offers products from the defensive consumer segment, the company is expected to grow steadily and the stock valuation is attractive.

Conclusion

Procter & Gamble is one of the largest consumer goods companies in the world with sales of more than $80 billion. The company has a portfolio of many well-known brands. PG has grown strongly in both sales and profits in recent years, but the recent quarterly figures show a mixed result. The gross margin was disappointing due to higher raw material costs and higher freight costs. I expect these charges to be temporary. Due to the chip shortage, fewer trucks are being delivered. Truck companies must realize more transport with the same number of trucks. I expect this to be temporary. The size of PG allows it to pass on the higher costs to the customer. Management is shareholder friendly by paying a high dividend and executing a share buyback program. The valuation metrics show that the stock is undervalued compared to its historical valuation. This makes the stock worth buying.

Be the first to comment