Christopher Polk

PLBY Group’s (NASDAQ:PLBY) shift to a capital-light model is ongoing with its management targeting a marked shrinkage of its operating cost base and an extension of its currently dire cash runway. The Los Angeles-based company reported a cash and equivalents position of $24.9 million as of the end of its fiscal 2023 first quarter, down around $7 million sequentially from the prior fourth quarter as free cash outflow jumped to $23.4 million. PLBY’s issuance of new common stock worth $61.5 million meant it could close the liquidity gap that arose during the quarter as well as contribute to debt repayment of $45.4 million. I was interested in owning PLBY’s commons shortly after it went public in early 2021, but baulked at the valuation, flagging sales, and sustained unprofitability. The situation now isn’t so different from a fundamental perspective but the valuation has crumbled to mean another look.

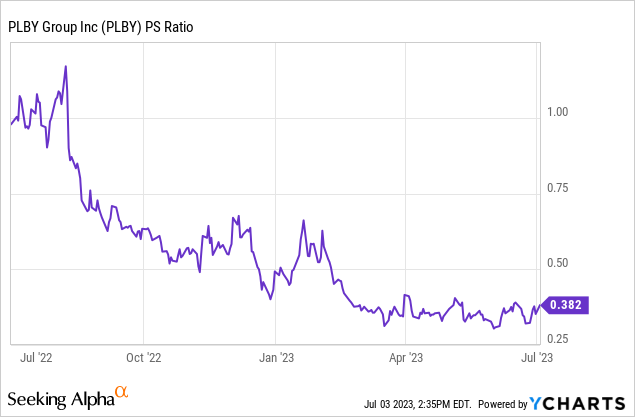

The commons are currently swapping hands at a 0.38x price-to-sales multiple, down from just over 1x a year ago. To be clear here, every $1 of revenue earned by PLBY got converted into around $1.15 of market cap this time last year, this is now being converted into around $0.38 of market cap. Why? Market confidence has waned in the ability of the company to turn around flagging operations as net losses, dilution, and cash burn stack up. Bears, who form the 14.8% short interest, have flagged a brand far past its peak where diminishing sales have become the consequence of a string of rag-tag acquisitions that are now being divested below cost.

The Yandy Sale Comes In Below Acquisition Price

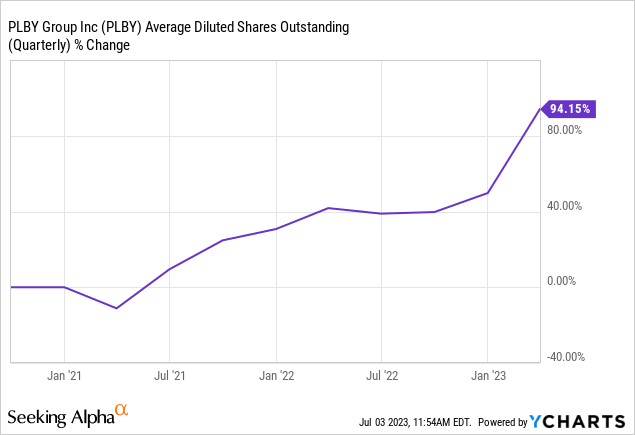

PLBY closed its pre-announced sale of Yandy in early April for $3 million. The lingerie and swimwear brand was acquired by PLBY for $13.1 million in 2019. Hence, the company has realized a roughly $10.1 million loss or around 77% on their Yandy purchase price since 2019. It’s hard to square up with this loss, especially against their cash needs. Bears would be right to highlight that this likely underscores a level of desperation by PLBY. Indeed, the company has had to ramp up its shares outstanding by 94% over the last 3 years to meet its liquidity needs and now tethers on trading below Nasdaq’s $1 minimum listing requirement.

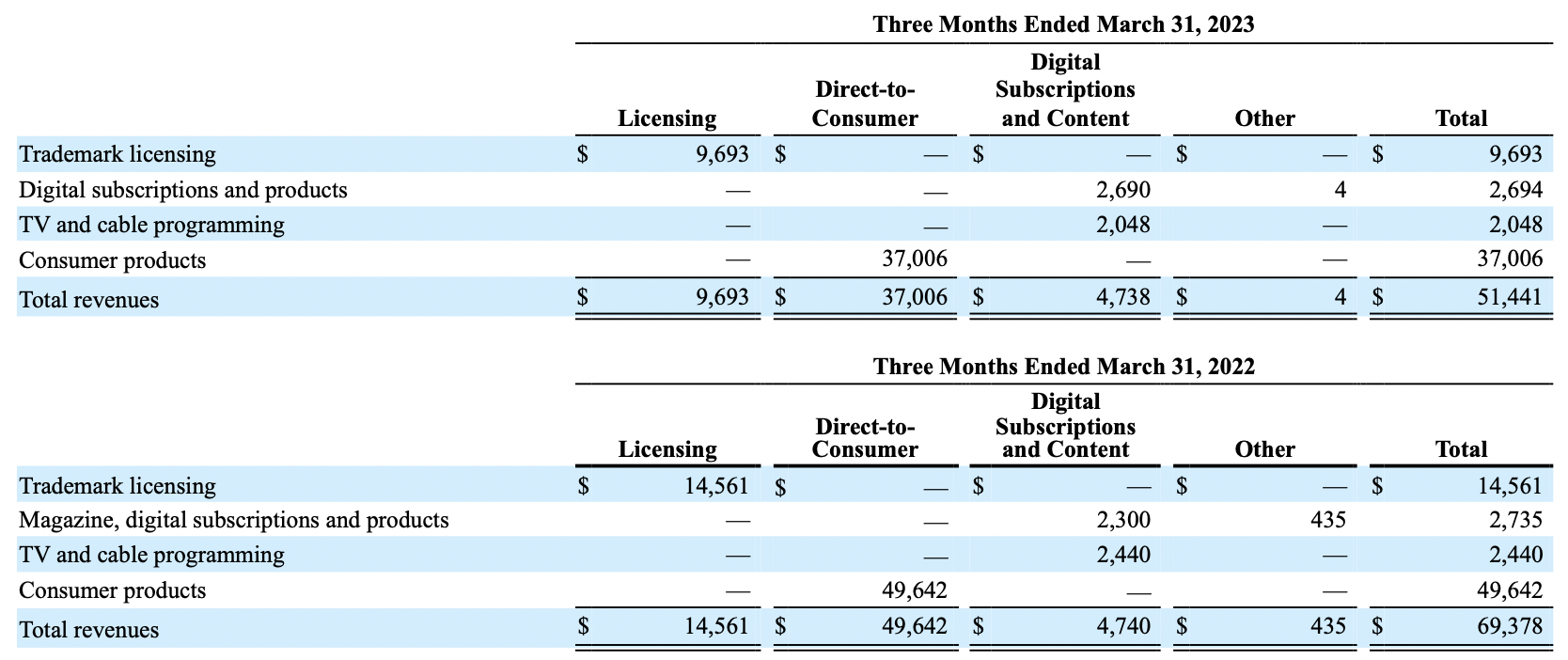

PLBY reported first-quarter revenue of $51.44 million, a 25.9% decline over its year-ago quarter and a miss by $5.04 million on consensus estimates. The drop was led by a broad decline across PLBY’s three operating segments. Licensing revenue of $9.69 million declined by $4.87 million over its year-ago comp with direct-to-consumer sales falling by $12.6 million year-over-year. However, perhaps the most confusing performance was actually digital subscriptions and content which essentially flatlined year-over-year.

PLBY Group Fiscal 2023 First Quarter Form 10-Q

This houses their creator platform, the engine of their growth and a core part of their long-term bullish story. Management flagged during their first-quarter earnings call that gross merchandise value for the first quarter increased by 2.4x over the fourth quarter. The company also flagged that weekly GMV has grown by a further 70% since the end of the period to early May when they published the first quarter earnings.

Rebuilding PLBY’s Cost Infrastructure

PLBY Group Fiscal 2023 First Quarter Form 10-Q

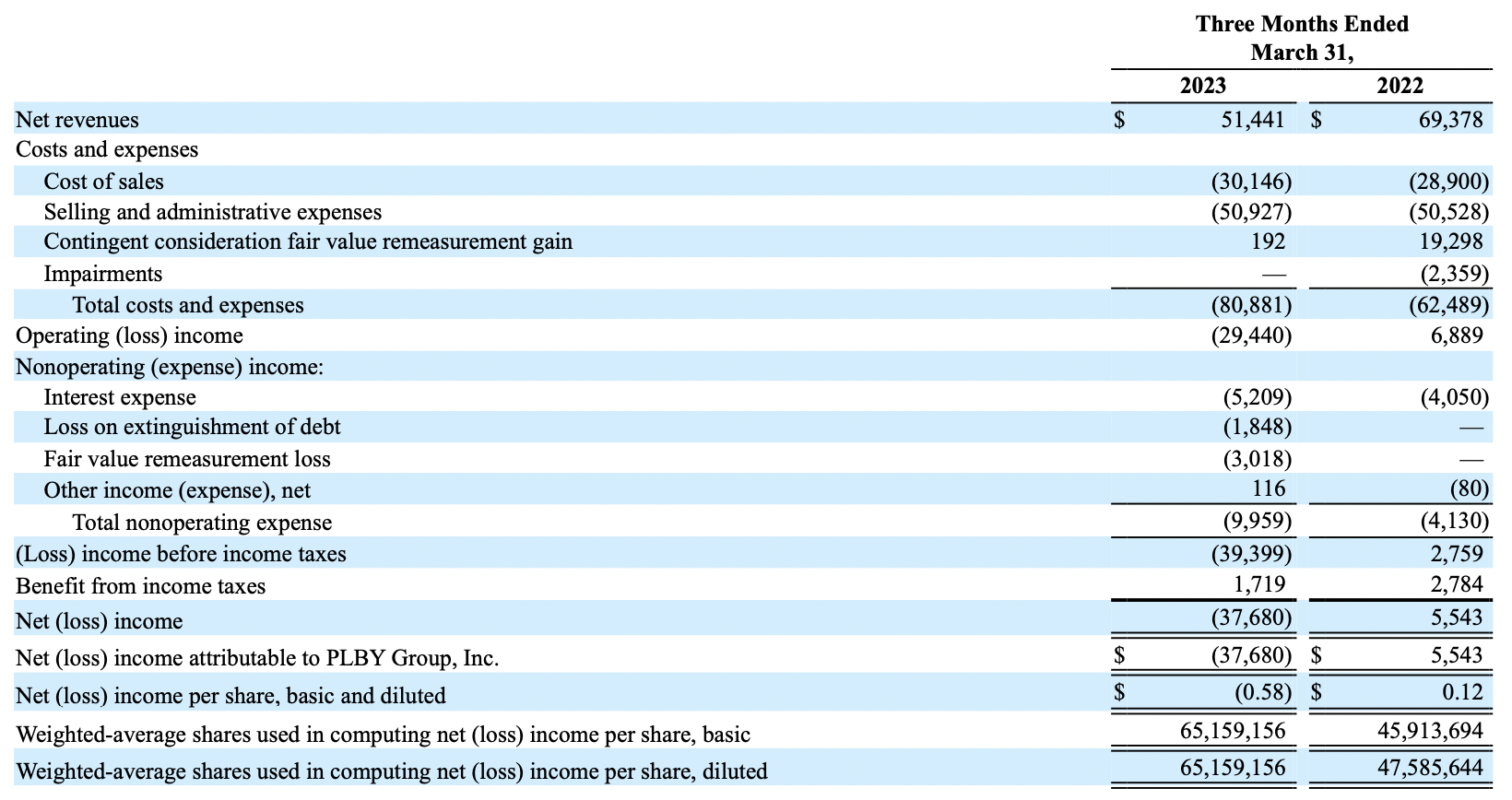

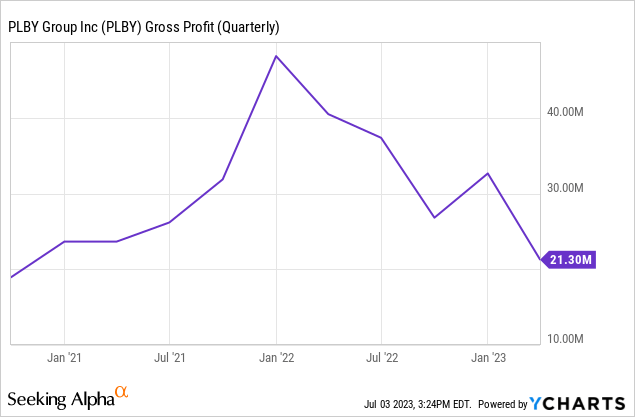

If we look through PLBY’s first quarter Form 10-Q we see that the fall in revenue was not followed by a proportional decline in cost of sales. COS actually increased by 4.3% year-over-year which meant a significant contraction in gross profit margins. This was 41.4% during the first quarter, a decline of roughly 1700 basis points over a gross profit margin of 58.34% in its year-ago comp and a further 625 basis points quarter-over-quarter decline.

Hence, PLBY’s first-quarter net loss at $37.68 million was a material deterioration from a $5.54 million profit in the year-ago comp. Keep in mind the company was highly dependent on selling new shares to fund its losses against a gross debt outstanding of $210 million as of the end of the first quarter. PLBY also stated its cash balance post-period end stands at around $35 million following a discount on debt from a lender made available as cash. Critically, the company is guiding for an improvement in its free cash flow as it fully exits operating its consumer product businesses to focus on its creator platform and licensing segments.

PLBY has already signed a term sheet to outsource its Playboy e-commerce business to a third party and is still exploring its options to offload other non-core assets, Lovers and Honey Birdette, for further debt reduction. If we assume a 50% reduction in free cash outflows through 2023 from the first quarter, the company is likely set to lose a further $35 million. This would fully consume its current cash position to mean a cash runway of just three quarters. Hence, the dilution is set to continue and I think this will further weigh down on the commons.

Be the first to comment