cemagraphics

It’s been about 4 1/2 months since I wrote my latest piece on Prestige Consumer Healthcare Inc. (NYSE:PBH), and in that time, the shares are up about 30% against a gain of about 1.4% for the S&P 500. While this is a positive outcome, obviously, I need to review the name again, because shares priced at $65.85 are definitely more risky than those same shares were at $50.60. I need to decide whether or not it makes sense to add to my position, continue to hold, or take my profits and walk away. I’ll make that determination by looking at the updated financial history here, and by looking at the valuation.

You’re a busy crowd, and, being the considerate soul that I am, I want to be mindful of your time. For that reason, I include a thesis statement in each of my articles. This is for those people who want a bit more than what they glean from a title and three bullet points, and who also leap to the second paragraph of the article. In this thesis statement, I offer you the highlights of my thinking. This saves you time, and insulates you against some of the more egregious elements of my articles. You’re welcome. I think Prestige Brands grew very nicely over the pandemic, but that growth has obviously slowed. Although I’m very impressed by the dramatic improvement in the capital structure, I don’t think this stock deserves a “growth” premium price. The shares are expensive in my view. The last time they reached current valuations, they went on to underperform. While this isn’t the same company as it was back then, I think the growth has slowed here, and I think the valuation should reflect that. It doesn’t. Finally, while I did well by selling put options previously, I can’t recommend selling puts at the moment, because the premia on offer isn’t worth it. The July 2023 puts with a strike of $50, for instance, are bid at $0. Thus, I must wait for what I consider to be an inevitable correction from current levels before buying back in.

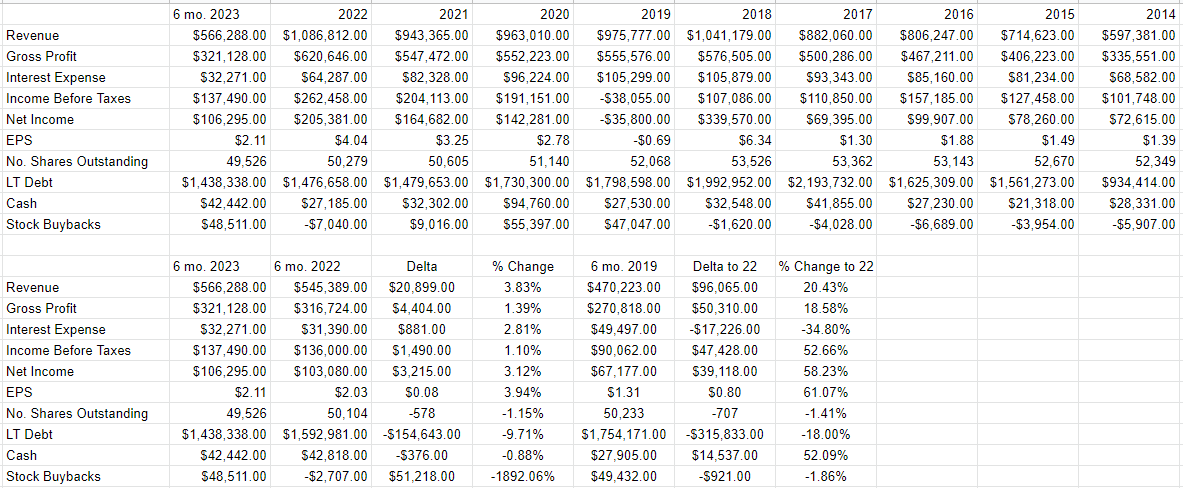

Financial Snapshot

The company grew very nicely last year, but hasn’t really budged since then. Thus, I’m increasingly of the view that this is no longer a growth company. Consider that revenue and net income for the first six months of 2022 was 20.4% and 58% higher than 2019 respectively. The growth between 2021 and last year had slowed to 3.8% and 3.1% respectively. Thus, I’m impressed by the fairly massive growth we’ve seen, but I don’t expect much from here. For that reason, I’m not going to be willing to pay “growth stock” valuations at the current time.

In the teeth of slowing growth, I’m happy to see that the capital structure has improved fairly dramatically over the past while. Specifically, long term debt is down fully 18% relative to 2019, and is down about 9.7% from last year. I think this de-risks the company fairly nicely.

So, I’d say that this company is becoming a bit of a cash cow, with fairly sclerotic growth, but the risk is being reduced. I’d be happy to add to my position, but only at the right price.

Prestige Brands Financials (Prestige Brands investor relations)

The Stock

My regular readers know that I consider the company and the stock to be very different things. If you’re new here, it’s time to let you in on this idea, too. I consider the stock and the company to be very different things. The company takes a number of inputs, adds value to them, and sells the results to someone else for a profit. The stock, on the other hand, is a traded instrument that reflects the crowd’s long-term views about the strength of the business. Additionally, the stock is affected by a number of variables that have little to do with the business, including changing interest rates, the crowd’s desire to own “stocks” as an asset class etc. In my experience, the only way to profit trading stocks is to spot discrepancies between the crowd’s views and subsequent reality. If the crowd is too pessimistic, for instance, it makes sense to buy and then ride the price higher as new information is eventually digested. I absolutely had to remind you about this, because doing so may come off as bragging, but that is basically the approach I took back in June of 2018 when I bought this stock before it went on to gain 75.5% against a gain of 47.4% for the S&P 500. At the same time, if the crowd is too optimistic about a company’s future, it’s best to avoid the name in my view. The level of optimism or pessimism in a stock is reflected in the valuation. If the crowd is optimistic, the shares are not cheap.

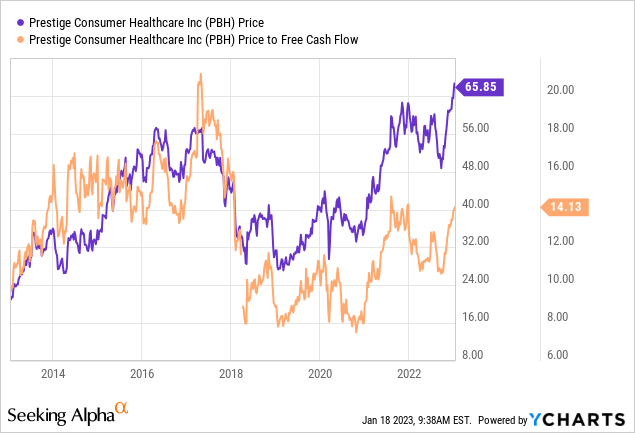

I measure the cheapness (or not) of a stock in a few ways, ranging from the simple to the more complex. On the simple side, I look at the ratio of market price to some measure of economic value, like earnings, sales, and the like. I want to see the shares trading at a discount to both the overall market, and to their own history. In case you don’t have your “Almanac of Doyle’s Trades” in front of you, I’ll remind you that I became indifferent about this investment when the price to free cash flow was 10.93. Fast forward to the present day, and we see that shares are about 29% more expensive per the following:

While I don’t think history necessarily repeats, I will write that it often rhymes. Whenever the shares have reached the current valuation anytime in the past, they’ve gone on to subsequently underperform. Although I’ll acknowledge that this is certainly a different company now, this fact doesn’t fill me with confidence.

In addition to looking at ratios, I want to try to work out what the market is “thinking” about a given investment. If you read my stuff regularly, you know that the way I do this is by turning to the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply some pretty basic math to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit opaque, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and we can infer what the market is currently “expecting” about the future.

Applying this approach to Prestige Brands at the moment suggests the market is assuming that this company will grow earnings at a rate of ~7.8% in perpetuity. I consider that to be a fairly optimistic forecast. Given the above, and given that I’m in the mood to preserve capital at the moment, I’ll be taking profits on this stock. I’ll buy back in if and when the valuation becomes reasonable again.

Options Update

In my previous missive I wrote about the fact that in addition to the gains I made on the stock, I earned an additional return on my investment by selling put options. Specifically, I sold the October 2018 puts with a strike of $35 for $1.55 each. I can’t deny that this was a not so subtle brag, but I think there’s also a lesson here. I added about 4% to my overall return by writing these options which were at the time fairly deep out of the money. Thus, if you haven’t yet considered short puts as a great way to enhance returns while reducing risk, I would recommend you familiarise yourself with these tools.

While I normally like to try to repeat success, I can’t in this instance because the premia on offer for reasonable strike prices is too low in my view. This often happens when shares are too richly priced. For example, the July 2023 put with a strike of $50 is currently bid at $0, for instance. For that reason, I can’t recommend selling puts until the shares inevitably fall in price from current levels.

Be the first to comment