cemagraphics

Since I put out the latest in a string of cautious articles on Polaris Inc. (NYSE:PII), the shares are down about 5% against a loss of about 7% for the S&P 500. The company has reported financials since then, so I thought I’d review the name yet again. After all, a stock trading at $103 is, by definition, less risky an investment than the same stock when it’s trading at $109. I’m going to decide whether or not it makes sense to buy at the moment by looking at these financial results, and by looking at the stock as a thing distinct from the underlying business. Lastly, I wrote some puts on this name last March which are hours away from expiring, and I’m champing at the bit to write about how that trade went.

Welcome to the thesis statement portion of the article. This paragraph is designed for those people who want a little bit more than what they can get with mere titles and bullet points, but far less than what they can get with an entire article jammed to the rafters with Doyle mojo. It’s my belief that Polaris shares are not yet cheap enough. The recent financial performance has been rather bad, as evidenced by the massive reduction in net income and the huge uptick in obligations, for instance. At the same time, it seems that the business is slowing, suggesting that valuation will look even worse in six months’ time. For that reason, I would recommend continuing to favour preservation of capital over taking a flyer on this name. Finally, I did well selling puts in March. In fact, the $4 I earned in put premia outperformed stock holders by about $10 since I put out my article. So this is yet another example of the risk reducing, yield enhancing potential of deep out of the money put options. Unfortunately, the premia on offer at the moment suggests that it’s not worth selling puts until shares inevitably drop in price.

Financial Snapshot

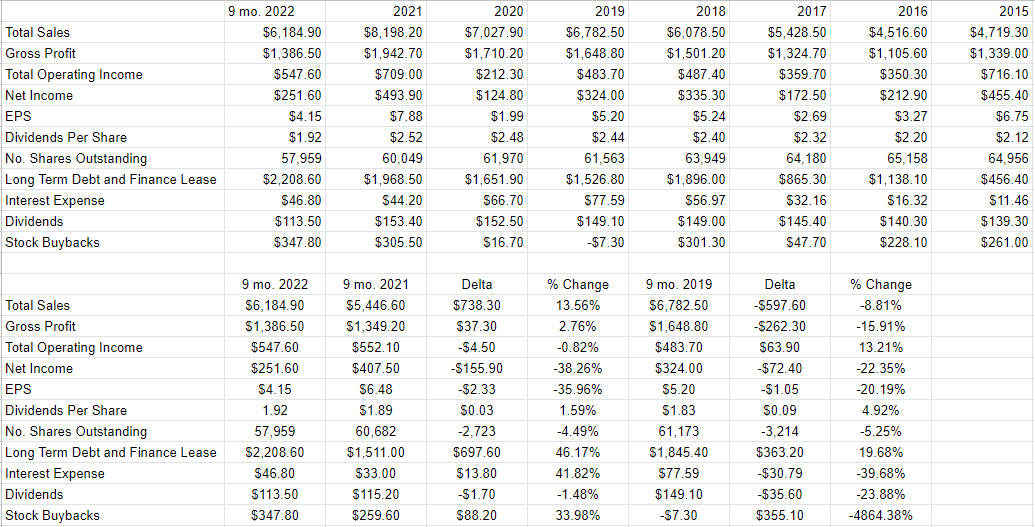

I think the most recent financial history here is “mixed to bad.” On the positive side, revenue for the first nine months of 2022 was about 13.5% higher than it was the same period in 2021. This is impressive in light of the fact that revenue in 2021 was a record high for the firm and was itself about 17% higher than sales were in 2020.

Unfortunately, that’s where the good news ends in my view. While revenue for the first nine months of the year was dramatically higher, net income absolutely cratered. Some of the blame can be apportioned to the fact that both R&D and G&A expenses increased by $17 million, and $17.9 million respectively. The most significant cause of net income reduction came down to the $142 million loss on the sale of discontinued assets. That written, even if we do what analysts sometimes do and wave away the impact of a $142 million loss because it’s not recurring, net income would have been approximately flat relative to the same period a year ago. This is hardly a stellar performance in my view.

The performance looks even softer when we compare this period to the pre-pandemic era. Revenue and net income in 2022 were lower than the same period in 2019 by 8.8% and 22.4% respectively. The company seems to have not yet recovered from the pandemic.

At the same time, the capital structure has deteriorated fairly dramatically. Specifically, long term debt and finance lease expenses have increased by approximately 46% over the past year. Long term debt is now at an all time high.

I should note that the poor stock performance happened in spite of the $347.8 million the company spent on buybacks during the first nine months of the year. To put this $347.8 million figure in context, it is about $42 million more than the company spent on buybacks throughout all of 2021, which was a record year for buybacks. I don’t mind buybacks in theory, but I don’t like them when there is debt to be paid down.

All that written, I continue to think that the dividend is reasonably secure, and I’d be willing to buy the shares, but only at a reasonable price.

Polaris Financials (Polaris investor relations)

The Stock

If you subject yourself to my stuff on a regular basis, you know that I consider the stock and the business to be distinct from each other. The business manufactures and markets power sports vehicles worldwide. The stock is a speculative instrument that gets buffeted by a host of factors, some of which have nothing to do with those activities. One of the things that affects the performance of a given stock, for example, is the crowd’s ever-changing views about the desirability of “stocks” as an asset class. There’s no way to prove this definitively, as it’s an obvious counterfactual, but it’s possible to make the case that some portion of Polaris stock’s drop in price since I last wrote about the name was a function of the 7.2% fall in the S&P 500..

So, this is why I consider the stock as a thing distinct from the business. The former is often a poor proxy for what’s going on at the company, and I think it’s possible to profitably exploit this disconnect. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. What I want to see in this regard is a stock that the crowd is somewhat pessimistic about that goes on to exceed expectations. When the crowd is pessimistic, the shares are cheap, which is why I try to buy only cheap stocks. So today the work involves deciding whether or not the shares are reasonably priced.

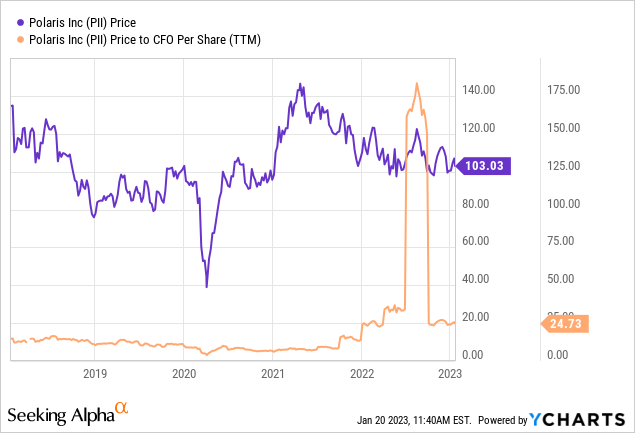

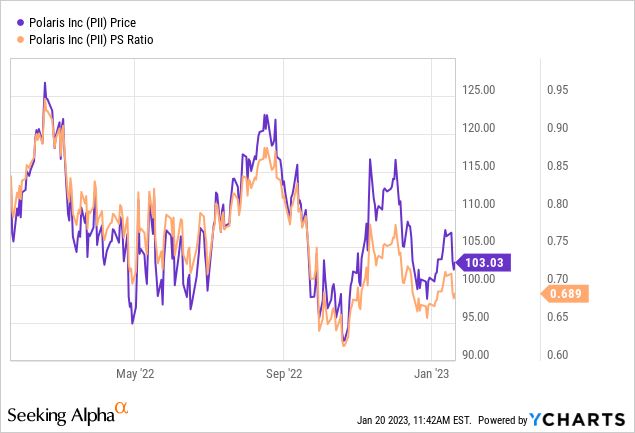

In my previous piece, in case you’ve forgotten, I remained cautious about this stock because the shares were trading at a price to CFO per share of about 22.8, and a price to sales ratio of about 0.82. This valuation was much worse than it was when I had looked at the name previously. Fast-forward to the present, and here’s the current lay of the land. The shares are now 8% more expensive on a price to CFO, but 15% cheaper on a price to sales basis, per the following.

Source: YCharts

Source: YCharts

My regulars also know that in addition to looking at ratios, I want to try to understand what the crowd is currently “assuming” about the future of a given company. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit too thick, you might want to crack the spine on “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future. Applying this approach to Polaris at the moment suggests the market is assuming that this company will not grow from current levels, which I consider to be a fairly pessimistic view.

Given the above, I think the shares are cheap, but are not cheap enough for me. For instance, although the stock is cheaper on a price to sales basis, investors are compensated for what’s left over after everyone else has been paid, making sales less relevant in my view. As I’ve written frequently recently, I am more inclined to preserve capital than I am to take on risk at the moment. For that reason, I’m going to remain on the sidelines.

Options Update

I’ve been selling deep out of the money puts on this stock for some time, and I continued that trend last March when I wrote January 2023 puts with a strike of $70 for $4 each. I considered this to be a very reasonable premium for selling puts that were at the time about 36% out of the money. This is one of those examples where the put seller actually outperforms the stock buyer. At the time I wrote my article, the shares were trading at about $109, so the stock holder has lost about $6 per share. The put seller has gained $4 per share, while taking on much less risk. I write about this to brag, obviously, but also to point out, yet again, the risk reducing, yield enhancing potential of short put options.

While I am a fan of trying to repeat success, I can’t recommend this strategy at the moment, because the premia on offer is too thin to make the exercise worth it. For instance, the September puts with a strike of $70 are only bid at $1.70 at the moment. This is ridiculous in my view, because this strike price is less out of the money than it was last March, while the premia is less than half of what I received at that time. For that reason, I must sit and wait for the shares to fall in price before I sell these.

Be the first to comment