shapecharge/iStock via Getty Images

This article was first released to Systematic Income subscribers and free trials on June 25.

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferreds and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the fourth week of June.

Be sure to check out our other weekly updates covering the BDC as well as the CEF markets for perspectives across the broader income space.

Market Action

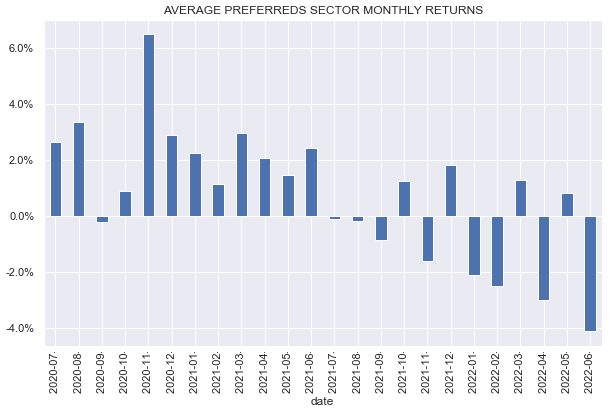

It was a good week for preferreds as nearly all income sectors were up. Recent flow data registered retail capitulation in equities and this likely washed out a lot of weak hands in preferreds as well, providing a firmer base for a recovery rally. In addition, a lower revision in University of Michigan inflation expectations as well as positive commentary from Fed’s James Bullard further supported income assets.

Despite the rally, however, June is shaping up to be the worst month since the COVID crash.

Systematic Income

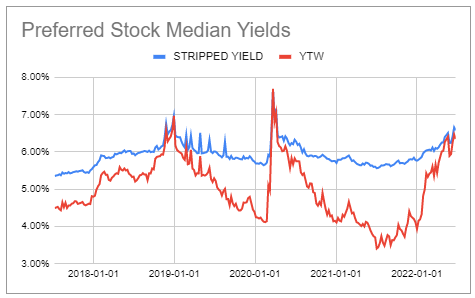

Preferred yields continue to trade at very elevated levels – due to an unusual rise in both Treasury yields as well as credit spreads. Interestingly, current yields are not far off the level of the previous Fed tantrum (the auto-pilot one) at the end of 2018. Stocks had also sold off by around 20% at that point also.

Systematic Income Preferreds Tool

Inflation is likely to remain fairly persistent so, while current yields are at attractive levels in our view, we shouldn’t expect the same kind of steady drop in yields as we saw over 2019. This suggests that investors may need to be satisfied with clipping coupons rather than expecting outsized capital gains going forward.

Market Themes

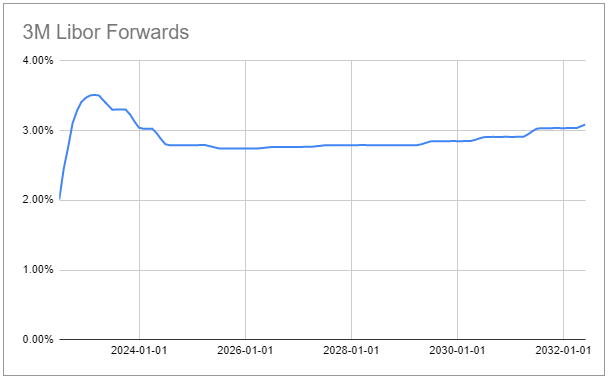

One thing that most investors can agree on is that short-term rates are going to keep rising as the Fed tries to get inflation under control. 3-month Libor has already risen to 2.15% which stands around 2% above its level at the start of the year.

However, what happens to short-term rates once the Fed is expected to reach the peak in its policy rate next year is unclear. Historically, the Fed has only stayed at its peak policy rate by 7 months on average. If inflation remains elevated we could see short-term rates remain range-bound. If inflation rises even further, short-term rates are likely to keep rising. And if, as the Fed appears willing to do, the economy enters a recession and inflation starts to subside due to a drop in demand, short-term rates are likely to move lower.

Market expectations are that Libor will peak around 3.5% then move lower to 2.8% and then remain range-bound around that level for the foreseeable future. This expectation is likely less a firm conviction in the exact path of short-term rates but more of a weighted-average across a very wide range of expectations.

Systematic Income Preferreds Tool

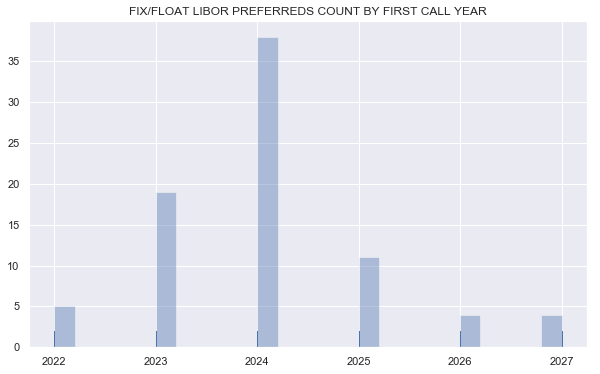

What is interesting is that the majority of Libor-based Fix/Float preferreds have a first call date sometime in 2024. In our view there is a clear potential downside for these preferreds.

Systematic Income

This is because short-term rates are less likely to keep rising in 2024 as they are this year and next. In fact, as seen in the chart above, the market consensus is for short-term rates to fall. The risk of recession is non-trivial and if this happens we could very well see a reversal of the Fed policy rate hikes. This will lower the coupon levels of 2024-reset preferreds. It will clearly also lower the coupon levels of 2022/2023-reset preferreds as well but at least these preferreds will have enjoyed a previous uplift in coupons as they would have reset to floating-rates at an earlier date.

What this means is that investors who are overweight 2024-reset preferreds may be exposed to lower income levels in case of a hard landing without having enjoyed the benefits of rising short-term rates. In our view, it may be worth diversifying the timing of the switch to floating-rates to near-term resets, which we highlighted earlier.

Market Commentary

Mortgage REIT Two Harbors Investment Corp (TWO) announced an authorization to repurchase up to 5m of its preferred shares (across 29m total A, B and C shares). This is good news for the preferreds. We shouldn’t expect all 5m to be bought back – possibly none will be bought – but, at least it demonstrates that the company is trying to maintain the quality of the preferreds by supporting their equity coverage. It’s also another example of how the interests of preferreds holders, at least in this case, are coming ahead of the common shareholders.

The company has previously supported preferreds by redeeming them despite their trading below “par”. They have also issued additional common shares which supports the equity / preferreds coverage.

The Q1 equity / pref coverage ratio for TWO preferreds was 3.5x – that’s not amazing, so it’s good to see the company potentially doing something to address this. It could also be an indication that agency mREIT (AGNC, ARR, DX, NLY, etc.) book values aren’t looking great in Q2 as TWO has an 80% allocation to agencies.

The positive for TWO is that its leverage is quite low at 4.7x among agency-focused mREITs. This is something that allowed its book value to do reasonably well over Q1 i.e. a 5.8% drop versus 15-16% drops for AGNC and NLY.

The TWO 8.125% Series A (TWO.PA) looks best in the suite at a 9.1% YTW to its 2027 first call date – after which it floats at 3mL+5.66%. We continue to hold the stock in our High Income Portfolio.

Stance & Takeaways

This week we rotated into the near-term reset mortgage REIT preferred Annaly Capital Management 6.95% Series F (NLY.PF) across two of our Income Portfolios. NLY.PF will soon take advantage of the baked-in rise in short-term rates given its reset to a floating-rate coupon in September. It also features a combination of modest leverage and high equity / preferred coverage in the agency-focused mREIT space. NLY.PF reset yield is 9.1% i.e. its stripped yield is expected to be this when it floats in September.

Be the first to comment