jetcityimage

Dear readers/followers

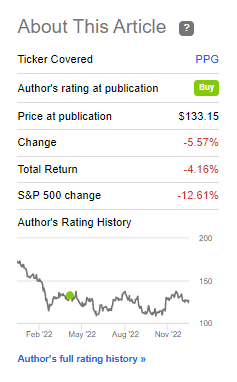

PPG Industries (NYSE:PPG) was actually one of my first COVID-19 discount articles. Traditionally, PPG trades at some impressive levels of overvaluation, but I went bullish on the company after a double-digit crash last year. The level and timing of that was, in hindsight, so-so.

PPG Industries Article (Seeking Alpha)

It wasn’t terrible timing – 4% isn’t that much when you consider the market did the equivalent of a massive hiccough in the meantime – but it’s also not the sort of undervaluation reversal that I was looking for at the time. Hence, my position in the company is slightly in the green, but only due to FX – otherwise, it would have been as negative as the picture suggests.

Let’s review PPG and see why the company hasn’t really been able to pick up.

PPG industries – Pressures and issues remain

The company hasn’t really been able to catch a break. After the fully justified overvaluation crash last year, SCM constraints, inflation, and other effects have been mercilessly pounding this company, despite PPG being able to mostly offset the worst effects by significant price increases for its products.

PPG is battling some fairly serious cost inflation issues due to its feedstock specifics. Despite near-$20M in savings, this wasn’t completely offset by positives during the last time I wrote about the company. The company’s expecting a double-digit adjusted EPS hit, which for PPG is somewhat rare. Currently, the severity for FY22 is expected to be a decline of about 11.5% – though I actually view this as a buying opportunity (more on that later)

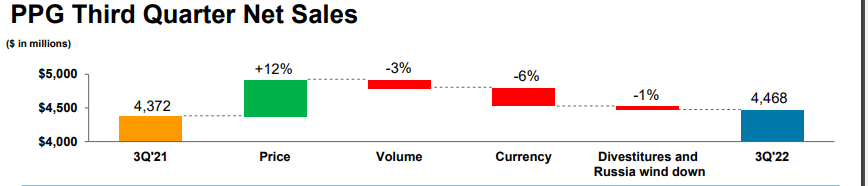

3Q22 results are what we have to go on here.

Sales were up 2%, and that’s with PPG pushing selling prices by 12%, as well as a significant 6% negative FX impact. The company is now experiencing slowing demand out of Europe and China, which is a situation we did not have to the same extent when I last wrote about the business.

The company still has significant backlogs of over $200M, coming in from aerospace and the auto-refinishing industry.

However, the costs for raw materials continue to increase – selling price continues to offset any and all cost increases, but unfavorable FX impacts the company’s results by more than $30M in 3Q22 alone, thus far. That’s more than any synergies by M&A’s and efficiencies managed to bring about, which is around $25M in overall savings.

Don’t get me wrong. Liquidity and other fundamentals remain very solid. The company has cut debt by over $400M, delivers operational cash flow of half a billion in a single quarter, and has $1.1B worth of cash at quarter-end. There are no fundamental worries for this company.

Instead, it’s all about the current pressures – because don’t forget, PPG had some Russian assets/sales as well.

PPG IR (PPG IR)

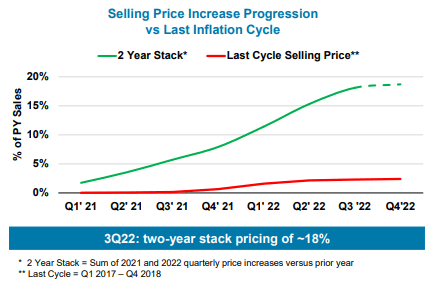

It’s all about how the company is hanging onto stable/slightly growing net sales simply by raising prices more and more, and for the time being, customers seem willing to accept this out of PPG. Their acceptance makes sense given the market situation and the company’s market position, but these price increases are very unfamiliar when looking at previous cycles and how they compare overall.

PPG IR (PPG IR)

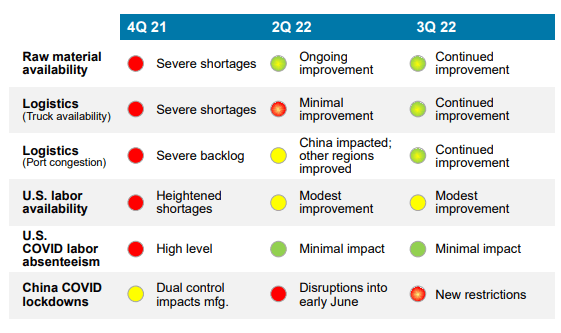

Also, let’s not beat around the bush and simply say that the company’s disruptions were severe (focus on were), but no longer are. There have been significant improvements since 4Q21 – and what’s more, regarding the China restrictions that we’re looking at here – we already know that they’re now cleared.

PPG IR (PPG IR)

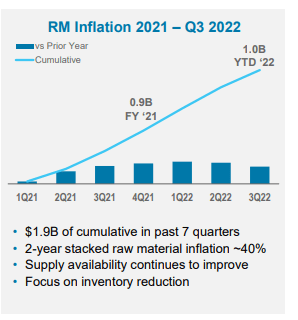

Still, I can almost understand why the market has been punishing the company as heavily as it has. Raw material inflation costs have been absolutely outlandish.

PPG IR (PPG IR)

And it doesn’t seem like they’re likely to stop increasing at this point either. The effects on the company’s segments are broad-based. From performance coatings to Industrial coatings – which by the way are the company’s two segments, we’re talking double-digit pricing increases. This did mean that we saw margin improvements as well, by almost 200 bps for industrial for instance, but we’re talking a 40% input increase, not even including energy cost increases.

There are some brighter spots to be had going forward. Demand for the company’s products remains at very strong levels, with every single sub-segment in the various company operating segments showing an increase in demand and sales, and the outlook remaining positive as well.

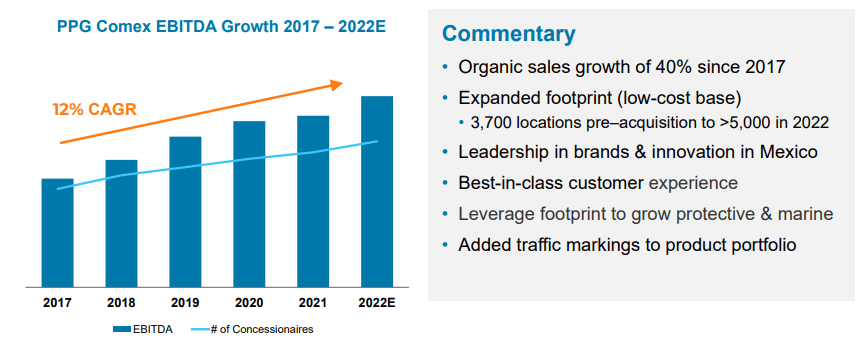

The company is also improving with PPG Comex, with strong EBITDA growth and an expanded footprint.

PPG IR (PPG IR)

The current company position and the case to be made for PPG is a balance between how much price increase the end market customers will accept, and for how long this will go on. Clearly, some price increase in accordance with the index is desired, and we want the companies we invest in to squeeze as much profit as possible from their products. But I understand the worries that are being expressed through the market valuation – where the company is bound to go for the next few years, and whether the company’s fundamentals will be enough.

As I see it, they will be.

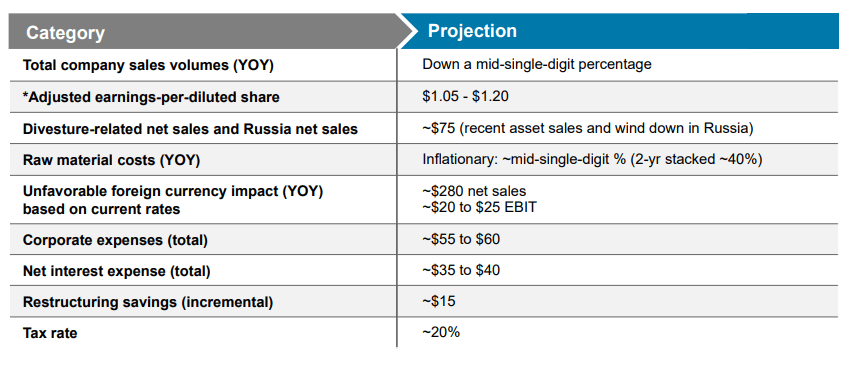

PPG remains BBB+ rated with extremely strong balance sheet metrics. And while debt is higher than 2020, the company is actively cutting it. Here are the company’s forecasts for the 4Q22 period.

PPG IR (PPG IR)

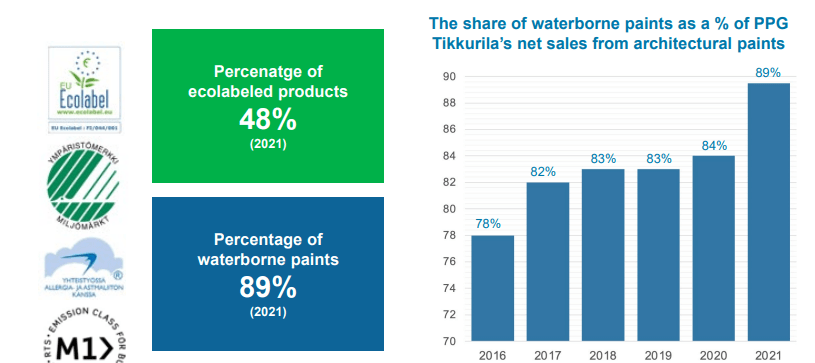

Perhaps more exciting for me as a Scandinavian investor is the company’s acquisition of Finnish Tikkurila Oyj. The company is a solid performer with a portfolio that’s very complementary to PPG’s existing portfolio, with over 350 third-party eco-labeled products, and 90% of Tikkurila’s paints that are waterborne. This company has roots that are older than PPG itself, and they’ve made paints for over 100 years, being Finland’s largest paint producer for a long time. Tikkurila was owned by Kemira (OTCPK:KOYJF), another Finnish company in chemicals that I own until it was spun off in 2010.

PPG IR (PPG IR)

Overall, I believe Tikkurila will make an excellent addition, and part of why I believe PPG will continue to outperform the markets for the foreseeable future.

Let’s look at PPG’s current valuation to see where we might be in 2023.

PPG’s valuation

PPG has been in the doldrums for most of 2022, owing to its fall from grace, or premium at the beginning of the year. However, 2023 is expected, at least currently, to bring about a reversal in this trend.

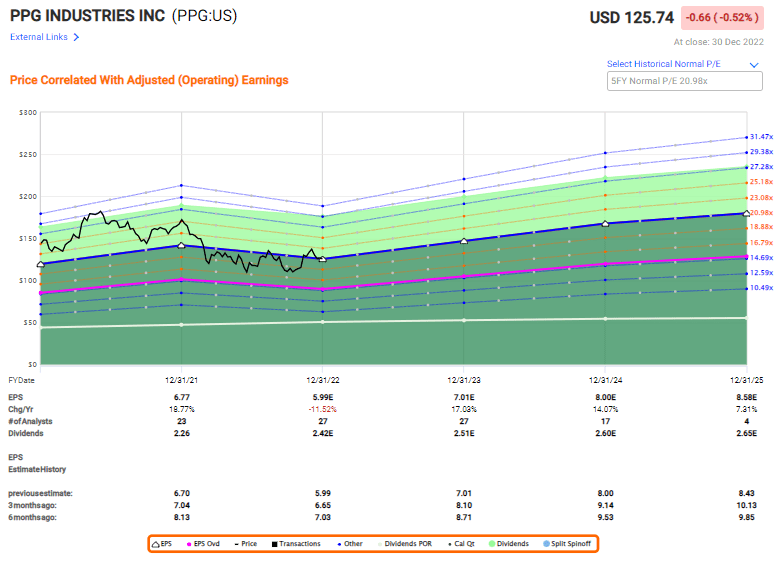

PPG valuation (FAST Graphs)

This company has a well-established pattern of going as low as 13-16X, and as high as 21-24X P/E. That means that buying at a 13-16X multiple, you can easily make as high returns as 50-80% on a safe business with a well-covered dividend and a credit rating of BBB+ by following these very simple valuation patterns/rules.

PPG is far from the only company where I try and do this, but it’s once where I actually saw success in this strategy, buying substantial amounts doing COVID-19. While I’m perfectly willing to hold stock in a “Forever” period, it bears mentioning that all companies can trade at multiples/ranges that are well outside their historical range.

That’s what happened to PPG and is also why I sold my stake in the company when it topped $175-$180/share.

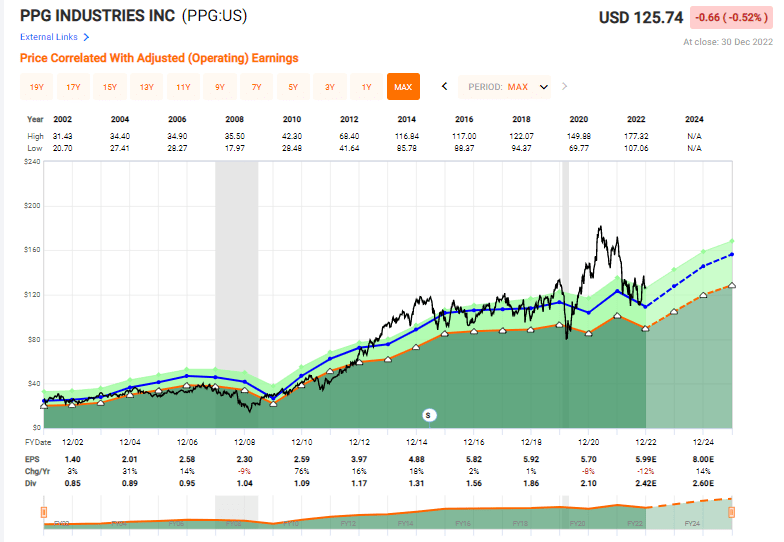

PPG valuation (FAST Graphs)

You don’t need to be a TA-oriented analyst to understand when a company is overvalued – it can help in fact, if you’re value-oriented, looking at things like averages over time, highs and lows, as opposed to current market trading flows.

I was back in when PPG crashed down – and while I haven’t been massively adding since then, I have been keeping my eye on PPG. The low dividend of sub-2% is holding me back, as was the expectation for 2022E, but now I’m slowly turning more positive on this company.

There are, simply put, always things to buy and always things that are expensive – it doesn’t matter what cycle/phase of the market we’re in.

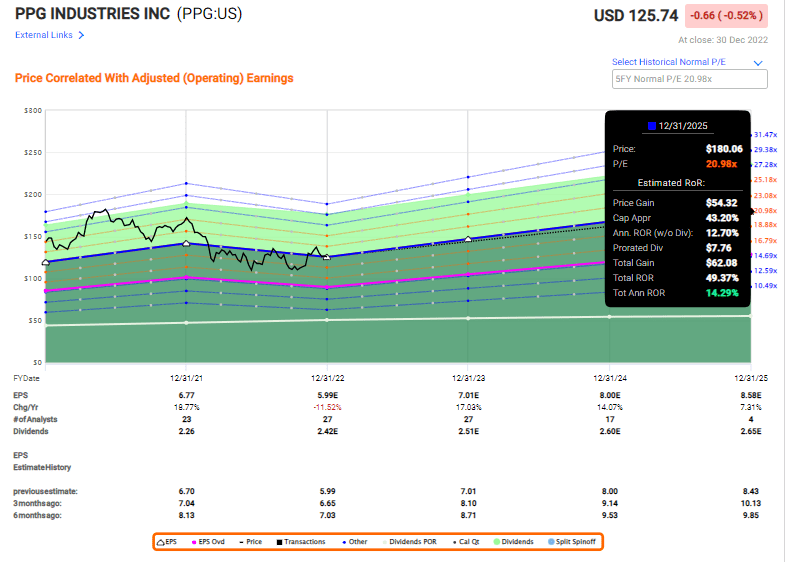

At 21x normalized P/E, the company is pretty much exactly trading at its 5-year average fair-value estimate, if we allow for the premium. My long-term PT for PPG was $160/share in my latest article, and this is a PT I’m sticking with based on a 2025E conservative 17-18x P/E range, despite the current 21x P/E being around $125. I believe the next couple of years will bring about significant EPS growth based on M&As, further pricing increases, but above all, demand normalization from key sectors.

Now, the fly in the ointment here is the recession potential. Then everything changes – and the potential for this is high.

That’s also why I’m not leaping to “BUY” PPG straight away, but more watching the company with increased interest, and willing to consider it a “BUY” if FX and opportunity line up (it doesn’t at the moment, FX is prohibitive for me).

PPG Upside (FAST Graphs)

So, where to go with PPG here?

Well, my PT remains – and $160 is for the long term. That makes the company a “BUY” at this time, and you could go for the common share in accordance with the thesis I present to you below.

Thesis for the common share

- PPG Industries is a quality company in chemicals/coatings. It has a solid history, good dividend growth, and very good fundamentals, despite an increasing debt due to M&A.

- At current valuations, there’s a very realistic upside to 2023-2025E based on market normalization in key segments, M&A/Integration synergies, cost savings, and increased demand. The risk is that these developments take longer or don’t materialize.

- I believe the likelihood is high that a company that’s been performing well for 20 years will continue to do just that. My thesis, based on this picture, is, therefore, a “BUY” with a PT of $160/share.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can’t call the company cheap based on current valuation trends for 2022-2023 – but I can call it attractive for the long term.

Thesis for Stock options

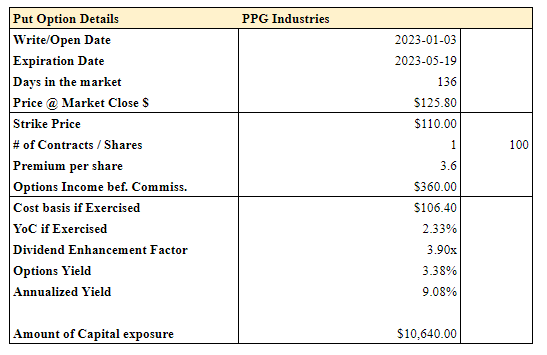

However, depending on intra-day trading and premium patterns, the current valuation dictates that PPG could be an appealing options play – if you’re willing to put the capital at risk. Given its share price, it’s a $10,000 play for a single contract.

Here is one I found at the market open today, the 3rd of January.

PPG Option (Author’s Data)

That’s a very good price, a nice 9% annualized RoR, and a better yield than you’d get today. As I see it, it’s better than buying PPG outright. If you’re feeling somewhat more risk-tolerant and want it to expire ITM, you could increase the strike to 115, which would see the premium at $4.6, annualizing at almost 12% instead.

That one would expire ITM with a high probability though, so keep that in mind.

Still, this is the route I would go for PPG – unless you’re constrained in terms of capital, then my PT holds.

Be the first to comment