Justin Sullivan/Getty Images News

When Pinterest (NYSE:PINS) reported Q4 earnings on Monday there were several important announcements including a $500M buyback, lower than expected revenue growth and a CFO leaving to “pursue new career opportunities” in July.

Overall, the Q4 was nothing to celebrate for investors. Revenues did grow 4% and CEO Bill Ready pointed out on the conference call that Pinterest is “actually outperforming compared to a lot of our peers”.

| Q4 Revenue Growth | FWD P/S | |

| Pins | +4% | 5.8x |

| Meta | -4.5% | 3.95x |

| +1% | 4.53x | |

| Snap | Flat | 3.68x |

| Microsoft | 10%* | 9.2x |

| Amazon | 19%* | 1.89x |

Source: Company Press Releases & Seeking Alpha*Just the advertising businesses

Yes, the 4% Q4 revenue growth outpaced the “pure play” online advertising peers like Meta (META), Google (GOOG) (GOOGL), and Snap (SNAP). However, other segments of the online advertising market are growing faster given the segment results we saw from Amazon (AMZN) and Microsoft (MSFT) in the quarter.

More importantly, the 4% “outperformance” from Pinterest should, in some ways, be implied given the premium Price-to-Sales Pinterest stock enjoys over its peers, let alone the 36x investors are paying for 2023 earnings. In comparison Google and Meta are around 20x.

Ignore the fact that Google and Meta also enjoy a slightly more diversified revenue stream, a larger moat, billions of users and Pinterest’s stock still appears to be overvalued.

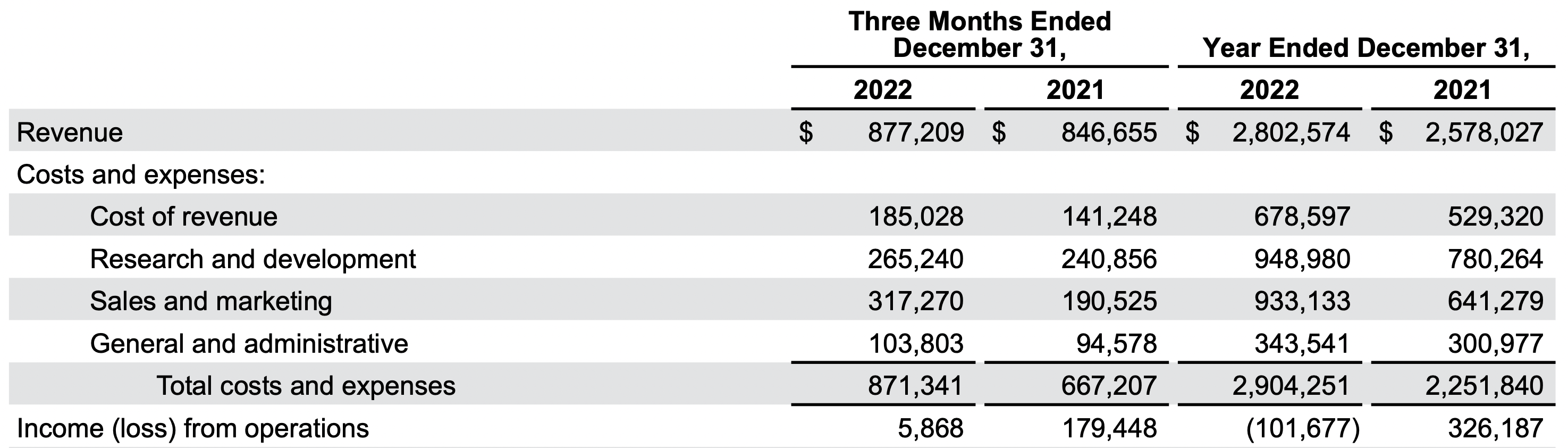

More alarming are the deteriorating financials at Pinterest. The company was once solidly profitable from a GAAP operating and net income basis, both turned negative over the past 12 months.

Pinterest Q4 Press Release

Equally alarming is the fact that while revenues did grow in the most recent quarter 4% – sales and marketing spend grew 66%.

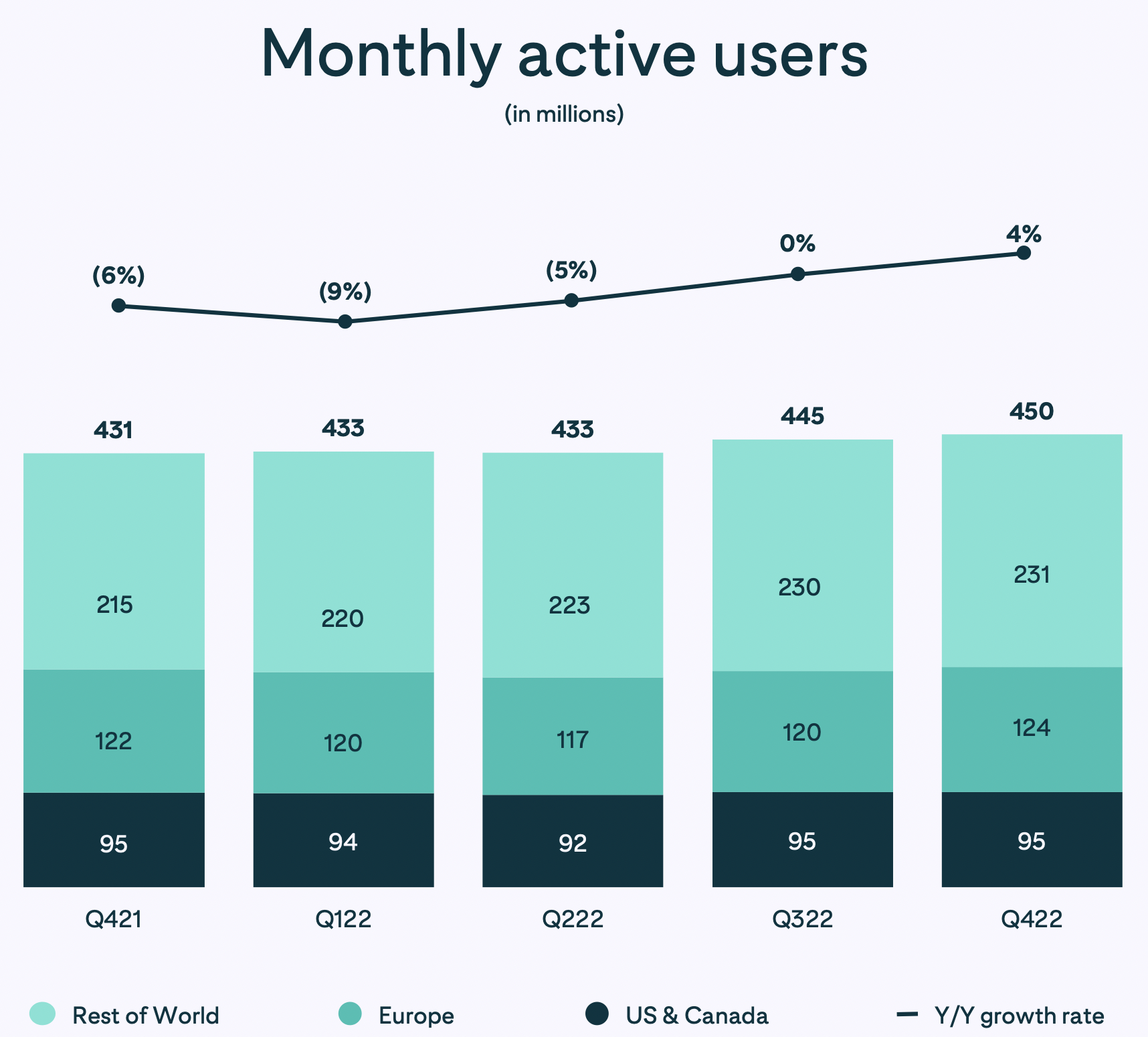

Management did indicate this marketing spend was somewhat one-off branding that likely did more to drive user growth rather than revenue growth, but even monthly active users grew just 4%.

Pinterest Q4 Slide Deck

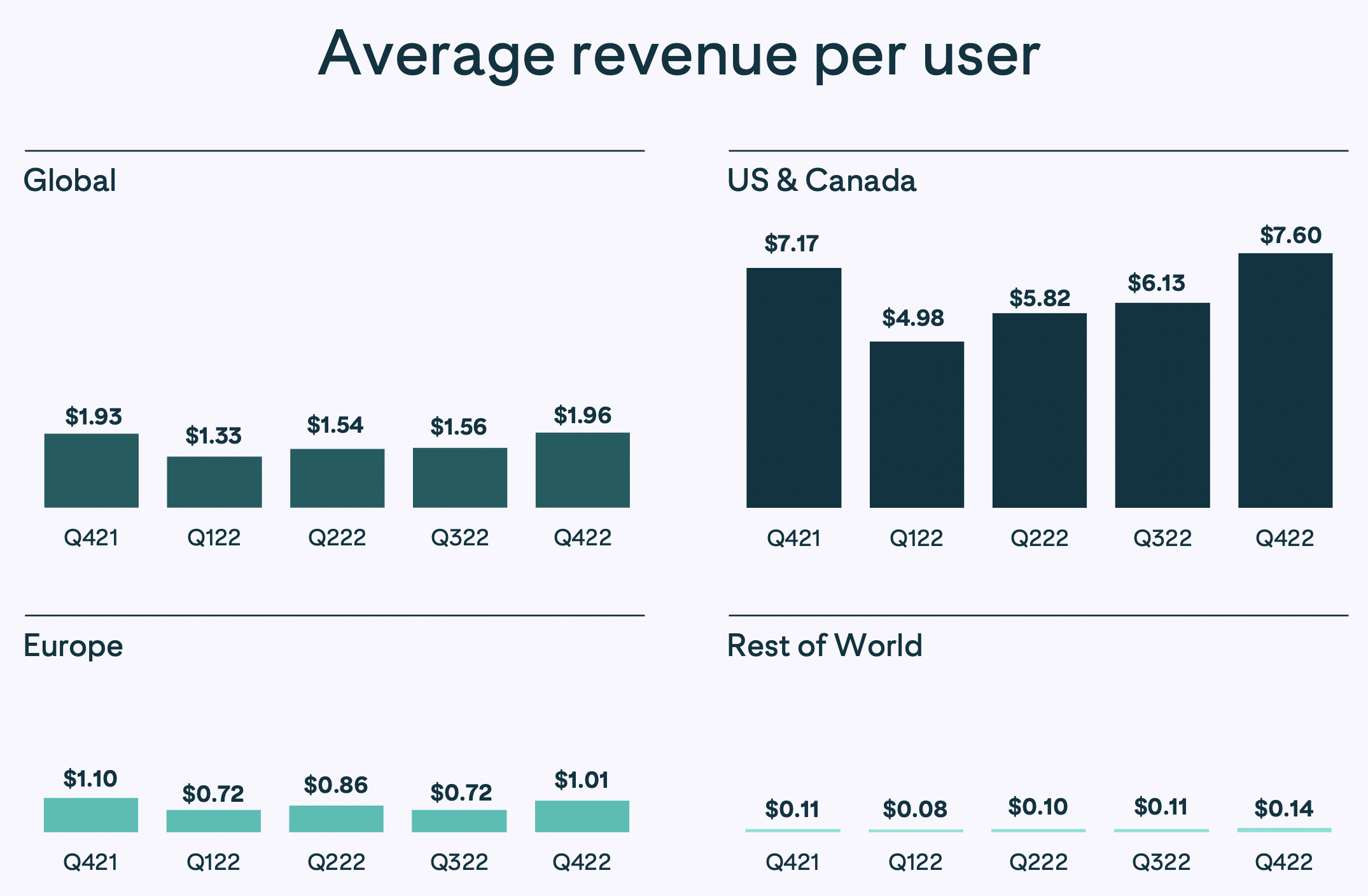

Note that the US and Canada market is flat Y/Y and Europe is largely flat, so almost all of Pinterest growth came from Rest of World which has a paltry $0.14 Average Revenue Per User (ARPU) metric compared to $7.60 for the US and Canada.

Pinterest Q4 Slide Deck

That means the company spent 66% more on marketing in the quarter to drive growth in the least profitable region from an ARPU perspective.

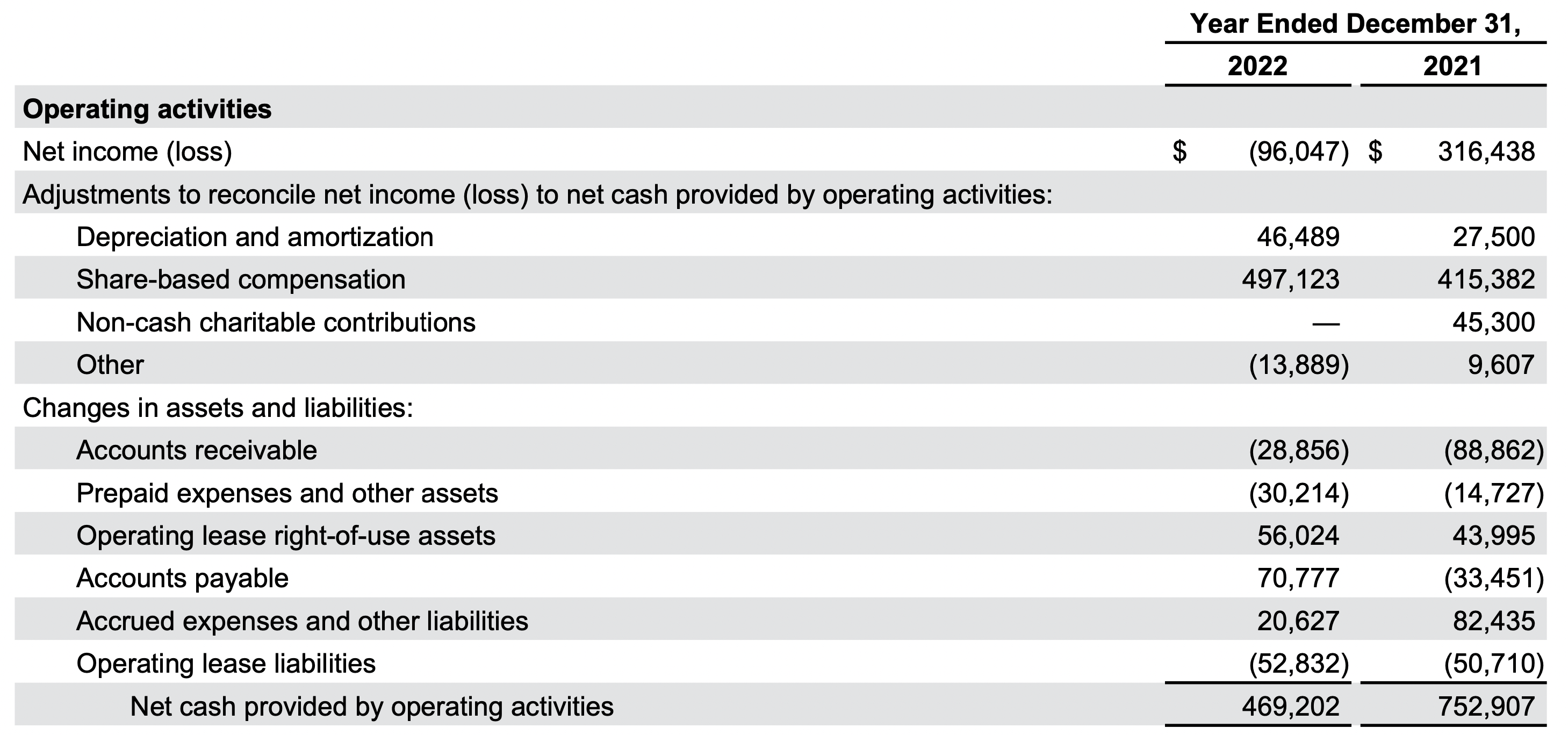

Many investors will ignore some of the disappointing user metrics and rightly point to operating cash flows.

Pinterest Q4 Operating Cash Flow

Yes, the nearly $470M in operating cash flow for 2022 is impressive, but it is down 37% from a year ago on higher revenue. Additionally the nearly $500M in stock based compensation added back skews the number higher.

I didn’t see a ton of investors overly excited about the $500M buy-back announcement from Pinterest, likely because it simply would offset some of the stock based compensation.

Looking ahead, the company guided Q1 for low single-digit growth which we assume is towards the low-end of estimates on Wall Street which before the Q4 announcement came in around 7% growth.

Somehow magically Pinterest is expected to re-accelerate revenue growth in Q2 to 11%, and Q3/Q4 to over 14%. Meanwhile, Meta, Snap and Google are expected to grow in the high single digits at best.

That likely means either Pinterest revenue estimates are too high and will be revised downward, or Meta, Snap and Google will have a solid chance at outperforming expectations the rest of the year trading at a lower sales multiple than Pinterest.

Conclusion

Pinterest spent heavily on marketing in Q4 and it barely moved the needle. The company already traded at a premium to Google and Meta, two companies with larger moats, user bases, diversified business models and gigantic share buybacks that will meaningfully reduce share counts. Given the fact Pinterest shares have risen over 21% this year alone, investors should follow the CFO out the door and pursue other investment opportunities.

Be the first to comment